Emera Incorporated has announced (on May 31):

that it has completed its bought deal offering of 12,000,000 Cumulative Minimum Rate Reset First Preferred Shares, Series H at a price of $25.00 per share for aggregate gross proceeds of $300 million. The syndicate of underwriters was led by Scotiabank, CIBC Capital Markets, RBC Capital Markets and TD Securities Inc., as joint bookrunners, and also included BMO Capital Markets, National Bank Financial Inc., Industrial Alliance Securities Inc. and Raymond James Ltd. The net proceeds of the offering will be used for general corporate purposes.

EMA.PR.H is a FixedReset, 4.90%+254M490, announced May 17. It will be tracked by HIMIPref™ and has been assigned to the FixedReset subindex.

The issue traded 1,345,583 shares on its May 31 opening day in a range of 24.65-95 before closing at 24.88-92. Vital Statistics are:

| EMA.PR.H | FixedReset | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-05-31 Maturity Price : 23.11 Evaluated at bid price : 24.88 Bid-YTW : 4.85 % |

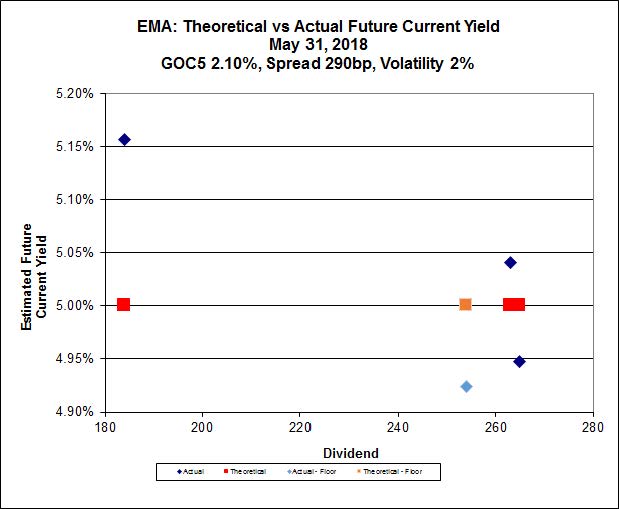

The new issue is somewhat expensive according to Implied Volatility Analysis:

Click for Big

According to the analysis above, the fair value is $24.50 … note, however, that complainers will triumphantly point out that this assigns a value of zero to the Floor Rate Guarantee. But as I stated in the February, 2018, edition of PrefLetter:

It is often asserted that a horrific fall of FixedReset prices is a completely logical expectation; that the 2014-16 bear market was completely justified; that similar experiences will happen again; and that floor rates are an excellent way to protect investors from the decline in income.

This assertion does not make a lot of sense to me. Suppose an investor holds a FixedReset with a coupon rate of 5% and that a decline in government yields makes a reduction to 4% seem both likely and imminent. If the bear market scenario is to play out, this investor and many like him will be selling to avoid experiencing the reset.

But where is this money to be deployed? Yields are already down in the government market and all other fixed income markets will be affected to some degree; corporate-government spreads increased during the recent episode (see Chart FR-63 ), but corporate yields did decline – they just didn’t decline as much. I see no reason for an expectation that FixedReset yields should magically remain constant if the face of global interest rate declines.

…

However, any increase in the price of the floor-rate issue is capped by the call price. In the simplest scenario, the non-floor issue will remain priced at par and reset to a 4% distribution, while the floored issue will be called; the investor will then have to reinvest his funds … and find that he is reinvesting at contemporary rates and experiencing transaction costs that are not borne by the investor in the non-floored issue. It’s not much of a win!In order for the floor rate to have value, both issues must be trading at a discount to par; this will give the floored issue room to rise in price on the secondary market. Such a price rise will be determined by the excess yield to be gained over the next five years until the next reset plus, perhaps, an allowance for the possibility that current conditions will persist and give the holder another chance to reset. The benefit will be capped by the distribution rate difference multiplied by the Modified Duration of the issues (which will normally be in the range of 20 to 25), so a price difference of between 20% and 25% for a one percent decline in government yields. However, this potential gain is capped by the potential for a call, so the issues must already be trading at a 20%-25% discount to par for this maximum to be reached … and to work out the value of this scenario, we must then calculate the probability of such a decline in government yields.

Once we see floor-rate issues trading at large discounts in an environment in which a significant decline in government rates has a reasonable probability, I will revisit my opinion of the value of such guarantees. I’m not holding my breath.

Now, against the above we have actual empirical data regarding the prices of the EMA FixedResets since the announcement date:

| Issue | Issue Reset Spread |

Total Return 5/17 – 5/31 |

| EMA.PR.A | 184 | +0.05% |

| EMA.PR.C | 265 | -2.76% |

| EMA.PR.F | 263 | -2.33% |

This has accompanied the fall in the GOC-5 yield from 2.33% on May 17 to 2.10% on May 31 (which, proponents will gleefully point out, has made the floor rate on the new issue a matter of great interest). For now, the situation remains murky.

However, even those unimpressed by all that “Implied Volatility” blather and tiresome pettifogging regarding Floor Guarantees should be, at the very least, tempted by EMA.PR.A in preference to the new issue. Sure, it only pays 2.555% at present … but it will reset on 2020-8-15 at GOC-5 + 184, or – given the May 31 GOC-5 yield of 2.10% – 3.94%. It was quoted May 31 at 19.10-31, an Expected Future Current Yield of 5.16%, which ain’t bad for investment grade!

Quick question-

Emera’s credit rating is BBB+ for its most secure debt.

Enbridge’s credit rating is A- to BBB+ for its most secure debt.

Yet, you call Emera’s issues as investment grade and Enbridge issues as junk.

Is there something basic I’m overlooking?

Thanks so much!

I classify Emera as Investment Grade on the basis of it S&P rating (for preferreds) of P-2(low). Emera does not have a DBRS rating.

The Enbridge preferred rating is P-2(low) at S&P but only Pfd-3(high) at DBRS. I use DBRS ratings for classification, when they exist.

Thanks much for the clarification! Really appreciate it.

Seems like they’ll be extending this issue.

https://investors.emera.com/news/news-details/2023/Emera-Incorporated-Announces-Conversion-Privilege-of-Cumulative-Minimum-Rate-Reset-First-Preferred-Shares-Series-H/default.aspx

Rate to be announced next week. Assuming around 3.75, this would reset at about 6.3, for a yield of about 7.5% at current prices. Not bad.

Hi Skeptical, why 3.75% for the 5yr GOC? Today it closed at 3.94% (using this

https://ca.investing.com/rates-bonds/canada-5-year-bond-yield )

BoC will hike for sure on Wed, do you expect something dovish from their commentary? I think rates will move higher post BoC meeting (as I think they continue promoting the notion of rates higher for longer than bonds are pricing in, so I think that we see a yield of north of 8% (based on the $20.81 last price). I think that I have a 50-50 shot at being right 🙂

Also resetting the same day is EMA.PR.C.

https://investors.emera.com/news/news-details/2023/Emera-Incorporated-Announces-Conversion-Privilege-of-Cumulative-Rate-Reset-First-Preferred-Shares-Series-C/default.aspx

Similar reset rate to “H” but no floor. I have noticed that the previous large premium that “H” traded at compared to “C” has narrowed quite a lot recently.

Just trying to be very conservative in my assumptions. It’s possible that the rates go up more from here and could stay above 4%.

If there’s a basic change in psychology that low rates are gone for good, we will see similar repricing. Ppl issues are acting the same.

I have a feeling that the complacency of the bond market needs to be tested before that scenario unfolds. The governments need to be reckless for some more time before we have higher for longer. And they are working hard towards that goal.

[…] is a FixedReset, 4.90%+254M490, that commenced trading 2018-5-31 after being announced 2018-5-17. It is tracked by HIMIPref™ but has been relegated to the Scraps […]

Hi, I’m new to this forum. Iv been searching for people trading pref share for a while.

I have been looking at the EMA pref resetting soon (C and H). Assuming a reset at 3.76%-4%, the C would give a 7.9-8.18% yield. To me there is an arbitrage there as the fixed gives 6.6-6.73% and all the other reset ranges from 4-6.16%.

The closest one to reset after is the A in aug 2025. Going from here, either all the other reset will go down in price to match the C and H yield, or the C and H will go up in price to get closer to the other one’s yield.

Am I missing something?

Cheers

Brassens, i suggest you get James’ newsletter for a few months. there is a lot of info every month that he provides. not least of which are the tables of all the prefs. if you’re new to prefs, you might also want to look into his videos (https://www.prefletter.com/eMailVerification.php?path=vid)

[…] is a FixedReset, 4.90%+254M490, that commenced trading 2018-5-31 after being announced 2018-5-17. Notice of extension was provided in 2023. It is tracked by […]