How ’bout them mutual funds, eh?

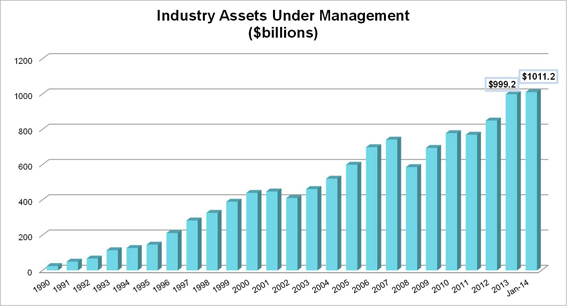

Canadians have accumulated savings of one trillion dollars in mutual funds – marking the first time in their 82-year history in Canada that funds have topped this significant milestone. As reported today by The Investment Funds Institute of Canada (IFIC), assets under management (AUM) for the mutual funds industry reached $1.01 trillion as of January 31, 2014, an increase of $140.1 billion or 16.1% over the previous 12 months.

Click for Big

DBRS confirmed NSI.PR.D at Pfd-2(low):

The rating assumes that the Company will continue to manage its annual dividend payout to maintain its regulated capital structure. While capital expenditures (capex) are expected to remain elevated ($283 million announced for 2014), operating cash flow is estimated to be adequate to support capex. DBRS expects that the residual operating cash flow after capex, combined with the incremental debt to maintain the regulatory capital structure, will be distributed to NSPI’s parent company, Emera Inc. (Emera; rated BBB (high), Under Review with Developing Implications). DBRS will continue to view NSPI on a stand-alone basis, assuming the Company adheres to the current flexible dividend distribution strategy.

It was another positive day for the Canadian preferred share market, with PerpetualDiscounts up 13bp, FixedResets gaining 5bp and DeemedRetractibles winning 14bp. Volatility was virtually non-existent. Volume was average.

PerpetualDiscounts now yield 5.60%, equivalent to 7.28% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.6%, so the pre-tax interest-equivalent spread (in this context, the Seniority Spread) is now about 270bp, unchanged from the February 12 report.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.6848 % | 2,399.2 |

| FixedFloater | 4.75 % | 4.34 % | 30,588 | 17.74 | 1 | 0.2506 % | 3,572.8 |

| Floater | 3.02 % | 3.11 % | 53,969 | 19.40 | 4 | -0.6848 % | 2,590.5 |

| OpRet | 4.61 % | -0.16 % | 68,681 | 0.28 | 3 | 0.0000 % | 2,687.8 |

| SplitShare | 4.89 % | 4.78 % | 59,693 | 4.37 | 5 | 0.4330 % | 3,025.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,457.7 |

| Perpetual-Premium | 5.67 % | 2.70 % | 100,087 | 0.08 | 12 | -0.0050 % | 2,335.3 |

| Perpetual-Discount | 5.54 % | 5.60 % | 150,268 | 14.45 | 26 | 0.1272 % | 2,392.4 |

| FixedReset | 4.85 % | 3.70 % | 209,977 | 6.88 | 80 | 0.0462 % | 2,492.1 |

| Deemed-Retractible | 5.10 % | 3.91 % | 164,648 | 1.69 | 42 | 0.1363 % | 2,430.1 |

| FloatingReset | 2.65 % | 2.64 % | 161,713 | 7.15 | 6 | 0.0872 % | 2,440.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.A | Floater | -2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-02-19 Maturity Price : 18.85 Evaluated at bid price : 18.85 Bid-YTW : 2.80 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.L | FixedReset | 153,971 | Will reset at 4.26%. Yield to Deemed Maturity 2021-1-31 is 3.81%. |

| MFC.PR.D | FixedReset | 116,460 | TD crossed 100,000 at 25.62. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-06-19 Maturity Price : 25.00 Evaluated at bid price : 25.62 Bid-YTW : 2.51 % |

| CM.PR.L | FixedReset | 71,662 | RBC crossed blocks of 26,700 and 27,000, both at 25.28. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-04-30 Maturity Price : 25.00 Evaluated at bid price : 25.29 Bid-YTW : 2.29 % |

| RY.PR.Z | FixedReset | 67,778 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-02-19 Maturity Price : 23.21 Evaluated at bid price : 25.20 Bid-YTW : 3.75 % |

| SLF.PR.F | FixedReset | 63,681 | TD crossed 50,000 at 25.54. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.54 Bid-YTW : 2.26 % |

| NA.PR.S | FixedReset | 54,674 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-02-19 Maturity Price : 23.18 Evaluated at bid price : 25.10 Bid-YTW : 3.94 % |

| There were 30 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.A | Floater | Quote: 18.85 – 19.40 Spot Rate : 0.5500 Average : 0.3774 YTW SCENARIO |

| BAM.PR.G | FixedFloater | Quote: 20.00 – 20.47 Spot Rate : 0.4700 Average : 0.3333 YTW SCENARIO |

| FTS.PR.H | FixedReset | Quote: 21.06 – 21.39 Spot Rate : 0.3300 Average : 0.2240 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 24.16 – 24.47 Spot Rate : 0.3100 Average : 0.2195 YTW SCENARIO |

| BAM.PF.B | FixedReset | Quote: 24.80 – 25.08 Spot Rate : 0.2800 Average : 0.1996 YTW SCENARIO |

| IGM.PR.B | Perpetual-Premium | Quote: 25.64 – 25.89 Spot Rate : 0.2500 Average : 0.1785 YTW SCENARIO |