The FOMC release was equivocal:

Growth in household spending has been moderate and the housing sector has shown additional improvement; however, business fixed investment and net exports stayed soft. The labor market continued to improve, with solid job gains and declining unemployment. On balance, a range of labor market indicators suggests that underutilization of labor resources has diminished since early this year. Inflation continued to run below the Committee’s longer-run objective, partly reflecting earlier declines in energy prices and decreasing prices of non-energy imports. Market-based measures of inflation compensation remain low; survey‑based measures of longer-term inflation expectations have remained stable.

…

The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced. Inflation is anticipated to remain near its recent low level in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of earlier declines in energy and import prices dissipate.

…

The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen some further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

There was no dissent.

Treasuries eased slightly on the news, but nothing special:

The 10-year note yield rose three basis points, or 0.03 percentage point, to 2.28 percent at 3:04 p.m. in New York, according to Bloomberg Bond Trader data. The benchmark 2.125 percent security due in May 2025 fell 7/32, or $2.19 per $1,000 face amount, to 98 21/32. The yield climbed three basis points on Tuesday.

…

Traders are pricing in a 39 percent probability that the Fed raises rates at or before the September meeting, based on the assumption that the effective fed funds rate will average 0.375 percent after liftoff. That compared with a 40 percent probability before the Fed announcement.The likelihood of a December rate increase was 71 percent, compared with 70 percent.

Meanwhile, Joe Oliver showed who’s boss at the Bank of Canada:

Last week, while addressing questions about Canada’s fragile economy, federal Finance Minister Joe Oliver was asked whether the Bank of Canada should consider using “quantitative easing” to stimulate Canada’s economy. He responded immediately, saying it’s “not on the table.” But whatever the case for the use of this approach to monetary policy, Mr. Oliver should know better than to speak about something clearly outside his purview.

…

Mr. Oliver can play his best role in this complex debate by staying out of it altogether.The federal government is the sole shareholder of the Bank of Canada, whose governor is accountable to the finance minister and, through him or her, to Parliament.

But the Bank of Canada is also “operationally independent” from the federal government, and this independence is crucial to the bank’s long-term success in maintaining low and stable inflation.

Over many years and across many countries, evidence clearly shows that when elected governments get too involved in the operational details of monetary policy, inflation rises and becomes more volatile.

Mr. Oliver should be talking a lot about the current weakness of the Canadian economy, and also about what he is prepared to do – with fiscal policy – to make the situation better for Canadians. But when he faces questions about monetary policy, he should defer to the bank’s governor. To do anything else is to undermine the bank’s ability to make monetary policy in the best interests of the country.

Trouble is, the BoC is no longer “operationally independent”. That went out the window with Dodge, Chretien and Turner.

There’s some interesting discussion of bond liquidity today … fund managers are holding cash, which is market timing:

Western Asset Management Co., which oversees about $455 billion, has developed a system of ranking securities based on their perceived liquidity to make sure they’ve got plenty of easy-to-sell assets in a pinch. Loomis Sayles & Co. is “comfortable holding higher-than-average reserves, such as cash and high-quality developed market sovereign debt,” according to a report this month.

For funds that are loaded up with hard-to-trade bonds, “it could be a challenge under difficult market conditions to meet very large redemptions” without suffering huge losses, according to Michael Buchanan, Western Asset’s deputy chief investment officer, in a July 20 paper. “Overall the trend is that liquidity will continue to decline.”

…

The silver lining is that these measures taken by investors may end up reducing the risk of a market seizure, both because banks are safer and investors are more prepared. Both Western Asset and Loomis Sayles are planning for a dislocation in which they can be on the other side of the trade, buying bonds in the case of a forced sale.

In the July 20th interview – not a paper, as far as I can tell – Mr. Buchanan says:

Proprietary trading and hedge funds were active participants in the trading of fixed-income markets. By closing these lines of business, the regulation reduced the number of players bidding and offering securities on a daily basis, making periods of heightened volatility more violent from a mark-to-market perspective. Market regulatory modifications include a proposal by the European Commission to implement a tax of 1–10 basis points (bps) on transactions in all classes of fixed-income instruments. If finalized as proposed, it would clearly act as yet another disincentive for market-makers to commit capital to the investment community, further reducing liquidity in the market.

…

Maintaining portfolio liquidity for mutual funds is of significant importance, and as such, we have been increasing the use of instruments such as cash, T-Bills, ETFs and derivatives to provide additional liquidity. Across all vehicles, we are utilizing the primary market more frequently as new issues price, more often than not, at large concessions to secondary issues, and the new issues actively trade with minimal bid/offer spreads. We are also employing derivatives via indices/tranches that provide a liquidity enhancement while maintaining exposure to the given asset class. In those cases when we consider an issue for investment, we often value the on-the-run investment opportunity more than an off-the-run opportunity on a relative value basis.

…

The biggest reduction in liquidity has been experienced by off-the-run issues in the credit market and non-current coupon bonds in the MBS market. For example, an off-the-run issue on a 10-year bond for an investment-grade issuer trades at a 10–20 bps discount to that issuer’s on-the-run issue, versus a 5–10 bps discount that was available pre-crisis.

And Matt Levine contributes some information in his usual entertaining style:

One potential solution for that problem is to have investors just trade bonds with each other, cutting out the banks as middlemen. But it turns out that doesn’t work very well, in part because investors don’t know how much bonds are supposed to cost, and need banks to tell them:

Many bonds don’t trade for weeks or months, leaving gaps in pricing that historically were filled by banks that had more market information at their command than their customers.

On Bondcube, which announced its closure on July 22, investors who found each other on the company’s system often couldn’t agree on a price, according to a person familiar with the matter, who asked not to be identified because the information isn’t public. So bids and offers were too far apart.

Oops.

…

Bondcube is also a nice little lens through which to look at the felony fraud charges against the mortgage traders — Jesse Litvak, Matthew Katke and potentially others — accused of lying about this sort of price information. I find these cases very confusing, because these guys didn’t lie about any fundamental facts of the bonds they were selling. They never fudged cash-flow statements or bribed home appraisers or anything like that. Instead they (allegedly) just told customers that they’d paid 58 cents on the dollar for a bond, when really they’d paid 57, and pocketed the difference. That seems clearly irrelevant to a sophisticated investor’s view of value, and so arguably not material: If the investor thought the bond was worth 59, and paid 58.25 for it, then why does it matter that the dealer bought it for 57 instead of 58?

…

Of course you could still make a go of it. That’s sort of the point of Ken Griffin’s op-ed from the other day, arguing that “recent reforms and regulatory pressures have dramatically increased the number of participants who can make prices and provide liquidity across many fixed-income markets.” The bio on that piece says that “Mr. Griffin is the founder and CEO of Citadel LLC, a hedge-fund manager and securities dealer,” and I suspect there was a time when it would have left off the “securities dealer” part. But Citadel realized that when banks won’t make markets, somebody has to, and it might as well be Citadel.

Tragically, Mr. Levine let a shibboleth go by unchallenged:

But one of the most popular solutions for bond-market illiquidity, urged by BlackRock and others, is more electronic trading of bonds. At best, electronic venues would aggregate price and order information in a way that increases price discovery and liquidity. Or they might just lead to a bunch of investors twiddling their thumbs and wishing there were some dealers to make markets.

Sadly, electronic trading of bonds (of anything, in fact) harms liquidity. It’s been proven over and over again.

It was another poor day for the Canadian preferred shares market, with PerpetualDiscounts losing 25bp, FixedResets off 6bp and DeemedRetractibles down 10bp. The Performance Highlights table is lengthy but balanced. Volume was average.

PerpetualDiscounts now yield 5.34%, equivalent to 6.94% at the standard equivalency factor of 1.3x. Long corporates now yield about 4.0%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 295bp, somewhat wider than the 285bp reported July 22.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

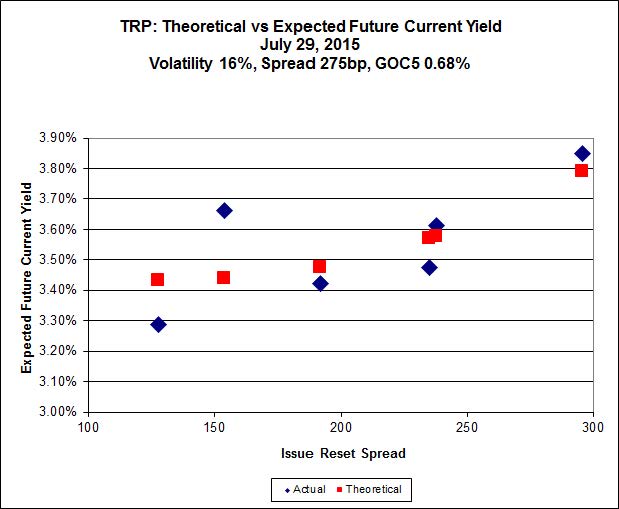

Here’s TRP:

Click for Big

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 14.90 to be $0.62 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.99 cheap at its bid price of 15.20.

Click for Big

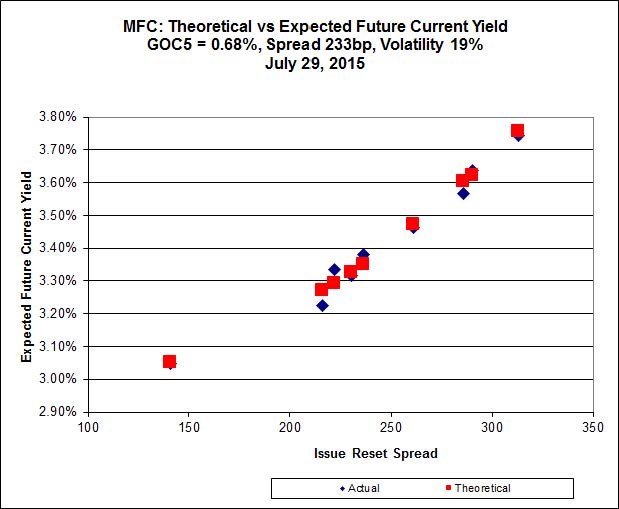

Another good fit today!

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 22.02 to be 0.30 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 21.75 to be $0.28 cheap.

Click for Big

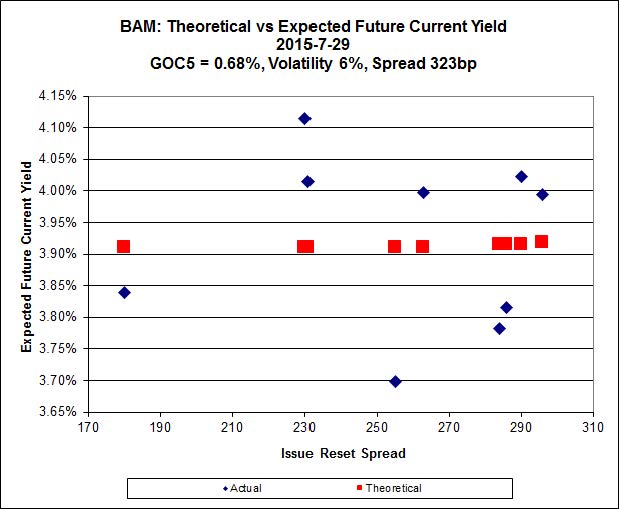

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 18.11 to be $0.94 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 21.83 and appears to be $1.18 rich.

Click for Big

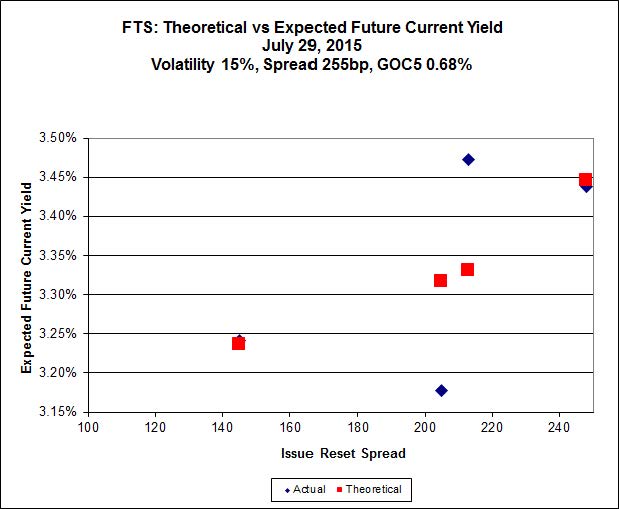

FTS.PR.K, with a spread of +205bp, and bid at 21.48, looks $0.90 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 20.23 and is $0.86 cheap.

Click for Big

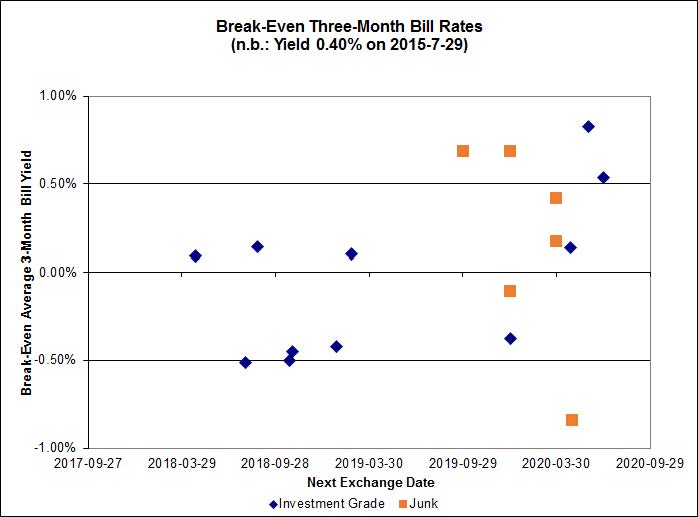

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of +0.08%, with one outlier above 1.00%. There are no junk outliers.

Click for Big

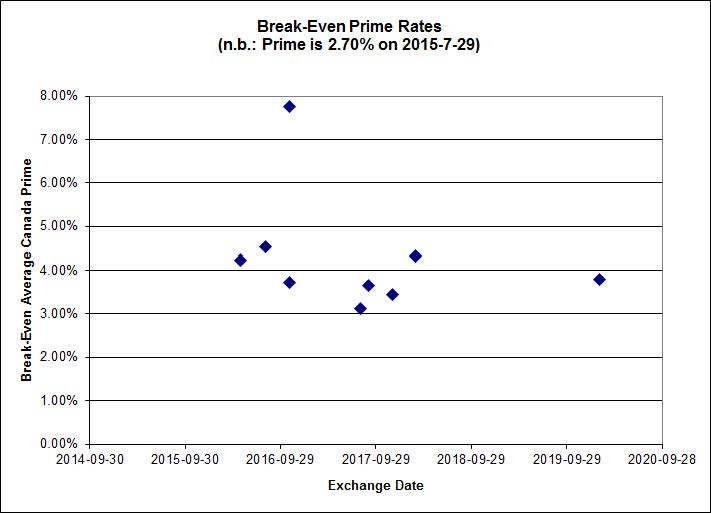

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3904 % | 2,129.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3904 % | 3,723.2 |

| Floater | 3.45 % | 3.45 % | 57,595 | 18.62 | 3 | 0.3904 % | 2,263.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1469 % | 2,785.2 |

| SplitShare | 4.57 % | 4.75 % | 62,512 | 3.17 | 3 | 0.1469 % | 3,264.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1469 % | 2,546.8 |

| Perpetual-Premium | 5.55 % | 4.96 % | 72,456 | 2.25 | 13 | -0.0950 % | 2,498.4 |

| Perpetual-Discount | 5.35 % | 5.34 % | 85,958 | 14.82 | 24 | -0.2536 % | 2,648.4 |

| FixedReset | 4.67 % | 3.76 % | 212,944 | 16.12 | 88 | -0.0562 % | 2,256.0 |

| Deemed-Retractible | 5.08 % | 5.18 % | 104,905 | 5.49 | 34 | -0.1014 % | 2,597.0 |

| FloatingReset | 2.39 % | 3.14 % | 43,477 | 6.06 | 10 | 0.2127 % | 2,277.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.X | FixedReset | -3.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 16.15 Evaluated at bid price : 16.15 Bid-YTW : 4.12 % |

| IAG.PR.A | Deemed-Retractible | -2.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.46 Bid-YTW : 6.11 % |

| TRP.PR.C | FixedReset | -2.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 15.15 Evaluated at bid price : 15.15 Bid-YTW : 3.65 % |

| BIP.PR.A | FixedReset | -2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 21.46 Evaluated at bid price : 21.75 Bid-YTW : 4.94 % |

| NA.PR.W | FixedReset | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 3.65 % |

| HSE.PR.G | FixedReset | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 22.13 Evaluated at bid price : 22.74 Bid-YTW : 4.71 % |

| BAM.PR.R | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 18.11 Evaluated at bid price : 18.11 Bid-YTW : 4.22 % |

| HSE.PR.C | FixedReset | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 21.49 Evaluated at bid price : 21.77 Bid-YTW : 4.55 % |

| BAM.PR.B | Floater | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 13.95 Evaluated at bid price : 13.95 Bid-YTW : 3.41 % |

| BAM.PF.E | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 21.53 Evaluated at bid price : 21.83 Bid-YTW : 3.99 % |

| SLF.PR.J | FloatingReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.25 Bid-YTW : 6.93 % |

| BAM.PF.A | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 21.92 Evaluated at bid price : 22.25 Bid-YTW : 4.15 % |

| FTS.PR.J | Perpetual-Discount | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 23.37 Evaluated at bid price : 23.75 Bid-YTW : 5.06 % |

| IFC.PR.A | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.30 Bid-YTW : 6.91 % |

| ENB.PF.C | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 4.80 % |

| ENB.PR.J | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 4.77 % |

| TD.PF.B | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 21.83 Evaluated at bid price : 22.20 Bid-YTW : 3.43 % |

| BMO.PR.S | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 22.08 Evaluated at bid price : 22.55 Bid-YTW : 3.44 % |

| ENB.PR.D | FixedReset | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 4.78 % |

| ENB.PR.N | FixedReset | 1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 17.70 Evaluated at bid price : 17.70 Bid-YTW : 4.89 % |

| ENB.PF.G | FixedReset | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 19.09 Evaluated at bid price : 19.09 Bid-YTW : 4.80 % |

| MFC.PR.F | FixedReset | 1.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.14 Bid-YTW : 6.89 % |

| TRP.PR.F | FloatingReset | 2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 3.36 % |

| IFC.PR.C | FixedReset | 2.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.30 Bid-YTW : 4.89 % |

| BAM.PR.C | Floater | 2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 13.41 Evaluated at bid price : 13.41 Bid-YTW : 3.55 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| ENB.PR.Y | FixedReset | 261,061 | TD traded two blocks of 123,000 shares each, both at 17.32. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 17.45 Evaluated at bid price : 17.45 Bid-YTW : 4.70 % |

| BMO.PR.Z | Perpetual-Discount | 96,035 | New issue settled today YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 23.67 Evaluated at bid price : 24.00 Bid-YTW : 5.22 % |

| RY.PR.F | Deemed-Retractible | 92,085 | RBC crossed blocks of 43,100 and 40,700, both at 24.96. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.00 Bid-YTW : 4.06 % |

| ENB.PF.C | FixedReset | 71,415 | RBC crossed 60,000 at 18.83. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 4.80 % |

| TRP.PR.C | FixedReset | 63,670 | Desjardins crossed 49,800 at 15.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 15.15 Evaluated at bid price : 15.15 Bid-YTW : 3.65 % |

| FTS.PR.H | FixedReset | 51,700 | TD crossed 50,000 at 16.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-29 Maturity Price : 16.43 Evaluated at bid price : 16.43 Bid-YTW : 3.34 % |

| There were 30 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.N | FixedReset | Quote: 16.24 – 16.81 Spot Rate : 0.5700 Average : 0.3261 YTW SCENARIO |

| POW.PR.G | Perpetual-Premium | Quote: 25.17 – 25.59 Spot Rate : 0.4200 Average : 0.2699 YTW SCENARIO |

| RY.PR.I | FixedReset | Quote: 24.68 – 25.10 Spot Rate : 0.4200 Average : 0.2766 YTW SCENARIO |

| GWO.PR.L | Deemed-Retractible | Quote: 25.31 – 25.79 Spot Rate : 0.4800 Average : 0.3390 YTW SCENARIO |

| BIP.PR.A | FixedReset | Quote: 21.75 – 22.25 Spot Rate : 0.5000 Average : 0.3622 YTW SCENARIO |

| CU.PR.E | Perpetual-Discount | Quote: 23.23 – 23.59 Spot Rate : 0.3600 Average : 0.2266 YTW SCENARIO |