Interesting story about the effects of mortgage rule changes in the UK – there are some who have borrowed on a floating rate mortgage. This carries a higher rate than a two-year mortgage – for reasons which I do not understand, since the Gilt curve is normal – and they want to switch, but are not allowed to do so because they no longer qualify for a fixed rate mortgage. They’re called mortgage prisoners:

The customer, who asked not to be named, had been stranded on Bank of Scotland’s standard variable rate (SVR) for over four years. He paid thousands of pounds a year in extra payments because the bank refused his requests to move to a cheaper, fixed-rate deal, and fell into arrears at some points.

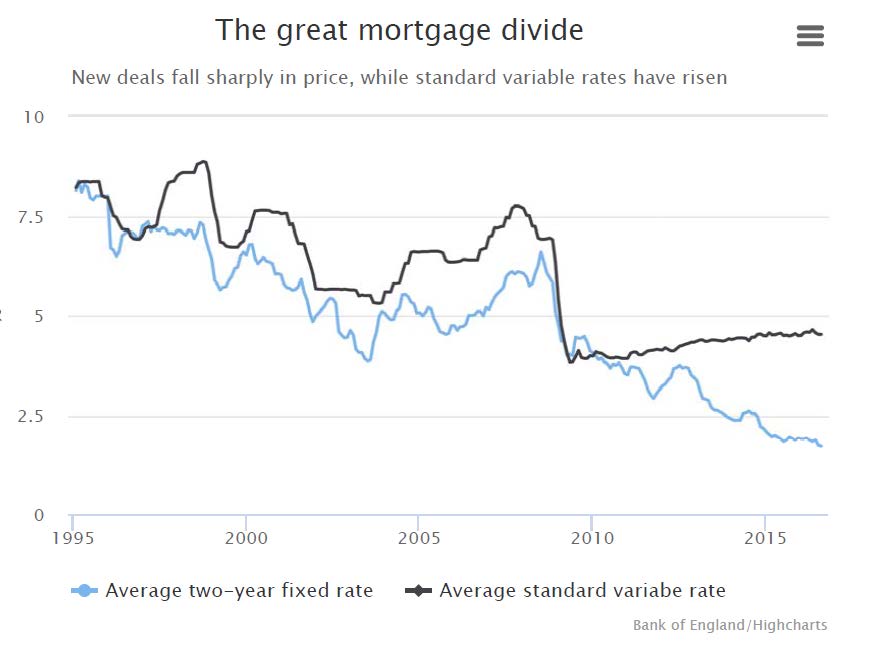

While fixed mortgage rates have fallen in line with the Bank of England base rate, lenders’ SVRs have remained flat or increased (see chart, below).

Thousands of people who took out mortgages before the financial crisis found they were barred from switching to new fixed-rate mortgages when existing deals ended.

Lenders said rules introduced following the crisis, known as the Mortgage Market Review, meant existing customers now failed stricter “affordability” tests. This led to the bizarre situation where customers, known as mortgage prisoners, were told they couldn’t afford to switch to cheaper rates.

Click for Big

I don’t understand why the inversion exists, given the current gilt curve:

Click for Big

But I have to say one thing … only an unholy alliance of bankers and regulators can produce the phrase ‘you can’t afford to halve your mortgage payments!’

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4636 % | 2,180.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4636 % | 4,001.3 |

| Floater | 3.49 % | 3.58 % | 40,754 | 18.36 | 4 | 0.4636 % | 2,306.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0196 % | 3,028.4 |

| SplitShare | 4.93 % | 4.21 % | 59,998 | 0.65 | 6 | 0.0196 % | 3,616.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0196 % | 2,821.8 |

| Perpetual-Premium | 5.27 % | -9.52 % | 72,786 | 0.09 | 23 | 0.0034 % | 2,793.0 |

| Perpetual-Discount | 5.06 % | 5.03 % | 115,688 | 15.36 | 13 | -0.1480 % | 3,009.0 |

| FixedReset | 4.33 % | 3.94 % | 242,964 | 6.66 | 94 | -0.0512 % | 2,386.9 |

| Deemed-Retractible | 4.97 % | 3.92 % | 143,887 | 0.12 | 31 | -0.1612 % | 2,900.8 |

| FloatingReset | 2.52 % | 3.10 % | 54,299 | 4.54 | 9 | 0.2562 % | 2,544.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.F | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.67 Bid-YTW : 9.15 % |

| MFC.PR.H | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.71 Bid-YTW : 4.47 % |

| BIP.PR.A | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-11 Maturity Price : 23.10 Evaluated at bid price : 24.35 Bid-YTW : 4.71 % |

| SLF.PR.J | FloatingReset | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.93 Bid-YTW : 8.42 % |

| BAM.PR.B | Floater | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-11 Maturity Price : 13.27 Evaluated at bid price : 13.27 Bid-YTW : 3.58 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PR.X | FixedReset | 143,727 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-11 Maturity Price : 17.44 Evaluated at bid price : 17.44 Bid-YTW : 4.19 % |

| SLF.PR.I | FixedReset | 122,659 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.57 Bid-YTW : 4.74 % |

| RY.PR.Z | FixedReset | 117,866 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-04-11 Maturity Price : 22.31 Evaluated at bid price : 22.60 Bid-YTW : 3.77 % |

| BNS.PR.B | FloatingReset | 106,500 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.16 Bid-YTW : 3.00 % |

| RY.PR.Q | FixedReset | 64,301 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 27.39 Bid-YTW : 3.21 % |

| TD.PF.H | FixedReset | 61,993 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 26.50 Bid-YTW : 3.38 % |

| There were 30 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.T | FixedReset | Quote: 23.10 – 23.44 Spot Rate : 0.3400 Average : 0.2477 YTW SCENARIO |

| PWF.PR.A | Floater | Quote: 14.62 – 14.90 Spot Rate : 0.2800 Average : 0.1999 YTW SCENARIO |

| BNS.PR.H | FixedReset | Quote: 26.45 – 26.66 Spot Rate : 0.2100 Average : 0.1306 YTW SCENARIO |

| MFC.PR.H | FixedReset | Quote: 24.71 – 24.92 Spot Rate : 0.2100 Average : 0.1318 YTW SCENARIO |

| IFC.PR.A | FixedReset | Quote: 18.98 – 19.24 Spot Rate : 0.2600 Average : 0.1830 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 15.67 – 15.88 Spot Rate : 0.2100 Average : 0.1459 YTW SCENARIO |