CU Inc. has announced:

that it will issue $580,000,000 of 2.963% Debentures maturing on September 7, 2049, at a price of $100.00 to yield 2.963%. This issue was sold by RBC Dominion Securities Inc., BMO Nesbitt Burns Inc., TD Securities Inc., Scotia Capital Inc., CIBC World Markets Inc. and MUFG Securities (Canada), Ltd. Proceeds from the issue will be used to finance capital expenditures, to repay existing indebtedness, and for other general corporate purposes.

CIU.PR.A, a Straight Perpetual, 4.60% that was announced 2007-4-3. Its credit quality with respect to the CIU corporate structure was discussed long ago.

CIU.PR.A closed 2019-9-3 at 20.91-53 to yield 5.54%-34. Call it a midpoint of 5.44%, and the interest equivalent of that with a conversion factor of 1.3x is 7.07%. Therefore, the Seniority Spread between this issue and the new bond is about 411bp, slightly but not significantly tighter than the 420bp reported for the more general measures of bond and preferred yields on August 28.

This follows my highlighting of the IGM.PR.B refunding on 2019-5-1 and the TRP long bond on 2019-4-10.

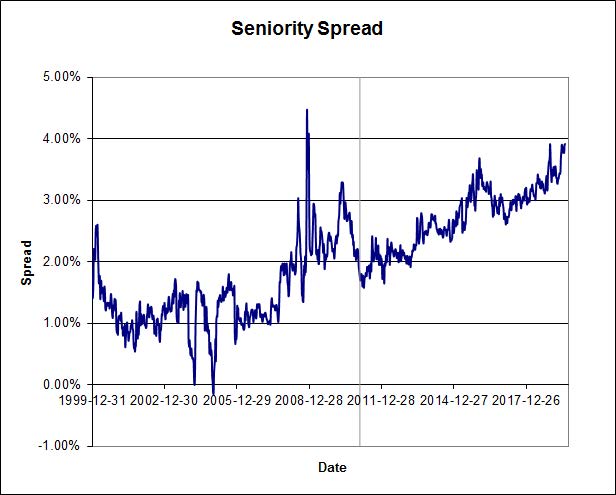

This data point supports the accuracy of the Seniority Spread calculated every Wednesday on PrefBlog, with long-term charts being published periodically, eg (chart end-date 2019-8-9):

Click for Big

It also highlights just how cheap Straight Preferreds are compared to long-term corporate bonds!

Holy smokes….what a yield for CU. Less than 3% for a 30 year bond! Wow.

I bet if rates fall further, credit like CU will fetch less than 2%. And then even these straight perpetuals yielding 4.5 to 4.6 are likely to get called sometime in the near future if this trend continues. Wow!

IMHO, perpetuals with coupons greater than 5% yield are most likely to get called as we witnessed with W.PR.J earlier this year.

Not a good sign for yield seekers that want less uncertainty of cash flows. At least, we’ll end up with a parting gift of capital gains!

So the first one to go away would be CU.PR.H that sports 5.25 but currently has to be bought at 26, I think. Over the next few years, this could change.

What will remain?

CIU.PR.C with a thin spread and similar issues.

I think perpetuals right now should have surged close to par for all good credit companies. I thank all the retail Canadian investors who piss on these instruments every day and give me an opportunity to meet my cash flow needs with little capital 🙂

“What will remain?”

If the seniority spread does not narrow, I suspect that the first thing to go (has already gone?) is new issuance (debt is way more attractive to issue than preferreds). Then NCIBs, SIBs and recalls will increase. Ultimately, as in any market, demand will finally exceed supply and the seniority spread will collapse to something more historically normal. This process does not need general calm and normality to return to global markets but that would certainly help.

I hope your both correct..

In the meantime, the companies can just purchase on the open market, saving themselves lots of cash (often at 1/2 of the issued price). However, I won’t sell at these prices….