The recent slide in PerpetualDiscounts has been particularly hard on insurers – and particularly the lower coupon issues in a continuation of the trend discussed in MAPF: February Performance.

In fact, implied volatility has gone negative:

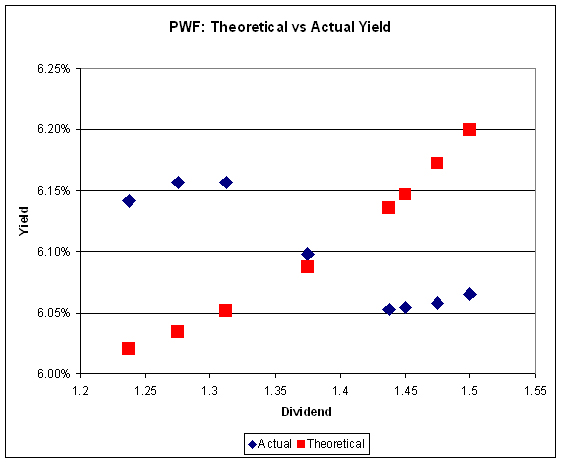

Click for Big

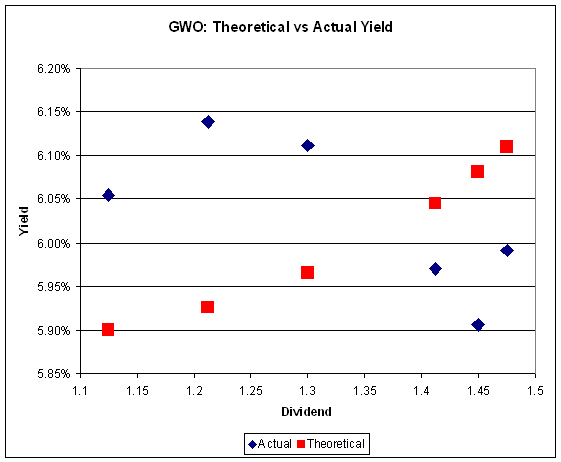

Click for Big

Both graphs have been prepared using the Straight Perpetual Implied Volatility Calculator and, for purposes of the theoretical curve, setting the implied volatility to 15% / 3 Years.

[…] time to time – in the spring of 2010, I noted that the relative prices for these two issues reflected negative Implied Volatility (which cannot actually be calculated because the math blows up). It happens. Sometimes, when the […]