The Bank of Canada rate cut is making a difference where it counts:

Bank of Montreal has renewed the mortgage war among Canada’s banks, slashing the posted rate on its five-year fixed mortgage to 2.79 per cent from 2.99 per cent, even as Ottawa and the International Monetary Fund fret over the state of Canada’s overheating housing market.

Toronto-Dominion Bank quickly rushed to match BMO’s rate special, saying it will drop its five-year fixed mortgage rate from 3.09 per cent to 2.79 starting Wednesday.

It hadn’t occurred to me that deferred prosecution settlements for criminal charges were actually bureaucratic job creation schemes, but that’s the way it is!

Deferred prosecution and non-prosecution agreements, as they are called, have been widely used by the Justice Department in recent years in investigations ranging from sanctions violations to market manipulation. A decision to revoke such a deal with a bank would be unprecedented.

Such settlements require the banks to admit responsibility and cooperate with ongoing investigations. Critics including Securities and Exchange Commission Chair Mary Jo White, who pioneered such agreements, argue the deals have been overused and don’t curb misconduct. The Justice Department defends the settlements, saying they force banks to correct wrongdoing and allow oversight.

There’s a fascinating article on Bloomberg about the mystic quality of private equity valuations:

For the most mature startups, investors agree to grant higher valuations, which help the companies with recruitment and building credibility, in exchange for guarantees that they’ll get their money back first if the company goes public or sells. They can also negotiate to receive additional free shares if a subsequent round’s valuation is less favorable. Interviews with more than a dozen founders, venture capitalists, and the attorneys who draw up investment contracts reveal the most common financial provisions used in private-market technology deals today.

The backroom agreements are becoming more common as tech companies stay private longer, according to the interviews and financial documents obtained by Bloomberg Business. The practice obfuscates the meaning of a valuation, which can become dangerous down the road because private investors aren’t taking the same risks a public-market shareholder would. By the time a company does go public, the valuation it got from VCs may not align with its balance sheet.

…

Each provision covers different ways to make sure new investors get paid back, even if disaster strikes, if an initial public offering gives the company a market cap far less than its private number, or, more commonly, if the startup has to raise money again at a lower valuation. One stipulation, called senior liquidation preference, ensures that a certain group gets its money back before anyone else, including employees. Another class, called downside protection or ratchets, automatically grants additional shares in the event of a declining valuation, removing a great deal of risk that the stake will ever lose value.

The Obama administration is proposing to impose a fiduciary standard on brokers handling retirement accounts:

The plan to be issued by the Labor Department would require brokers to act in a customer’s best interest, a change that could limit the earnings of financial advisers in the handling of Americans’ $11 trillion of retirement savings.

…

At the heart of the proposal is an effort to tighten the legal standard for brokers handling retirement funds in individual retirement accounts and 401(k)s, which now hold more than $11 trillion. Under current rules, brokers can sell any product that is “suitable” for an investor, meaning it fits the client’s needs and tolerance for risk.Brokers typically earn money from upfront sales commissions or fees paid by investors who purchase mutual funds. White House officials said that kind of compensation arrangement provides an incentive to recommend products that net higher fees or commissions without yielding better returns for investors. Clients lose as much as $17 billion a year from such conflicted advice, according to the Obama administration.

…

Subjecting brokers to a fiduciary duty, a standard that now applies to professional money managers, will lead to more lawsuits against the industry and add burdensome compliance requirements, industry groups argue.The added costs will probably prompt brokers to drop client accounts with less than $50,000 of assets, leaving those investors to manage their own savings, according to the Securities Industry and Financial Markets Association.

So naturally every office-seeker in town is jumping on the bandwagon:

The SEC should “implement a uniform fiduciary duty for broker-dealers and investment advisers where the standard is to act in the best interest of the investor,” White said Tuesday at a conference sponsored by the Securities Industry and Financial Markets Association in Phoenix.

The SEC, which oversees the brokerage industry as a whole, has studied the issue for years without taking any regulatory action. The agency now finds itself in the middle of what promises to be one of the most bruising Wall Street lobbying battles in years.

The financial industry has been watching closely for White to reveal her position, which would break a standoff between the two Democrat and two Republican commissioners. White said she will begin talking with other commissioners about the outlines of new rules.

…

Some investor groups say the current rules don’t go far enough to limit conflicts of interests for brokers, who are paid by mutual funds and other companies for selling their products.

…

White’s support for the measures aligns her with the Obama administration and congressional Democrats. It pits her against many Republicans, who have said a fiduciary standard will be costly for brokers and could make them drop less wealthy clients.

So who’s going to sell anything? And what will happen to new issue commissions, which are formally paid by the issuer? Proxy solicitation fees?

The only way fiduciary duty can work is if it exists in isolation. Perfect isolation. That means that one guy can’t be a fiduciary to somebody and a broker to somebody else; and it means that one firm can’t have both fiduciaries and brokers, and it means that one firm can’t have subsidiaries – or even significant stock holdings – in both fiduciary firms and broking firms. And guess what? That ain’t gonna happen.

Perhaps you will say that Chinese Walls will work just as well. Perhaps you will insist that proper oversight and regulation will regulate a distinction between the buy side and the sell side. Perhaps you are a fool. Follow the money. Regulation will produce nothing more than a few cushy jobs for regulators, reams of ultimately unread paperwork generated by guys who have better things to do and a total lack of service to Granny with her $50,000 account but – on the bright side – lots of new business for banks, who will stick their clients into GOOD SAFE GICS and ZERO-RISK Principal Protected Notes!

Click for Big

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

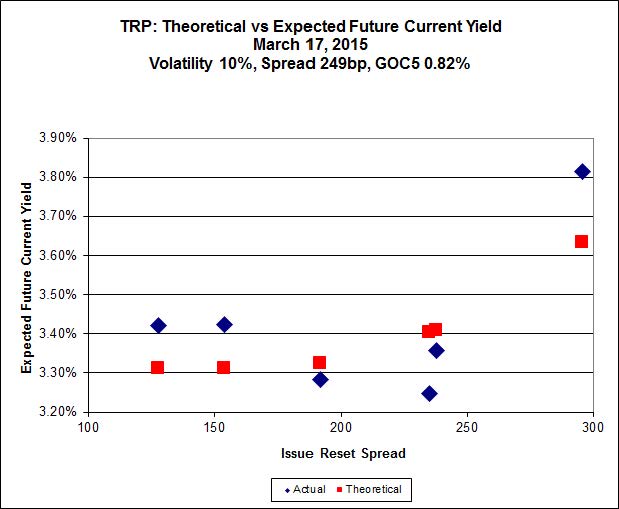

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.41 to be $1.12 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.23 cheap at its bid price of 24.78.

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum, although it declined substantially today. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 24.35 to be $0.63 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.86 to be $0.69 cheap.

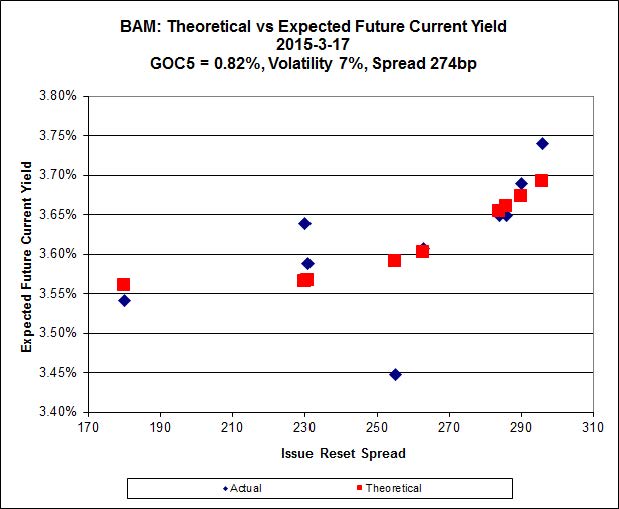

Click for Big

The fit on this series is actually quite reasonable – it’s the scale that makes it look so weird.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 21.44 to be $0.44 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 24.44 and appears to be $0.98 rich.

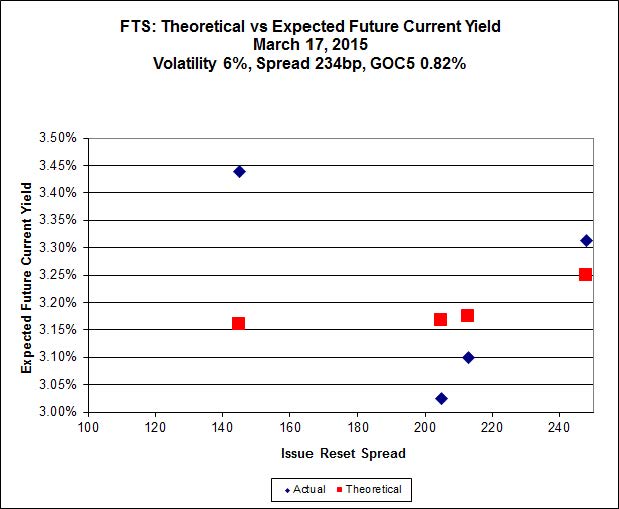

Click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 16.50, looks $1.46 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.72 and is $1.07 rich.

Click for Big

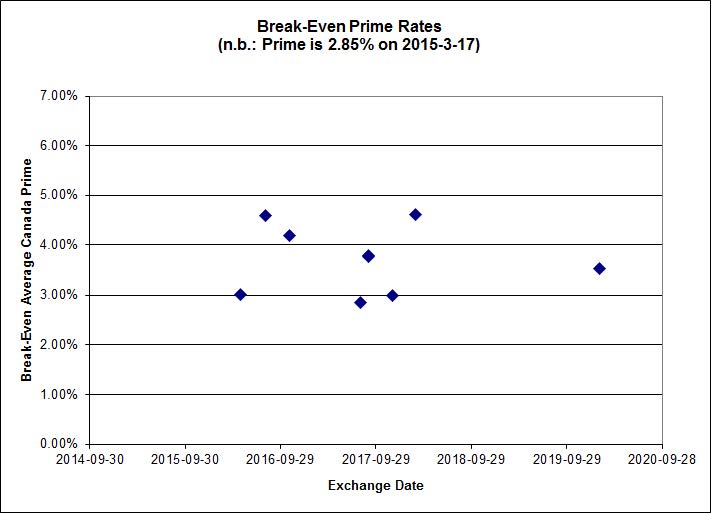

The cancellation of the previously announced deflationary environment had an immediate effect on the implied three month bill rate, with investment-grade pairs predicting an average over the next five years of about 0.00% – except for one outlier, TRP.PR.A / TRP.PR.F, which has a break-even of -0.83%. The DC.PR.B / DC.PR.D pair has gone from the extreme to the ludicrous and now predicts an average bill rate over the next 4 3/4 years of -2.09%

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

It was a rough day for the Canadian preferred share market, with PerpetualDiscounts losing 31bp, FixedResets down 29bp and DeemedRetractibles off 7bp. Floater and FixedReset losers dominated the Performance Highlights table. Volume was average.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.5126 % | 2,343.2 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.5126 % | 4,097.0 |

| Floater | 3.24 % | 3.23 % | 65,483 | 19.17 | 3 | -1.5126 % | 2,491.0 |

| OpRet | 4.07 % | 1.21 % | 100,236 | 0.26 | 1 | 0.0000 % | 2,763.7 |

| SplitShare | 4.46 % | 4.42 % | 55,440 | 4.43 | 5 | 0.5269 % | 3,221.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,527.1 |

| Perpetual-Premium | 5.29 % | 0.40 % | 57,945 | 0.08 | 25 | -0.1250 % | 2,521.5 |

| Perpetual-Discount | 5.00 % | 4.99 % | 152,053 | 15.14 | 9 | -0.3082 % | 2,798.0 |

| FixedReset | 4.39 % | 3.51 % | 245,770 | 16.68 | 85 | -0.2937 % | 2,427.6 |

| Deemed-Retractible | 4.90 % | -0.14 % | 107,334 | 0.12 | 37 | -0.0661 % | 2,658.1 |

| FloatingReset | 2.50 % | 2.93 % | 83,830 | 6.32 | 8 | -0.0643 % | 2,329.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.F | FixedReset | -2.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.33 Bid-YTW : 5.54 % |

| IAG.PR.G | FixedReset | -2.21 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.70 Bid-YTW : 2.96 % |

| TRP.PR.C | FixedReset | -2.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 17.23 Evaluated at bid price : 17.23 Bid-YTW : 3.62 % |

| SLF.PR.G | FixedReset | -2.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.06 Bid-YTW : 6.04 % |

| BAM.PR.B | Floater | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 15.53 Evaluated at bid price : 15.53 Bid-YTW : 3.20 % |

| BAM.PR.T | FixedReset | -1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 21.46 Evaluated at bid price : 21.81 Bid-YTW : 3.74 % |

| BAM.PR.X | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 3.87 % |

| BAM.PR.K | Floater | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 15.30 Evaluated at bid price : 15.30 Bid-YTW : 3.25 % |

| BAM.PR.C | Floater | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 15.40 Evaluated at bid price : 15.40 Bid-YTW : 3.23 % |

| FTS.PR.H | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 3.50 % |

| CU.PR.C | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 23.07 Evaluated at bid price : 23.92 Bid-YTW : 3.42 % |

| IFC.PR.A | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.06 Bid-YTW : 5.12 % |

| ENB.PR.H | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 18.45 Evaluated at bid price : 18.45 Bid-YTW : 4.30 % |

| MFC.PR.N | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.31 Bid-YTW : 3.85 % |

| ENB.PR.Y | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 19.94 Evaluated at bid price : 19.94 Bid-YTW : 4.30 % |

| CIU.PR.C | FixedReset | 7.21 % | Notoriously volatile. Rarely means anything. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 16.35 Evaluated at bid price : 16.35 Bid-YTW : 3.52 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.G | FixedReset | 95,348 | Desjardins sold blocks of 10,800 shares, 26,100 and 13,100 to anonymous at 18.20. Desjardins then went to the well again, selling blocks of 12,500 and 12,400 to anonymous at 18.10. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.06 Bid-YTW : 6.04 % |

| GWO.PR.N | FixedReset | 71,710 | Desjardins sold 46,700 to anonymous at 18.65, then sold 13,700 to RBC at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.55 Bid-YTW : 5.70 % |

| HSE.PR.E | FixedReset | 56,820 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 23.16 Evaluated at bid price : 25.00 Bid-YTW : 4.34 % |

| FTS.PR.M | FixedReset | 53,290 | RBC crossed 50,000 at 24.98. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 23.15 Evaluated at bid price : 24.90 Bid-YTW : 3.39 % |

| RY.PR.M | FixedReset | 42,770 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-17 Maturity Price : 22.85 Evaluated at bid price : 24.25 Bid-YTW : 3.51 % |

| RY.PR.I | FixedReset | 41,200 | Scotia crossed 40,000 at 25.41. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.42 Bid-YTW : 2.98 % |

| There were 34 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.F | FixedReset | Quote: 19.33 – 20.00 Spot Rate : 0.6700 Average : 0.4716 YTW SCENARIO |

| BAM.PF.E | FixedReset | Quote: 24.44 – 24.80 Spot Rate : 0.3600 Average : 0.2335 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 18.66 – 19.30 Spot Rate : 0.6400 Average : 0.5216 YTW SCENARIO |

| BMO.PR.L | Deemed-Retractible | Quote: 25.86 – 26.10 Spot Rate : 0.2400 Average : 0.1511 YTW SCENARIO |

| CU.PR.C | FixedReset | Quote: 23.92 – 24.50 Spot Rate : 0.5800 Average : 0.4962 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 24.31 – 24.65 Spot Rate : 0.3400 Average : 0.2576 YTW SCENARIO |