Nothing happened today.

The Canadian preferred share market was on fire today, with PerpetualDiscounts winning 88bp, FixedResets up 28bp and DeemedRetractibles gaining 15bp. There’s a good list of winners in the Performance Highlights table. Volume was below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

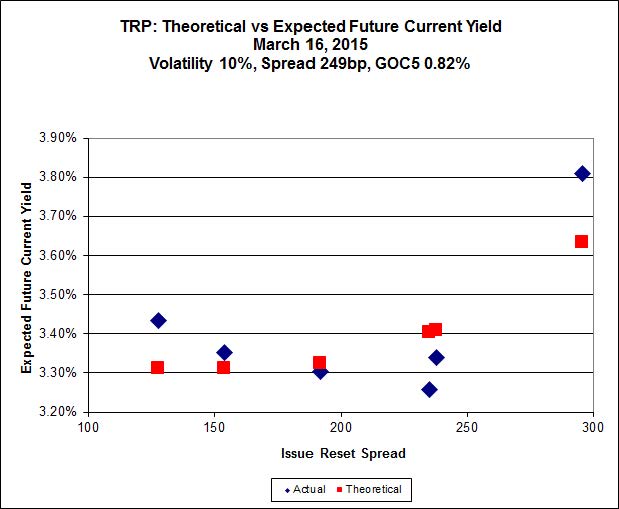

Here’s TRP:

click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.32 to be $1.03 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.21 cheap at its bid price of 24.80.

click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum, although it declined substantially today. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 24.35 to be $0.43 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 26.00 to be $0.58 cheap.

click for Big

The fit on this series is actually quite reasonable – it’s the scale that makes it look so weird.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 21.59 to be $0.59 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 24.67 and appears to be $0.99 rich.

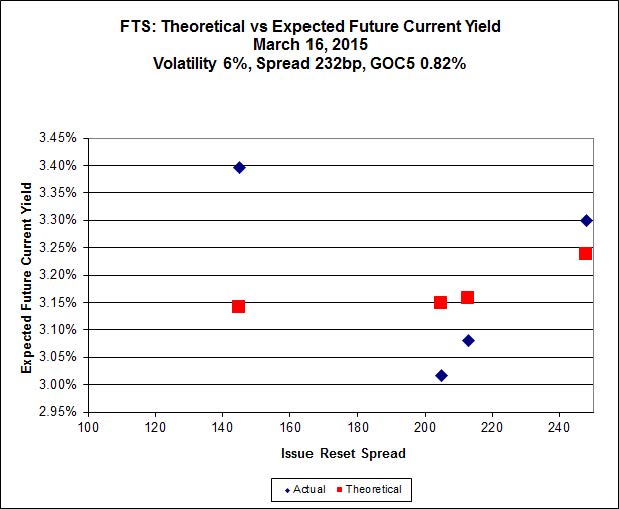

click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 16.71, looks $1.36 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.79 and is $1.00 rich.

click for Big

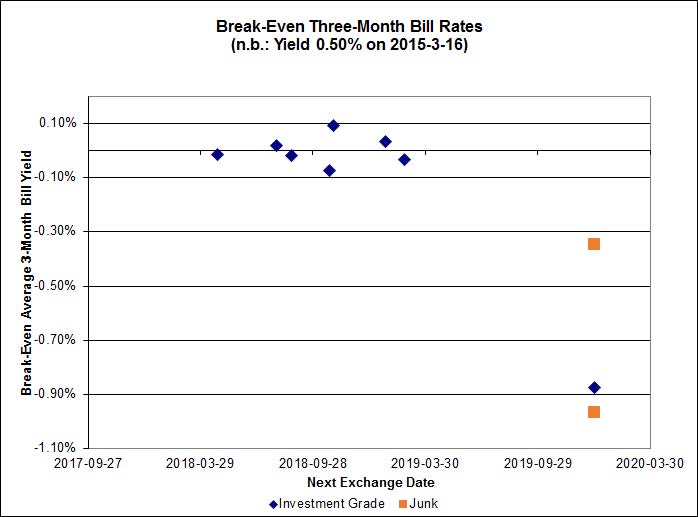

The cancellation of the previously announced deflationary environment had an immediate effect on the implied three month bill rate, with investment-grade pairs predicting an average over the next five years of about 0.00% – except for one outlier, TRP.PR.A / TRP.PR.F, which has a break-even of -0.87%.

click for Big

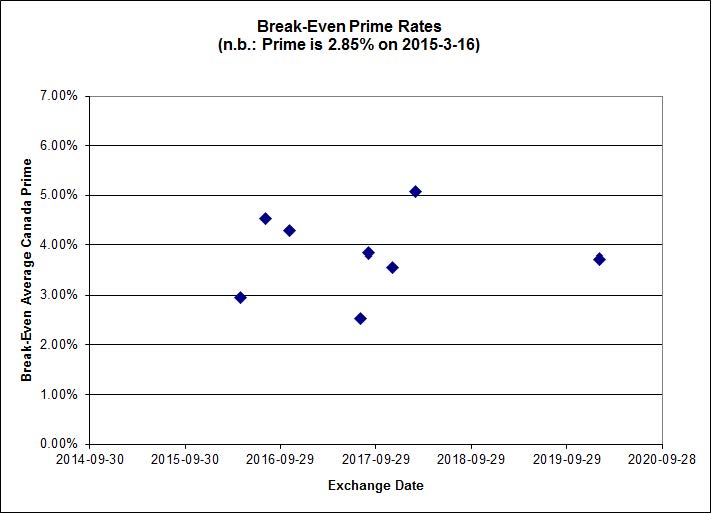

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1277 % | 2,379.2 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1277 % | 4,159.9 |

| Floater | 3.19 % | 3.19 % | 65,776 | 19.27 | 3 | -0.1277 % | 2,529.2 |

| OpRet | 4.07 % | 1.20 % | 101,525 | 0.26 | 1 | 0.0397 % | 2,763.7 |

| SplitShare | 4.48 % | 4.56 % | 51,332 | 4.46 | 5 | -0.0917 % | 3,204.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0397 % | 2,527.1 |

| Perpetual-Premium | 5.28 % | -0.62 % | 58,962 | 0.08 | 25 | 0.2035 % | 2,524.7 |

| Perpetual-Discount | 4.98 % | 4.98 % | 152,763 | 15.16 | 9 | 0.8808 % | 2,806.6 |

| FixedReset | 4.38 % | 3.51 % | 249,495 | 16.75 | 85 | 0.2787 % | 2,434.8 |

| Deemed-Retractible | 4.90 % | -1.07 % | 108,726 | 0.12 | 37 | 0.1548 % | 2,659.8 |

| FloatingReset | 2.50 % | 2.87 % | 86,719 | 6.32 | 8 | -0.1230 % | 2,330.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CIU.PR.C | FixedReset | -7.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 15.25 Evaluated at bid price : 15.25 Bid-YTW : 3.78 % |

| TRP.PR.F | FloatingReset | -2.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 3.30 % |

| SLF.PR.H | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.51 Bid-YTW : 4.40 % |

| BAM.PF.E | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 23.04 Evaluated at bid price : 24.67 Bid-YTW : 3.56 % |

| CU.PR.C | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 23.21 Evaluated at bid price : 24.20 Bid-YTW : 3.37 % |

| BAM.PF.C | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 22.91 Evaluated at bid price : 23.22 Bid-YTW : 5.22 % |

| TRP.PR.A | FixedReset | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 20.74 Evaluated at bid price : 20.74 Bid-YTW : 3.47 % |

| MFC.PR.C | Deemed-Retractible | 1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.95 Bid-YTW : 5.07 % |

| MFC.PR.M | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.93 Bid-YTW : 3.60 % |

| MFC.PR.N | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.57 Bid-YTW : 3.71 % |

| FTS.PR.J | Perpetual-Premium | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 24.60 Evaluated at bid price : 25.03 Bid-YTW : 4.76 % |

| BAM.PR.M | Perpetual-Discount | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 22.49 Evaluated at bid price : 22.78 Bid-YTW : 5.21 % |

| MFC.PR.F | FixedReset | 1.85 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.81 Bid-YTW : 5.25 % |

| BAM.PR.N | Perpetual-Discount | 1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 22.51 Evaluated at bid price : 22.77 Bid-YTW : 5.22 % |

| HSE.PR.A | FixedReset | 2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 17.34 Evaluated at bid price : 17.34 Bid-YTW : 3.84 % |

| TRP.PR.C | FixedReset | 2.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 17.60 Evaluated at bid price : 17.60 Bid-YTW : 3.54 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.G | Perpetual-Premium | 229,837 | Called for redemption April 30. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-04-15 Maturity Price : 25.00 Evaluated at bid price : 25.29 Bid-YTW : -0.62 % |

| CM.PR.Q | FixedReset | 85,660 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 23.02 Evaluated at bid price : 24.66 Bid-YTW : 3.57 % |

| BNS.PR.Y | FixedReset | 84,421 | Scotia bought 10,000 from TD at 22.50. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.45 Bid-YTW : 3.64 % |

| RY.PR.M | FixedReset | 65,251 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 22.84 Evaluated at bid price : 24.23 Bid-YTW : 3.52 % |

| HSE.PR.E | FixedReset | 63,080 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 23.13 Evaluated at bid price : 24.92 Bid-YTW : 4.36 % |

| TD.PF.D | FixedReset | 55,955 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-16 Maturity Price : 23.13 Evaluated at bid price : 24.97 Bid-YTW : 3.50 % |

| There were 24 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CIU.PR.C | FixedReset | Quote: 15.25 – 16.80 Spot Rate : 1.5500 Average : 0.9596 YTW SCENARIO |

| CU.PR.D | Perpetual-Premium | Quote: 25.25 – 25.64 Spot Rate : 0.3900 Average : 0.2779 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 24.32 – 24.65 Spot Rate : 0.3300 Average : 0.2247 YTW SCENARIO |

| BAM.PR.K | Floater | Quote: 15.50 – 15.89 Spot Rate : 0.3900 Average : 0.3095 YTW SCENARIO |

| GWO.PR.F | Deemed-Retractible | Quote: 25.69 – 25.99 Spot Rate : 0.3000 Average : 0.2211 YTW SCENARIO |

| RY.PR.H | FixedReset | Quote: 24.70 – 24.95 Spot Rate : 0.2500 Average : 0.1745 YTW SCENARIO |

I’m a long time reader who enjoys your commentary, so thank you for the blog.

I don’t think I’ve seen it specified, so wanted to ask – when you give a bp move in a pref group / index, what yield metric is that based on (current yield, ytm, and if ytm what assumption is being made about maturity parameters for eg fixed resets with no set maturity)? For example, when you stated that fixed resets were up 28 bps, I’m curious to know the yield parameters so I can get a feel for the % movement that has happened.

Thanks

When I state that FixedResets were up 28bp, I am speaking in terms of total return. If I haven’t made a mistake, it will be equal to the “Day’s Perf.[ormance]” column in the applicable row of the first table.