FFH.PR.J has been created by partial exchange from FFH.PR.I, following the latter issue’s reset to 3.708% for the next five years, a reduction of about 26% in the dividend rate.

FFH.PR.J will pay 3-month bills + 285bp, reset quarterly.

The company has made no announcement regarding the take-up of the conversion offer or the commencement of trading, but the TMX website indicates that 1,534,447 shares of FFH.PR.J are outstanding, implying a conversion rate of 12.8% given that the TMX reports 10,465,553 shares of FFH.PR.I currently outstanding. It will be recalled that I recommended against conversion.

FFH.PR.J will be tracked by HIMIPref™ and has been assigned to the Scraps subindex on credit concerns.

The issue traded no shares before closing at 17.00-50, 1×1.

Vital Statistics are:

| FFH.PR.J | FloatingReset | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 4.88 % |

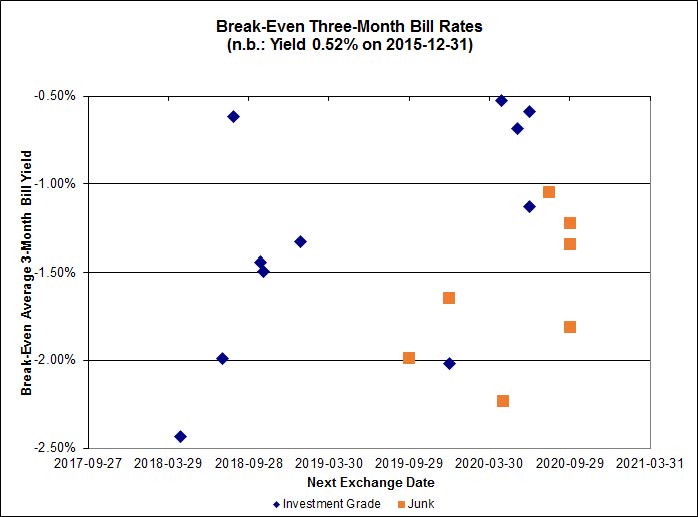

Strong Pair theory, for which a calculator is available, allows us to examine the consistency of the bid price of FFH.PR.I with FFH.PR.J; they are interconvertible in the future. The bids of 17.12 and 17.00, respectively, allow us to gauge that total returns over the next five years will be equal if the three-month Bill Yield exceeds 0.74%.

Click for Big

Whatever one might think of the probability of the bill yield averaging over 0.74% over the next five years, it is clearly rational to believe that the break-even yield will decline in the future, to become more comparable to the break-even yield of the issues’ peers. This implies an expectation that the bid price of the FloatingReset, FFH.PR.J, will decline in the next little while relative to that of FFH.PR.I [note the word “relative”! They could both increase or both decrease!]. In fact, keeping the bid price of FFH.PR.I constant at 17.12, a decline of the bid for FFH.PR.J to 14.80 will bring the break-even yield of the pair to -1.50%, the centerpoint of the chart.

In other words, I suggest there is good reason to believe FFH.PR.J will get substantially cheaper relative to FFH.PR.I over the next little while!