The federal Competition Bureau has heretofore been best known for its decision, reported July 4, 2012, to allow the banks to reduce competition in the Canadian financial market, provided extra payments were made to their buddies at the OSC. It would seem that the Bureau has been very impressed by the OSC’s ability to fund puppet groups providing employment for their buddies at taxpayer expense and have decided that this is just too good a deal to turn down:

As part of a consent agreement with the Competition Bureau, Telus will issue rebates of up to $7.34 million to certain current and former wireless customers after the Bureau concluded that Telus made, or permitted to be made, false or misleading representations in advertisements for premium text messages in pop‑up ads, apps and on social media.

…

Telus will also donate a total of $250,000 to the Ryerson University Privacy and Big Data Institute; Éducaloi, a non‑profit organization dedicated to helping the public understand their rights and responsibilities under the law; and the Centre de recherche en droit public de l’Université de Montréal.

It’s nice work, if you can get it!

Canadian preferred share investors celebrated the first calendar week of No More Tax Loss Selling!

Click for Big

It was an excellent day overall for the Canadian preferred share market, although DeemedRetractibles provided a reminder of what 2015 was like, with PerpetualDiscounts gaining 63bp, FixedResets up 93bp and DeemedRetractibles off 18bp. The Performance Highlights table continues to show lots of churn. Volume was virtually non-existent.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

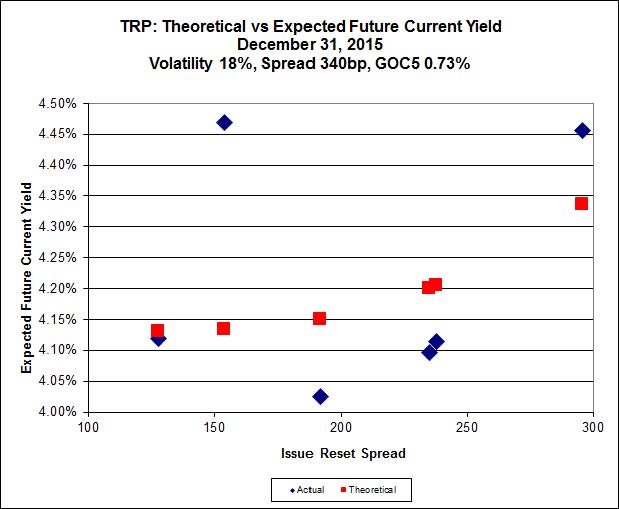

Here’s TRP:

Click for Big

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 16.46 to be $0.50 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.03 cheap at its bid price of 12.70.

Click for Big

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 20.42 to be 0.47 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 22.59 to be 0.66 cheap.

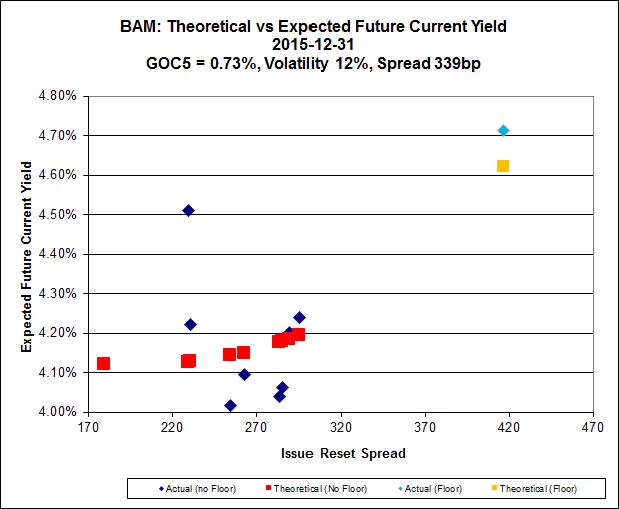

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.80 to be $1.56 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.10 and appears to be $0.73 rich.

Click for Big

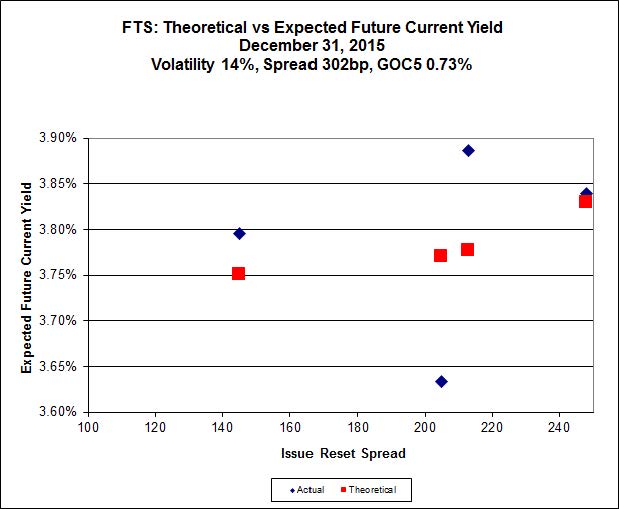

FTS.PR.K, with a spread of +205bp, and bid at 19.13, looks $0.70 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.40 and is $0.53 cheap.

Click for Big

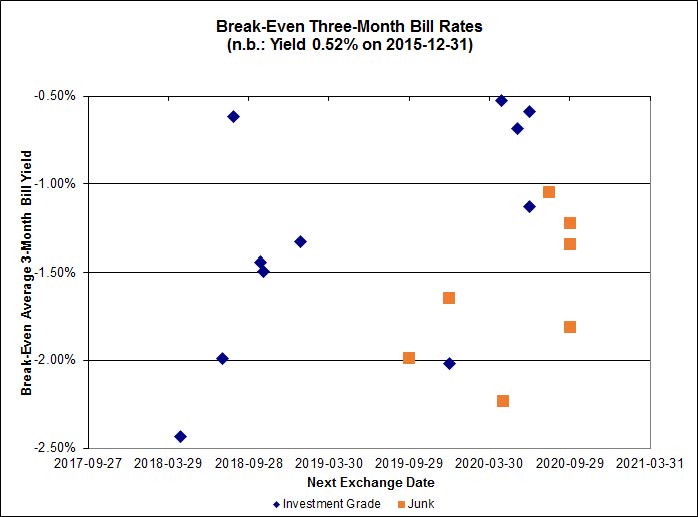

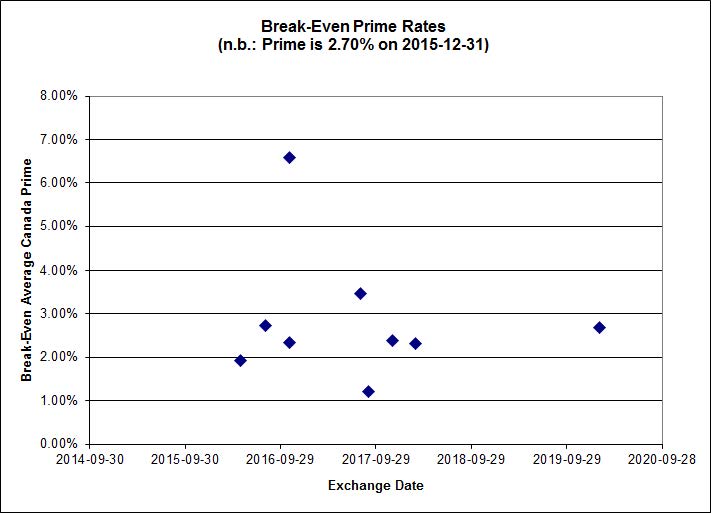

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.09%, with two outliers above -0.50%, including the newly created GWO.PR.N / GWO.PR.O pair. There are four junk outliers above -0.50%, including the newly created FFH.PR.I / FFH.PR.J pair.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.68 % | 5.67 % | 29,722 | 17.08 | 1 | 0.6944 % | 1,662.5 |

| FixedFloater | 6.81 % | 6.03 % | 37,769 | 16.17 | 1 | 3.7175 % | 2,865.7 |

| Floater | 4.18 % | 4.32 % | 79,998 | 16.76 | 4 | -0.3306 % | 1,828.4 |

| OpRet | 4.84 % | 3.69 % | 24,986 | 0.65 | 1 | 0.3172 % | 2,749.5 |

| SplitShare | 4.80 % | 5.55 % | 83,852 | 1.83 | 6 | 0.1454 % | 3,217.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1454 % | 2,510.4 |

| Perpetual-Premium | 5.75 % | 2.81 % | 91,918 | 0.08 | 7 | 0.1017 % | 2,535.4 |

| Perpetual-Discount | 5.60 % | 5.66 % | 104,639 | 14.38 | 33 | 0.6347 % | 2,567.6 |

| FixedReset | 4.92 % | 4.26 % | 259,128 | 14.92 | 81 | 0.9296 % | 2,094.4 |

| Deemed-Retractible | 5.17 % | 5.09 % | 128,555 | 5.31 | 33 | -0.1768 % | 2,599.6 |

| FloatingReset | 2.80 % | 4.15 % | 68,430 | 5.64 | 12 | 0.1337 % | 2,159.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.B | FixedReset | -2.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 12.20 Evaluated at bid price : 12.20 Bid-YTW : 4.18 % |

| IAG.PR.A | Deemed-Retractible | -1.85 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.25 Bid-YTW : 6.89 % |

| BAM.PF.A | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 21.30 Evaluated at bid price : 21.60 Bid-YTW : 4.33 % |

| SLF.PR.G | FixedReset | -1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.40 Bid-YTW : 8.34 % |

| SLF.PR.D | Deemed-Retractible | -1.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.55 Bid-YTW : 7.19 % |

| SLF.PR.C | Deemed-Retractible | -1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.69 Bid-YTW : 7.09 % |

| IAG.PR.G | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.22 Bid-YTW : 5.27 % |

| BAM.PR.N | Perpetual-Discount | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.01 Evaluated at bid price : 20.01 Bid-YTW : 5.98 % |

| MFC.PR.F | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.99 Bid-YTW : 8.73 % |

| BAM.PF.B | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.51 Evaluated at bid price : 20.51 Bid-YTW : 4.27 % |

| TD.PF.C | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.46 Evaluated at bid price : 19.46 Bid-YTW : 4.08 % |

| ELF.PR.G | Perpetual-Discount | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.89 Evaluated at bid price : 20.89 Bid-YTW : 5.71 % |

| MFC.PR.G | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.59 Bid-YTW : 5.07 % |

| TD.PF.D | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 21.05 Evaluated at bid price : 21.05 Bid-YTW : 4.25 % |

| BMO.PR.S | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 4.01 % |

| CU.PR.C | FixedReset | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.17 Evaluated at bid price : 20.17 Bid-YTW : 3.97 % |

| MFC.PR.I | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.15 Bid-YTW : 4.79 % |

| RY.PR.H | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.60 Evaluated at bid price : 19.60 Bid-YTW : 4.06 % |

| RY.PR.Z | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 4.03 % |

| MFC.PR.J | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.95 Bid-YTW : 5.25 % |

| W.PR.H | Perpetual-Discount | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 23.25 Evaluated at bid price : 23.55 Bid-YTW : 5.85 % |

| FTS.PR.M | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.90 Evaluated at bid price : 20.90 Bid-YTW : 4.07 % |

| BMO.PR.Y | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 4.13 % |

| BNS.PR.D | FloatingReset | 1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.46 Bid-YTW : 5.76 % |

| FTS.PR.K | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.13 Evaluated at bid price : 19.13 Bid-YTW : 3.90 % |

| RY.PR.M | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.41 Evaluated at bid price : 20.41 Bid-YTW : 4.21 % |

| MFC.PR.M | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.18 Bid-YTW : 5.69 % |

| IFC.PR.A | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.66 Bid-YTW : 8.20 % |

| MFC.PR.N | FixedReset | 1.65 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.95 Bid-YTW : 5.77 % |

| FTS.PR.G | FixedReset | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 4.09 % |

| BMO.PR.W | FixedReset | 1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 4.02 % |

| PWF.PR.T | FixedReset | 1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 22.84 Evaluated at bid price : 23.75 Bid-YTW : 3.39 % |

| HSE.PR.G | FixedReset | 1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.43 Evaluated at bid price : 19.43 Bid-YTW : 5.61 % |

| TD.PF.B | FixedReset | 1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.64 Evaluated at bid price : 19.64 Bid-YTW : 4.05 % |

| BAM.PR.Z | FixedReset | 2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 21.42 Evaluated at bid price : 21.76 Bid-YTW : 4.35 % |

| BMO.PR.T | FixedReset | 2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 4.01 % |

| CIU.PR.A | Perpetual-Discount | 2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.74 Evaluated at bid price : 20.74 Bid-YTW : 5.62 % |

| SLF.PR.H | FixedReset | 2.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.91 Bid-YTW : 6.59 % |

| BAM.PR.R | FixedReset | 2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 4.57 % |

| TD.PF.A | FixedReset | 2.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.84 Evaluated at bid price : 19.84 Bid-YTW : 4.02 % |

| FTS.PR.F | Perpetual-Discount | 2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 22.97 Evaluated at bid price : 23.24 Bid-YTW : 5.32 % |

| FTS.PR.I | FloatingReset | 2.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 12.75 Evaluated at bid price : 12.75 Bid-YTW : 3.77 % |

| BAM.PF.D | Perpetual-Discount | 2.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 6.02 % |

| CM.PR.O | FixedReset | 2.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.11 Evaluated at bid price : 20.11 Bid-YTW : 3.97 % |

| CIU.PR.C | FixedReset | 2.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 12.70 Evaluated at bid price : 12.70 Bid-YTW : 4.17 % |

| CU.PR.F | Perpetual-Discount | 3.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 20.69 Evaluated at bid price : 20.69 Bid-YTW : 5.51 % |

| HSE.PR.E | FixedReset | 3.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.38 Evaluated at bid price : 19.38 Bid-YTW : 5.63 % |

| CM.PR.P | FixedReset | 3.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.77 Evaluated at bid price : 19.77 Bid-YTW : 3.95 % |

| HSE.PR.A | FixedReset | 3.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 13.10 Evaluated at bid price : 13.10 Bid-YTW : 4.70 % |

| BAM.PR.G | FixedFloater | 3.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 25.00 Evaluated at bid price : 13.95 Bid-YTW : 6.03 % |

| BAM.PR.X | FixedReset | 3.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 15.92 Evaluated at bid price : 15.92 Bid-YTW : 4.21 % |

| NA.PR.W | FixedReset | 3.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 4.17 % |

| MFC.PR.K | FixedReset | 3.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.40 Bid-YTW : 5.91 % |

| IFC.PR.C | FixedReset | 4.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.85 Bid-YTW : 5.84 % |

| SLF.PR.J | FloatingReset | 4.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.00 Bid-YTW : 9.10 % |

| HSE.PR.C | FixedReset | 5.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 18.47 Evaluated at bid price : 18.47 Bid-YTW : 5.44 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| MFC.PR.F | FixedReset | 44,160 | RBC crossed 34,300 at 15.00. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.99 Bid-YTW : 8.73 % |

| BAM.PR.R | FixedReset | 21,263 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 4.57 % |

| CM.PR.P | FixedReset | 18,500 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 19.77 Evaluated at bid price : 19.77 Bid-YTW : 3.95 % |

| MFC.PR.I | FixedReset | 12,950 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.15 Bid-YTW : 4.79 % |

| HSE.PR.A | FixedReset | 12,929 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-31 Maturity Price : 13.10 Evaluated at bid price : 13.10 Bid-YTW : 4.70 % |

| SLF.PR.J | FloatingReset | 12,700 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.00 Bid-YTW : 9.10 % |

| There were 3 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.E | FixedReset | Quote: 18.80 – 20.00 Spot Rate : 1.2000 Average : 0.8799 YTW SCENARIO |

| HSE.PR.G | FixedReset | Quote: 19.43 – 20.07 Spot Rate : 0.6400 Average : 0.3922 YTW SCENARIO |

| W.PR.J | Perpetual-Discount | Quote: 23.89 – 24.42 Spot Rate : 0.5300 Average : 0.3703 YTW SCENARIO |

| BNS.PR.C | FloatingReset | Quote: 22.29 – 22.99 Spot Rate : 0.7000 Average : 0.5610 YTW SCENARIO |

| SLF.PR.G | FixedReset | Quote: 15.40 – 16.00 Spot Rate : 0.6000 Average : 0.4723 YTW SCENARIO |

| IGM.PR.B | Perpetual-Premium | Quote: 25.30 – 25.70 Spot Rate : 0.4000 Average : 0.2982 YTW SCENARIO |