Malachite Aggressive Preferred Fund’s Net Asset Value per Unit as of the close November 29, 2019, was $7.8207. Performance was adversely affected in November, 2019, as the assumption of DeemedRetraction was cancelled in the wake of the IAIS decision included in ICS 2.0. This was probably a major factor in recent underperformance of low-spread Insurance issues, in which the portfolio is overweighted.

On a brighter note, this cancellation of this assumption means that the preferred share universe has become much more homogeneous and I anticipate a higher level of trading in the future.

| Returns to November 29, 2019 | ||||

| Period | MAPF | BMO-CM “50” Preferred Share Index | TXPR* Total Return |

CPD – according to Blackrock |

| One Month | +0.40% | +1.07% | +1.18% | N/A |

| Three Months | +3.53% | +4.92% | +4.76% | N/A |

| One Year | -9.34% | -2.71% | -0.62% | -1.27% |

| Two Years (annualized) | -8.28% | -4.87% | -3.56% | N/A |

| Three Years (annualized) | +2.64% | +3.31% | +3.05% | +2.54% |

| Four Years (annualized) | +3.79% | +4.17% | +3.69% | N/A |

| Five Years (annualized) | -1.54% | -0.51% | -0.85% | -1.30% |

| Six Years (annualized) | +0.38% | +0.20% | +0.19% | N/A |

| Seven Years (annualized) | +0.11% | +0.36% | +0.13% | N/A |

| Eight Years (annualized) | +1.59% | +1.06% | +0.84% | N/A |

| Nine Years (annualized) | +1.47% | +1.61% | +1.22% | N/A |

| Ten Years (annualized) | +3.06% | +2.64% | +2.06% | +1.52% |

| Eleven Years (annualized) | +9.04% | +5.23% | +4.58% | |

| Twelve Years (annualized) | +6.89% | +2.75% | +2.11% | |

| Thirteen Years (annualized) | +5.92% | +2.00% | ||

| Fourteen Years (annualized) | +5.97% | +2.17% | ||

| Fifteen Years (annualized) | +6.00% | +2.34% | ||

| Sixteen Years (annualized) | +6.54% | +2.57% | ||

| Seventeen Years (annualized) | +7.82% | +2.87% | ||

| Eighteen Years (annualized) | +7.27% | +2.85% | ||

| MAPF returns assume reinvestment of distributions, and are shown after expenses but before fees. | ||||

| The full name of the BMO-CM “50” index is the BMO Capital Markets “50” Preferred Share Index. It is calculated without accounting for fees. | ||||

| “TXPR” is the S&P/TSX Preferred Share Index. It is calculated without accounting for fees, but does assume reinvestment of dividends. | ||||

| CPD Returns are for the NAV and are after all fees and expenses. Reinvestment of dividends is assumed. | ||||

| Figures for National Bank Preferred Equity Income Fund (formerly Omega Preferred Equity) (which are after all fees and expenses) for 1-, 3- and 12-months are +1.47%, +4.97% and +0.17%, respectively, according to Globe & Mail / Fundata after all fees & expenses. Three year performance is +3.09%; five year is +0.07; ten year is +2.71%

Figures from Morningstar are no longer conveniently available. |

||||

| Manulife Preferred Income Class Adv has been terminated by Manulife. The performance of this fund was last reported here in March, 2018. | ||||

| Figures for Horizons Active Preferred Share ETF (HPR) (which are after all fees and expenses) for 1-, 3- and 12-months are +1.48%, +5.64% & -2.99%, respectively. Three year performance is +2.27%, five-year is -0.42% | ||||

| Figures for National Bank Preferred Equity Fund (formerly Altamira Preferred Equity Fund) are +1.44%, +5.71% and -3.09% for one-, three- and twelve months, respectively. Three year performance is +2.44%; five-year is -0.47%.

Acccording to the fund’s fact sheet as of June 30, 2016, the fund’s inception date was October 30, 2015. I do not know how they justify this nonsensical statement, but will assume that prior performance is being suppressed in some perfectly legal manner that somebody at National considers ethical. The last time Altamira Preferred Equity Fund’s performance was reported here was April, 2014; performance under the National Bank banner was first reported here May, 2014. |

||||

| The figures for the NAV of BMO S&P/TSX Laddered Preferred Share Index ETF (ZPR) is -3.55% for the past twelve months. Two year performance is -5.39%, three year is +2.45%, five year is -2.84%. | ||||

| Figures for Fiera Canadian Preferred Share Class Cg Series F, (formerly Natixis Canadian Preferred Share Class Series F) (formerly NexGen Canadian Preferred Share Tax Managed Fund) are +1.29%, +4.12% and -4.66% for one-, three- and twelve-months, respectively. Three year performance is -0.37%; five-year is -0.63% | ||||

| Figures for BMO Preferred Share Fund (advisor series) according to BMO are +1.17%, +4.82% and -5.15% for the past one-, three- and twelve-months, respectively. Three year performance is -0.80%; five-year is -2.98%. | ||||

| Figures for PowerShares Canadian Preferred Share Index Class, Series F (PPS) are -2.08% for the past twelve months. The three-year figure is +3.16%; five years is -0.46% | ||||

| Figures for the First Asset Preferred Share Investment Trust (PSF.UN) are no longer available since the fund has merged with First Asset Preferred Share ETF (FPR).

Performance for the fund was last reported here in September, 2016; the first report of unavailability was in October, 2016. |

||||

| Figures for Lysander-Slater Preferred Share Dividend Fund (Class F) according to the company are +1.46%, +5.77% and -3.66% for the past one, three and twelve months, respectively. Three year performance is +0.72%. | ||||

| Figures for the Desjardins Canadian Preferred Share Fund A Class (A Class), as reported by the company are +0.99%, +4.33% and -3.68% for the past one, three and twelve months, respectively. Two year is -6.00% and three year performance is +1.13%. | ||||

MAPF returns assume reinvestment of dividends, and are shown after expenses but before fees. Past performance is not a guarantee of future performance. You can lose money investing in Malachite Aggressive Preferred Fund or any other fund. For more information, see the fund’s main page. The fund is available either directly from Hymas Investment Management or through a brokerage account at Odlum Brown Limited.

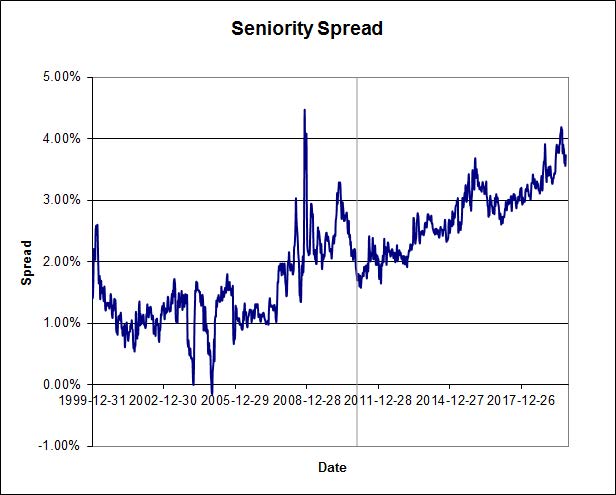

The preferred share market continues to suffer, leaving a lot of room for outsized gains. The Seniority Spread (the interest-equivalent yield on reasonably liquid, investment-grade PerpetualDiscounts less the yield on long term corporate bonds) is extremely elevated (chart end-date 2019-11-08):

)

) Click for Big

Note that the Seniority Spread was 370bp on November 27, a widening from the October 30 figure of 355bp. As a good practical example of the spreads between markets, consider that CIU issued a long-term bond in early September yielding 2.963%, about 411bp cheaper than the interest-equivalent figure of 7.07% for CIU.PR.A, which was then yielding about 5.44% as a dividend. Shaw Communications issued 30-year notes at 4.25% interest on December 5, when their FixedResets, SJR.PR.A, were yielding 6.59% dividends.

As has been noted, the increase in the Seniority Spread over the past year has been due not to an increase in yield (drop in prices) of Straight Preferreds over the year, but because the yield of the Straight Preferreds has remained relatively constant while the yield of long-term corporate bonds has dropped dramatically.

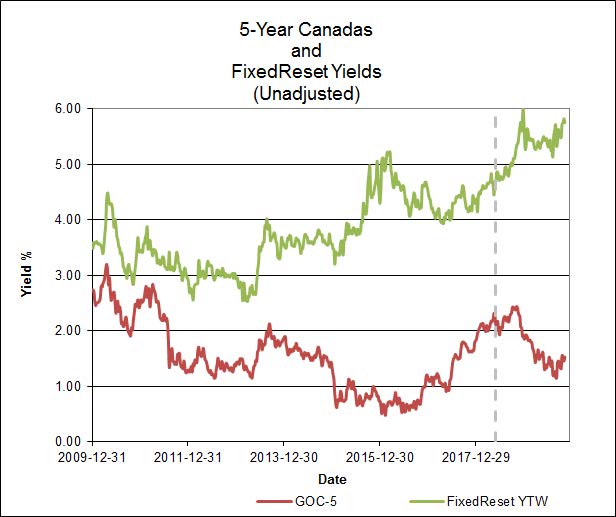

… and the relationship between five-year Canada yields and yields on investment-grade FixedResets is also well within what I consider ‘decoupled panic’ territory (chart end-date 2019-11-8):

Click for Big

In addition, I feel that the yield on five-year Canadas is unsustainably low (it should be the inflation rate plus an increment of … 1%? 1.5%? 2.0%?),and a return to sustainable levels is likely over the medium term.

It seems clear that many market players are, wittingly or not, using FixedResets to speculate on future moves in the Canada 5-Year yield. This is excellent news for those who take market action based on fundamentals and the long term characteristics of the market because nobody can consistently time the markets. The speculators will, over the long run and in aggregate, lose money, handing it over to more sober investors.

It should be noted that I have been unable to explain the very strong performance of Floor issues over the past year relative to their non-Floor counterparts. See the discussions on PrefBlog at LINK, LINK and LINK.

I believe the bear-market outperformance by the Floor issues is a behavioural phenomenon with very little basis in fundamentals. When interest rates in general move, FixedReset prices should not change much (to a first approximation), since in Fixed Income investing it is spreads that are important, not absolute yields. There should be some effect on Floor issues, which should move up slightly in price as yields go down since the ‘option’ to receive the floor rate will become more valuable. Adjustments due to this effect should be fairly small, however – and over the past year issues with a floor, that started the period being expensive, have simply gotten even more expensive, relative to their non-floored counterparts.

And the tricky thing about behavioural models of investing is that they can lose their explanatory power very quickly when an investment fashion shifts, whereas fundamentals will always be effective. Just to give an example from the preferred share market – until the end of 2014, FixedResets were priced relative to each other according to their initial dividend; when the reset of TRP.PR.A shocked a lot of investors, relative pricing became much more dependent upon the Issue Reset Spread, a much more logical and fundamental property.

FixedReset (Discount) performance on the month was +1.45% vs. PerpetualDiscounts of +0.96% in November; the two classes finally decoupled in mid-November, 2018, after months of moving in lockstep, but it still appears to me that yields available on FixedResets are keeping the yields of PerpetualDiscounts up, even though a consistent valuation based on an expectation of declining interest rates would greatly increase the attractiveness of PerpetualDiscounts:

Click for Big

Floaters continued to recover, returning +2.83% for November but the figure for the past twelve months remains horrific at -24.80. Look at the long-term performance:

Click for Big

Some Assiduous Readers will be interested to observe that the ‘Quantitative Easing’ decline was not initially as bad as the ‘Credit Crunch’ decline, which took the sector down to the point where the 15-year cumulative total return was negative. I wrote about that at the time. but it became worse in August, 2019! On August 30, 2019 the HIMI Floater Index (total return) value was calculated as 1906.6; the index first surpassed this value on 2003-8-13. Thus, cumulative total return (that is, including dividends) was negative over a period of slightly-over sixteen years.

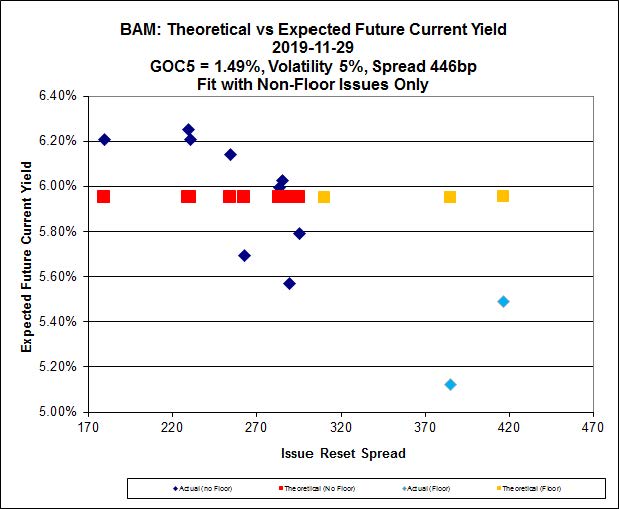

It seems clear that Floaters are used, wittingly or otherwise, as a vehicle for speculation on the policy rate and Canada Prime, while FixedResets are being used as a vehicle for speculation on the five-year Canada rate. In support of this idea, I present an Implied Volatility analysis of the TRP series of FixedResets as of November 29, which is comprised of six issues without a Minimum Rate Guarantee and two issues which do have this feature:

Click for Big

The two issues with floors, TRP.PR.J (+469, minimum 5.50%) and TRP.PR.K (+385, minimum 4.90%) are $2.82 and $4.73 rich, respectively. These are modest decreases from last month, despite the fact that their floor will not become effective unless five-year Canadas dip below 0.81% and 1.05%, respectively. For all the gloom, we’re still above those levels!

Lest this be considered a fluke, I also show results for the BAM series of FixedResets, which includes three issues with dividend floors: BAM.PF.H (+417, Minimum 5.00%); BAM.PF.I (+386, Minimum 4.80%); and BAM.PF.J (+310, Minimum 4.75%); these issues are all rich compared to their non-floor siblings, being 2.01, 3.63 and 5.11 expensive, respectively, wider in aggregate thatn last month’s figures of $2.07, $3.43 and $4.84.

Click for Big

Relative performance during the month was not correlated with Issue Reset Spreads for either “Pfd-2 Group” or “Pfd-3 Group” issues:

Click for Big

… and results over the quarter were similar (Pfd-3 Group correlation was 11%):

Click for Big

In both charts the poor performance of the low-spread insurance issues may be observed. These issues are GWO.PR.N (Issue Reset Spread 130bp, 1-Month performance -2.91%); IFC.PR.A (172bp, -1.46%); MFC.PR.F (141bp, -0.69%); and SLF.PR.G (141bp, -0.59%). There are sufficient MFC FixedReset issues to do an Implied Volatility Analysis:

Click for Big

If anything, MFC.PR.F now appears to be somewhat cheap to its peers, indicating that if its recent weakness is due to speculators dumping their positions, there is little reason to fear continued relative declines.

As for the future, of course, it’s one thing to say that ‘spreads are unsustainable and so are government yields’ and it’s quite another to forecast just how and when a more economically sustainable environment will take effect. It could be years. The same caution applies for an end to the overpricing of issues with a minimum rate guarantee. There could be a reversal, particularly if Trump’s international trade policies cause a severe recession or even a depression. And, of course, I could be just plain wrong about the sustainability of the current environment.

On the other hand, I will pass on my observation that international interest in the Canadian preferred share market is increasing, as other Floating Rate indices globally are doing much better. Consider, for example the Solactive Australian Bank Senior Floating Rate Bond Index, which “provides exposure to the largest and most liquid floating rate debt securities issued by selected Australian banks. The index is comprised of investment grade floating rate debt securities denominated in AUD and calculated as a Total Return Index” (LINK although the index constituents currently all have a remaining term of less than five years), and the S&P U.S. Floating Rate Preferred Stock Index.

Yields on preferred shares of all stripes are extremely high compared to those available from other investments of similar quality. As I told John Heinzl in an eMail interview in late November, 2018, the best advice I can offer investors remains Shut up and clip your coupons!

I think that a broad, sustainable rally in FixedResets will require higher five-year Canada yields (or a widespread expectation of them) … and although I’m sure this will happen eventually, it would be foolish to speculate on just when it will happen!

| Calculation of MAPF Sustainable Income Per Unit | ||||||

| Month | NAVPU | Portfolio Average YTW |

Leverage Divisor |

Securities Average YTW |

Capital Gains Multiplier |

Sustainable Income per current Unit |

| June, 2007 | 9.3114 | 5.16% | 1.03 | 5.01% | 1.3240 | 0.3524 |

| September | 9.1489 | 5.35% | 0.98 | 5.46% | 1.3240 | 0.3773 |

| December, 2007 | 9.0070 | 5.53% | 0.942 | 5.87% | 1.3240 | 0.3993 |

| March, 2008 | 8.8512 | 6.17% | 1.047 | 5.89% | 1.3240 | 0.3938 |

| June | 8.3419 | 6.034% | 0.952 | 6.338% | 1.3240 | $0.3993 |

| September | 8.1886 | 7.108% | 0.969 | 7.335% | 1.3240 | $0.4537 |

| December, 2008 | 8.0464 | 9.24% | 1.008 | 9.166% | 1.3240 | $0.5571 |

| March 2009 | $8.8317 | 8.60% | 0.995 | 8.802% | 1.3240 | $0.5872 |

| June | 10.9846 | 7.05% | 0.999 | 7.057% | 1.3240 | $0.5855 |

| September | 12.3462 | 6.03% | 0.998 | 6.042% | 1.3240 | $0.5634 |

| December 2009 | 10.5662 | 5.74% | 0.981 | 5.851% | 1.1141 | $0.5549 |

| March 2010 | 10.2497 | 6.03% | 0.992 | 6.079% | 1.1141 | $0.5593 |

| June | 10.5770 | 5.96% | 0.996 | 5.984% | 1.1141 | $0.5681 |

| September | 11.3901 | 5.43% | 0.980 | 5.540% | 1.1141 | $0.5664 |

| December 2010 | 10.7659 | 5.37% | 0.993 | 5.408% | 1.0298 | $0.5654 |

| March, 2011 | 11.0560 | 6.00% | 0.994 | 5.964% | 1.0298 | $0.6403 |

| June | 11.1194 | 5.87% | 1.018 | 5.976% | 1.0298 | $0.6453 |

| September | 10.2709 | 6.10% Note |

1.001 | 6.106% | 1.0298 | $0.6090 |

| December, 2011 | 10.0793 | 5.63% Note |

1.031 | 5.805% | 1.0000 | $0.5851 |

| March, 2012 | 10.3944 | 5.13% Note |

0.996 | 5.109% | 1.0000 | $0.5310 |

| June | 10.2151 | 5.32% Note |

1.012 | 5.384% | 1.0000 | $0.5500 |

| September | 10.6703 | 4.61% Note |

0.997 | 4.624% | 1.0000 | $0.4934 |

| December, 2012 | 10.8307 | 4.24% | 0.989 | 4.287% | 1.0000 | $0.4643 |

| March, 2013 | 10.9033 | 3.87% | 0.996 | 3.886% | 1.0000 | $0.4237 |

| June | 10.3261 | 4.81% | 0.998 | 4.80% | 1.0000 | $0.4957 |

| September | 10.0296 | 5.62% | 0.996 | 5.643% | 1.0000 | $0.5660 |

| December, 2013 | 9.8717 | 6.02% | 1.008 | 5.972% | 1.0000 | $0.5895 |

| March, 2014 | 10.2233 | 5.55% | 0.998 | 5.561% | 1.0000 | $0.5685 |

| June | 10.5877 | 5.09% | 0.998 | 5.100% | 1.0000 | $0.5395 |

| September | 10.4601 | 5.28% | 0.997 | 5.296% | 1.0000 | $0.5540 |

| December, 2014 | 10.5701 | 4.83% | 1.009 | 4.787% | 1.0000 | $0.5060 |

| March, 2015 | 9.9573 | 4.99% | 1.001 | 4.985% | 1.0000 | $0.4964 |

| June, 2015 | 9.4181 | 5.55% | 1.002 | 5.539% | 1.0000 | $0.5217 |

| September | 7.8140 | 6.98% | 0.999 | 6.987% | 1.0000 | $0.5460 |

| December, 2015 | 8.1379 | 6.85% | 0.997 | 6.871% | 1.0000 | $0.5592 |

| March, 2016 | 7.4416 | 7.79% | 0.998 | 7.805% | 1.0000 | $0.5808 |

| June | 7.6704 | 7.67% | 1.011 | 7.587% | 1.0000 | $0.5819 |

| September | 8.0590 | 7.35% | 0.993 | 7.402% | 1.0000 | $0.5965 |

| December, 2016 | 8.5844 | 7.24% | 0.990 | 7.313% | 1.0000 | $0.6278 |

| March, 2017 | 9.3984 | 6.26% | 0.994 | 6.298% | 1.0000 | $0.5919 |

| June | 9.5313 | 6.41% | 0.998 | 6.423% | 1.0000 | $0.6122 |

| September | 9.7129 | 6.56% | 0.998 | 6.573% | 1.0000 | $0.6384 |

| December, 2017 | 10.0566 | 6.06% | 1.004 | 6.036% | 1.0000 | $0.6070 |

| March, 2018 | 10.2701 | 6.22% | 1.007 | 6.177% | 1.0000 | $0.6344 |

| June | 10.2518 | 6.22% | 0.995 | 6.251% | 1.0000 | $0.6408 |

| September | 10.2965 | 6.62% | 1.018 | 6.503% | 1.0000 | $0.6696 |

| December, 2018 | 8.6875 | 7.16% | 0.997 | 7.182% | 1.0000 | $0.6240 |

| March, 2019 | 8.4778 | 7.09% | 1.007 | 7.041% | 1.0000 | $0.5969 |

| June | 8.0896 | 7.33% | 0.996 | 7.359% | 1.0000 | $0.5953 |

| September | 7.7948 | 7.96% | 0.998 | 7.976% | 1.0000 | $0.6217 |

| November, 2019 | 7.8207 | 6.18% | 1.004 | 6.155% | 1.0000 | $0.4814 |

| NAVPU is shown after quarterly distributions of dividend income and annual distribution of capital gains. Portfolio YTW includes cash (or margin borrowing), with an assumed interest rate of 0.00% The Leverage Divisor indicates the level of cash in the account: if the portfolio is 1% in cash, the Leverage Divisor will be 0.99 Securities YTW divides “Portfolio YTW” by the “Leverage Divisor” to show the average YTW on the securities held; this assumes that the cash is invested in (or raised from) all securities held, in proportion to their holdings. The Capital Gains Multiplier adjusts for the effects of Capital Gains Dividends. On 2009-12-31, there was a capital gains distribution of $1.989262 which is assumed for this purpose to have been reinvested at the final price of $10.5662. Thus, a holder of one unit pre-distribution would have held 1.1883 units post-distribution; the CG Multiplier reflects this to make the time-series comparable. Note that Dividend Distributions are not assumed to be reinvested. Sustainable Income is the resultant estimate of the fund’s dividend income per current unit, before fees and expenses. Note that a “current unit” includes reinvestment of prior capital gains; a unitholder would have had the calculated sustainable income with only, say, 0.9 units in the past which, with reinvestment of capital gains, would become 1.0 current units. |

||||||

| DeemedRetractibles are comprised of all Straight Perpetuals (both PerpetualDiscount and PerpetualPremium) issued by BMO, BNS, CM, ELF, GWO, HSB, IAG, MFC, NA, RY, SLF and TD, which are not exchangable into common at the option of the company or the regulator (definition refined in May, 2011). These issues are analyzed as if their prospectuses included a requirement to redeem at par on or prior to 2022-1-31 (banks) or the Deemed Maturity date for insurers and insurance holding companies (see below)), in addition to the call schedule explicitly defined. See the Deemed Retractible Review: September 2016 for the rationale behind this analysis.

The same reasoning is also applied to FixedResets from these issuers, other than explicitly defined NVCC from banks. In November, 2019, the assumption of DeemedRetraction was cancelled in the wake of the IAIS decision included in ICS 2.0. |

||||||

| The Deemed Maturity date for insurers was set at 2022-1-31 at the commencement of the process in February, 2011. It was extended to 2025-1-31 in April, 2013 and to 2030-1-31 in December, 2018. In November, 2019, the assumption of DeemedRetraction was cancelled in the wake of the IAIS decision included in ICS 2.0. | ||||||

| Yields for September, 2011, to January, 2012, were calculated by imposing a cap of 10% on the yields of YLO issues held, in order to avoid their extremely high calculated yields distorting the calculation and to reflect the uncertainty in the marketplace that these yields will be realized. From February to September 2012, yields on these issues have been set to zero. All YLO issues held were sold in October 2012. | ||||||

These calculations were performed assuming constant contemporary GOC-5 and 3-Month Bill rates, as follows:

| Canada Yields Assumed in Calculations | ||

| Month-end | GOC-5 | 3-Month Bill |

| September, 2015 | 0.78% | 0.40% |

| December, 2015 | 0.71% | 0.46% |

| March, 2016 | 0.70% | 0.44% |

| June | 0.57% | 0.47% |

| September | 0.58% | 0.53% |

| December, 2016 | 1.16% | 0.47% |

| March, 2017 | 1.08% | 0.55% |

| June | 1.35% | 0.69% |

| September | 1.79% | 0.97% |

| December, 2017 | 1.83% | 1.00% |

| March, 2018 | 2.06% | 1.08% |

| June | 1.95% | 1.22% |

| September | 2.33% | 1.55% |

| December, 2018 | 1.88% | 1.65% |

| March, 2019 | 1.46% | 1.66% |

| June | 1.34% | 1.66% |

| September | 1.41% | 1.66% |

| November, 2019 | 1.51% | 1.67% |

The large drop this month in the projected sustainable yield is due to the fact that in November, 2019, the assumption of DeemedRetraction was cancelled in the wake of the IAIS decision included in ICS 2.0.

I will also note that the sustainable yield calculated above is not directly comparable with any yield calculation currently reported by any other preferred share fund as far as I am aware. The Sustainable Yield depends on:

i) Calculating Yield-to-Worst for each instrument and using this yield for reporting purposes;

ii) Using the contemporary value of Five-Year Canadas to estimate dividends after reset for FixedResets. The assumption regarding the five-year Canada rate has become more important as the proportion of low-spread FixedResets in the portfolio has increased.

iii) Making the assumption that deeply discounted NVCC non-compliant issues from both banks and insurers, both Straight and FixedResets will be redeemed at par on their DeemedMaturity date as discussed above.

It should be noted that I have been unable to explain the very strong performance of Floor issues over the past year relative to their non-Floor counterparts. See the discussions on PrefBlog at LINK, LINK and LINK.

The industry, always willing to cater to trends, actually has an ETF that came out in late September 2019 called “Dividend Stability Preferred Share ETF” [ a catchy name, eh?] which seeks to appeal to those investors who believe in Floor Resets. I don’t know whether buying activity from this ETF has helped in that market .

Regardless, I too wonder about the appeal of the Floor issues. Of the 40 Floor issues on the market, the great majority trade at a premium to par and have what I would consider generous reset spreads [around 4.00% +]. Arguably imho this means a [comparatively] higher risk of them being called on their first available reset date, so you want to at least be aware of the Yield-to-Reset. Evolve does not disclose its Yield-to-Reset, but Scotia has a sheet as of Dec. 6 that shows YTR’s of 3.14, 4.17, 5.03, 4.04, 3.43, 4.36 and 3.51% for Evolve’s top 7 Floors.

FWIW, I use the Rate Reset Calculator [ for which see Prefblog March 26 2015] to run YTW scenarios for non-Floors based on a 10 year minimum holding period, and then play with different GOC rates and price variables including further drops of say 10-12%. It’s not sophisticated but it’s enough to show me that the current pricing of many non-Floors can provide for “protection” — a 10-year YTW comfortably in the range of 5.25% + in its own right even on pessimistic assumptions — and always the better the longer the holding period. I also note James’ post above showing a YTW for his MAPF of 6.155%, although that will presumably come down as a result of the cancellation of DeemedRetraction.

The first paragraph above is a quote from James’s post — I haven’t learned how to cut and paste from the original yet 🙁

so you want to at least be aware of the Yield-to-Reset.

I prefer Yield-to-Worst … there are some Floor Issues for which the Yield-to-Worst Scenario is existence to perpetuity.

Rate Reset Calculator [ for which see Prefblog March 26 2015]

I prefer the link What Is The Yield Of HSE.PR.A?, as that gives detailed instructions for the use of the calculator.

I haven’t learned how to cut and paste from the original yet

I use italics in the comments to indicate a quote: <, i, >, TEXT, <, /, i, >.

Remove commas and spacing and there you have it.

Sometimes, if I’m quoting an entire paragraph, I’ll blockquote it – replace both instances of “i” in the above with the word “blockquote”.

Basic HTML coding is fairly simple, and there are lots of tutorials available on the Internet. More advanced stuff may be produced using PHP, an interpreted coding language based loosely on C++. If you know C++, you’ll find PHP (a) easy to learn because 99% of it is the same thing, and (b) infuriating, because every now and then the syntax differs slightly and you go crazy. But it’s very useful!

Geez, when I think how much money I spent having a guy build my website back in 2000 when it was an esoteric art …. and just think, there are people still complaining that schools don’t teach cursive any more!

Thank you for your patience with a posting-challenged commentator!