OSFI has announced:

OSFI is issuing this statement to reinforce guidance around the design of the regulatory treatment of Additional Tier 1 and Tier 2 capital instruments.

Canada’s capital regime preserves creditor hierarchy which helps to maintain financial stability.

If a deposit-taking bank reaches the point of non-viability, OSFI’s capital guidelines require Additional Tier 1 and Tier 2 capital instruments to be converted into common shares in a manner that respects the hierarchy of claims in liquidation. This results in significant dilution to existing common shareholders.

Such a conversion ensures that Additional Tier 1 and Tier 2 holders are entitled to a more favorable economic outcome than existing common shareholders who would be the first to suffer losses. These capital requirements are administered by OSFI as well as the conversion of the Additional Tier 1 and Tier 2 capital instruments.

Additional Tier 1 and Tier 2 instruments are and will remain an important component of the capital structure of Canadian deposit-taking banks.

Canadians can be confident that we have a sound and effective regulatory and supervisory foundation that works to protect depositors and creditors.

And the European Central Bank teamed up with other regulators to announce:

ECB Banking Supervision, the Single Resolution Board and the European Banking Authority welcome the comprehensive set of actions taken yesterday by the Swiss authorities in order to ensure financial stability.

The European banking sector is resilient, with robust levels of capital and liquidity.

The resolution framework implementing in the European Union the reforms recommended by the Financial Stability Board after the Great Financial Crisis has established, among others, the order according to which shareholders and creditors of a troubled bank should bear losses.

In particular, common equity instruments are the first ones to absorb losses, and only after their full use would Additional Tier 1 be required to be written down. This approach has been consistently applied in past cases and will continue to guide the actions of the SRB and ECB banking supervision in crisis interventions.

Additional Tier 1 is and will remain an important component of the capital structure of European banks.

This announcement appears to be due to the treatment of AT1 instruments in the collapse of Credit Suisse:

Trading in Credit Suisse’s bonds rose sharply at the end of last week as strain in the banking sector mounted, according to official trade data.

There were two types of trades that the investors conducted: one that is set to make money, the other that is set to lose money.

…

The second trade that investors plowed into was in Credit Suisse’s roughly $17 billion of so-called AT1 bonds. This is a special type of debt issued by banks that can be converted to equity capital should they run into trouble. This made that debt inherently riskier to hold, because it carried the chance that bondholders could be wiped out. Investors saw the buying of the bonds for as low as 20 cents on the dollar as a kind of lottery ticket — a long shot, but with a big reward if it had worked out.

…

On Sunday, the Swiss Financial Market Supervisory Authority, or Finma, approved a deal for UBS to take over its smaller rival. “The transaction and the measures taken will ensure stability for the bank’s customers and for the financial center,” said a statement from Finma.

It said that the AT1 bonds would be wiped out as part of the deal, to add roughly $16 billion of equity to support UBS’s takeover.

That raised eyebrows among some investors because it upended the normal order in which holders of different assets of a company expect to be paid in bankruptcy. Stock investors are at the bottom of that repayment list and usually lose all their money ahead of other investors.

However, in this instance, regulators chose to trigger the conversion of the AT1 bonds to equity capital to help the bank, while still offering Credit Suisse shareholders one UBS share for every 22.48 Credit Suisse shares held.

As further explained:

The eleventh-hour Swiss rescue is backed by a massive government guarantee, helping prevent what would have been one of the largest banking collapses since the fall of Lehman Brothers in 2008.

However, the Swiss regulator decided Credit Suisse’s additional tier-1 (AT1) bonds with a notional value of $17 billion will be valued at zero, angering some holders of the debt who thought they would be better protected than shareholders.

AT1 bonds – a $275 billion sector also known as “contingent convertibles” or “CoCo” bonds – can be converted into equity or written off if a bank’s capital level falls below a certain threshold. The deal will also make UBS Switzerland’s only global bank and the Swiss economy more dependent on a single lender.

“Massive guarantee”? Yes:

The deal includes 100 billion Swiss francs ($108 billion) in liquidity assistance for UBS and Credit Suisse from the Swiss central bank.

To enable UBS to take over Credit Suisse, the federal government is providing a loss guarantee of a maximum of 9 billion Swiss francs for a clearly defined part of the portfolio, the government said.

This will be activated if losses are actually incurred on this portfolio. In that eventuality, UBS would assume the first 5 billion francs, the federal government the next 9 billion francs, and UBS would assume any further losses, the government said.

And UBS boasted:

UBS benefits from CHF 25 billion of downside protection from the transaction to support marks, purchase price adjustments and restructuring costs, and additional 50% downside protection on non-core assets.

This caused an immediate drop in the price of other AT1s:

The write-down to zero at Credit Suisse will produce the largest loss in the $275 billion AT1 market to date, dwarfing the 1.35 billion euros ($1.44 billion) bondholders of Spain’s Banco Popular lost in 2017.

Bid prices on AT1 bonds from banks, including Deutsche Bank , HSBC, UBS and BNP Paribas, were among those under pressure on Monday. They recovered marginally but were still down 6-11 points on the day, sending yields sharply higher, data from Tradeweb showed.

A UBS AT1 bond callable in January 2024 was trading at a yield of 27%, up from 12% on Friday, demonstrating how much more costly this type of debt could become in the wake of the Credit Suisse rescue.

…

Funds that track AT1 debt also fell sharply.

Invesco’s AT1 Capital Bond exchange-traded fund was last down 6%, having been over 10% lower earlier. WisdomTree’s AT1 CoCo bond ETF was indicated 9% lower.

At Credit Suisse, the bank’s AT1 bonds were bid as low as 1 cent on the dollar on Monday as investors braced for the wipeout.

But the lawyers will get rich, as usual:

Lawyers from Switzerland, the United States and UK are talking to a number of Credit Suisse Additional Tier 1 (AT1) bond holders about possible legal action after the state-backed rescue of Credit Suisse by UBS wiped out AT1 bonds, law firm Quinn Emanuel Urquhart & Sullivan said on Monday.

Quinn Emanuel said it was in discussions with Credit Suisse AT1 bondholders representing a “significant percentage” of the total notional value the instruments. Quinn Emanuel did not name the bondholders.

Under the UBS-Credit Suisse merger deal, holders of Credit Suisse AT1 bonds will get nothing, while shareholders, who usually rank below bondholders in terms of who gets paid when a bank or company collapses, will receive $3.23 billion.

In Switzerland, the bonds’ terms state that in a restructuring, the financial watchdog is under no obligation to adhere to the traditional capital structure hierarchy, which is how Credit Suisse AT1 bondholders lost out.

And so … what it are the implications for Canadian NVCC preferred shares? I have to say: not much, based on the following two factors.

First, it looks like Credit Suisse was in even worse shape than everyone thought last Friday. As reported above, “shareholders, who usually rank below bondholders in terms of who gets paid when a bank or company collapses, will receive $3.23 billion.” This is after wiping out 16- or 17-billion in AT1 capital (reporting differs according to source, presumably due to rounding and difference in exchange rate conversion). So, if we take these figures at face value – i.e., there hasn’t been too much jiggery-pokery in the values received – the Credit Suisse common had a market value of about NEGATIVE 14-billion on Friday, a far cry from the 8-billion valuation at the close on Friday, never mind the values of previous years:

This is before considering the value of the ‘massive guarantee’ that the Swiss central bank has given UBS, which are quite substantial. So it would seem that AT1 holders wouldn’t have gotten much of a recovery anyway.

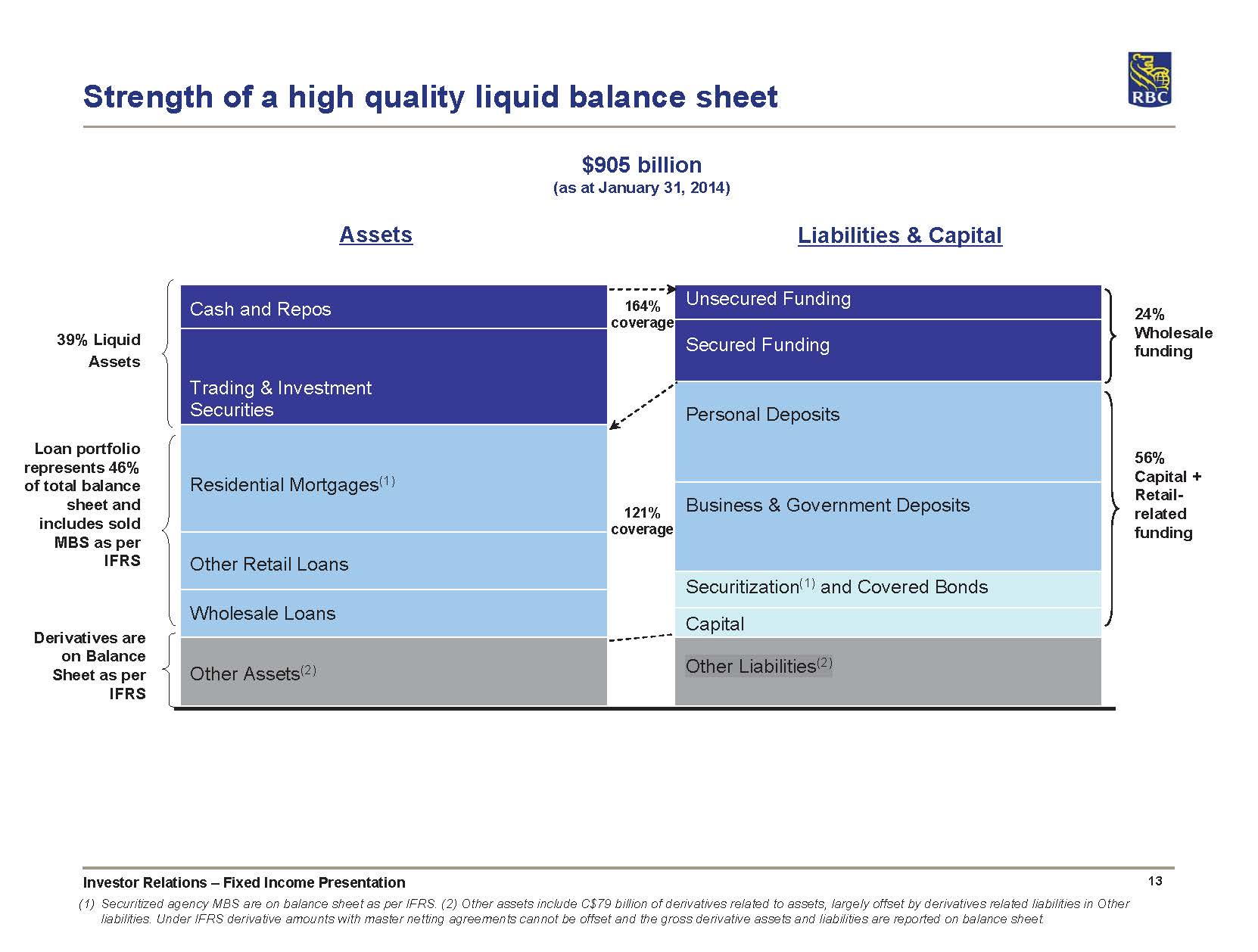

Secondly, ‘when in doubt, look at the prospectus’, as the adage goes. Here’s the prospectus for RY.PR.H, taken from RBC’s preferred share page:

Upon the occurrence of a Trigger Event (as defined below), each outstanding Series BB Preferred Share and each outstanding Series BC Preferred Share will automatically and immediately be converted, on a full and permanent basis, into a number of Common Shares equal to (Multiplier x Share Value) ÷ Conversion Price (rounding down, if necessary, to the nearest whole number of Common Shares) (an “NVCC Automatic Conversion”). For the purposes of the foregoing:

“Conversion Price” means the greater of (i) $5.00, and (ii) the Current Market Price of the Common Shares. The floor price of $5.00 is subject to adjustment in the event of (i) the issuance of Common Shares or securities exchangeable for or convertible into Common Shares to all holders of Common Shares as a stock dividend, (ii) the subdivision, redivision or change of the Common Shares into a greater number of Common Shares, or (iii) the reduction, combination or consolidation of the Common Shares into a lesser number of Common Shares. The adjustment shall be computed to the nearest one-tenth of one cent provided that no adjustment of the Conversion Price shall be required unless such adjustment would require an increase or decrease of at least 1% of the Conversion Price then in effect.

“Current Market Price” of the Common Shares means the volume weighted average trading price of the Common Shares on the TSX, if such shares are then listed on the TSX, for the 10 consecutive trading days ending on the trading day preceding the date of the Trigger Event. If the Common Shares are not then listed on the TSX, for the purpose of the foregoing calculation reference shall be made to the principal securities exchange or market on which the Common Shares are then listed or quoted or, if no such trading prices are available, “Current Market Price” shall be the fair value of the Common Shares as reasonably determined by the board of directors of the Bank.

“Multiplier” means 1.0.

“Share Value” means $25.00 plus declared and unpaid dividends as at the date of the Trigger Event.

So, mainly there’s no ‘writedown to zero’ provision, which is one good thing. And secondly, on a trigger event they’re converted to common at a defined price.

It’s not all rosy! The conversion price for the common is defined as the VWAP for two weeks prior to the Trigger (or $5, it that’s higher, which could very well be the case. I bet nobody saw Credit Suisse being taken out for less than $1/share!), and that could be substantially higher than the price at the end of the period, or the price received in some kind of takeover or recapitalization scenario. As a mitigating factor, the value converted at this conversion price is par, or roughly 50% higher than what RY preferreds are trading at now. But the main thing is that the effects of a trigger are conversion into common, which means that whatever else might be the case, preferred shareholders will get some kind of recovery after a trigger event (as long as the common shareholders get something, which will not necessarily be the case), and not be left out in the cold as the Credit Suisse AT1 holders have been. And, as I have always said, expectations for preferred shareholders (NVCC or otherwise) of an operating company in a bankruptcy scenario are basically zero anyway, so any recovery should be considered a bonus!

Now, make no mistake: I do not like Canada’s implementation of the NVCC rules. I don’t like the ‘low trigger’, which basically guarantees that any loss will take place at a time of maximum confusion (as well as acting entirely to mitigate damage to senior creditors, as opposed to forestalling problems before they get more serious), and I don’t like the arbitrary power granted to OSFI to declare a ‘Trigger Event’, which circumvents the courts and gives civil servants one heckofa lot of power. But, it appears to me, a Credit Suisse scenario is not something to worry about.

Update, 2023-3-22: DBRS has released an analysis titled Credit Suisse’s AT1 Controversy Unlikely Outside Switzerland (at time of writing, no password or log-in was required):

Credit Suisse´s AT1 Write-Down Based on a Specific Swiss Contractual Clause

It is important to note that FINMA has not framed the sale of Credit Suisse AG to UBS as a resolution action (restructuring under Swiss terminology). This is a key consideration, as under a resolution, FINMA could have written-down the AT1s but only after CS´s shareholders equity had been completely written-off and cancelled (see link). We consider that FINMA avoided initiating a resolution, asthat could have had unknown consequences for the Swiss and global financial markets. In addition, CS was still not fully resolvable as explained by FINMA in their last Resolution Report in 2022 (see link). As a result, opening resolution procedures (even just during the weekend) might have had important implications on an operative level (derivatives, deposits, other critical contracts). Nevertheless, in order to close the deal, it seems that UBS required downside protection. The deal was closed after granting this protection by writing-off CHF 15.8 billion of AT1s and adding government protection of CHF 9 billion (which applies only after UBS has absorbed the first CHF 5 billion of losses).

We understand that FINMA’s interpretation was that the AT1 write-down was legally possible under a contractual clause called “viability event”. In particular, according to the AT1 prospectus, an irrevocable commitment of extraordinary support from the public sector would trigger this “viability event” thus allowing the total write-down of AT1s. FINMA interpreted the CHF 9 billion protection as extraordinary support from the public sector. However, some investors are arguing that the public sector support was not given to CS but to UBS. As a result, we anticipate CS AT1 bondholders could initiate legal action against these decisions. Furthermore, we observe that the possibility

to writedown and cancel AT1 bondholder rights based on this specific contractual clause is a feature particular to the Swiss banks’ AT1s. Swiss banks issued some of the first AT1s after the previous financial crisis and they were intended to strengthen a bank, both as going concern as well as a gone concern situation.

Implications for Other Resolution Jurisdictions

We view the sale of CS to UBS as positive for financial stability, reducing potential negative market reaction and contagion from a disorderly resolution or bankruptcy of CS. However, it raises some questions as to how authorities will apply their powers. We note some important takeaways from this case, that are applicable to all regimes, including the EU, UK and Canada. First, the complexity of resolution and quasi resolution situations makes the reality different from theoretical resolution planning. Second, the interpretation of the law made by national authorities could be different from what markets expect in these situations. Third, that bail-in strategies for Globally Systemically Important Banks (G-SIB) are difficult and the too big to fail issue is still present.

Nevertheless, we also consider that there are some differences between Switzerland and other regions. Specifically, we view that the decision to impose larger losses on the AT1 securities than on shareholders will not set a precedent in the EU, UK or Canada. We consider that the instruments in these regimes have different wording and authorities have been vocal to clarify that AT1 securities are always senior to equity.

Update, 2023-3-23: DBRS has released a commentary on LRCNs that is very similar in tone to their piece on preferred shares.