There are high level worries about the Hong Kong property market:

Hong Kong home prices are the highest relative to shares of the city’s publicly-traded developers in almost two decades. For Bocom International Holdings Co. analyst Alfred Lau, that’s a sign that the property market’s about to drop as much as 20 percent.

…

While home values kept rising in August, sales showed signs of a slowdown. The number of transactions tumbled 37 percent from a year earlier amid concern about China’s economic outlook and the prospect of higher borrowing costs as the Federal Reserve prepares to raise interest rates. Analysts including JPMorgan Chase & Co.’s Cusson Leung and Morgan Stanley’s Praveen K. Choudhary are calling for Hong Kong property prices to slide as much as 10 percent next year.

…

The Hong Kong Monetary Authority said in a report Friday the risk of a “downward adjustment” in home prices is increasing amid volatility in global and domestic financial markets.

One wonders what implications that will have for Vancouver and, to a lesser extent, for Toronto.

We may see more rights offerings in Canada:

On September 24, 2015, the Canadian Securities Administrators (CSA) announced the adoption of a streamlined prospectus-exempt rights offering process, which is aimed at providing reporting issuers with greater access to this prospectus exemption. Rights offerings permit issuers to distribute to their existing securityholders rights to purchase securities, generally at a discount to the prevailing market price. These offerings are often viewed as a fair way to raise capital because they protect existing investors from dilution. The rights offering prospectus exemption has historically not been frequently used in Canada, owing to the time and cost associated with the current regime. Under the new regime, none of the materials provided to securityholders will be reviewed by regulators prior to their use, substantially reducing the time frame in which an issuer can complete a rights offering. The new rights offering prospectus exemption will be available only to reporting issuers (other than investment funds) issuing an existing class of securities.

The process for completing a rights offering under the streamlined new prospectus exemption and the required documentation are set out below.

- •Prior to the commencement of the exercise period for the rights, the issuer files a rights offering notice on SEDAR and sends it to all securityholders resident in Canada holding the class of securities to be issued on the exercise of the rights. The notice contains only basic information about the offering, such as the size of the offering, the steps required to participate in the offering and how to access the rights offering circular electronically. The CSA does not expect a rights offering notice to be longer than two pages.

- •Concurrently with the filing of the rights offering notice, the issuer files a rights offering circular on SEDAR (the issuer is not required to send the circular to securityholders). The rights offering circular includes, in question-and-answer format, limited disclosure regarding the distribution, such as information relating to the particulars of the offering, the sources and uses of funds available after the offering and insider participation in the offering. The issuer must also disclose in the circular any material facts or material changes that have not yet been disclosed and include a statement that there are no undisclosed material facts or materials changes in respect of the issuer. The circular also must be certified not to contain a misrepresentation by the issuer’s CEO, CFO and two of its directors. The CSA does not expect a rights offering circular to be longer than 10 pages.

- •The exercise period for the rights must be at least 21 days but not more than 90 days.

- •On the closing date of the offering, the issuer must issue and file on SEDAR a news release setting out, among other things, the aggregate proceeds of the distribution and the number of securities issued under the basic subscription privilege, any additional subscription privilege and stand-by commitment.

Under this new rights offering prospectus exemption, the permitted dilution under an exempt rights offering will be increased from the current 25% to 100% in any 12-month period, which should make the exemption more attractive to smaller issuers. Rights offerings that result in greater dilution will have to be conducted by way of a prospectus.

…

We expect that the new rights offering prospectus exemption will be well received by reporting issuers because it should reduce the time and cost associated with rights offerings, thereby making such offerings a more practical means of raising capital. Issuers that are not reporting issuers and that wish to raise capital from existing securityholders will now have to rely on the existing shareholder exemption or one of the other exemptions available under Canadian provincial securities laws, such as the accredited investor exemption or the private issuer exemption.

DBRS downgraded 31 European banks due to removal of systemic support:

DBRS Ratings Limited and DBRS Inc., collectively DBRS, have downgraded the senior debt and deposit ratings of 31 banking groups in Europe that had previously benefited from some uplift for systemic support. The short-term debt ratings of 13 banking groups were also downgraded. At the same time, positive fundamental trends have led to an upgrade of the Intrinsic Assessment of 10 banks, which has offset the removal of support uplift for these banks.

These rating actions conclude the reviews that were initiated on 20 May 2015. They reflect DBRS’s view that developments in European regulation and legislation mean that there is less certainty about the likelihood of timely systemic support. Overall, DBRS views this as negative for European banks’ senior bondholders, whilst noting that certain fundamental improvements – particularly in capitalisation – have offset some of the impact from these developments.

DBRS has reviewed and changed the support assessment for 46 banking groups to reflect DBRS’s view of the reduction in the predictability of systemic support. This has led to the removal of systemic support uplift from the senior debt ratings for a total of 31 banking groups, removing 1 notch of uplift from 29 banks and 2 notches of uplift from 2 banks. At the same time the Intrinsic Assessments (IAs) of 10 banks were raised by 1 notch, offsetting the impact of the removal of support uplift. In addition, the senior debt ratings of 5 banks were unaffected by the change in the support assessment, because their Intrinsic Assessments were already at the same level as or higher than the respective sovereign rating.

HSBC Holdings and hence HSBC Bank Canada, proud issuer of HSB.PR.C and HSB.PR.D, was caught in the sweep but preferred share ratings are unaffected:

DBRS Limited (collectively with DBRS Ratings Limited and DBRS Inc., DBRS) has today downgraded the Long-Term Deposits and Senior Debt of HSBC Bank Canada to A (high) from AA (low) and its Subordinated Debt ratings to “A” from A (high). The trend is now Stable. Today’s rating actions follow DBRS’s lowering of the ratings of HSBC Holdings plc, HSBC Bank Canada’s ultimate parent. DBRS has also removed the ratings from Under Review with Negative Implications, where they were placed on May 20, 2015. There is no change to the Short-Term Instruments rating nor to the Non-Cumulative Preferred Shares Class I rating of HSBC Bank Canada as a result of today’s actions.

Today’s rating actions are driven by DBRS’s having downgraded the senior debt and deposit ratings of a number of banking groups in Europe, including HSBC Holdings plc, that had previously benefited from some uplift for systemic support. These rating actions conclude the review that was initiated on May 20, 2015, and reflect DBRS’s view that developments in European regulation and legislation mean that there is less certainty about the likelihood of timely systemic support. Given HSBC Bank Canada’s position in HSBC’s global franchise, DBRS has assigned an SA1 designation to the bank, which implies strong and predictable support from the parent, should it be required. As a supported rating with a SA1 designation, HSBC Bank Canada’s rating will generally move in tandem with HSBC Holdings plc’s rating.

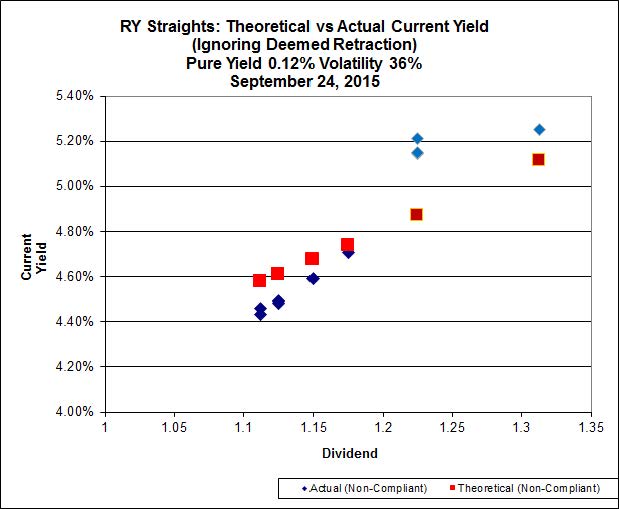

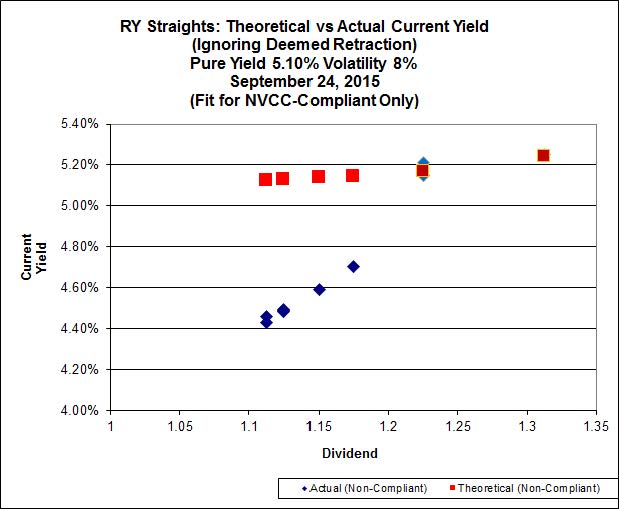

As part of a continuing series on well-known Canadian preferred share investors, PrefBlog proudly introduces the Wicked Witch of the East:

Click for Big

In a startling turn of events, not all classes of Canadian preferred share had a bad day today, as PerpetualDiscounts were off 23bp, FixedResets down 69bp and DeemedRetractibles gained 12bp. The Performance Highlights table continues to be absurdly long. Volume was very high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

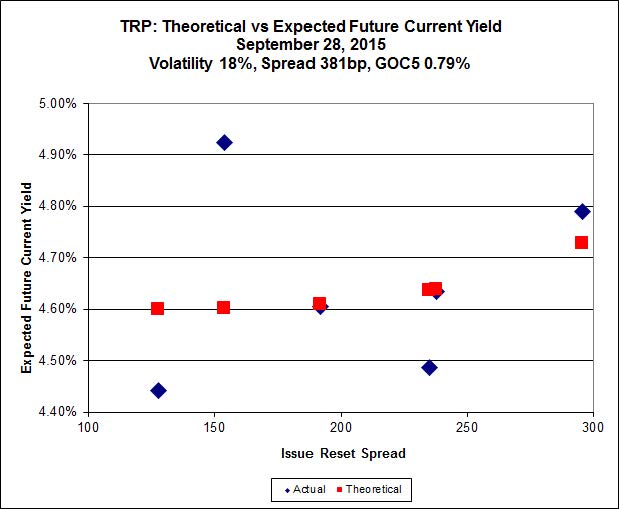

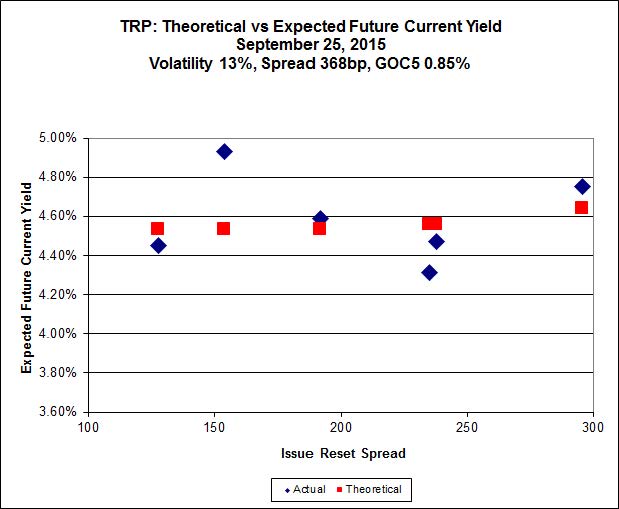

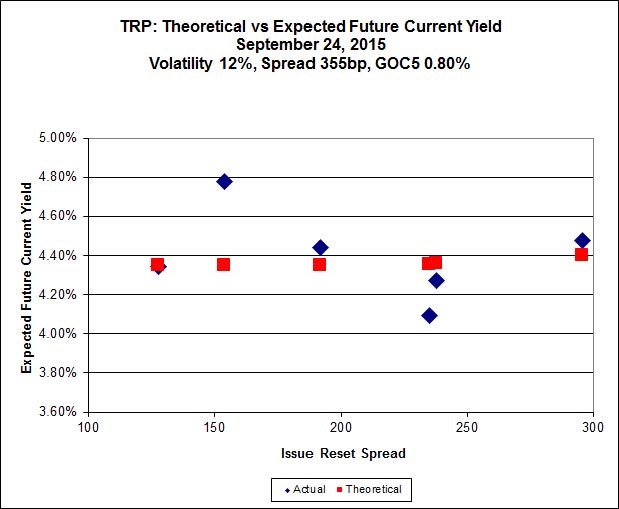

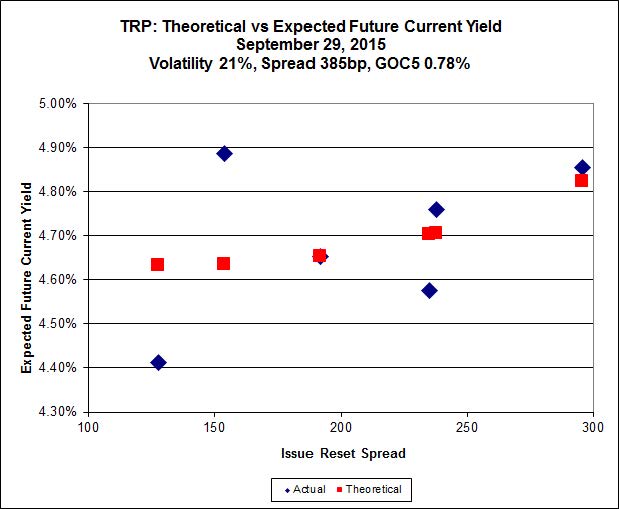

Here’s TRP:

Click for Big

Implied Volatility jumped again today.

TRP.PR.B, which resets 2020-6-30 at +235, is bid at 11.67 to be $0.55 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $0.64 cheap at its bid price of 11.87.

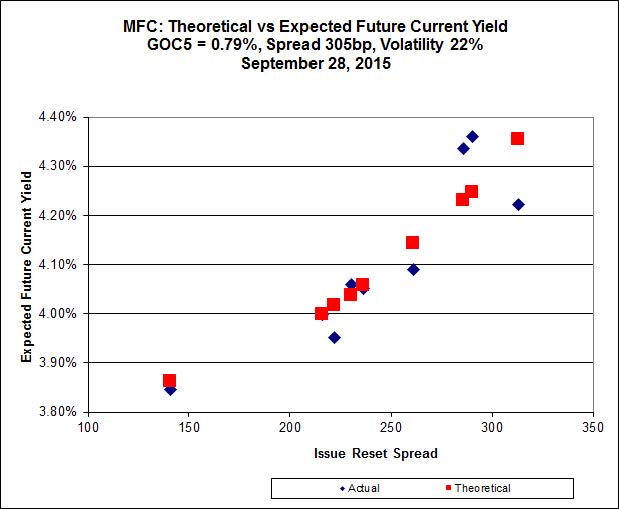

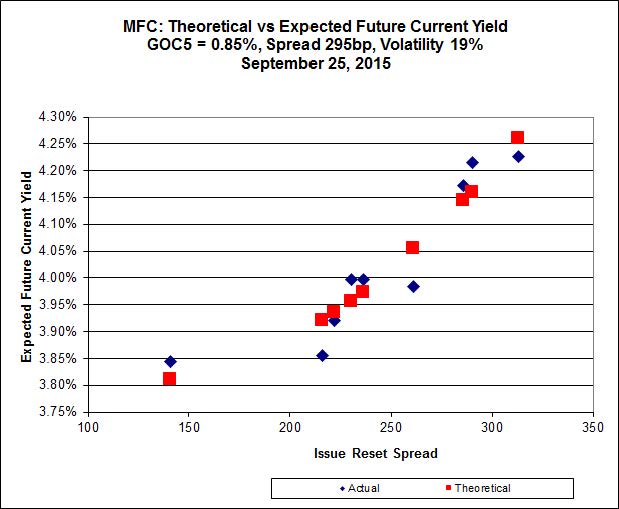

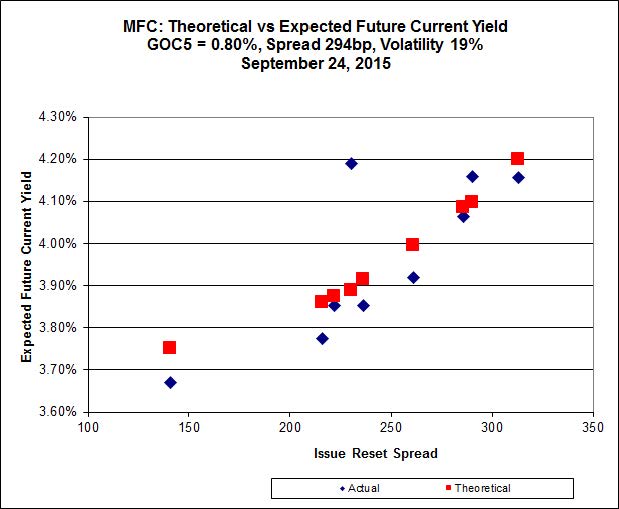

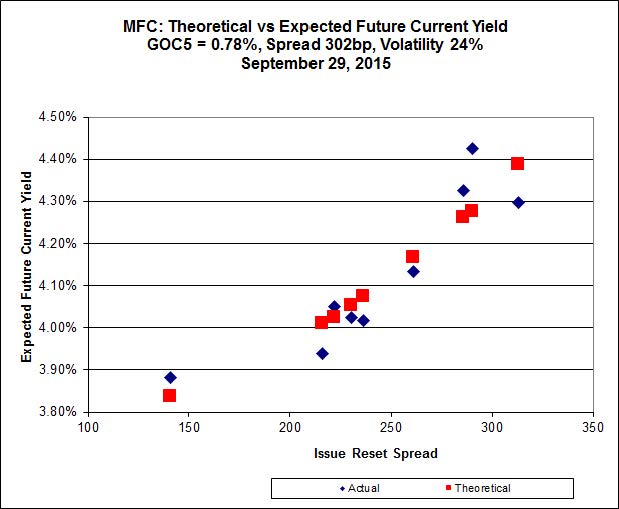

Click for Big

Another good fit today for MFC, with Implied Volatility edging upward.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 22.75 to be 0.48 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 20.79 to be 0.73 cheap.

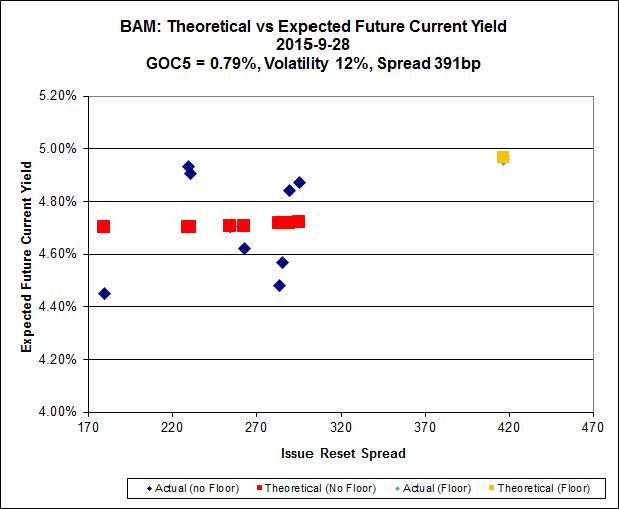

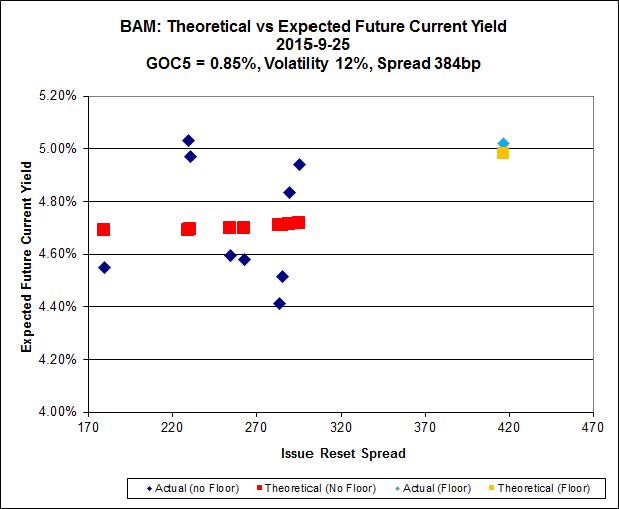

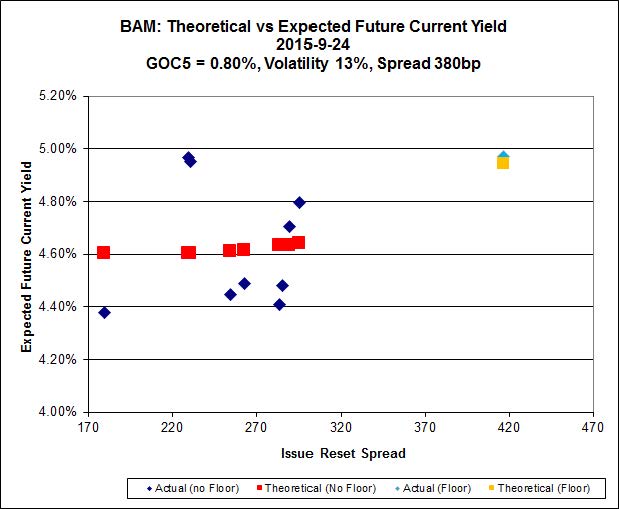

Click for Big

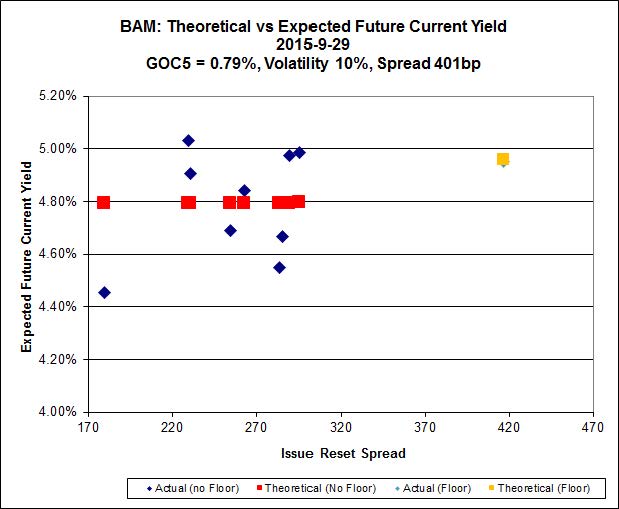

The fit on the BAM issues continues to be horrible. Note that the pending new issue has been added with a price of 25.00; the valuation effects of the rate floor have been ignored.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.30 to be $0.77 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.90 and appears to be $1.02 rich.

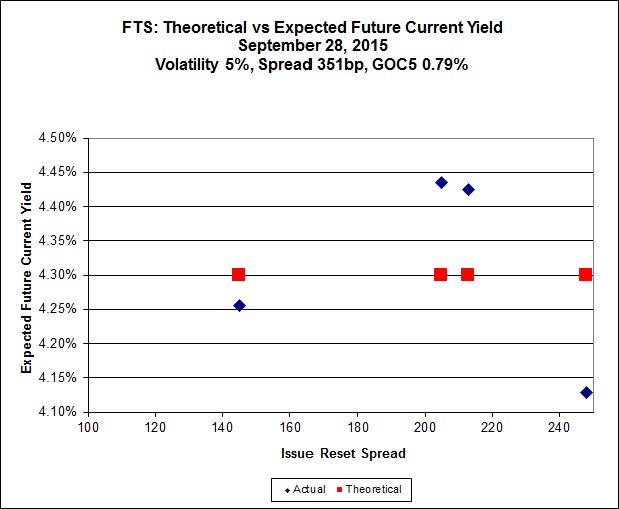

Click for Big

FTS.PR.M, with a spread of +248bp, and bid at 19.65, looks $0.65 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.45 and is $0.51 cheap.

Click for Big

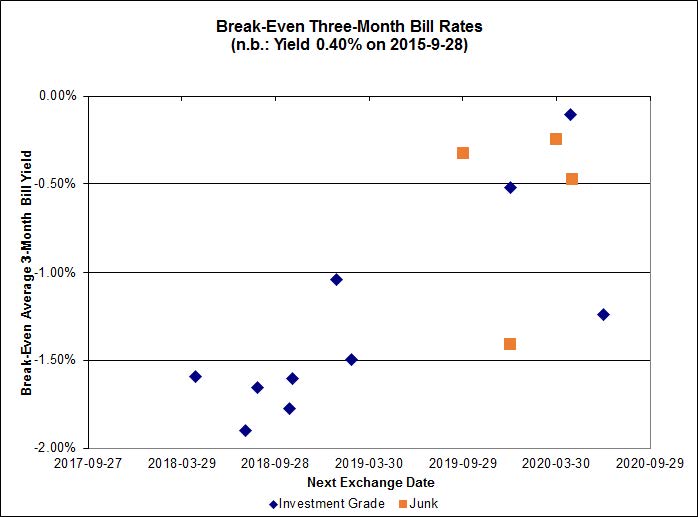

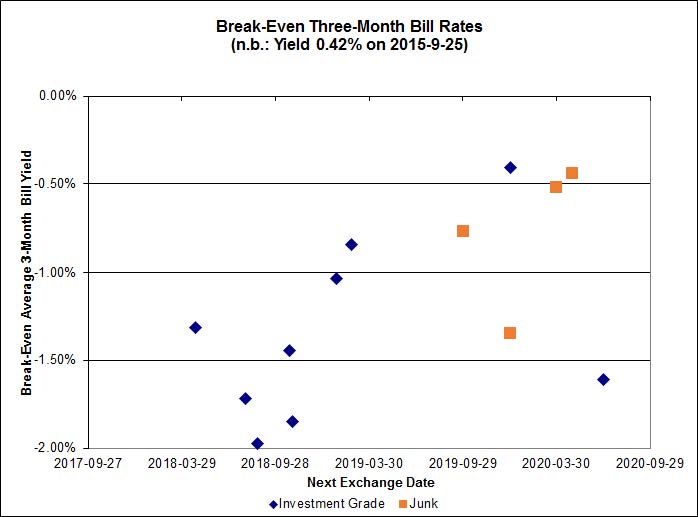

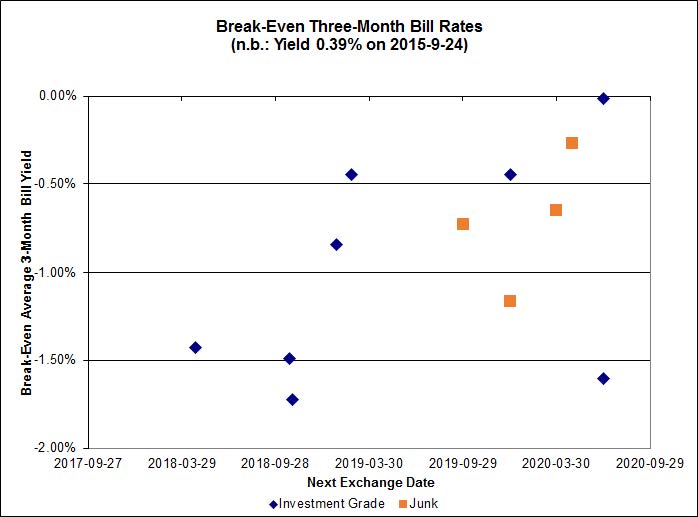

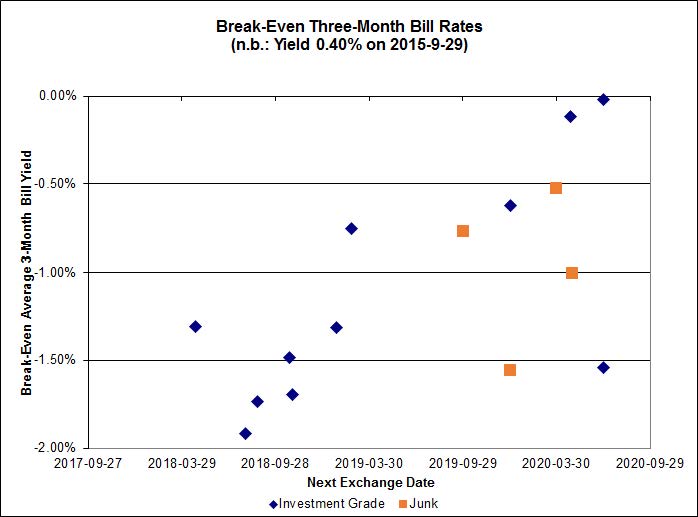

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.03%, with one outlier above 0.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -1.46% and other issues averaging -0.43%. There are two junk outliers above 0.00%.

Click for Big

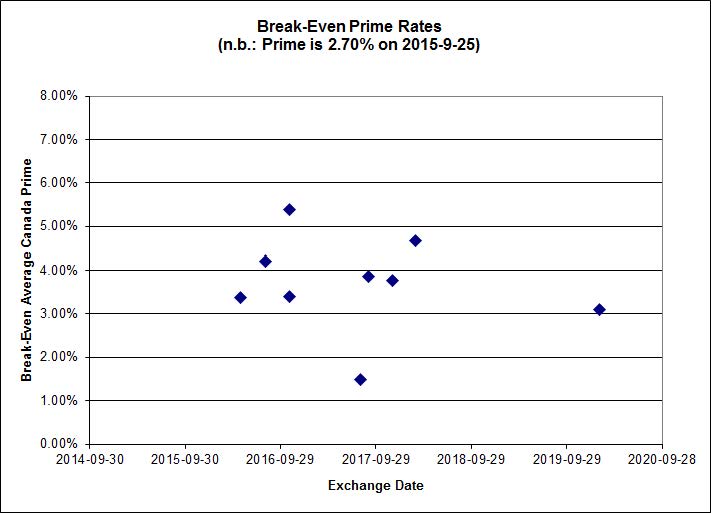

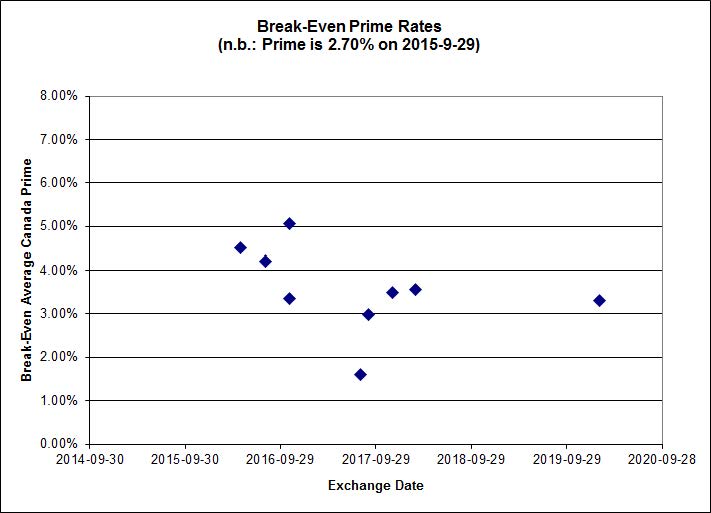

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.5999 % | 1,649.7 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.5999 % | 2,884.4 |

| Floater | 4.50 % | 4.54 % | 61,917 | 16.33 | 3 | -0.5999 % | 1,753.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0129 % | 2,761.4 |

| SplitShare | 4.50 % | 4.73 % | 64,991 | 3.02 | 4 | 0.0129 % | 3,236.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0129 % | 2,525.0 |

| Perpetual-Premium | 5.83 % | 5.88 % | 68,604 | 13.98 | 8 | -0.2162 % | 2,459.8 |

| Perpetual-Discount | 5.72 % | 5.78 % | 71,482 | 14.18 | 30 | -0.2278 % | 2,487.9 |

| FixedReset | 5.19 % | 4.71 % | 179,113 | 15.19 | 75 | -0.6938 % | 1,960.5 |

| Deemed-Retractible | 5.27 % | 5.15 % | 97,431 | 5.46 | 33 | 0.1216 % | 2,520.7 |

| FloatingReset | 2.65 % | 4.55 % | 62,346 | 5.83 | 9 | -0.5407 % | 2,055.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PF.B | FixedReset | -4.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 17.61 Evaluated at bid price : 17.61 Bid-YTW : 5.11 % |

| BIP.PR.A | FixedReset | -4.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 20.10 Evaluated at bid price : 20.10 Bid-YTW : 5.49 % |

| SLF.PR.I | FixedReset | -3.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.20 Bid-YTW : 7.12 % |

| TRP.PR.D | FixedReset | -2.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 16.60 Evaluated at bid price : 16.60 Bid-YTW : 5.01 % |

| BAM.PF.A | FixedReset | -2.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 5.20 % |

| MFC.PR.K | FixedReset | -2.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.52 Bid-YTW : 7.20 % |

| BAM.PR.Z | FixedReset | -2.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 5.22 % |

| BMO.PR.T | FixedReset | -2.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 18.25 Evaluated at bid price : 18.25 Bid-YTW : 4.44 % |

| BAM.PF.F | FixedReset | -2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 4.94 % |

| SLF.PR.J | FloatingReset | -2.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.50 Bid-YTW : 10.27 % |

| TRP.PR.E | FixedReset | -2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 17.10 Evaluated at bid price : 17.10 Bid-YTW : 4.94 % |

| BAM.PR.R | FixedReset | -2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 15.31 Evaluated at bid price : 15.31 Bid-YTW : 5.20 % |

| RY.PR.I | FixedReset | -2.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.47 Bid-YTW : 4.35 % |

| TRP.PR.F | FloatingReset | -2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 12.82 Evaluated at bid price : 12.82 Bid-YTW : 4.53 % |

| RY.PR.D | Deemed-Retractible | -2.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.28 Bid-YTW : 5.15 % |

| CU.PR.C | FixedReset | -2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.32 % |

| BAM.PR.N | Perpetual-Discount | -2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 19.74 Evaluated at bid price : 19.74 Bid-YTW : 6.06 % |

| MFC.PR.H | FixedReset | -1.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.75 Bid-YTW : 5.31 % |

| IAG.PR.G | FixedReset | -1.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.30 Bid-YTW : 6.52 % |

| BAM.PR.K | Floater | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 10.40 Evaluated at bid price : 10.40 Bid-YTW : 4.55 % |

| MFC.PR.G | FixedReset | -1.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.79 Bid-YTW : 6.23 % |

| BAM.PF.G | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 19.90 Evaluated at bid price : 19.90 Bid-YTW : 4.86 % |

| TD.PF.F | Perpetual-Discount | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 22.41 Evaluated at bid price : 22.71 Bid-YTW : 5.48 % |

| TD.PF.E | FixedReset | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 21.40 Evaluated at bid price : 21.40 Bid-YTW : 4.34 % |

| TRP.PR.G | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 19.26 Evaluated at bid price : 19.26 Bid-YTW : 4.93 % |

| FTS.PR.H | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 12.97 Evaluated at bid price : 12.97 Bid-YTW : 4.47 % |

| MFC.PR.F | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.10 Bid-YTW : 9.56 % |

| TRP.PR.A | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 14.51 Evaluated at bid price : 14.51 Bid-YTW : 4.92 % |

| MFC.PR.J | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.50 Bid-YTW : 6.18 % |

| CU.PR.F | Perpetual-Discount | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 19.75 Evaluated at bid price : 19.75 Bid-YTW : 5.77 % |

| BNS.PR.P | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.87 Bid-YTW : 3.98 % |

| BAM.PR.M | Perpetual-Discount | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 19.83 Evaluated at bid price : 19.83 Bid-YTW : 6.03 % |

| PWF.PR.P | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 14.35 Evaluated at bid price : 14.35 Bid-YTW : 4.27 % |

| HSE.PR.E | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 21.35 Evaluated at bid price : 21.35 Bid-YTW : 5.17 % |

| PWF.PR.O | Perpetual-Premium | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 24.78 Evaluated at bid price : 25.07 Bid-YTW : 5.88 % |

| ELF.PR.G | Perpetual-Discount | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 21.01 Evaluated at bid price : 21.01 Bid-YTW : 5.67 % |

| POW.PR.C | Perpetual-Premium | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 24.49 Evaluated at bid price : 24.72 Bid-YTW : 5.88 % |

| HSE.PR.A | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 13.22 Evaluated at bid price : 13.22 Bid-YTW : 4.90 % |

| IFC.PR.A | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.34 Bid-YTW : 9.40 % |

| PWF.PR.L | Perpetual-Discount | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 22.20 Evaluated at bid price : 22.47 Bid-YTW : 5.76 % |

| BMO.PR.Y | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 20.61 Evaluated at bid price : 20.61 Bid-YTW : 4.44 % |

| GWO.PR.N | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.10 Bid-YTW : 9.24 % |

| GWO.PR.L | Deemed-Retractible | 1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.31 Bid-YTW : 6.08 % |

| MFC.PR.L | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.66 Bid-YTW : 7.20 % |

| GWO.PR.R | Deemed-Retractible | 1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.52 Bid-YTW : 6.88 % |

| W.PR.H | Perpetual-Discount | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 23.20 Evaluated at bid price : 23.50 Bid-YTW : 5.86 % |

| CM.PR.Q | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 4.30 % |

| PWF.PR.F | Perpetual-Discount | 1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 22.71 Evaluated at bid price : 23.00 Bid-YTW : 5.80 % |

| RY.PR.J | FixedReset | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 4.39 % |

| BMO.PR.Z | Perpetual-Discount | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 22.83 Evaluated at bid price : 23.21 Bid-YTW : 5.46 % |

| NA.PR.S | FixedReset | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 19.24 Evaluated at bid price : 19.24 Bid-YTW : 4.42 % |

| RY.PR.F | Deemed-Retractible | 1.92 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.98 Bid-YTW : 4.57 % |

| FTS.PR.K | FixedReset | 2.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 16.35 Evaluated at bid price : 16.35 Bid-YTW : 4.71 % |

| HSE.PR.C | FixedReset | 2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 4.90 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| FTS.PR.F | Perpetual-Discount | 137,700 | Desjardins crossed 135,400 at 21.75. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 21.33 Evaluated at bid price : 21.60 Bid-YTW : 5.73 % |

| MFC.PR.G | FixedReset | 91,136 | Desjardins bought two blocks from RBC, 66,700 and 10,700, both at 20.85. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.79 Bid-YTW : 6.23 % |

| TD.PR.Y | FixedReset | 67,277 | Desjardins crossed 56,200 at 24.30. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.11 Bid-YTW : 3.78 % |

| CU.PR.I | FixedReset | 64,000 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-29 Maturity Price : 23.15 Evaluated at bid price : 25.00 Bid-YTW : 4.41 % |

| GWO.PR.S | Deemed-Retractible | 56,011 | RBC crossed 38,900 at 22.80. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.88 Bid-YTW : 6.52 % |

| BNS.PR.A | FloatingReset | 47,890 | TD crossed 44,100 at 22.20. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.33 Bid-YTW : 4.40 % |

| There were 58 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| RY.PR.D | Deemed-Retractible | Quote: 24.28 – 24.94 Spot Rate : 0.6600 Average : 0.4225 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 17.10 – 17.90 Spot Rate : 0.8000 Average : 0.6233 YTW SCENARIO |

| RY.PR.I | FixedReset | Quote: 23.47 – 23.98 Spot Rate : 0.5100 Average : 0.3404 YTW SCENARIO |

| W.PR.J | Perpetual-Discount | Quote: 23.25 – 24.00 Spot Rate : 0.7500 Average : 0.5852 YTW SCENARIO |

| BNS.PR.P | FixedReset | Quote: 23.87 – 24.30 Spot Rate : 0.4300 Average : 0.2787 YTW SCENARIO |

| PWF.PR.O | Perpetual-Premium | Quote: 25.07 – 25.50 Spot Rate : 0.4300 Average : 0.2882 YTW SCENARIO |