Canadian preferred shares appear to have been hit over the past few months by tax loss selling, but we’re not the only targets:

Investors pulled more money from U.S. mutual funds last week than they have in any seven-day period in the past two and a half years.

Net redemptions reached $28.6 billion in the week ended Dec. 16, according to a statement from the Investment Company Institute, a trade group. It was the biggest weekly outflow since June 2013, ICI data show.

Some of the redemptions might reflect year-end tax-loss selling, which are sales made for tax purposes, ICI Senior Economist Shelly Antoniewicz said in the statement.

Investors withdrew $11.1 billion from stock funds, $12 billion from bond funds and $5.6 billion from funds that buy a mix of stocks and bonds. Municipal bond funds attracted $647 million, the only category that saw inflows.

Mutual funds have experienced net redemptions every month since July, according to ICI data. In each of the first six months of the year, funds gathered money.

On September 21 I discussed the characterization of the Canadian dollar as a petrodollar. Now it turns out that, as far as one measure is concerned, we’re the petrodollariest in the world!

No other major currency is as closely tied to the value of its key commodity export as the loonie is to crude right now. The correlation between the Canadian dollar and the benchmark West Texas Intermediate oil price is about 0.56, meaning the two have a strong positive relationship. That’s the closest association among 16 of the world’s most-traded currencies including the Australian and New Zealand dollars, Norway’s krone and Brazil’s real.

With oil futures trading below $45 a barrel through 2016, the loonie may continue to struggle. The currency has declined 16 per cent over the past year, touching an 11-year low of $1.4001 per U.S. dollar last week. The drop comes as the price of WTI fell to the lowest since 2009 after the Organization of Petroleum Exporting Countries announced this month it was abandoning production limits, and with U.S. crude stockpiles forecast to climb to the highest since 1930.

…

The 120-day correlation coefficient between 16 major currencies tracked by Bloomberg and their country’s main export commodity — based on 2014 World Bank data — show that the Mexican peso and oil had the second strongest correlation, at 0.41. The correlation between the Australian dollar and iron ore was 0.13, while the link between New Zealand’s currency and whole milk powder was 0.11. A reading of 1 means that gauges move in lockstep; minus 1 means they move in opposite directions.

Crude fell below $34 a barrel on Dec. 21. WTI futures for delivery in March are trading at about $37, compared to $39 for those settling in June.

The Canadian dollar has already fallen below Scotiabank’s 2016 target of $1.39 and there is “clear risk of an overshoot” toward $1.42-$1.43 through the first quarter, [chief foreign-exchange strategist for Bank of Nova Scotia] Mr. [Shaun] Osborne said.

There’s an interesting piece on the bond market, examined through the lens of the Litvak case:

Earlier this year, Sally Yates, the agency’s No. 2 official, ordered policy changes to push prosecutors to bring criminal charges against company executives suspected of financial wrongdoing. Her memo almost admitted that the U.S. Department of Justice had lapsed in its duty to put criminals behind bars. In a September speech, Yates said: “This memo is designed to ensure that all attorneys across the department are consistent in our best efforts to hold to account the individuals responsible for illegal corporate conduct. It’s the only way to truly deter corporate wrongdoing.”

The case against Litvak was supposed to be the opening salvo against dishonest conduct among bond traders. The Justice Department and U.S. Securities and Exchange Commission have built more than a dozen other cases using the one against Litvak as a model.

The cases won’t be easy victories for the government. Lying doesn’t necessarily violate securities law. It’s only fraud when that deception is considered important to a buyer. The question becomes: Is it important that the buyer knew how much Litvak paid for bonds he later sold? “The government may not like how these markets work, and it may look bad from the outside looking in, but it is how they do work,” says Charles Geisst, a Wall Street historian at Manhattan College in New York.

…

As the SEC sees it, just because something is common practice on Wall Street doesn’t mean it conforms to securities laws. The agency has built its own algorithms to comb through trading data to look for red flags instead of waiting for complaints. The SEC has uncovered brokers charging buyers higher fees, traders hiding their positions, and dealers running deceptive auctions. “We’ve identified billions of dollars of potentially problematic trades,” says Michael Osnato Jr., head of the regulator’s Complex Financial Instruments unit. “We have opened promising investigations thus far based on these efforts and expect more to follow soon.”

The Litvak ruling will shape how the SEC pursues some of these violations. The intensive monitoring of debt backed by mortgages and other assets represents a first for the agency. Before the credit crisis, the SEC viewed the market participants as sophisticated investors who didn’t need close supervision. That assumption came undone when plummeting prices in the debt markets kicked off the crisis. “The government’s new interest is reflective of the fact that they’ve had very little interest in this market historically,” says James Cox, a professor at Duke University School of Law. “They just hadn’t looked at it.”

The SEC doesn’t understand any markets, really, other than bank accounts that accrue interest daily. But hey! Markets went down, therefore nefarious activity was behind it, therefore somebody’s got to go to jail – it doesn’t matter who, really. The persecution of Litvak has been discussed on PrefBlog many times before, most recently on December 8.

Speaking of the way the market operates, I see there’s a dust-up with Dominion Diamond Corp. I have no knowledge of this company, but one part of the article drew my attention as a possible winner of “2015 Statements Best Illustrating Intellectual Bankruptcy of Equities Markets”:

Dominion enjoys considerable financial flexibility, according to Edward Sterck, a London-based analyst with Bank of Montreal’s investment arm. The miner has amassed net cash of $284-million (U.S.), equal to about 40 per cent of its market capitalization, he wrote in a research note.

He said that while Dominion’s near-term mine plan has been subject to frequent changes, its longer-term outlook has remained consistently positive.

Mr. Sterck projects an attractive bump in free cash flow over the years to come as new production comes into play, but added that “the problem is that the increased cash flows do not really begin in earnest until mid-2016, so why should investors hold the stock now?”

Ummmm … because increased cash flows begin in earnest in mid-2016?

Meanwhile, there has been a sudden change in the living rooms of preferred share investors … they now look like this:

Click for Big

Click for BigIt was a strong day for the Canadian preferred share market, with PerpetualDiscounts gaining 30bp, FixedResets winning 166bp and DeemedRetractibles up 37bp … it appears that bargain hunters have decided not to wait until the precise end of tax-loss selling season after all! The performance highlights table is as lengthy as one might guess from the raw numbers. Volume continued to be enormously high … which leads to interesting speculation as to what might happen when tax-loss selling season ends.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

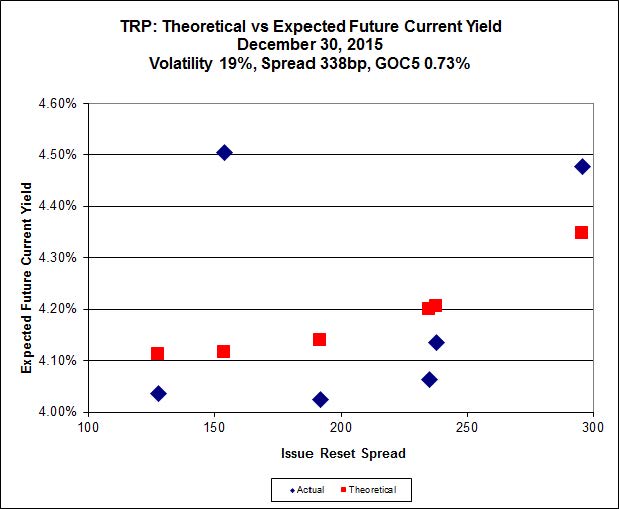

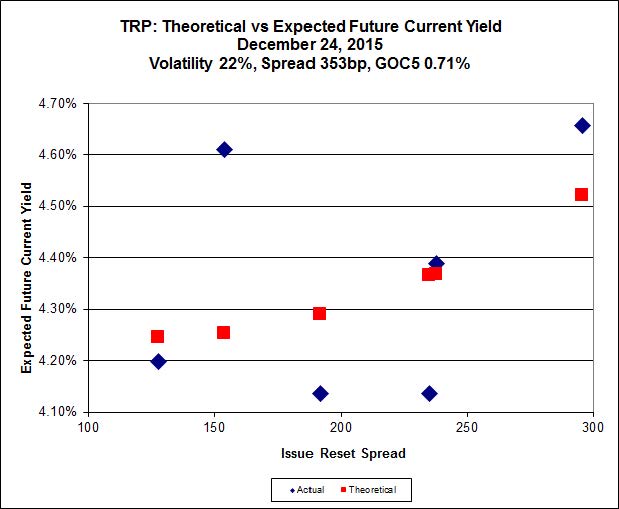

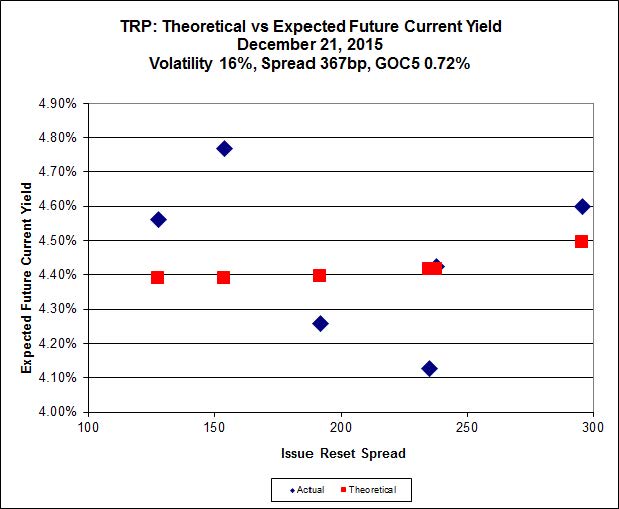

Here’s TRP:

Click for Big

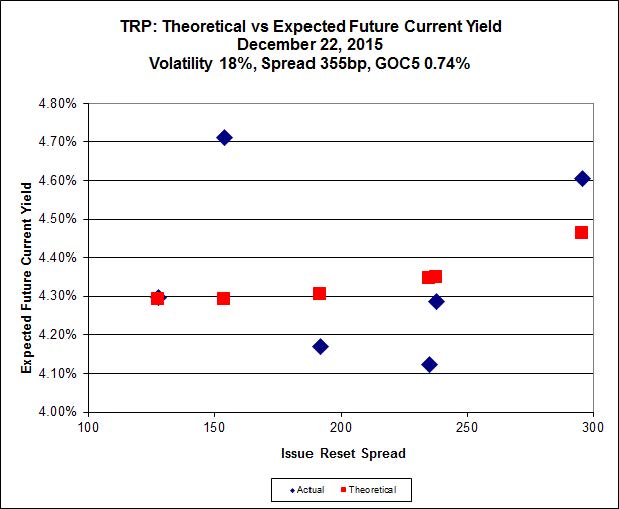

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.73 to be $0.96 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.18 cheap at its bid price of 12.10.

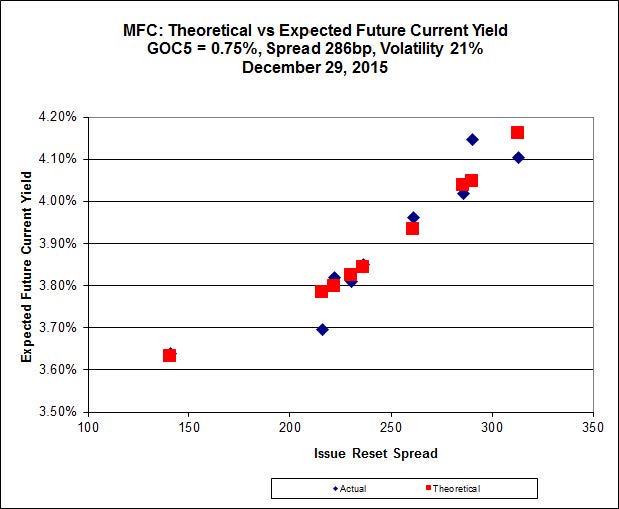

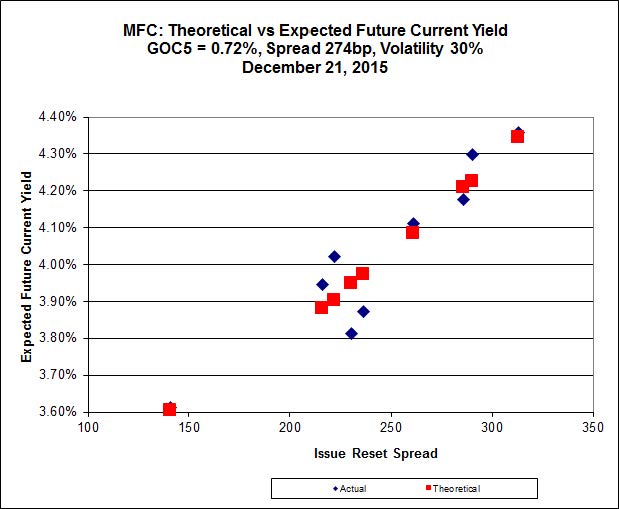

Click for Big

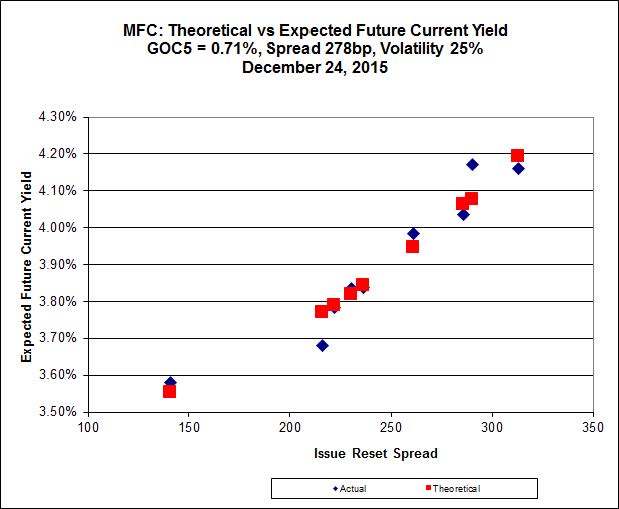

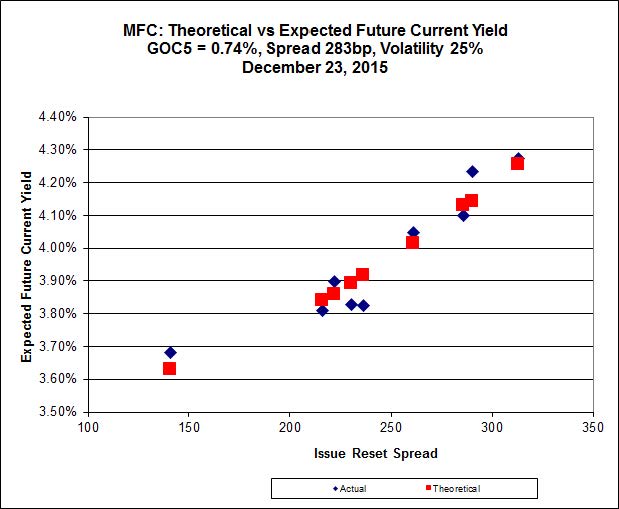

Click for BigMost expensive is MFC.PR.M, resetting at +236bp on 2019-12-19, bid at 20.26 to be 0.48 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 21.50 to be 0.48 cheap.

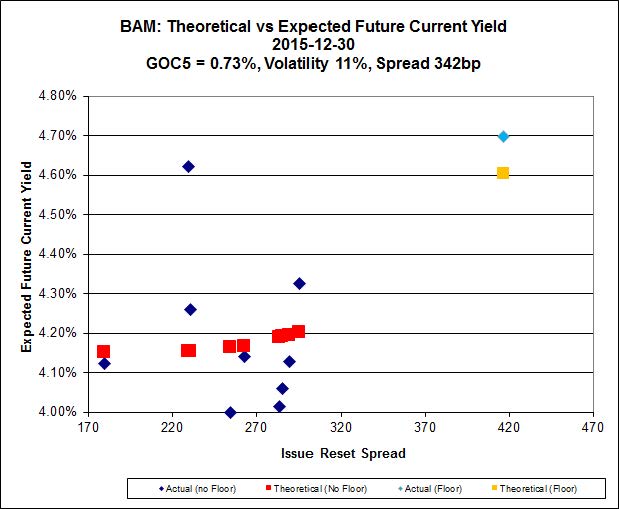

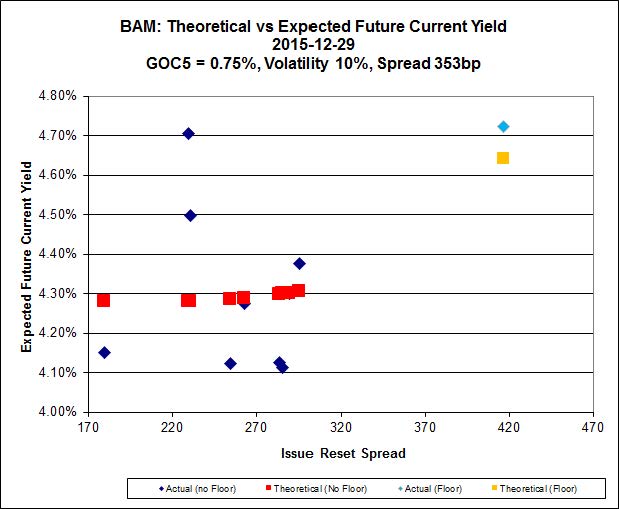

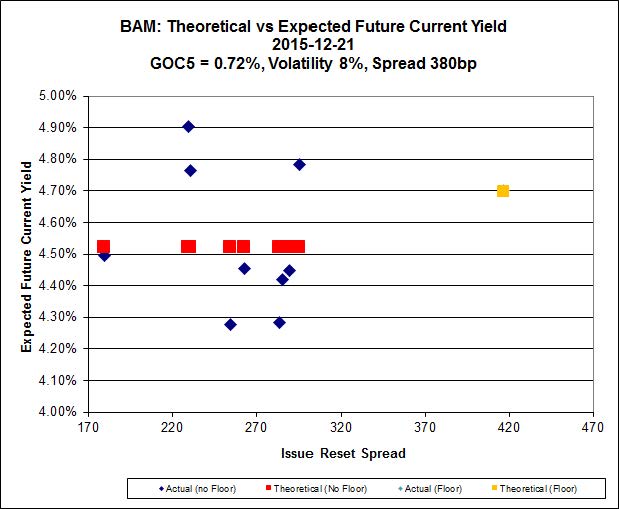

Click for Big

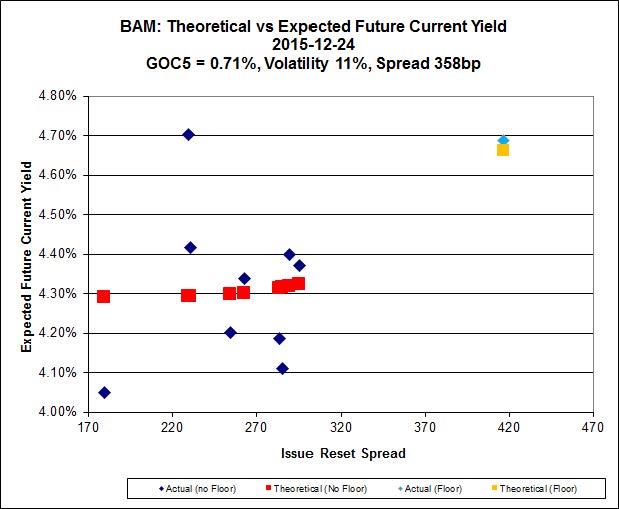

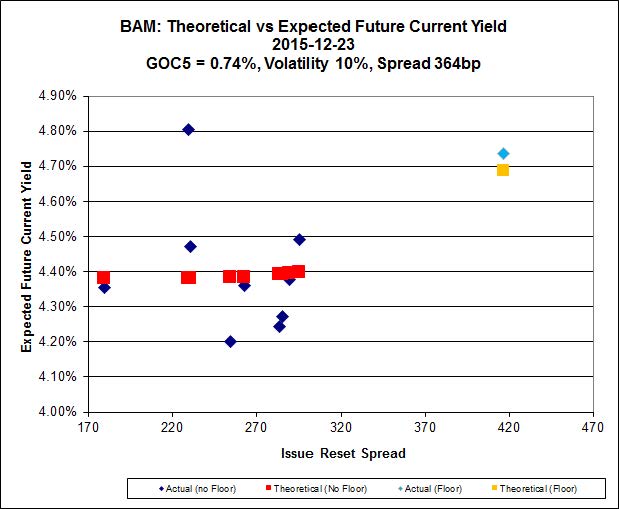

Click for BigThe cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.82 to be $1.53 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 19.58 and appears to be $0.81 rich.

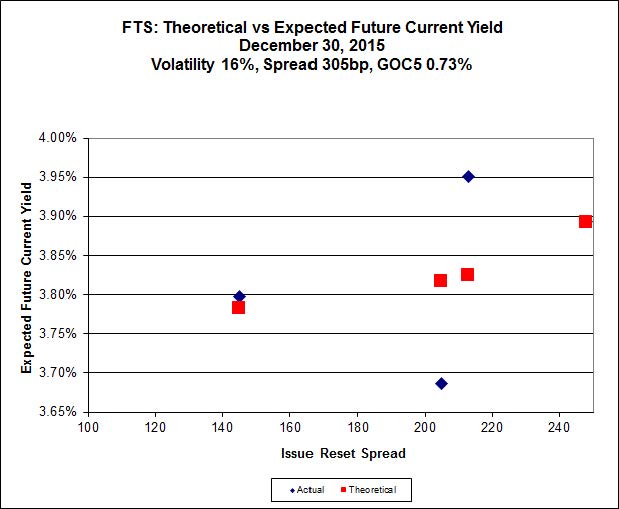

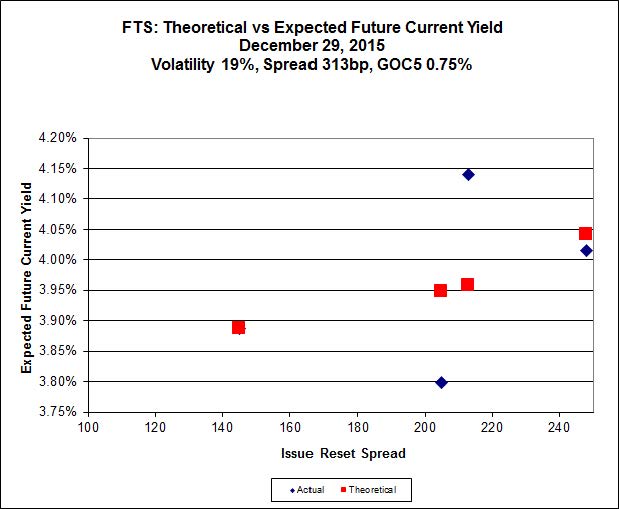

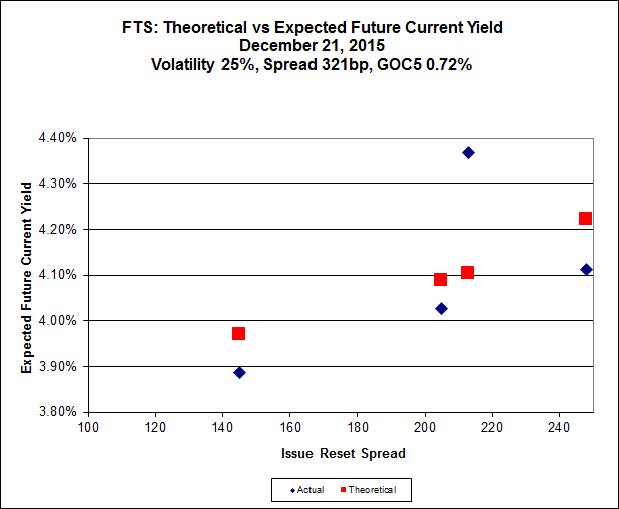

Click for Big

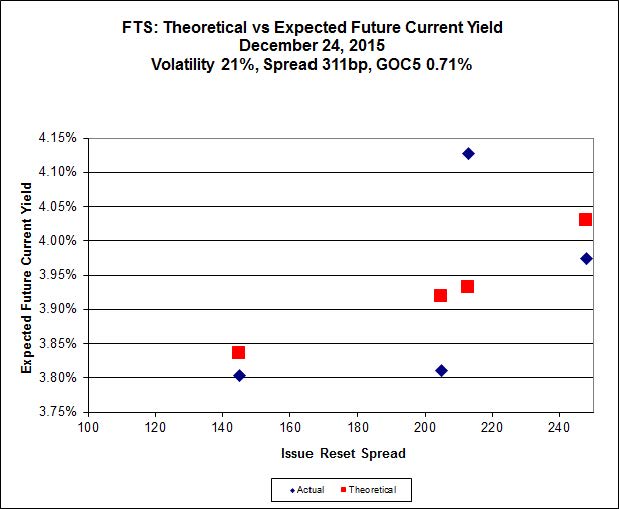

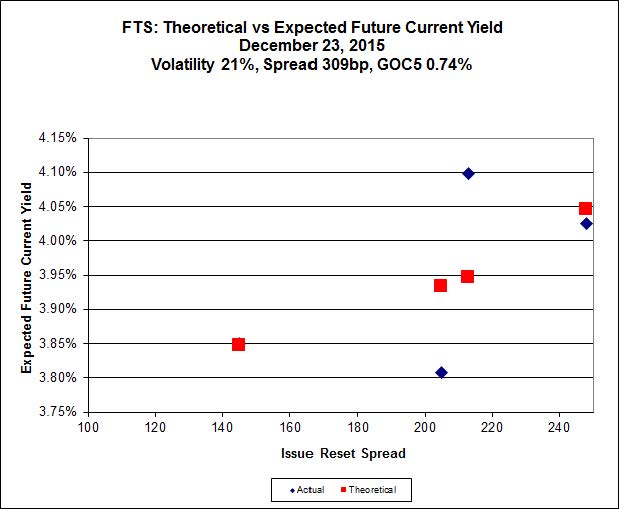

Click for BigFTS.PR.K, with a spread of +205bp, and bid at 18.32, looks $0.59 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.51 and is $0.67 cheap.

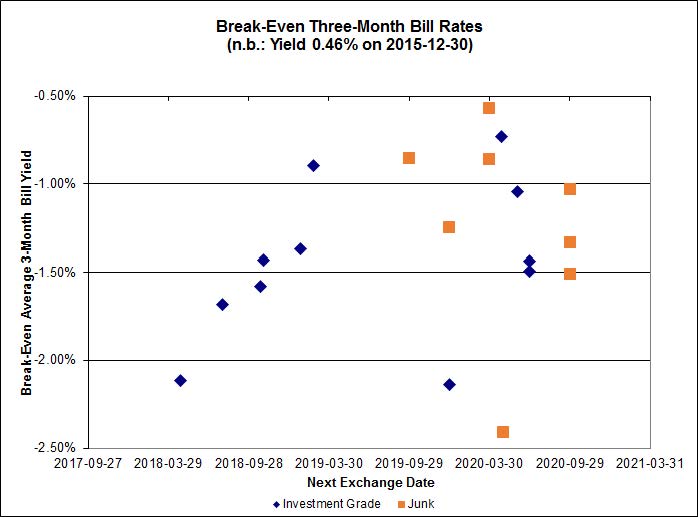

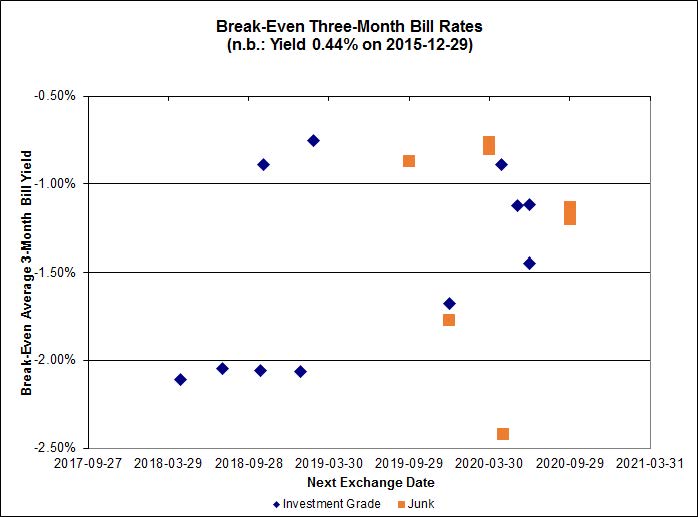

Click for Big

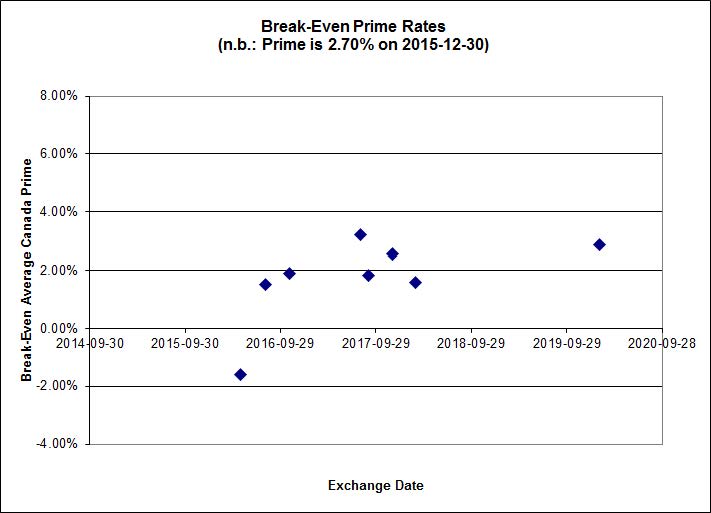

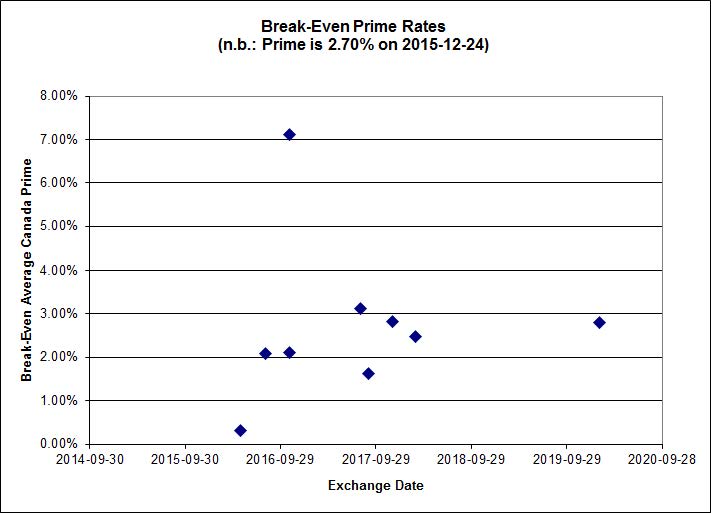

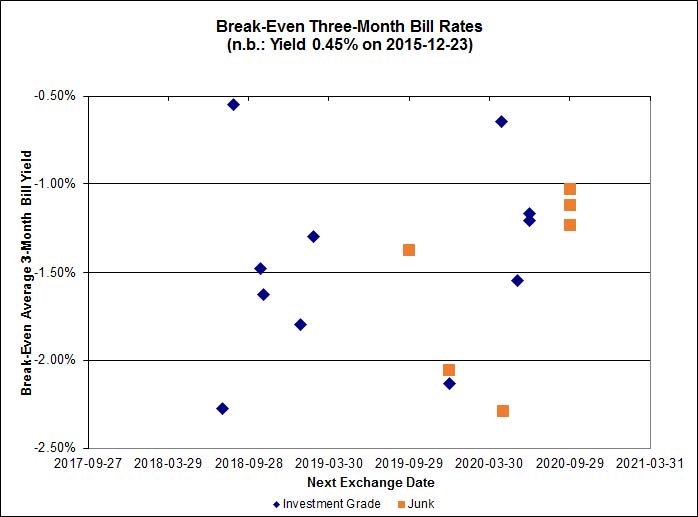

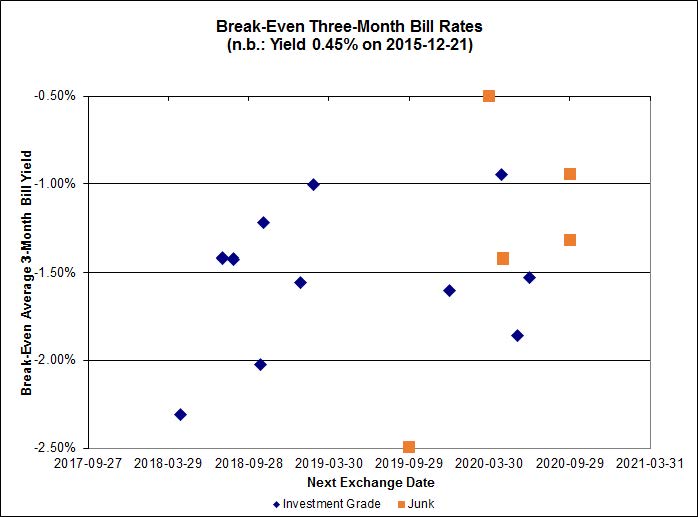

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.52%, with one outlier below -2.50%. There are four junk outliers above -0.50%.

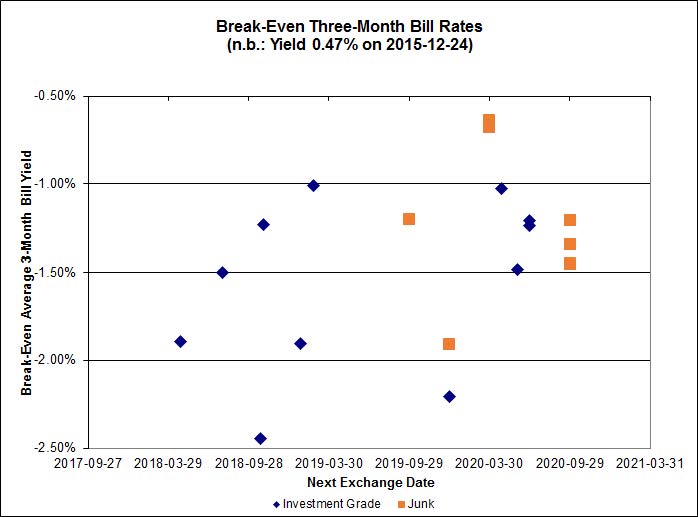

Click for Big

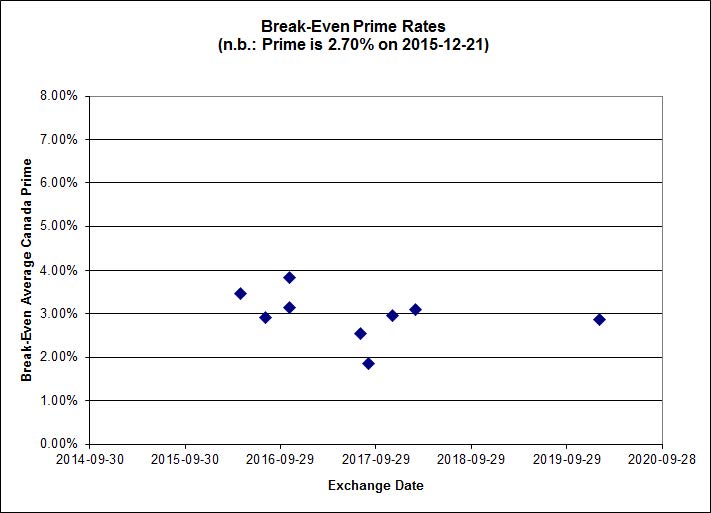

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

4.85 % |

5.90 % |

35,026 |

16.75 |

1 |

0.0000 % |

1,598.0 |

| FixedFloater |

7.20 % |

6.38 % |

41,323 |

15.76 |

1 |

-0.4525 % |

2,711.6 |

| Floater |

4.36 % |

4.54 % |

84,982 |

16.36 |

4 |

-1.3667 % |

1,750.7 |

| OpRet |

4.86 % |

4.17 % |

27,412 |

0.67 |

1 |

0.0000 % |

2,738.6 |

| SplitShare |

4.83 % |

5.87 % |

84,887 |

1.86 |

6 |

0.0293 % |

3,201.3 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0293 % |

2,497.8 |

| Perpetual-Premium |

5.82 % |

5.87 % |

97,659 |

13.91 |

7 |

0.2347 % |

2,501.1 |

| Perpetual-Discount |

5.74 % |

5.80 % |

107,756 |

14.19 |

33 |

0.3040 % |

2,501.1 |

| FixedReset |

5.14 % |

4.48 % |

278,104 |

14.72 |

81 |

1.6599 % |

2,011.9 |

| Deemed-Retractible |

5.21 % |

4.80 % |

139,962 |

5.29 |

33 |

0.3745 % |

2,575.0 |

| FloatingReset |

2.80 % |

4.10 % |

70,387 |

5.65 |

11 |

1.8268 % |

2,123.0 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| MFC.PR.F |

FixedReset |

-4.45 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.60

Bid-YTW : 9.06 % |

| BAM.PR.B |

Floater |

-2.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 10.42

Evaluated at bid price : 10.42

Bid-YTW : 4.54 % |

| BAM.PR.K |

Floater |

-2.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 10.30

Evaluated at bid price : 10.30

Bid-YTW : 4.59 % |

| PWF.PR.P |

FixedReset |

-1.41 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 14.00

Evaluated at bid price : 14.00

Bid-YTW : 4.21 % |

| PVS.PR.B |

SplitShare |

-1.26 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2019-01-10

Maturity Price : 25.00

Evaluated at bid price : 23.60

Bid-YTW : 6.51 % |

| GWO.PR.N |

FixedReset |

-1.19 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.32

Bid-YTW : 9.97 % |

| ENB.PR.A |

Perpetual-Discount |

-1.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 22.41

Evaluated at bid price : 22.67

Bid-YTW : 6.12 % |

| POW.PR.C |

Perpetual-Premium |

1.01 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2016-01-22

Maturity Price : 25.00

Evaluated at bid price : 25.00

Bid-YTW : 1.36 % |

| BAM.PR.R |

FixedReset |

1.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 15.82

Evaluated at bid price : 15.82

Bid-YTW : 4.87 % |

| RY.PR.L |

FixedReset |

1.09 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 25.04

Bid-YTW : 3.91 % |

| BAM.PF.G |

FixedReset |

1.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 21.09

Evaluated at bid price : 21.09

Bid-YTW : 4.50 % |

| TRP.PR.A |

FixedReset |

1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 15.95

Evaluated at bid price : 15.95

Bid-YTW : 4.36 % |

| CIU.PR.A |

Perpetual-Discount |

1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 20.03

Evaluated at bid price : 20.03

Bid-YTW : 5.81 % |

| BAM.PR.M |

Perpetual-Discount |

1.19 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 19.56

Evaluated at bid price : 19.56

Bid-YTW : 6.11 % |

| MFC.PR.G |

FixedReset |

1.22 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.50

Bid-YTW : 5.73 % |

| BNS.PR.Y |

FixedReset |

1.34 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.42

Bid-YTW : 5.42 % |

| RY.PR.O |

Perpetual-Discount |

1.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 22.08

Evaluated at bid price : 22.41

Bid-YTW : 5.51 % |

| TD.PF.D |

FixedReset |

1.37 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 20.02

Evaluated at bid price : 20.02

Bid-YTW : 4.47 % |

| TRP.PR.E |

FixedReset |

1.41 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.73

Evaluated at bid price : 18.73

Bid-YTW : 4.49 % |

| TRP.PR.G |

FixedReset |

1.41 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 20.09

Evaluated at bid price : 20.09

Bid-YTW : 4.66 % |

| TD.PF.B |

FixedReset |

1.42 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.61

Evaluated at bid price : 18.61

Bid-YTW : 4.29 % |

| BAM.PF.H |

FixedReset |

1.45 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2020-12-31

Maturity Price : 25.00

Evaluated at bid price : 25.91

Bid-YTW : 4.19 % |

| FTS.PR.H |

FixedReset |

1.50 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 14.22

Evaluated at bid price : 14.22

Bid-YTW : 3.98 % |

| MFC.PR.I |

FixedReset |

1.57 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.95

Bid-YTW : 5.50 % |

| BNS.PR.A |

FloatingReset |

1.61 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.68

Bid-YTW : 4.23 % |

| SLF.PR.I |

FixedReset |

1.64 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.83

Bid-YTW : 6.62 % |

| IAG.PR.A |

Deemed-Retractible |

1.67 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.35

Bid-YTW : 6.80 % |

| TD.PR.Y |

FixedReset |

1.68 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.77

Bid-YTW : 3.24 % |

| IFC.PR.C |

FixedReset |

1.70 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.13

Bid-YTW : 6.99 % |

| SLF.PR.H |

FixedReset |

1.70 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.30

Bid-YTW : 7.77 % |

| MFC.PR.L |

FixedReset |

1.76 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.03

Bid-YTW : 6.94 % |

| HSE.PR.C |

FixedReset |

1.78 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 16.55

Evaluated at bid price : 16.55

Bid-YTW : 6.09 % |

| MFC.PR.N |

FixedReset |

1.79 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.86

Bid-YTW : 6.48 % |

| VNR.PR.A |

FixedReset |

1.89 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.85

Evaluated at bid price : 18.85

Bid-YTW : 4.89 % |

| TD.PF.A |

FixedReset |

1.90 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.81

Evaluated at bid price : 18.81

Bid-YTW : 4.25 % |

| BAM.PF.E |

FixedReset |

1.93 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 19.58

Evaluated at bid price : 19.58

Bid-YTW : 4.52 % |

| TD.PR.S |

FixedReset |

1.98 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.69

Bid-YTW : 3.11 % |

| CM.PR.O |

FixedReset |

2.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.77

Evaluated at bid price : 18.77

Bid-YTW : 4.27 % |

| BNS.PR.R |

FixedReset |

2.14 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.82

Bid-YTW : 3.50 % |

| RY.PR.H |

FixedReset |

2.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.80

Evaluated at bid price : 18.80

Bid-YTW : 4.24 % |

| HSE.PR.G |

FixedReset |

2.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.80

Evaluated at bid price : 18.80

Bid-YTW : 5.80 % |

| CM.PR.P |

FixedReset |

2.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.25

Evaluated at bid price : 18.25

Bid-YTW : 4.29 % |

| TD.PF.E |

FixedReset |

2.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 21.26

Evaluated at bid price : 21.26

Bid-YTW : 4.31 % |

| NA.PR.W |

FixedReset |

2.24 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.25

Evaluated at bid price : 18.25

Bid-YTW : 4.40 % |

| CU.PR.C |

FixedReset |

2.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 19.06

Evaluated at bid price : 19.06

Bid-YTW : 4.21 % |

| MFC.PR.M |

FixedReset |

2.32 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.26

Bid-YTW : 6.28 % |

| MFC.PR.J |

FixedReset |

2.38 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.69

Bid-YTW : 6.04 % |

| BNS.PR.Q |

FixedReset |

2.46 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.55

Bid-YTW : 3.44 % |

| BMO.PR.Q |

FixedReset |

2.51 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.65

Bid-YTW : 4.70 % |

| FTS.PR.M |

FixedReset |

2.51 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 20.00

Evaluated at bid price : 20.00

Bid-YTW : 4.27 % |

| MFC.PR.K |

FixedReset |

2.54 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.99

Bid-YTW : 6.86 % |

| TD.PF.C |

FixedReset |

2.55 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.50

Evaluated at bid price : 18.50

Bid-YTW : 4.30 % |

| TRP.PR.B |

FixedReset |

2.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 11.75

Evaluated at bid price : 11.75

Bid-YTW : 4.35 % |

| CM.PR.Q |

FixedReset |

2.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 19.75

Evaluated at bid price : 19.75

Bid-YTW : 4.47 % |

| RY.PR.Z |

FixedReset |

2.73 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.80

Evaluated at bid price : 18.80

Bid-YTW : 4.19 % |

| TRP.PR.D |

FixedReset |

2.77 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.20

Evaluated at bid price : 18.20

Bid-YTW : 4.55 % |

| BAM.PF.A |

FixedReset |

2.87 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 20.79

Evaluated at bid price : 20.79

Bid-YTW : 4.53 % |

| NA.PR.S |

FixedReset |

2.92 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.69

Evaluated at bid price : 18.69

Bid-YTW : 4.47 % |

| TRP.PR.C |

FixedReset |

2.98 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 12.10

Evaluated at bid price : 12.10

Bid-YTW : 4.75 % |

| BAM.PF.F |

FixedReset |

2.98 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 21.07

Evaluated at bid price : 21.07

Bid-YTW : 4.48 % |

| BMO.PR.R |

FloatingReset |

3.10 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.25

Bid-YTW : 3.36 % |

| BMO.PR.T |

FixedReset |

3.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.60

Evaluated at bid price : 18.60

Bid-YTW : 4.26 % |

| FTS.PR.K |

FixedReset |

3.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.32

Evaluated at bid price : 18.32

Bid-YTW : 4.09 % |

| PWF.PR.T |

FixedReset |

3.78 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 22.29

Evaluated at bid price : 22.78

Bid-YTW : 3.58 % |

| HSE.PR.A |

FixedReset |

3.85 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 11.59

Evaluated at bid price : 11.59

Bid-YTW : 5.33 % |

| BAM.PR.Z |

FixedReset |

3.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 20.59

Evaluated at bid price : 20.59

Bid-YTW : 4.63 % |

| BNS.PR.B |

FloatingReset |

3.95 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.37

Bid-YTW : 4.10 % |

| BAM.PR.T |

FixedReset |

4.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 17.05

Evaluated at bid price : 17.05

Bid-YTW : 4.60 % |

| FTS.PR.G |

FixedReset |

4.29 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 17.51

Evaluated at bid price : 17.51

Bid-YTW : 4.32 % |

| BNS.PR.Z |

FixedReset |

4.75 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.06

Bid-YTW : 6.21 % |

| BMO.PR.Y |

FixedReset |

6.00 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 20.67

Evaluated at bid price : 20.67

Bid-YTW : 4.30 % |

| BNS.PR.D |

FloatingReset |

7.11 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.97

Bid-YTW : 6.27 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| CU.PR.I |

FixedReset |

82,237 |

Scotia crossed 75,000 at 25.75.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2020-12-01

Maturity Price : 25.00

Evaluated at bid price : 25.70

Bid-YTW : 3.95 % |

| RY.PR.Q |

FixedReset |

79,291 |

Recent new issue.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-05-24

Maturity Price : 25.00

Evaluated at bid price : 25.73

Bid-YTW : 4.93 % |

| SLF.PR.C |

Deemed-Retractible |

69,404 |

Desjardins crossed 51,900 at 20.40.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.32

Bid-YTW : 7.33 % |

| RY.PR.J |

FixedReset |

58,200 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 19.75

Evaluated at bid price : 19.75

Bid-YTW : 4.47 % |

| TRP.PR.D |

FixedReset |

51,563 |

National crossed 11,900 at 18.20.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.20

Evaluated at bid price : 18.20

Bid-YTW : 4.55 % |

| BNS.PR.E |

FixedReset |

50,490 |

Recent new issue.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-04-25

Maturity Price : 25.00

Evaluated at bid price : 25.89

Bid-YTW : 4.78 % |

| There were 81 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| TRP.PR.E |

FixedReset |

Quote: 18.73 – 19.30

Spot Rate : 0.5700

Average : 0.3645

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 18.73

Evaluated at bid price : 18.73

Bid-YTW : 4.49 % |

| RY.PR.L |

FixedReset |

Quote: 25.04 – 25.69

Spot Rate : 0.6500

Average : 0.4498

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 25.04

Bid-YTW : 3.91 % |

| CM.PR.Q |

FixedReset |

Quote: 19.75 – 20.49

Spot Rate : 0.7400

Average : 0.5464

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-23

Maturity Price : 19.75

Evaluated at bid price : 19.75

Bid-YTW : 4.47 % |

| IAG.PR.A |

Deemed-Retractible |

Quote: 21.35 – 22.00

Spot Rate : 0.6500

Average : 0.4633

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.35

Bid-YTW : 6.80 % |

| GWO.PR.S |

Deemed-Retractible |

Quote: 24.31 – 24.76

Spot Rate : 0.4500

Average : 0.3057

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.31

Bid-YTW : 5.66 % |

| MFC.PR.L |

FixedReset |

Quote: 19.03 – 19.49

Spot Rate : 0.4600

Average : 0.3198

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.03

Bid-YTW : 6.94 % |