I sent three eMails of inquiry (on 1/31, 2/1 and 2/4) to Fortis Investor Relations regarding the reset rate for FTS.PR.K:

Will the captioned security be redeemed? Or will the dividend rate be reset, with a conversion option? Will there be a press release, similar to the press releases of your competitors for capital, Enbridge and Pembina Pipelines, with respect to their issues resetting on the same date?

I finally got a reply today well after the close of business:

Good Evening Mr. Hymas,

Thank you for contacting Fortis Inc. Fortis does not intend to exercise its right to redeem all or any part of the currently outstanding Cumulative Redeemable Fixed Rate Reset First Preference Shares, Series K of the Corporation (the “Series K Shares”) on March 1, 2019.

Subject to certain conditions set out in the prospectus supplement of the Corporation dated July 9, 2013 to the base shelf prospectus of the Corporation dated May 10, 2012 relating to the issuance of the Series K Shares, the holders of the Series K Shares have the right to convert all or part of their Series K Shares, on a one-for-one basis, into Cumulative Redeemable Floating Rate First Preference Shares, Series L of the Corporation (the “Series L Shares”) on March 1, 2019 (the “Conversion Date”). This prospectus is on the Fortis website.

You should check CDS Advisory Bulletins for ongoing corporate actions relating to the conversion and/or redemption of Series K first preference shares. Furthermore, Fortis will be announcing the new dividend rate for the Series K upon the board of directors approval and declaration, which should occur around mid-February.

If you have any further questions please let me know.

There is a lot to complain about here.

First is the question of timing:

Fortis will be announcing the new dividend rate for the Series K upon the board of directors approval and declaration, which should occur around mid-February.

I note from the prospectus:

The holders of Series K First Preference Shares will have the right, at their option, to convert any or all of their Series K First Preference Shares into an equal number of Cumulative Redeemable Floating Rate First Preference Shares, Series L of the Corporation (the “Series L First Preference Shares”), subject to certain conditions, on March 1, 2019, and on March 1 every fifth year thereafter (each, a “Series K Conversion Date”).

…

The conversion of the Series K First Preference Shares may be effected by delivery to the Corporation of written notice thereof not earlier than the 30th day prior to, but not later than 5:00 p.m. (Toronto time) on the 15th day preceding, a Series K Conversion Date.

So March 1, 2019, is a Series K Conversion Date and the deadline for notification of conversion is the 15th day preceding this date, which is February 14, which is “around mid-February”. So the deadline for notification of conversion and the public announcement of the new rate will occur more or less simultaneously.

However, we may also note, from the prospectus, that:

“Fixed Rate Calculation Date” means, for any Subsequent Fixed Rate Period, the 30th day prior to the first day of such Subsequent Fixed Rate Period.

…

“Subsequent Fixed Rate Period” means, for the initial Subsequent Fixed Rate Period, the period commencing on March 1, 2019 to, but excluding, March 1, 2024 and, for each succeeding Subsequent Fixed Rate Period, the period commencing on the first day of March immediately following the end of the immediately preceding Subsequent Fixed Rate Period to, but excluding, March 1 in the fifth year thereafter.

…

The Corporation will, on the Fixed Rate Calculation Date, give written notice of the Annual Fixed Dividend Rate for the ensuing Subsequent Fixed Rate Period to the registered holders of the then outstanding Series K First Preference Shares.

So we may assume that Fortis has followed the letter of the prospectus and has already notified the “registered holders” of FTS.PR.K of the reset rate.

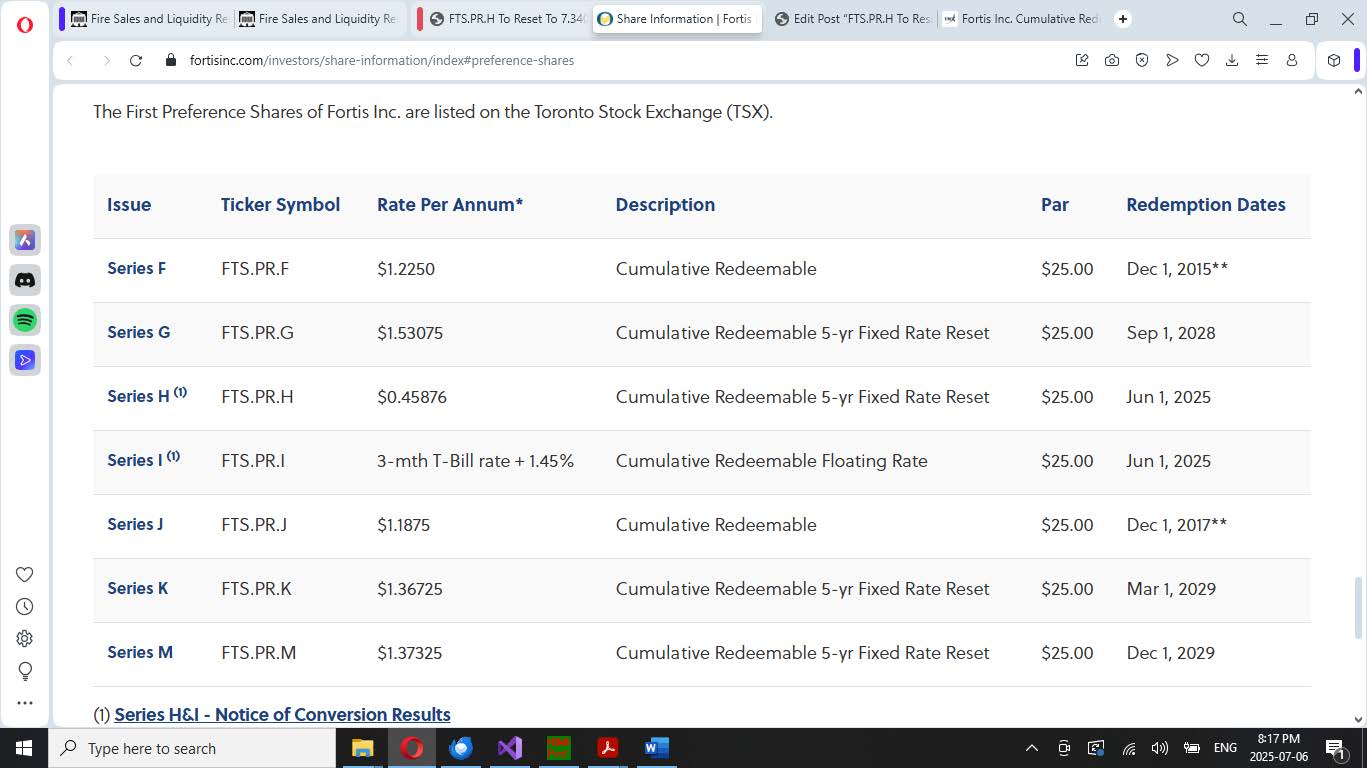

One thing sometimes forgotten when discussing “registered holders” nowadays is that there is usually exactly one registered holder: the depositary, which maintains accounts for each of its participants (brokerages) which in turn maintain accounts for each of their customers. This is called a “book based” system and is described in the prospectus, from which the following is extracted:

Except as otherwise provided below, the Series K First Preference Shares and the Series L First Preference Shares will be issued in a “book entry only” form and must be purchased or transferred through participants (“Participants”) in the depository service of CDS Clearing and Depository Services Inc. (“CDS”) or its nominee which include securities brokers and dealers, banks and trust companies. On the Closing Date, the Corporation will cause a global certificate representing the Series K First Preference Shares to be delivered to, and registered in the name of, CDS or its nominee. Except as otherwise provided below, no purchaser of Series K First Preference Shares or Series L First Preference Shares will be entitled to a certificate or other instrument from the Corporation or CDS evidencing that purchaser’s ownership, and no purchaser will be shown on the records maintained by CDS except through a book entry account of a Participant acting on behalf of the purchaser. Each purchaser of Series K First Preference Shares or Series L First Preference Shares will receive a customer confirmation of purchase from the registered dealer from which the Series K First Preference Shares or Series L First Preference Shares are purchased in accordance with the practices and procedures of the dealer. The practices of registered dealers may vary, but generally customer confirmations are issued promptly after execution of a customer order.

So what this means is that CDS has been notified, at which point Fortis has taken no further action to disseminate the information; refusing even to answer direct questions to their Investor Relations Department.

This is ridiculous. This is selective disclosure – perhaps not in law, but for all practical purposes this means that CDS (an entity controlled by the Toronto Stock Exchange) and the brokerages (who are “participants” in CDS) are getting notification of the news and are then advising clients at some later time when they damn well choose.

As far as interested investors and advisors are concerned, I’ve looked up how to get access to the CDS Advisory Bulletins:

The Advisory Bulletins service provides issuers an additional facility to communicate extraordinary details related to pending, ongoing or completed entitlements and corporate actions.

Delivery: Web, MT564/MT568 (ISO 15022)

Depending upon the nature of the message, the details of the bulletin will also be delivered via MT564 – Entitlements Notification and MT568 – Entitlements Narrative message.

Pricing: $1,125

Access the product sheet.

Contact us for pricing and other information

Non – CDS Participant Inquiries for CDS Innovation /TMX Datalinx

Email: datasales@tmx.com

CDS Participant & Issuer Inquiries

Client Relationship Managers cdscdccrelationshipmgmt@tmx.com

I have written to the Exchange:

What is the cost to subscribe to the captioned service? May these bulletins be purchased individually?

There is nothing filed regarding this matter on SEDAR, that bastion of brokerage privilege. Fortis seems very eager to pad the profits of TMX Group Limited!

I’m sure Fortis is operating within the letter of the laws and regulations and I’m sure they’ve got large legal bills to prove it. But I consider the lack of immediate public disclosure – which is standard for its competitors, I can’t think of a single other exception to this practice off the top of my head – to be contrary to the spirit of the regulations.

Given the obsession of Fortis management with keeping this information strictly under wraps, to the extent of refusing to answer a direct question regarding the reset rate when selective disclosure has already been made, I am unable to publish a formal recommendation regarding whether FTS.PR.K security holders should convert or hold their shares.

{kind=link}