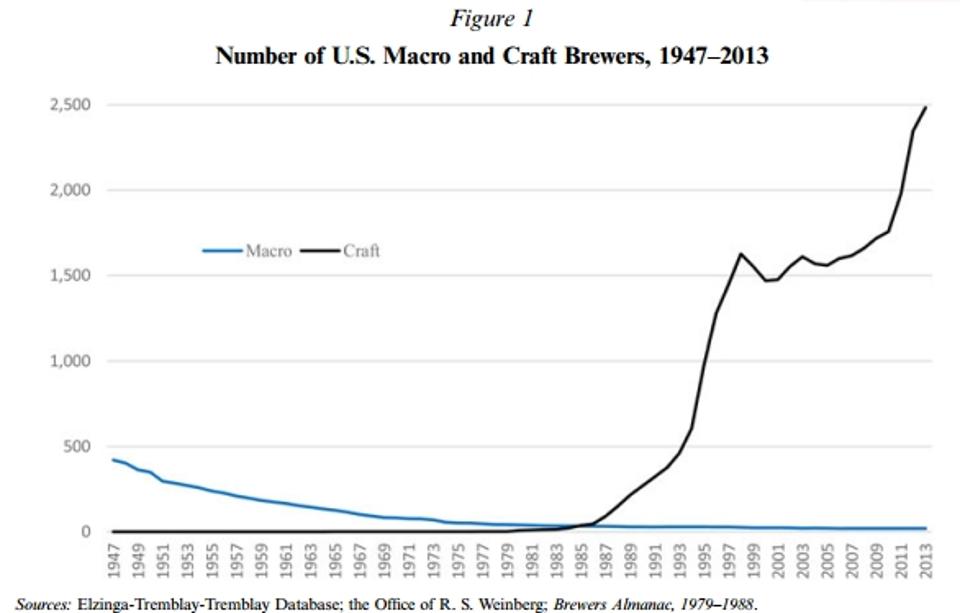

More on my speculation on small-batch craftsmanship as the future of employment:

Today, smaller plants are particularly important to job creation in factory work, said Scott Paul, president of the Alliance for American Manufacturing. “Megafactories are the exception today,” Mr. Paul said. “Small manufacturing is holding its own — and you are seeing some interesting developments in urban centers.”

Out of 252,000 manufacturing companies in the United States, only 3,700 had more than 500 workers. The vast majority employ fewer than 20

While they may not rival the scale of 1950s assembly lines, these smaller craft-type producers hold out hope for cities, Mr. Paul said, particularly as some companies look to move jobs back from overseas to be closer to customers and more nimble to supply customized, small-batch orders.

What is more, these jobs pay people more. According to the Bureau of Labor Statistics, manufacturing workers typically earn just over $26 an hour. By contrast, medical orderlies and nurse’s assistants (a growing field) earn half as much. And fast food, a mainstay for Americans with a high school diploma or less, has a median hourly wage of $9.11.

It’s also support for my other thesis: don’t bet against America! That bet’s been a losing game since 1850!

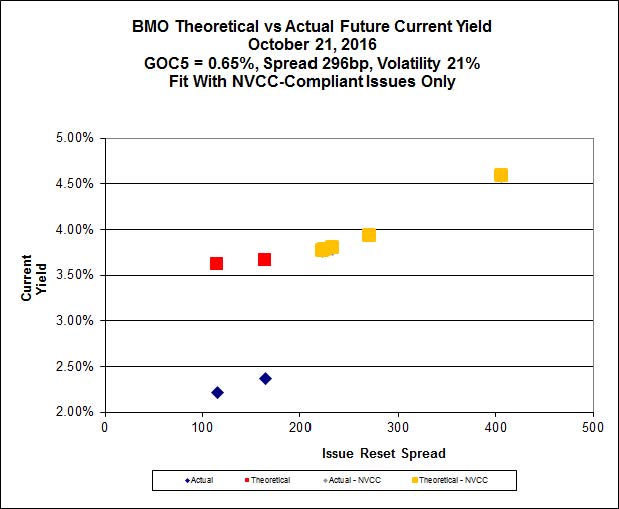

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2087 % | 1,714.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2087 % | 3,131.6 |

| Floater | 4.37 % | 4.52 % | 42,928 | 16.36 | 4 | 0.2087 % | 1,804.8 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1191 % | 2,903.2 |

| SplitShare | 4.82 % | 4.69 % | 42,352 | 2.07 | 6 | 0.1191 % | 3,467.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1191 % | 2,705.1 |

| Perpetual-Premium | 5.35 % | 4.16 % | 73,222 | 0.09 | 23 | -0.0377 % | 2,703.6 |

| Perpetual-Discount | 5.09 % | 5.10 % | 93,918 | 15.30 | 15 | 0.1605 % | 2,925.9 |

| FixedReset | 4.83 % | 4.22 % | 177,718 | 6.89 | 93 | 0.1763 % | 2,106.8 |

| Deemed-Retractible | 5.02 % | 4.64 % | 116,325 | 1.12 | 32 | -0.0496 % | 2,811.4 |

| FloatingReset | 2.87 % | 3.56 % | 40,172 | 4.93 | 12 | 0.2104 % | 2,283.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| GWO.PR.N | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.90 Bid-YTW : 10.29 % |

| VNR.PR.A | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-10-31 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.72 % |

| TRP.PR.D | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-10-31 Maturity Price : 18.35 Evaluated at bid price : 18.35 Bid-YTW : 4.40 % |

| IFC.PR.D | FloatingReset | 1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.75 Bid-YTW : 7.28 % |

| IFC.PR.A | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.78 Bid-YTW : 9.40 % |

| SLF.PR.J | FloatingReset | 1.92 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.25 Bid-YTW : 10.63 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.B | FixedReset | 1,173,708 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.72 Bid-YTW : 4.29 % |

| BNS.PR.H | FixedReset | 95,800 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-01-26 Maturity Price : 25.00 Evaluated at bid price : 25.90 Bid-YTW : 4.23 % |

| RY.PR.Z | FixedReset | 68,313 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-10-31 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 3.99 % |

| BAM.PF.F | FixedReset | 63,200 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-10-31 Maturity Price : 20.89 Evaluated at bid price : 20.89 Bid-YTW : 4.50 % |

| BMO.PR.T | FixedReset | 60,760 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-10-31 Maturity Price : 18.99 Evaluated at bid price : 18.99 Bid-YTW : 4.06 % |

| GWO.PR.P | Deemed-Retractible | 53,917 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.40 Bid-YTW : 5.26 % |

| There were 35 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| VNR.PR.A | FixedReset | Quote: 19.00 – 19.50 Spot Rate : 0.5000 Average : 0.3467 YTW SCENARIO |

| GWO.PR.N | FixedReset | Quote: 13.90 – 14.25 Spot Rate : 0.3500 Average : 0.2297 YTW SCENARIO |

| BAM.PF.G | FixedReset | Quote: 21.15 – 21.47 Spot Rate : 0.3200 Average : 0.2043 YTW SCENARIO |

| IFC.PR.A | FixedReset | Quote: 15.78 – 16.05 Spot Rate : 0.2700 Average : 0.1610 YTW SCENARIO |

| W.PR.M | FixedReset | Quote: 26.05 – 26.39 Spot Rate : 0.3400 Average : 0.2378 YTW SCENARIO |

| HSE.PR.A | FixedReset | Quote: 12.12 – 12.40 Spot Rate : 0.2800 Average : 0.1861 YTW SCENARIO |