The European Central Bank released a blog post titled Why central bank independence matters – lessons from the past 50 years (on 2025-12-23):

Recent political pressure on central banks in some countries to ease their policy rates irrespective of the macroeconomic conditions has sparked renewed interest in the merits of central bank independence.[1] The idea is that central banks that are insulated from government interference can devote themselves fully to the pursuit of their mandate – which, nowadays, is primarily to preserve price stability. Conversely, politically dependent central banks may be prevented from doing so. In theory, this should leave independent central banks better placed to keep prices stable.

But is this actually the case? Based on a study of 155 central banks covering a 50-year period, the research presented in this blog post shows that independence matters for price stability. Independent central banks are able to pursue more credible monetary policies and are therefore more effective at keeping inflation under control.

…

The idea of central bank independence then began to gain traction, backed by various research findings:First, independence offers an antidote to the time-inconsistency problem. This stems from the fact that central banks implement monetary policies aimed at maintaining price stability over a relatively long horizon – inflation does not respond to changes in the monetary policy stance immediately, but rather with long and variable lags. Meanwhile, to boost their chances of re-election, governments may be tempted to stimulate the economy, even at the cost of higher inflation.[2] Put simply, there are times when a government will choose to prioritise short-term economic growth over long-term price stability.

Second, independence was put forward as a way to counter this inflation bias, through the appointment of conservative central bankers who are more likely than society as a whole to prefer combating inflation to reducing unemployment.[3]

Third, there is broad consensus that independence and inflation are negatively related overall, and that an increase in central bank independence has no adverse impact on economic growth.[4]

…

The quantitative analysis draws on annual macroeconomic data from the World Bank and the International Monetary Fund. It also uses a legal index measuring the degree of central bank independence over time and across countries.[6] Derived from a detailed analysis of central bank statutes based on 42 criteria, the index ranges from 0 (the lowest level) to 1 (the highest). It can therefore be used to make international comparisons. Examples of the criteria used include the way in which board members are appointed and dismissed, monetary policy objectives and their operational implementation, limitations on lending to the government, central bank financial independence and reporting and disclosure requirements.To test whether the thinking behind the time-inconsistency theory holds up in practice, we examined the varying degrees of central bank credibility, meaning the extent to which a central bank is able to stabilise inflation around its policy target.[7] To this end, the study looked at absolute deviations between the observed inflation and the inflation targets for each country (overshooting and undershooting a target both have adverse effects on credibility). The smaller the deviations, the more credible the central bank (0 being the highest possible level).

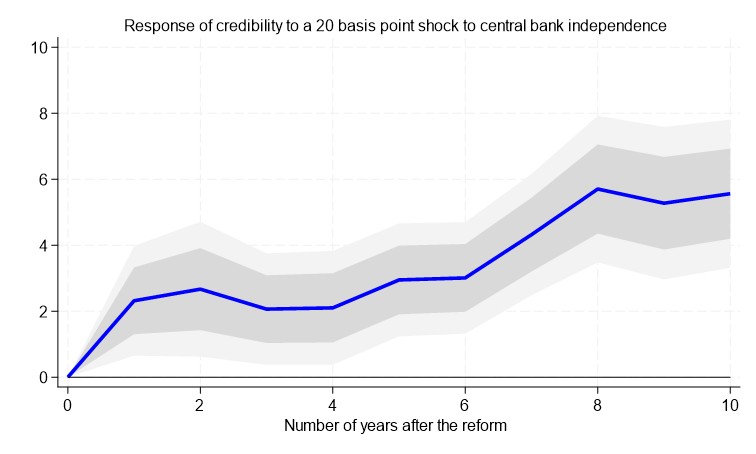

To check whether there is a causal relationship between the two variables, we use the local projections method. Thereby, we can show the impact of central bank reforms over time and their cumulative impact on our measures of policy credibility.[8]

The results show that independence is indeed causal for credibility (see Chart 2). An increase in the independence index of 20 basis points – the average historical change from the worldwide reforms carried out between 1990 and 2020 – leads to a persistent increase in credibility by 6% after ten years.

In short, independence enhances monetary policy credibility. On average, the more independent a central bank is, the better aligned the inflation outcomes are with its target.

For my own views, see In this politicized climate, the Bank of Canada needs to be a lot better at communicating

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2477 % | 2,495.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2477 % | 4,731.8 |

| Floater | 5.77 % | 6.06 % | 55,339 | 13.73 | 3 | 0.2477 % | 2,727.0 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4743 % | 3,667.3 |

| SplitShare | 4.76 % | 4.05 % | 82,969 | 0.94 | 5 | 0.4743 % | 4,379.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4743 % | 3,417.1 |

| Perpetual-Premium | 5.70 % | 5.81 % | 81,444 | 14.05 | 7 | -0.0284 % | 3,068.8 |

| Perpetual-Discount | 5.64 % | 5.73 % | 45,840 | 14.23 | 28 | -0.3267 % | 3,353.0 |

| FixedReset Disc | 5.89 % | 5.90 % | 130,587 | 13.77 | 27 | -0.5974 % | 3,196.3 |

| Insurance Straight | 5.50 % | 5.59 % | 58,762 | 14.53 | 22 | -0.1529 % | 3,305.3 |

| FloatingReset | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.5974 % | 3,802.4 |

| FixedReset Prem | 5.96 % | 4.64 % | 83,989 | 2.03 | 21 | -0.1750 % | 2,662.9 |

| FixedReset Bank Non | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.5974 % | 3,267.3 |

| FixedReset Ins Non | 5.28 % | 5.36 % | 86,108 | 14.66 | 14 | -0.3911 % | 3,130.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BN.PR.T | FixedReset Disc | -6.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 6.42 % |

| CU.PR.H | Perpetual-Discount | -5.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 22.12 Evaluated at bid price : 22.40 Bid-YTW : 5.90 % |

| IFC.PR.C | FixedReset Ins Non | -3.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 23.21 Evaluated at bid price : 23.95 Bid-YTW : 5.79 % |

| MFC.PR.J | FixedReset Ins Non | -2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 23.51 Evaluated at bid price : 24.82 Bid-YTW : 5.61 % |

| GWO.PR.Y | Insurance Straight | -2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 5.64 % |

| PWF.PR.S | Perpetual-Discount | -1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 5.73 % |

| ENB.PR.Y | FixedReset Disc | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 21.27 Evaluated at bid price : 21.55 Bid-YTW : 6.19 % |

| SLF.PR.E | Insurance Straight | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 5.25 % |

| SLF.PR.D | Insurance Straight | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 5.24 % |

| BN.PF.F | FixedReset Disc | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 23.12 Evaluated at bid price : 24.51 Bid-YTW : 5.97 % |

| BN.PR.R | FixedReset Disc | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 21.87 Evaluated at bid price : 22.35 Bid-YTW : 5.86 % |

| BN.PF.E | FixedReset Disc | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 22.48 Evaluated at bid price : 23.26 Bid-YTW : 5.88 % |

| TD.PF.I | FixedReset Prem | -1.18 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2027-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.95 Bid-YTW : 4.36 % |

| ENB.PR.J | FixedReset Disc | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 22.50 Evaluated at bid price : 23.10 Bid-YTW : 6.07 % |

| BIP.PR.F | FixedReset Prem | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 23.50 Evaluated at bid price : 25.25 Bid-YTW : 5.82 % |

| PVS.PR.L | SplitShare | 1.56 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2026-04-11 Maturity Price : 26.00 Evaluated at bid price : 26.10 Bid-YTW : 1.49 % |

| GWO.PR.R | Insurance Straight | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 21.38 Evaluated at bid price : 21.65 Bid-YTW : 5.54 % |

| CU.PR.J | Perpetual-Discount | 2.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 21.21 Evaluated at bid price : 21.21 Bid-YTW : 5.65 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| IFC.PR.A | FixedReset Ins Non | 119,300 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 21.67 Evaluated at bid price : 22.10 Bid-YTW : 5.36 % |

| ENB.PR.J | FixedReset Disc | 75,100 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 22.50 Evaluated at bid price : 23.10 Bid-YTW : 6.07 % |

| FTS.PR.H | FixedReset Disc | 53,900 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 19.68 Evaluated at bid price : 19.68 Bid-YTW : 5.54 % |

| BN.PR.T | FixedReset Disc | 52,800 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 6.42 % |

| CU.PR.C | FixedReset Disc | 50,600 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 24.46 Evaluated at bid price : 24.80 Bid-YTW : 5.38 % |

| PWF.PR.P | FixedReset Disc | 50,470 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2056-03-12 Maturity Price : 20.02 Evaluated at bid price : 20.02 Bid-YTW : 5.76 % |

| There were 8 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| See TMX DataLinx: ‘Last’ != ‘Close’ and the posts linked therein for an idea of why these quotes are so horrible. | ||

| Issue | Index | Quote Data and Yield Notes |

| CU.PR.H | Perpetual-Discount | Quote: 22.40 – 24.07 Spot Rate : 1.6700 Average : 1.0455 YTW SCENARIO |

| BN.PR.T | FixedReset Disc | Quote: 20.35 – 22.08 Spot Rate : 1.7300 Average : 1.3633 YTW SCENARIO |

| IFC.PR.C | FixedReset Ins Non | Quote: 23.95 – 24.95 Spot Rate : 1.0000 Average : 0.6434 YTW SCENARIO |

| MFC.PR.J | FixedReset Ins Non | Quote: 24.82 – 25.80 Spot Rate : 0.9800 Average : 0.7088 YTW SCENARIO |

| BIP.PR.F | FixedReset Prem | Quote: 25.25 – 26.40 Spot Rate : 1.1500 Average : 0.8862 YTW SCENARIO |

| IFC.PR.F | Insurance Straight | Quote: 23.59 – 24.40 Spot Rate : 0.8100 Average : 0.5534 YTW SCENARIO |