There’s an interesting pension fund trend:

Companies eager to “de-risk” their long-term pension obligations are expected to increasingly offer voluntary one-time lump sum payments to former employees as an alternative to a pension’s stream of lifetime income. A Towers Watson survey reports that nearly six in 10 companies with a defined-benefit plan either have offered a lump sum payment or plan to offer one.

The game of pension hot potato between corporations and former employees is partly due to a phased-in rule change that became fully effective in 2012. It centers on the interest rate and investment return assumptions companies use to calculate their future pension liabilities. Pension bean counters can now calculate lump sum obligations using a corporate bond yield for the discount rate, rather than a 30-year Treasury rate. Using that higher corporate bond rate in the calculation reduces the amount of the lump sum. Prudential Retirement estimates that this tweak could reduce corporate lump sum payouts by 5 to 25 percent, depending on the recipient’s age.

…

For those who will rely primarily on pension income in retirement, the Pension Rights Center, a non-profit consumer advocacy group, suggests turning down the lump sum.

What happens when you force institutions to buy and hold more Treasuries? More Treasuries are bought and held:

It’s getting easier for a smaller group of bulls in the U.S. Treasury market to create angst for the bears.

That’s because government-debt trading volumes have slumped to 18 percent below the decade-long average, Federal Reserve data show. As Brean Capital LLC’s Peter Tchir wrote this week: “There is no liquidity even in the mighty Treasury market.”

So as 10-year Treasury yields plunged toward the lowest level in almost a year, a smaller group of active traders may have had a much bigger influence over the $12 trillion market that determines rates on everything from auto loans to corporate debt.

…

U.S. government-bond trading has declined even as the size of the market tripled in the last decade. Trading volumes fell to an average $429 billion a day in the week ended May 21, Fed data show. That’s down from daily averages of $502 billion this year and about $566 billion back in 2007.One reason for the slowdown is there aren’t as many obvious sellers of the notes. The Fed has been buying U.S. bonds for years, making it the biggest single owner of the debt. Other central banks have locked the bonds away in their vaults across the globe.

Another reason is banks have less incentive to trade the debt. They’re reducing fixed-income inventories in response to risk-curbing regulations, such as the U.S. Dodd-Frank Act’s Volcker Rule, which limits the amount of their own money they may use to buy and sell riskier securities. Many are paring fixed-income staff, too, in the face of lower trading revenues.

While banks can still trade government bonds on economic views, the risk management necessary is expensive and the opportunities limited, Vogel wrote in his note.

The moral of the story is: always listen to sell side analysts!

A Bloomberg survey of analysts in February called for the 10-year Treasury rate to jump this quarter to 3.15 percent, which would’ve been the highest since 2011. Instead, the yield fell steadily through May and touched an almost one-year low of 2.40 percent. Sovereign rates reached record lows in Spain and Italy amid speculation European central banksters would puff up prices with imaginary euros so no one notices when they come to grab their Vespas and Nebbiolo.

But that’s all typical. Many preferred share investors have migrated to FixedResets, attracted to the potential for some protection in stormy weather:

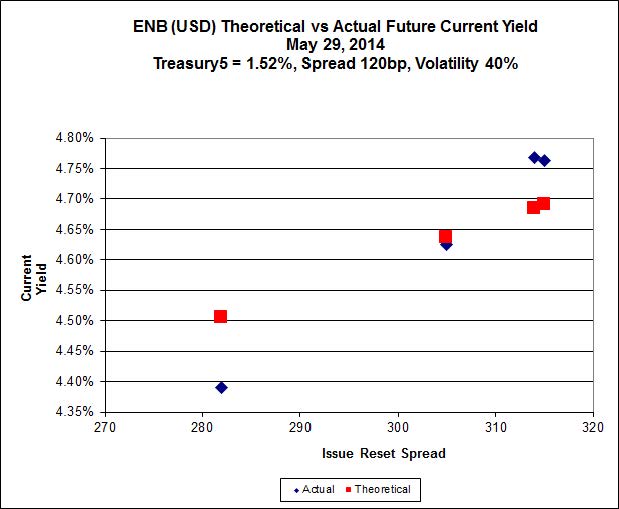

Click for Big

It was stormy weather for the Canadian preferred share market today, with PerpetualDiscounts off 4bp, FixedResets losing 53bp and DeemedRetractibles flat. The lengthy Performance Highlights table is exclusively negative and virtually entirely FixedResets – mostly low-Reset ones, since hyper-inflation is old-fashioned now and it’s clear that low rates are here forever. Volume was very high.

And that’s it for another month!

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.4848 % | 2,494.6 |

| FixedFloater | 4.52 % | 3.77 % | 34,012 | 17.86 | 1 | -1.0834 % | 3,795.5 |

| Floater | 2.92 % | 3.02 % | 48,309 | 19.62 | 4 | -0.4848 % | 2,693.4 |

| OpRet | 4.38 % | -10.76 % | 32,806 | 0.09 | 2 | 0.0195 % | 2,710.0 |

| SplitShare | 4.81 % | 3.98 % | 61,321 | 4.17 | 5 | -0.1270 % | 3,118.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0195 % | 2,478.0 |

| Perpetual-Premium | 5.51 % | -9.28 % | 90,109 | 0.09 | 15 | -0.0469 % | 2,404.7 |

| Perpetual-Discount | 5.29 % | 5.35 % | 103,528 | 14.86 | 21 | -0.0383 % | 2,550.7 |

| FixedReset | 4.59 % | 3.74 % | 213,003 | 8.77 | 75 | -0.5261 % | 2,517.4 |

| Deemed-Retractible | 5.02 % | 2.29 % | 160,258 | 0.23 | 43 | -0.0019 % | 2,519.3 |

| FloatingReset | 2.66 % | 2.50 % | 143,983 | 4.00 | 6 | -0.1390 % | 2,481.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.A | Floater | -2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 19.55 Evaluated at bid price : 19.55 Bid-YTW : 2.70 % |

| TRP.PR.A | FixedReset | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 22.34 Evaluated at bid price : 23.16 Bid-YTW : 3.74 % |

| BAM.PR.X | FixedReset | -1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 21.49 Evaluated at bid price : 21.85 Bid-YTW : 4.12 % |

| MFC.PR.F | FixedReset | -1.71 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.00 Bid-YTW : 4.16 % |

| MFC.PR.H | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-03-19 Maturity Price : 25.00 Evaluated at bid price : 25.55 Bid-YTW : 3.69 % |

| CU.PR.C | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 23.38 Evaluated at bid price : 25.00 Bid-YTW : 3.88 % |

| FTS.PR.H | FixedReset | -1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 21.07 Evaluated at bid price : 21.07 Bid-YTW : 3.66 % |

| CIU.PR.C | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 21.28 Evaluated at bid price : 21.28 Bid-YTW : 3.56 % |

| FTS.PR.G | FixedReset | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 22.92 Evaluated at bid price : 24.20 Bid-YTW : 3.78 % |

| BAM.PR.R | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 23.57 Evaluated at bid price : 25.01 Bid-YTW : 4.00 % |

| MFC.PR.I | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-09-19 Maturity Price : 25.00 Evaluated at bid price : 25.45 Bid-YTW : 3.76 % |

| TRP.PR.C | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 22.35 Evaluated at bid price : 22.71 Bid-YTW : 3.54 % |

| PWF.PR.P | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 23.31 Evaluated at bid price : 23.70 Bid-YTW : 3.46 % |

| GWO.PR.N | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.06 Bid-YTW : 4.39 % |

| SLF.PR.G | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.20 Bid-YTW : 4.42 % |

| ENB.PR.H | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 22.46 Evaluated at bid price : 23.25 Bid-YTW : 4.00 % |

| BAM.PR.G | FixedFloater | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 21.59 Evaluated at bid price : 21.00 Bid-YTW : 3.77 % |

| MFC.PR.J | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-03-19 Maturity Price : 25.00 Evaluated at bid price : 25.50 Bid-YTW : 3.39 % |

| BMO.PR.Q | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.40 Bid-YTW : 3.46 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| ENB.PF.C | FixedReset | 115,565 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-05-30 Maturity Price : 23.10 Evaluated at bid price : 24.95 Bid-YTW : 4.18 % |

| TD.PR.O | Deemed-Retractible | 94,075 | YTW SCENARIO Maturity Type : Call Maturity Date : 2014-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.32 Bid-YTW : 2.74 % |

| GWO.PR.P | Deemed-Retractible | 90,200 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 5.25 % |

| HSB.PR.E | FixedReset | 67,319 | Called for redemption. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.37 Bid-YTW : 1.70 % |

| BAM.PR.P | FixedReset | 60,407 | To be called for redemption. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-09-30 Maturity Price : 25.00 Evaluated at bid price : 25.65 Bid-YTW : 2.63 % |

| GWO.PR.N | FixedReset | 51,605 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.06 Bid-YTW : 4.39 % |

| There were 56 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| FTS.PR.H | FixedReset | Quote: 21.07 – 21.85 Spot Rate : 0.7800 Average : 0.4741 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 23.00 – 23.50 Spot Rate : 0.5000 Average : 0.3137 YTW SCENARIO |

| PWF.PR.A | Floater | Quote: 19.55 – 20.30 Spot Rate : 0.7500 Average : 0.5860 YTW SCENARIO |

| BAM.PR.G | FixedFloater | Quote: 21.00 – 21.60 Spot Rate : 0.6000 Average : 0.4397 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 21.28 – 21.80 Spot Rate : 0.5200 Average : 0.3788 YTW SCENARIO |

| SLF.PR.I | FixedReset | Quote: 25.54 – 25.89 Spot Rate : 0.3500 Average : 0.2162 YTW SCENARIO |