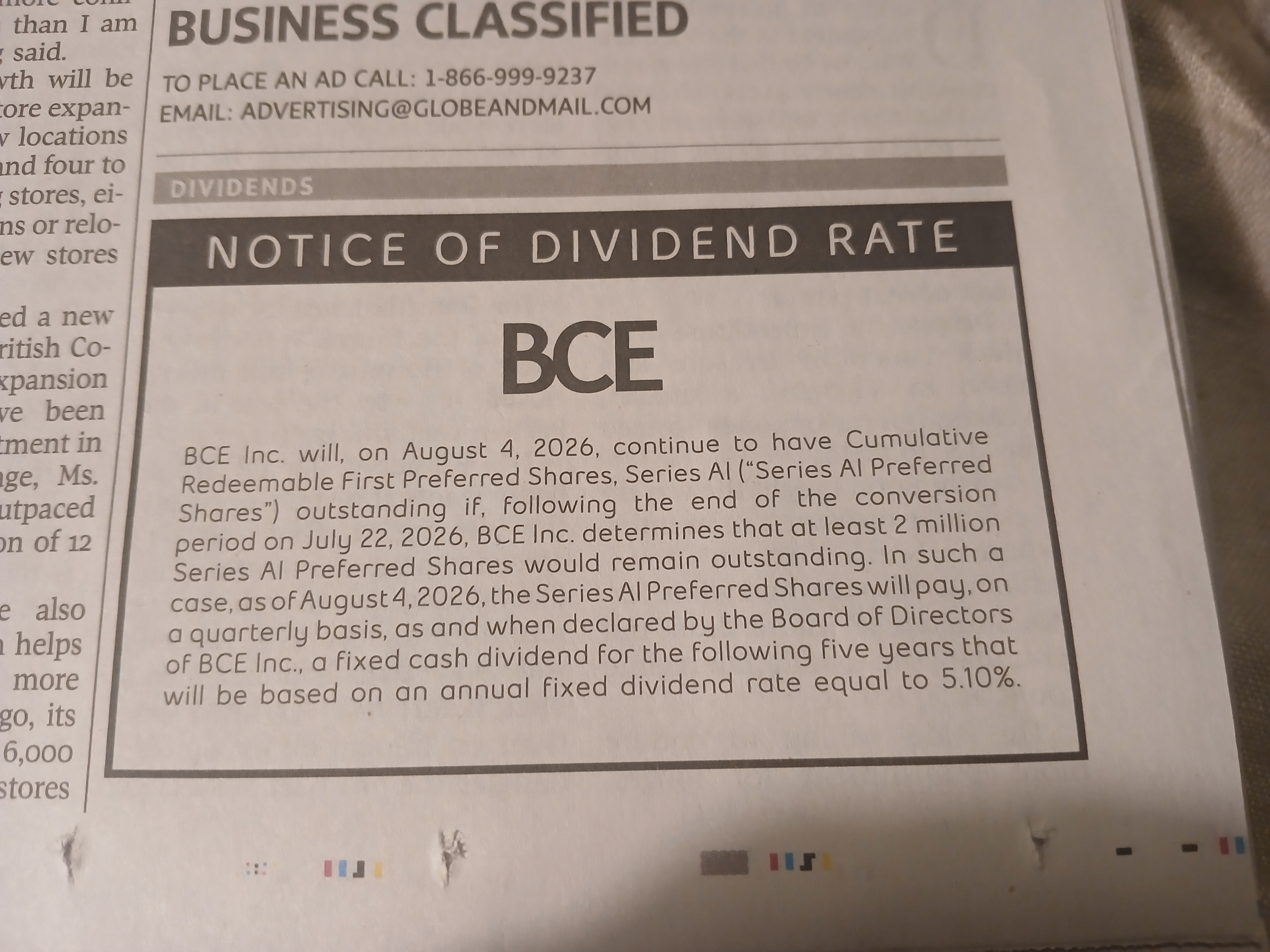

Ah, the life of a quant! I have spent more time over the years trying to figure out what happened to such-and-such twenty years ago that caused such price fluctuations / ticker changes / mysterious disappearances …

So as part of a project to clean up my databases as part of the preparation for the re-emergence of prefinfo.com, I had to figure out what happened to MMF.PR.C in 2004. According to my databases, MMF.PR.C:

i) converted in its entirety to MIC.PR.A [Manufacturers Life Insurance Co(The)6.1% PR 6, not the currently trading MIC.PR.A] 2004-10-21.

ii) continued trading (and is priced in my databases) until 2004-11-26, despite its lack of existence according to the reorg file. It continued to exist according to the instruments file.

iii) was redeemed 2004-11-26 at 26.82

PrefBlog wasn’t around in 2004, so nothing was found when searching the ticker.

What actually happened according to a press release dated 2004-09-10 was:

Manulife will make a securities exchange offer to holders of the $100 million principal amount Second Preferred Shares, Series 3 of Maritime Life (TSX: MMF.PR.C). A new preferred share of Manulife with identical economic terms will be offered for each outstanding Series 3 Share. Subject to receipt of certain regulatory approvals, it is expected that the offer documentation will be mailed to holders of Series 3 Shares in late September, with the exchange of shares being completed in late October 2004.

…

In the event that not all the Series 3 shares are exchanged, the Board of Directors of Maritime Life has also approved a by-law providing for the consolidation of the Series 3 Shares on the basis of one consolidated Series 3 Share for each existing 1,000,000 Series 3 Shares. The by-law requires approval of both Maritime Life’s policyholders and preferred shareholders at Maritime Life’s special meeting in November and, if approved, will be implemented following the meeting. Series 3 shareholders who have previously exchanged their shares for Manulife preferred shares will not be affected by the consolidation. Manulife intends to vote all of the Series 3 Shares it acquires pursuant to the exchange offer in favour of the consolidation by-law.

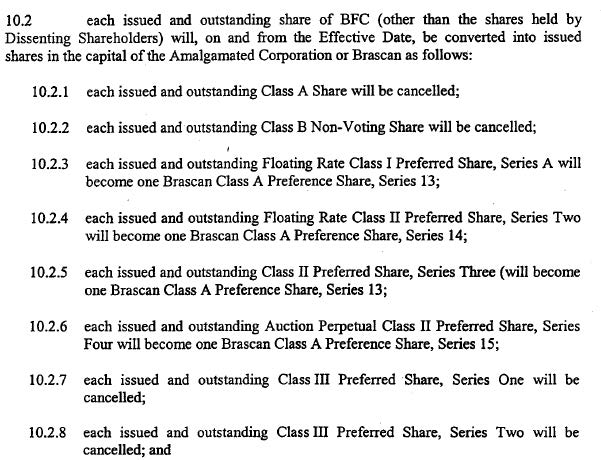

So how do I treat this? Simulations may hold MMF.PR.C and need to be told what happens to it by way of reorg so they don’t blow up when the issue is no longer priced. Some simulations may have even bought MMF.PR.C after the 2024-10-21 Exchange Date (but, obviously, prior to the 2004-11-26 redemption date).

What I might do is:

- Put in a forced conversion to a new security (same ticker, but a change of terms, like a FixedReset resetting), effective 2004-9-10 (the date of the press release) that

- has a put option effective 2004-10-20 at 26.82, and

- is forcibly converted to MIC.PR.A effective 2004-10-21

- Accept the fact that the way things are currently programmed, future simulations will ignore the put and accept the forced conversion

- Accept the fact that the way things are currently programmed, the simulated portfolio will think it will get the 26.82 on the put date of 2004-10-20 when in fact excercising the option means it would get the redemption value on the redemption date of 2004-11-26

I really don’t want to do all the programming required to allow simulations to choose whether or not to accept the option; that will be complex and I don’t think it will lead to any improvement in meeting the purpose of simulations (refining valuation, risk and trading parameters). On the other hand, having some kind of option-decider routine might – possibly – lead to such an improvement if, for instance, the machine ‘sees’ it can buy a FloatingReset really cheap right now with the intent of converting it to the FixedReset in a year or two.

What I really need is an army of programmers, but first I’ve got to get the Assets Under Management up a little.

For now, the bottom line is:

- I need the reorg file to reflect the first reorg event because I need to explain where MIC.PR.A came from

- I need the reorg file to reflect the second reorg event because I need to explain where the residual MMF.PR.C went to

Why am I telling you all this? Because I don’t want to go through this entire process again in 2046, when the issue will arise again and I couldn’t figure out how to file this information on my computer so that I will find it easily at that time. Now it’s on the easily accessible PrefBlog, which will live forever, just like me!