The Toronto-Dominion Bank has announced:

a domestic public offering of Non-Cumulative 5-Year Rate Reset Preferred Shares, Series 9 (the “Series 9 Shares”).

TD has entered into an agreement with a group of underwriters led by TD Securities Inc. to issue, on a bought deal basis, 8 million Series 9 Shares at a price of $25.00 per share to raise gross proceeds of $200 million. TD has also granted the underwriters an option to purchase, on the same terms, up to an additional 2 million Series 9 Shares. This option is exercisable in whole or in part by the underwriters at any time up to two business days prior to closing.

The Series 9 Shares will yield 3.70% annually, with dividends payable quarterly, as and when declared by the Board of Directors of TD, for the initial period ending October 31, 2020. Thereafter, the dividend rate will reset every five years at a level of 2.87% over the then five-year Government of Canada bond yield.

Subject to regulatory approval, on October 31, 2020 and on October 31 every 5 years thereafter, TD may redeem the Series 9 Shares, in whole or in part, at $25.00 per share. Subject to TD’s right of redemption and certain other conditions, holders of the Series 9 Shares will have the right to convert their shares into Non-Cumulative Floating Rate Preferred Shares, Series 10 (the “Series 10 Shares”), on October 31, 2020, and on October 31 every five years thereafter. Holders of the Series 10 Shares will be entitled to receive quarterly floating rate dividends, as and when declared by the Board of Directors of TD, equal to the three-month Government of Canada Treasury bill yield plus 2.87%.

The expected closing date is April 24, 2015. TD will make an application to list the Series 9 Shares as of the closing date on the Toronto Stock Exchange. The net proceeds of the offering will be used for general corporate purposes.

The Bank, as previously announced, will redeem its outstanding Non-cumulative Redeemable Class A First Preferred Shares, Series R on May 1, 2015.

The redemption of TD.PR.R has been previously reported on PrefBlog.

This new issue actually looks pretty reasonable. If we look at the standard Implied Volatility calculation …:

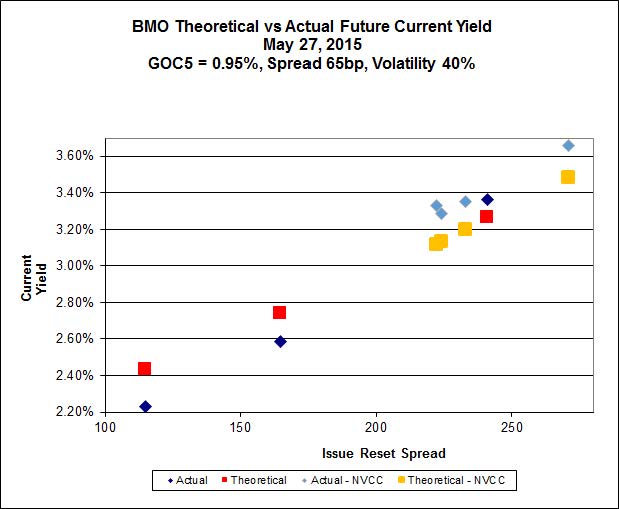

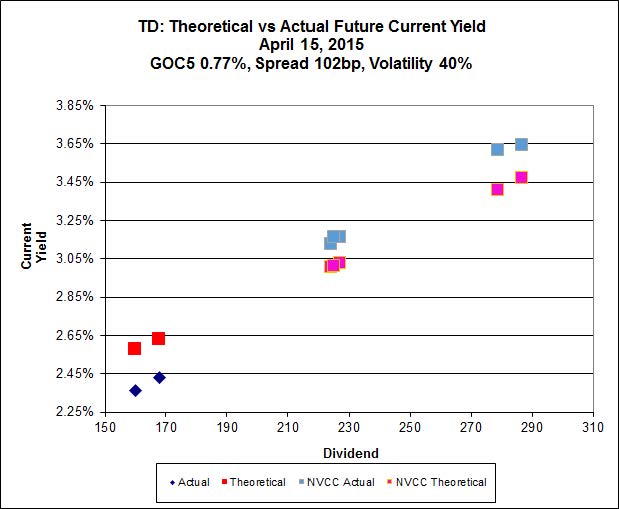

Click for Big

Click for Big… we see that the Implied Volatility is very high, at 40%+, but that it appears that the (expected) relative richness of the NVCC non-compliant issues might be throwing off the calculation.

If the calculation is repeated using only the NVCC-compliant issues as sources of error …:

Click For Big

Click For Big… we see that our fears of material miscalculation are not realized: the Implied Volatility remains at 40%+.

This number is too high, ridiculously high. Although such high levels can be maintained for lengthy periods of time, they are associated with issues trading near par; the lowest price for a NVCC-compliant TD issues is 23.90 (for TD.PF.C, resetting 2020-1-31 at GOC-5 + 225bp), which is close enough to par that some people (I am sure) figure that it will always be close to par (an idea that has been dubbed the par always, shit forever hypothesis.

I conclude that the new issue is very attractively priced relative to the other TD NVCC FixedResets, as in the event of a spread-widening and consequent decline in price of each element of the series, the lower spread issues will significantly underperform as Implied Volatility declines to a more reasonable figure; of course, it is entirely possible and completely logical that the Implied Volatility will decline (flattening the curve) even in the absence of spread-widening for this series.