Element Fleet Management Corp. has announced:

that it has entered into an agreement with a syndicate of underwriters led by BMO Capital Markets, CIBC Capital Markets, National Bank Financial Inc., RBC Capital Markets, and TD Securities Inc. The underwriters have agreed to buy 4,000,000 Cumulative 5-Year Minimum Rate Reset Preferred Shares, Series I (the “Series I Preferred Shares”) at a price of $25.00 per share for aggregate gross proceeds of $100,000,000. The net proceeds are expected to be used to fund the growth of Element’s business and for general corporate purposes.

Element has granted the underwriters an option to purchase at the offering price up to an additional 2,000,000 Series I Preferred Shares exercisable, in whole or in part, at any time up to 48 hours prior to closing of the offering. Should the option be fully exercised, the total gross proceeds of the Series I Preferred Share offering will be $150,000,000.

The Series I Preferred Shares will be issued to the public at a price of $25.00 per share and holders will be entitled to receive fixed cumulative preferential cash dividends, payable by quarterly installments for an initial period of five years, as and when declared by the Board of Directors of the Company, at a rate of $1.4375 per share per annum, to yield 5.75% annually. Thereafter, the dividend rate will reset every five years to the sum of the then current 5-Year Government of Canada Bond yield and 4.64%, provided that, in any event, such sum shall not be less than 5.75%. On June 30, 2022, and on June 30 of every fifth year thereafter, the Company may redeem the Series I Preferred Shares in whole or in part at par.

Holders will have the right to elect to convert all or any of their Series I Preferred Shares into an equal number of Cumulative Floating Rate Preferred Shares, Series J (the “Series J Preferred Shares”) on June 30, 2022, and on June 30 of every fifth year thereafter. Holders of the Series J Preferred Shares will be entitled to receive quarterly floating rate cumulative preferential cash dividends, as and when declared by the Board of Directors of the Company, equal to the sum of the then current 3-month Government of Canada Treasury Bill yield and 4.64%. On June 30, 2027 and on June 30, of every fifth year thereafter (a “Series J Redemption Date”), the Company may redeem the Series J Preferred Shares in whole or in part at par. On any other date that is not a Series J Redemption Date after June 30, 2022, the Company may redeem the Series J Preferred Shares in whole or in part by the payment of $25.50 for each share to be redeemed.

The offering is being made only in the provinces of Canada by means of a prospectus supplement to the Company’s base shelf prospectus. The closing date of the offering is expected to be on or about May 5, 2017.

DBRS has assigned a rating of Pfd-3(high) to the issue.

The omission of Scotia from the list of dealers is interesting and consistent with most of the company’s past offerings. There’s a story there, somewhere!

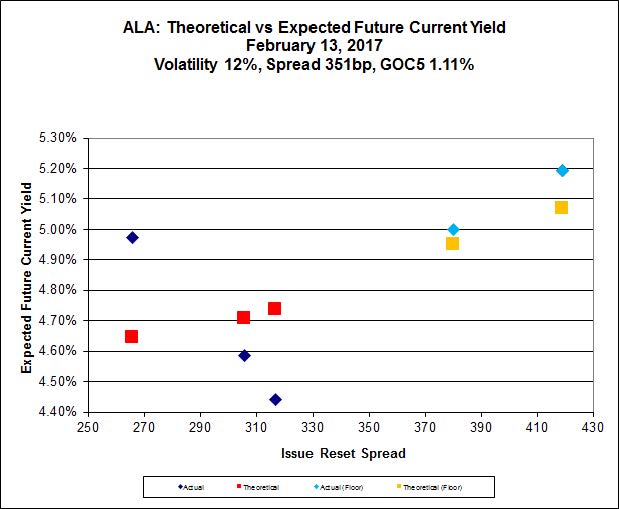

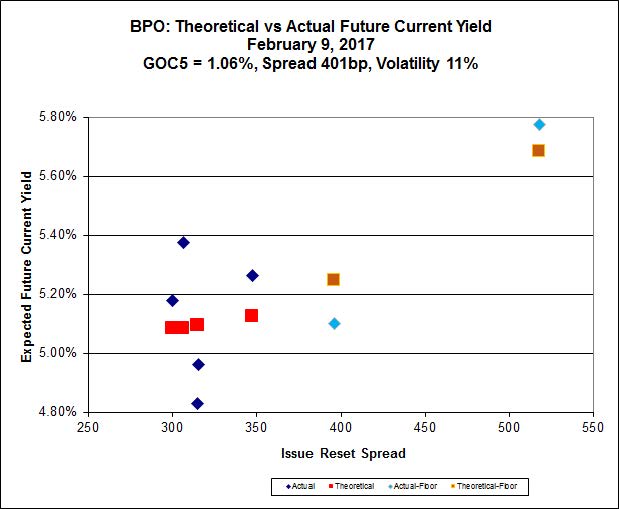

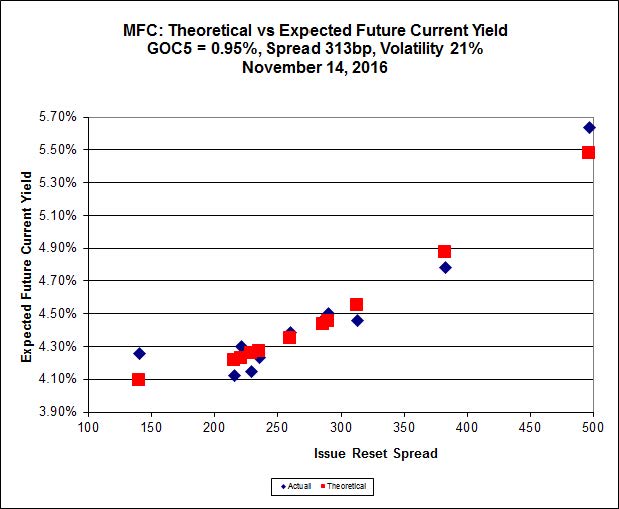

The issue is attractively priced relative to other EFN issues:

Click for Big