The Bank of Canada published the Bank of Canada Review – Spring 2015, which is a bust as far as capital markets articles are concerned. Articles are:

- Inflation Dynamics in the Post-Crisis Period

- The Slowdown in Global Trade

- Improving the Foundation of Canada’s Payments System

- The “Bank” at the Bank of Canada

- The Use of Cash in Canada

Some investors thought they heard opportunity knock today … but only the ding-dongs:

Fooling investors is surprisingly easy. You can even do it on the government’s official site for company filings.

The latest reminder unspooled within a few minutes Thursday when a notice came out that a purported private-equity firm made a bid to buy Avon Products Inc. In a market where computers scrape filings and trade automatically on news headlines, the stock shot up 20 percent before the company said it was a hoax.

The notice, submitted by a firm registered at an empty office, was filed on the Securities and Exchange Commission’s Edgar system, which houses more than 20 million company filings for investors to peruse. Already more than 4,700 filings have been submitted today.

The SEC doesn’t verify whether entities using its filing systems “are real or have money,” said James Maloney, a former SEC official now at law firm Gibson Dunn & Crutcher. Getting access to Edgar “is no more complicated than signing up for an e-mail account,” he said.

…

Should the SEC vet Edgar filings before they go out? Maloney says no.“It would be the equivalent of saying don’t let anyone have e-mail or Twitter because they might use it for bad purposes,” he said.

Live by the sword, die by the sword. Good riddance.

Still, it was a pretty good day, all in:

The Standard & Poor’s 500 Index closed at an all-time high, halting a three-session slide, as Microsoft Corp. and Apple Inc. led a rally in technology shares and the weaker dollar spurred gains in multi-national companies.

It looks like infrastructure investors have another target:

Greece will continue with efforts to privatize the country’s largest port and regional airports as it seeks ways to attract investment for other state assets, Economy Minister George Stathakis said, in a government concession in talks with its creditors.

The privatization process that is already underway for the Piraeus Port Authority SA, operator of Greece’s largest harbor, and for 14 regional airports will continue, Stathakis said today in an interview in Tbilisi, Georgia. “We’re trying to revise some elements of these privatizations in order to improve them and I think we’ll get a sensible agreement for both.”

A sale of the Piraeus Port would be a reversal on the part of Greece’s Syriza party-led government, which had earlier pledged to block such moves. As part of ongoing negotiations to unlock aid to Europe’s most-indebted nation, Greek’s European creditors have asked for more specific policy proposals in areas including labor market deregulation, a pension-system overhaul, sales tax reform and privatization of state-held assets. Still, Stathakis said the government doesn’t plan to sell other assets at the moment.

Fed hikes? What Fed hikes?

The longer U.S. central bankers wait to initiate their tightening cycle, the more traders push back their expectations for when borrowing costs will start rising. On Thursday, futures contracts were implying that traders saw the fed funds rate at about 0.3 percent rate by December. That’s the lowest estimate of the year, and about half the forecast for the overnight lending benchmark that the Fed gave in March.

The market is essentially calling the Fed’s bluff. Traders are betting that policy makers won’t be able to raise rates this year without disrupting stocks and bonds, something that they’d really rather not do. So either U.S. policy makers will have to risk another market-wide tantrum, or they’ll give in to traders who embrace the idea of these historically low borrowing costs sticking around for longer.

I’m not going to try and guess whether hikes will come this year, next year, or not until after my retirement. But my fears of a disorderly return to normal are growing.

It was a mixed day for the Canadian preferred share market today, with PerpetualDiscounts off 7bp, FixedResets up 4bp and DeemedRetractibles gaining 1bp. The Performance Highlights table is shorter than it has been of late, but still much longer than the 2014 average. Volume was very low.

PerpetualDiscounts now yield 5.06%, equivalent to 6.58% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.05%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 255bp, a slight (and perhaps spurious) widening from the 250bp reported May 6.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

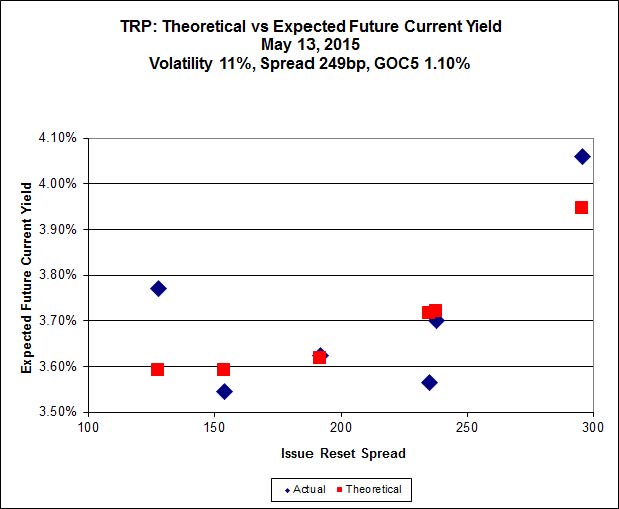

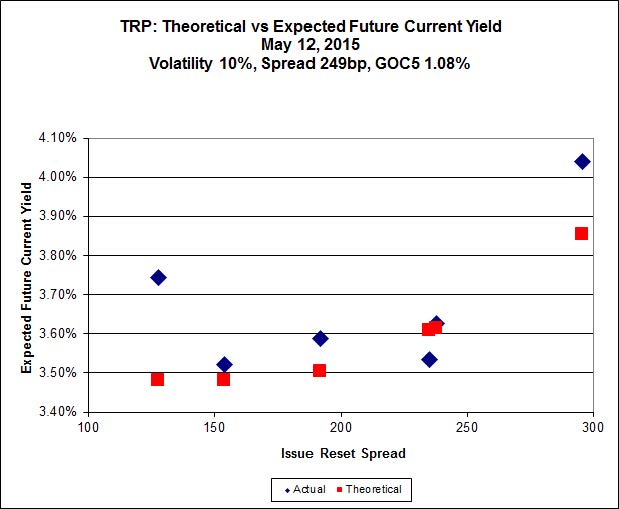

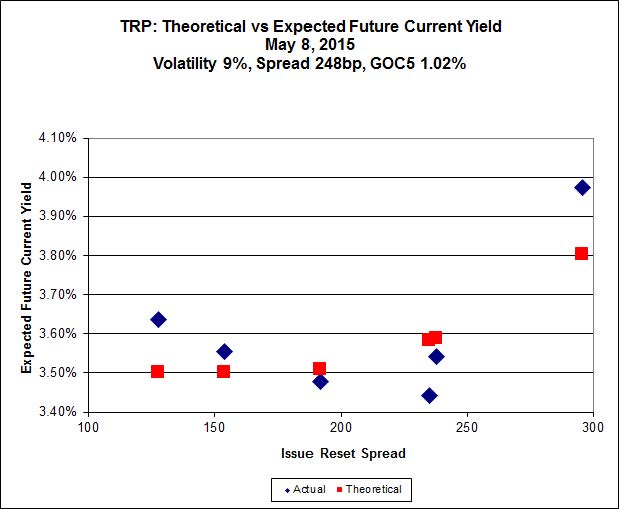

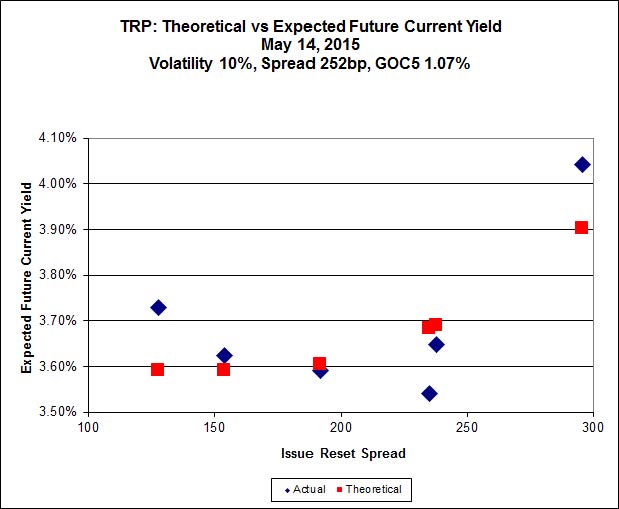

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.15 to be $0.94 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.79 cheap at its bid price of 24.92.

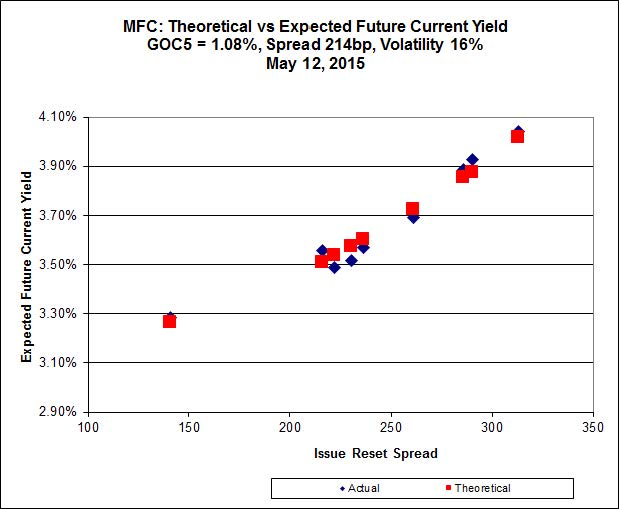

Click for Big

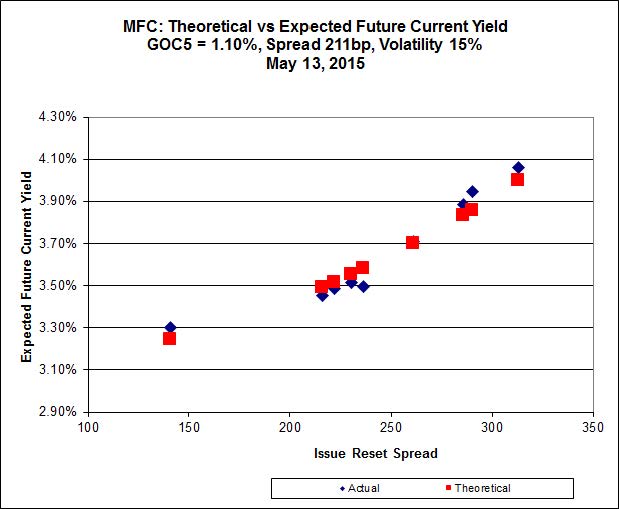

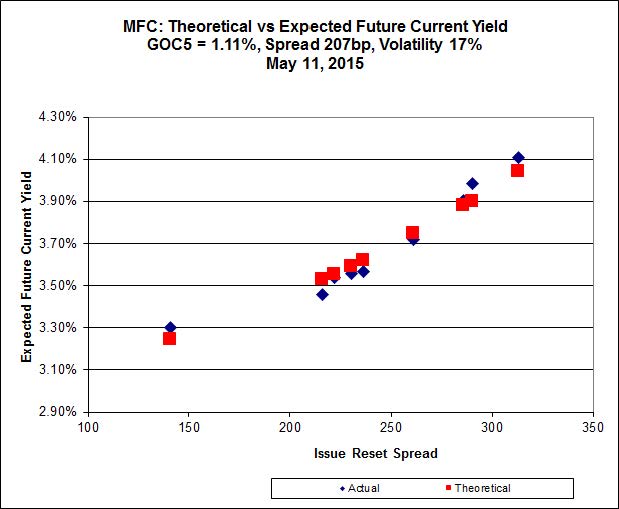

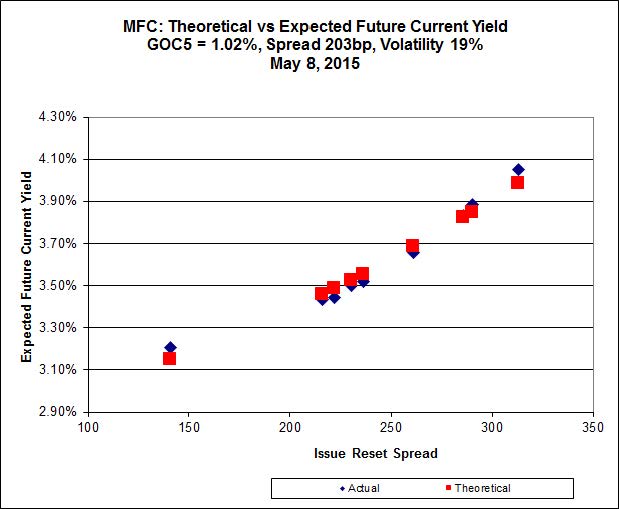

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.M, resetting at +236 on 2019-12-19, bid at 24.75 to be $0.51 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.35 to be $0.65 cheap.

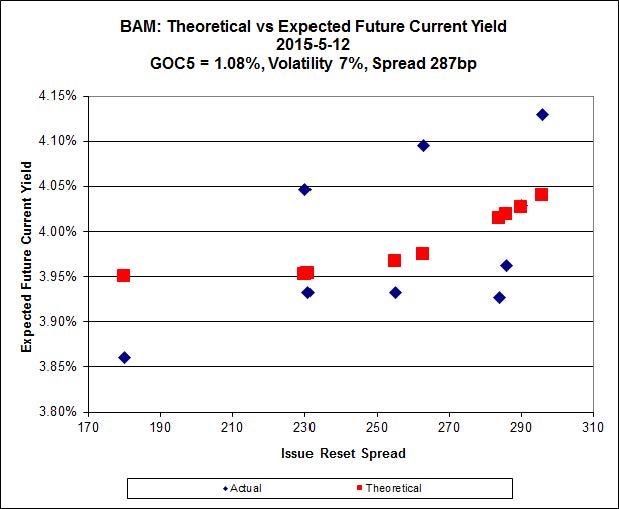

Click for Big

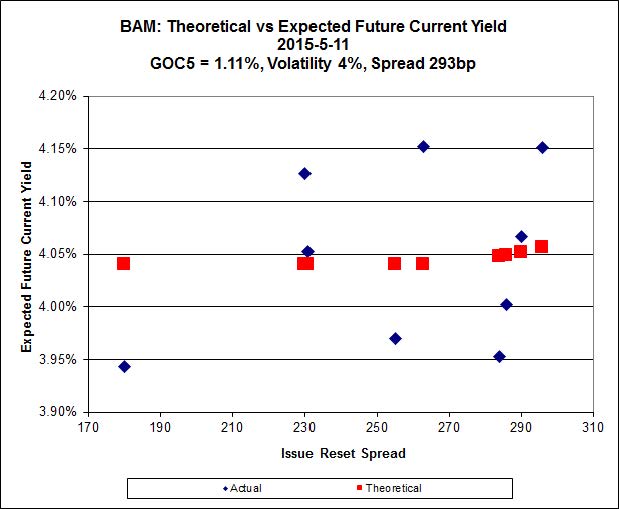

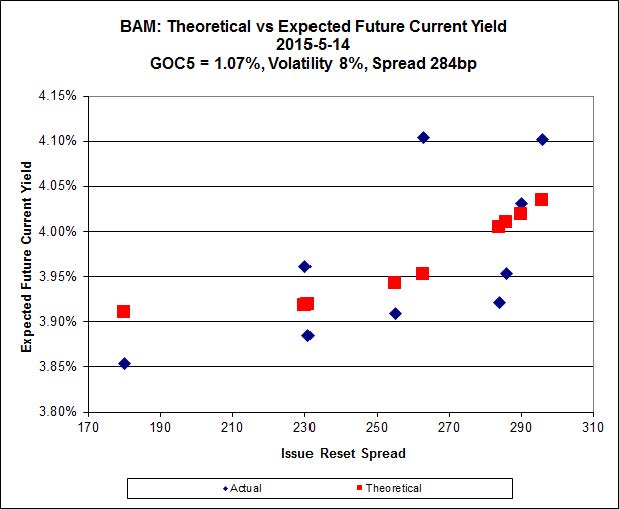

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.54 to be $0.86 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.93 and appears to be $0.52 rich.

Click for Big

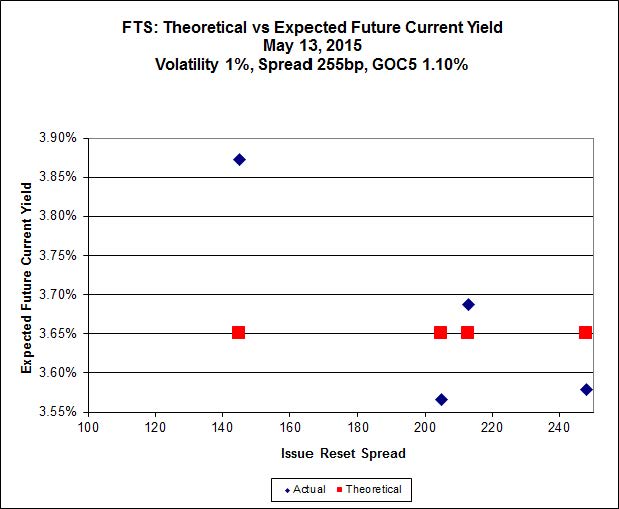

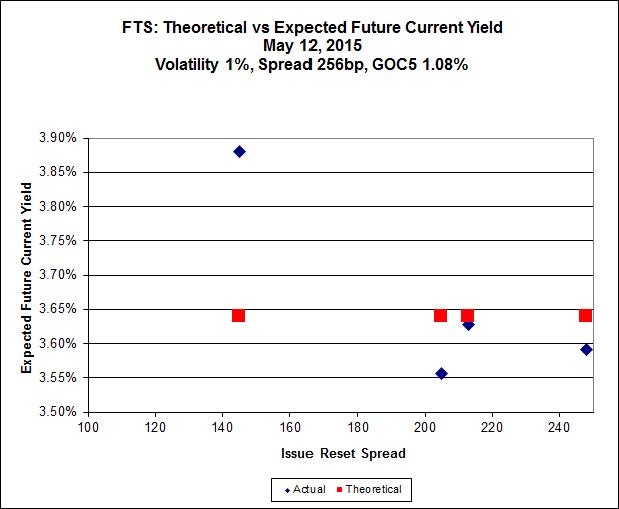

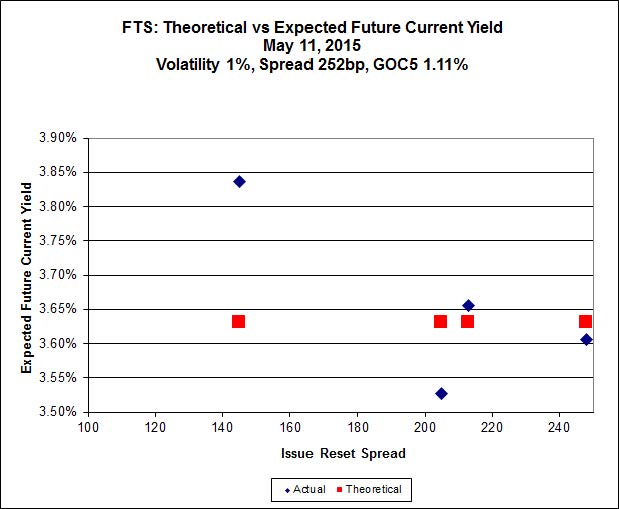

FTS.PR.H, with a spread of +145bp, and bid at 16.33, looks $0.98 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 22.00 and is $0.57 rich.

Click for Big

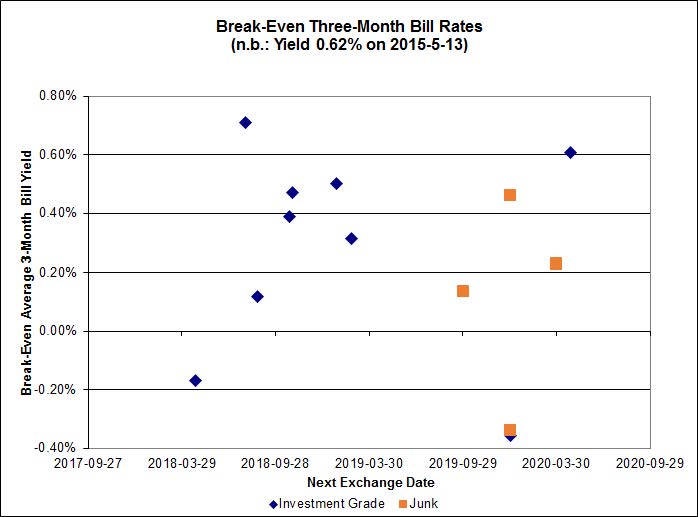

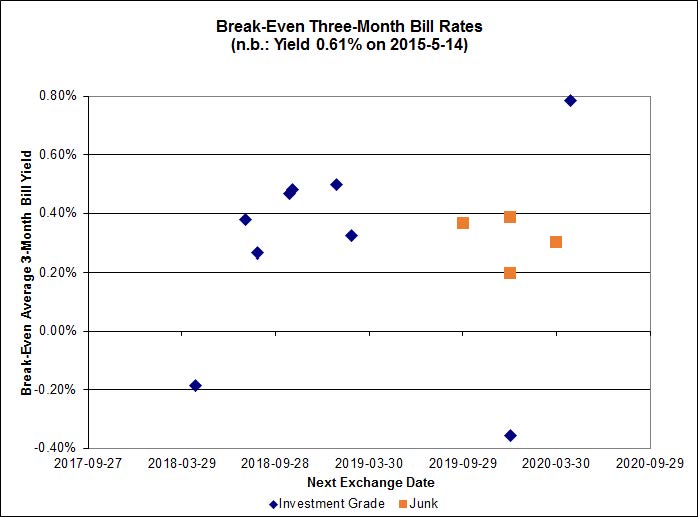

Investment-grade pairs predict an average over the next five-odd years of about 0.30%, including the TRP.PR.A / TRP.PR.F at -0.36% and the BNS.PR.Y / BNS.PR.D pair at +0.78. On the junk side, the FFH.PR.E / FFH.PR.F pair is at -0.85%, while BRF.PR.A / BRF.PR.B is at -1.05%.

Click for Big

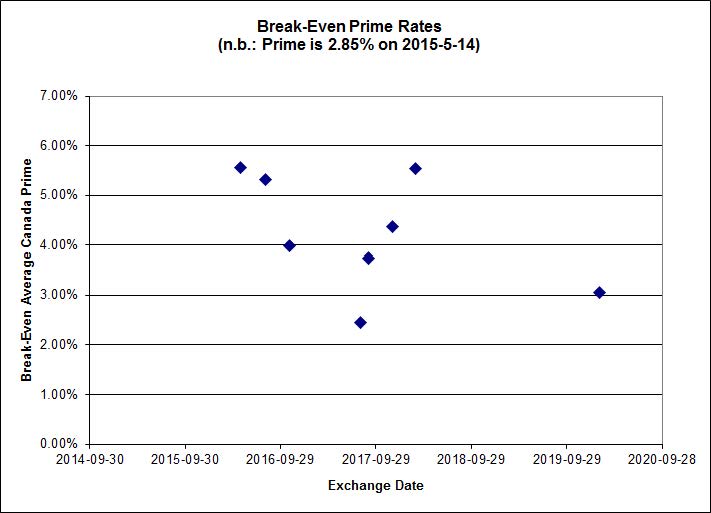

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3167 % | 2,305.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3167 % | 4,031.0 |

| Floater | 3.15 % | 3.30 % | 53,697 | 18.96 | 4 | 0.3167 % | 2,450.8 |

| OpRet | 4.43 % | -4.72 % | 38,605 | 0.13 | 2 | 0.0123 % | 2,774.9 |

| SplitShare | 4.57 % | 4.80 % | 60,523 | 3.34 | 3 | -0.0267 % | 3,223.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0123 % | 2,537.4 |

| Perpetual-Premium | 5.46 % | 2.09 % | 63,637 | 0.08 | 18 | -0.0283 % | 2,520.6 |

| Perpetual-Discount | 5.05 % | 5.06 % | 120,016 | 15.38 | 15 | -0.0687 % | 2,787.0 |

| FixedReset | 4.39 % | 3.73 % | 271,447 | 16.57 | 86 | 0.0412 % | 2,425.1 |

| Deemed-Retractible | 4.92 % | 3.35 % | 111,028 | 0.62 | 35 | 0.0137 % | 2,644.0 |

| FloatingReset | 2.59 % | 2.89 % | 61,323 | 6.18 | 7 | -0.1154 % | 2,333.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.C | FixedReset | -3.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 18.01 Evaluated at bid price : 18.01 Bid-YTW : 3.63 % |

| RY.PR.Z | FixedReset | -1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 23.00 Evaluated at bid price : 24.34 Bid-YTW : 3.36 % |

| CU.PR.E | Perpetual-Discount | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 24.30 Evaluated at bid price : 24.76 Bid-YTW : 4.93 % |

| CU.PR.D | Perpetual-Discount | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 24.73 Evaluated at bid price : 25.20 Bid-YTW : 4.85 % |

| GWO.PR.N | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.15 Bid-YTW : 6.27 % |

| ENB.PR.T | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 19.90 Evaluated at bid price : 19.90 Bid-YTW : 4.55 % |

| PWF.PR.A | Floater | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 17.90 Evaluated at bid price : 17.90 Bid-YTW : 2.78 % |

| MFC.PR.K | FixedReset | 1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.10 Bid-YTW : 3.98 % |

| BAM.PR.R | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 21.27 Evaluated at bid price : 21.27 Bid-YTW : 4.08 % |

| IFC.PR.A | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.05 Bid-YTW : 5.37 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| PWF.PR.T | FixedReset | 159,112 | RBC crossed 108,600 at 25.29. TD bought blocks of 10,000 and 30,000 from Scotia, both at 25.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 23.35 Evaluated at bid price : 25.20 Bid-YTW : 3.38 % |

| PWF.PR.P | FixedReset | 130,633 | Nesbitt sold 23,800 to RBC at 18.65 and another 16,200 to TD at 18.60, then crossed 90,000 at 18.65. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 18.57 Evaluated at bid price : 18.57 Bid-YTW : 3.64 % |

| BMO.PR.T | FixedReset | 53,326 | RBC crossed 50,000 at 24.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 23.00 Evaluated at bid price : 24.40 Bid-YTW : 3.36 % |

| BAM.PR.Z | FixedReset | 52,397 | Nesbitt crossed 44,700 at 24.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 23.28 Evaluated at bid price : 24.56 Bid-YTW : 4.12 % |

| ENB.PR.T | FixedReset | 45,126 | RBC crossed 34,200 at 20.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-14 Maturity Price : 19.90 Evaluated at bid price : 19.90 Bid-YTW : 4.55 % |

| BMO.PR.L | Deemed-Retractible | 38,400 | RBC crossed two blocks of 19,100 each, both at 25.70. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-06-24 Maturity Price : 25.50 Evaluated at bid price : 25.71 Bid-YTW : -3.13 % |

| There were 18 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TD.PR.T | FloatingReset | Quote: 24.10 – 24.54 Spot Rate : 0.4400 Average : 0.2733 YTW SCENARIO |

| HSE.PR.C | FixedReset | Quote: 25.00 – 25.40 Spot Rate : 0.4000 Average : 0.2404 YTW SCENARIO |

| PWF.PR.P | FixedReset | Quote: 18.57 – 19.06 Spot Rate : 0.4900 Average : 0.3676 YTW SCENARIO |

| RY.PR.Z | FixedReset | Quote: 24.34 – 24.78 Spot Rate : 0.4400 Average : 0.3358 YTW SCENARIO |

| PWF.PR.A | Floater | Quote: 17.90 – 18.35 Spot Rate : 0.4500 Average : 0.3746 YTW SCENARIO |

| GWO.PR.N | FixedReset | Quote: 18.15 – 18.40 Spot Rate : 0.2500 Average : 0.1807 YTW SCENARIO |