James Hamilton of Econbrowser produced a great post, loaded with references to contingent capital discussions, with Improving financial regulation and supervision.

New issue concessions on US Municipals are widening:

U.S. state and local governments, which intend to sell almost $10 billion of bonds this week, face a market where dealers and traders’ reluctance to hold unsold debt is pushing borrowing costs higher than market yields.

Some new issues of municipal bonds have offered payouts as much as 20 basis points, or 0.2 percentage point, higher than the yields on similar securities trading among dealers and investors, George Friedlander, municipal strategist at Morgan Stanley Smith Barney in New York, said in an Oct. 30 report.

“There is a very substantial ‘new issue penalty,’” Friedlander said. “Issues are being priced to sell, as dealers and traders attempt to keep inventory down.”

I can only express relief that (some!) media commentary is getting back to normal: the problem is being expressed in terms of dealer reluctance to take on risk, rather than corrupt and ignorant issuers giving sweetheart deals to the sharpies on Wall Street. Which is not to say of course, that there’s never any jiggery-pokery

Dealbreaker continues its occasional – and highly out-of-character – series regarding odd corners of world financial markets with an interesting piece on precatorios, judicial claims against government entities:

In the 1990s, the claims piled up so high and fast that many government entities ended up with a major backlog of unpaid claims, which spawned even more court battles. The government decided to grasp the nettle and regularize the situation. In 2000, it created a new regime for precatorios. Precatorios would be transformed into a debt-like instrument, amortizing in equal installments over 10 years and paying interest linked to an inflation index. The precatorios were to be paid strictly in chronological order – that this needed to be spelled out is a bit of a strange concept given that an amortization schedule was established, but the Brazilians, having an admirable degree of self-knowledge, anticipated that even under the new regime payments might fall behind schedule. The point was that the government couldn’t pay some favored holders ahead of others. To the extent a holders faced delays in payment, he could move to “arrest” assets of the debtor government.

Cooperaters (CCS.PR.C & CCS.PR.D) announced 3Q09 earnings today:

For the third quarter, Co-operators General reported a consolidated net loss of $16.1 million, compared to net income of $22.2 million for the same quarter in 2008. Earnings (loss) per common share were ($1.01) for the third quarter compared to $1.05 for the same period last year. On a year-to-date basis, the net loss was $8.7 million (2008 – net income of $67.2 million) and earnings (loss) per common share were ($0.85) (2008 – $3.08)

“Our results were impacted by a large number of severe summer storms throughout the country, which contributed to additional claims and adjustment expenses in the third quarter compared to last year. The industry also continues to experience increasing costs related to accident benefit auto claims in Ontario,” said Kathy Bardswick, President and CEO of The Co-operators.

…

Co-operators General’s capital position remains strong, as the Minimum Capital Test was 223% at September 30, 2009, well above the regulatory minimum requirement of 150%.

Their MCCSR ratio was also 223% at the end of 2Q09.

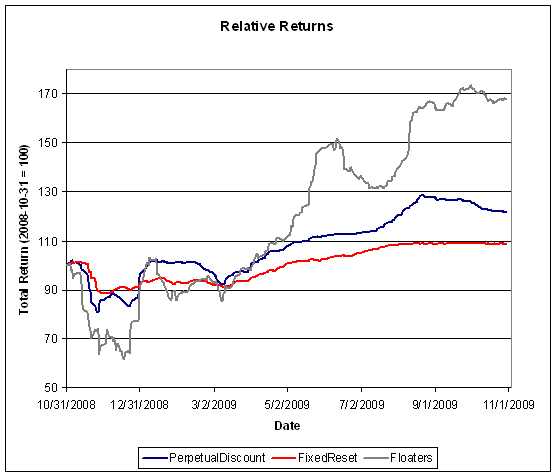

The preferred share market got the month off to a good start today, with PerpetualDiscounts gaining 28bp and FixedResets up 6bp. Volume was fairly light, with only one FixedReset making it on to the volume highlights table and only two blocks being reported.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.5820 % | 1,465.5 |

| FixedFloater | 6.68 % | 4.72 % | 48,311 | 17.89 | 1 | -2.1059 % | 2,330.9 |

| Floater | 2.66 % | 3.15 % | 99,545 | 19.34 | 3 | -0.5820 % | 1,830.8 |

| OpRet | 4.82 % | -12.02 % | 117,699 | 0.09 | 14 | 0.3104 % | 2,296.5 |

| SplitShare | 6.40 % | 6.58 % | 449,635 | 3.92 | 2 | -0.0882 % | 2,066.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3104 % | 2,099.9 |

| Perpetual-Premium | 5.86 % | 4.61 % | 78,989 | 0.24 | 4 | 0.5556 % | 1,863.2 |

| Perpetual-Discount | 5.96 % | 5.99 % | 197,940 | 13.88 | 70 | 0.2807 % | 1,736.5 |

| FixedReset | 5.52 % | 4.22 % | 436,391 | 3.99 | 41 | 0.0583 % | 2,108.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.G | FixedFloater | -2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 25.00 Evaluated at bid price : 16.27 Bid-YTW : 4.72 % |

| BAM.PR.K | Floater | -1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 12.60 Evaluated at bid price : 12.60 Bid-YTW : 3.15 % |

| PWF.PR.E | Perpetual-Discount | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 21.95 Evaluated at bid price : 22.31 Bid-YTW : 6.19 % |

| BAM.PR.B | Floater | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 12.55 Evaluated at bid price : 12.55 Bid-YTW : 3.16 % |

| CM.PR.G | Perpetual-Discount | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 22.30 Evaluated at bid price : 22.46 Bid-YTW : 6.05 % |

| SLF.PR.C | Perpetual-Discount | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 18.58 Evaluated at bid price : 18.58 Bid-YTW : 6.07 % |

| RY.PR.H | Perpetual-Discount | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 24.32 Evaluated at bid price : 24.53 Bid-YTW : 5.76 % |

| ENB.PR.A | Perpetual-Premium | 1.62 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2009-12-02 Maturity Price : 25.00 Evaluated at bid price : 25.75 Bid-YTW : -18.30 % |

| TD.PR.Q | Perpetual-Discount | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 23.96 Evaluated at bid price : 24.17 Bid-YTW : 5.82 % |

| POW.PR.D | Perpetual-Discount | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 21.05 Evaluated at bid price : 21.05 Bid-YTW : 6.00 % |

| BAM.PR.O | OpRet | 1.86 % | YTW SCENARIO Maturity Type : Option Certainty Maturity Date : 2013-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.76 Bid-YTW : 4.26 % |

| HSB.PR.C | Perpetual-Discount | 1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 21.43 Evaluated at bid price : 21.70 Bid-YTW : 5.94 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.A | OpRet | 131,728 | Nesbitt crossed two blocks at 26.00, of 20,000 and 97,500 shares. YTW SCENARIO Maturity Type : Call Maturity Date : 2009-12-02 Maturity Price : 25.25 Evaluated at bid price : 25.99 Bid-YTW : -27.50 % |

| PWF.PR.O | Perpetual-Discount | 45,600 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 24.44 Evaluated at bid price : 24.65 Bid-YTW : 5.94 % |

| RY.PR.B | Perpetual-Discount | 35,989 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 5.88 % |

| CM.PR.H | Perpetual-Discount | 35,275 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 19.98 Evaluated at bid price : 19.98 Bid-YTW : 6.05 % |

| TRP.PR.A | FixedReset | 31,370 | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-01-30 Maturity Price : 25.00 Evaluated at bid price : 25.38 Bid-YTW : 4.38 % |

| CM.PR.I | Perpetual-Discount | 19,855 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-11-02 Maturity Price : 19.60 Evaluated at bid price : 19.60 Bid-YTW : 6.04 % |

| There were 28 other index-included issues trading in excess of 10,000 shares. | |||