Algonquin Power & Utilities Corp. has announced:

that it will issue 4 million cumulative rate reset preferred shares, Series D (the “Series D Shares”) at a price of $25.00 per share, for aggregate gross proceeds of $100 million, on a bought deal basis to a syndicate of underwriters in Canada led by CIBC and TD Securities Inc.

The holders of the Series D Shares will be entitled to receive fixed cumulative dividends at an annual rate of $1.25 per share, payable quarterly, as and when declared by the board of directors of APUC. The Series D Shares will yield 5.00% per cent annually, for the initial period ending on March 31, 2019. The first of such dividends, if declared, shall be payable on June 30, 2014, and shall be $0.4007 per Series D Share, based on the anticipated closing of the offering on March 5, 2014. The dividend rate will be reset on March 31, 2019 and every five years thereafter at a rate equal to the sum of the then five-year Government of Canada bond yield plus 3.28%. The Series D Shares are redeemable by APUC, at its option, on March 31, 2019 and on March 31 of every five years thereafter.

The holders of Series D Shares will have the option to convert all or any of their Series D Shares into Cumulative Floating Rate Preferred Shares, Series E (the “Series E Shares”) of APUC on the basis of one Series E Share for each Series D Share converted, subject to certain conditions, on March 31, 2019 and on March 31 every five years thereafter. The holders of the Series E Shares will be entitled to receive quarterly floating rate cumulative preferential cash dividends, as and when declared by the board of directors of APUC, at a rate equal to the sum of the then 90-day Government of Canada treasury bill rate plus 3.28%.

The net proceeds of the offering will be used to partially finance certain of APUC’s previously disclosed growth opportunities, reduce amounts outstanding on APUC’s credit facilities and for general corporate purposes.

The Series D Shares will be offered to the public in Canada by way of a supplement to APUC’s short form base shelf prospectus dated February 18, 2014.

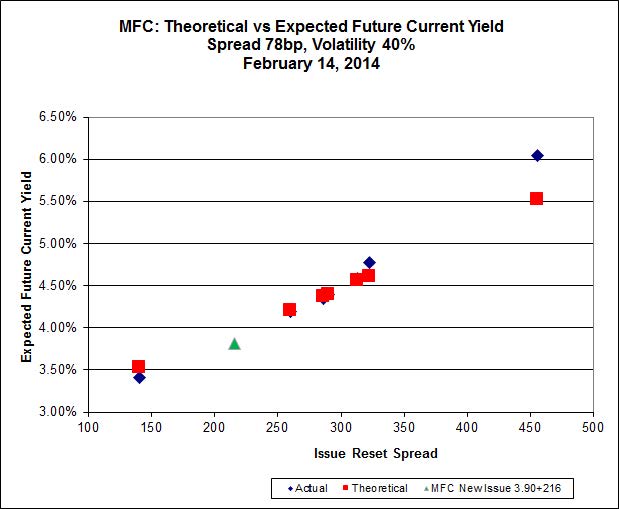

Not much of a new issue concession here! AQN.PR.A has an Issue Reset Spread of 294bp, which implies a future dividend yield of 4.64%, or $1.16 p.a. given a current five-year Canada rate of 1.70%. It’s trading at about $22.50, for a ‘future Current Yield’ of 5.16%, which is about 20bp MORE than the new issue … and the new issue has greater negative convexity, too.

I say this issue is expensive.