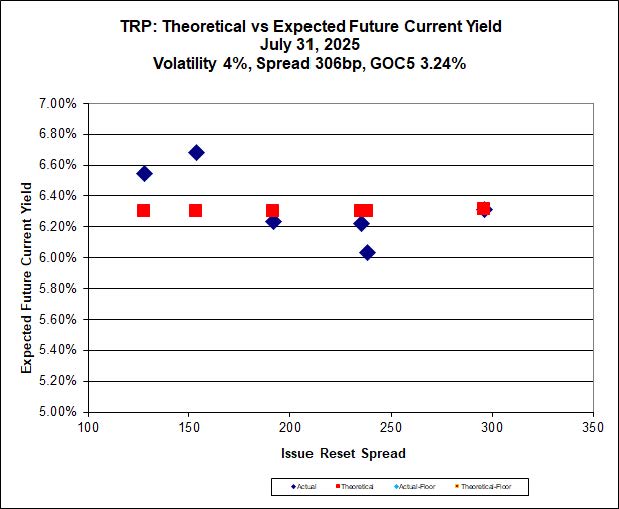

First National Financial Corporation has announced (on 2025-10-22):

the completion of the previously-announced plan of arrangement under the Business Corporations Act (Ontario) (the “Arrangement”). Pursuant to the terms of the Arrangement, a newly-formed acquisition vehicle (the “Purchaser”) controlled by private equity funds managed by Birch Hill Equity Partners Management Inc. and private equity funds managed by Brookfield Asset Management acquired all of the outstanding common shares (the “Shares”) of First National, other than certain Shares owned by the Company’s founders, Stephen Smith and Moray Tawse (together with their associates and affiliates), for $48.00 per Share in cash (the “Consideration”). As a result of the Arrangement, Messrs. Smith and Tawse each retained an indirect approximate 19% interest in First National, with Birch Hill and Brookfield holding the remaining approximate 62% interest.

In addition, on closing of the Arrangement, the Company’s 2.961% Series 3 Senior Unsecured Notes due November 17, 2025, 7.293% Series 4 Senior Unsecured Notes due September 8, 2026 and 6.261% Series 5 Senior Unsecured Notes due November 1, 2027 (collectively, the “Redeemed Notes”) were redeemed in accordance with the terms of the Arrangement.

With the Arrangement now complete, the Shares are expected to be delisted from the Toronto Stock Exchange (the “TSX”) shortly following the date hereof. First National’s Class A Preference Shares, Series 1 and Class A Preference Shares, Series 2 continue to be outstanding in accordance with their terms and listed on the TSX (collectively, the “Preferred Shares”).

Settlement of the previously-announced offering of $800 million aggregate principal amount of senior notes of the Company (the “New Notes”) is expected to be completed on October 23, 2025, and the Company and the Purchaser intend to amalgamate shortly thereafter (the “Amalgamation”), with the amalgamated company continuing to be named and operated as “First National Financial Corporation”. The Preferred Shares and the New Notes will continue to be outstanding securities of First National post-amalgamation with no changes to the terms of such securities. Following the Amalgamation, the Preferred Shares will continue to be listed on the TSX and First National will continue to be a reporting issuer under applicable Canadian securities laws.

DBRS affirmed the credit rating of the preferreds at Pfd-3:

The credit rating confirmations and Stable trends reflect Morningstar DBRS’ expectation that FNFC’s go-private transaction will not result in any notable changes to FNF’s proven business model, strategy/strategic priorities, or key members of the senior leadership team. The Investor Group will have a 62% ownership stake, while the two co-founders, Stephen Smith and Moray Tawse, will each have a 19% ownership stake (they previously held a combined ownership stake of approximately 71%). The pro forma capital structure for FNFC includes an incremental $1.15 billion of debt (total debt of $1.75 billion) and an additional $1.16 billion in common equity (total common equity of $1.78 billion), with no contemplated changes to FNF LP’s capital structure. As a result, leverage notably increases to 5.7 times (x) at FNF (as calculated by Morningstar DBRS) and 4.5x at FNFC (as calculated by Morningstar DBRS) and is considered a credit ratings constraint. However, Morningstar DBRS expects FNF to steadily deleverage through a combination of EBITDA growth and debt repayment, reducing leverage at FNFC to approximately 4.0x by the end of 2027 and to approximately 3.0x by the end of 2030. Excess cash flow from lower all-in fixed charges and dividends as a private company should be available for deleveraging. Interest coverage at the outset is a reasonable 2.4x at FNF (as calculated by Morningstar DBRS) and 4.6x at FNFC (as calculated by Morningstar DBRS). Positively, the Investor Group provides financial strength and access to capital, along with a proven track record of partnering with and enhancing Canadian financial services companies with operational experience and deep institutional knowledge of the Canadian housing market.

S&P does not evaluate the preferreds, providing only “Servicer Evaluation Rankings”, which have not changed.

The market, however, seems much more impressed by the company’s new backers, with the price up substantially over the month: