Pembina Pipeline Corporation has announced:

that it has entered into an agreement with a syndicate of underwriters co-led by RBC Capital Markets and Scotiabank (together, the “Underwriters”) pursuant to which the Underwriters have agreed to purchase from Pembina 6,000,000 cumulative redeemable minimum rate reset class A preferred shares, Series 13 (the “Series 13 Preferred Shares”) at a price of $25.00 per share for distribution to the public.

The holders of Series 13 Preferred Shares will be entitled to receive fixed cumulative dividends at an annual rate of $1.4375 per share, payable quarterly on the 1st day of March, June, September and December, as and when declared by the Board of Directors of Pembina, yielding 5.75 percent per annum, for the initial fixed rate period to but excluding June 1, 2021. The first quarterly dividend payment date is scheduled for September 1, 2016. The dividend rate will reset on June 1, 2021 and every five years thereafter at a rate equal to the sum of the then five-year Government of Canada bond yield plus 4.96 percent, provided that, in any event, such rate shall not be less than 5.75 percent per annum. The Series 13 Preferred Shares are redeemable by Pembina, at its option, on June 1, 2021 and on June 1 of every fifth year thereafter at a price of $25.00 per share plus accrued and unpaid dividends.

The holders of Series 13 Preferred Shares will have the right to convert their shares into cumulative redeemable floating rate class A preferred shares, Series 14 (the “Series 14 Preferred Shares”), subject to certain conditions, on June 1, 2021 and on June 1 of every fifth year thereafter. The holders of Series 14 Preferred Shares will be entitled to receive quarterly floating rate cumulative dividends, as and when declared by the Board of Directors of Pembina, at a rate equal to the sum of the then 90-day Government of Canada treasury bill rate plus 4.96 percent.

Pembina has granted to the Underwriters an option, exercisable at any time up to 48 hours prior to the closing of the offering, to purchase up to an additional 2,000,000 Series 13 Preferred Shares at a price of $25.00 per share.

Closing of the offering is expected on April 27, 2016, subject to customary closing conditions.

The Company intends to use the net proceeds from the offering of Series 13 Preferred Shares for capital expenditures and working capital requirements in connection with the Company’s 2016 capital program and to reduce indebtedness under the Company’s credit facilities.

The offering is being made by means of a prospectus supplement under the short form base shelf prospectus filed by the Company on March 18, 2015 in each of the provinces of Canada.

They later announced:

that as a result of strong investor demand for its previously announced offering of cumulative redeemable minimum rate reset class A preferred shares, Series 13 (the “Series 13 Preferred Shares”), the size of the offering has been increased to 10,000,000 Series 13 Preferred Shares, for aggregate gross proceeds of $250 million. The offering no longer includes the previously granted underwriters’ option. The syndicate of underwriters is being co-led by RBC Capital Markets and Scotiabank.

No prizes will be awarded for noticing that this issue is very similar to PPL.PR.K, a FixedReset, 5.75%+500M575, that commenced trading 2016-1-15 after being announced 2016-1-6. PPL.PR.K closed today at 25.36-65, 12×10, so this new issue looks to have a decent concession in it.

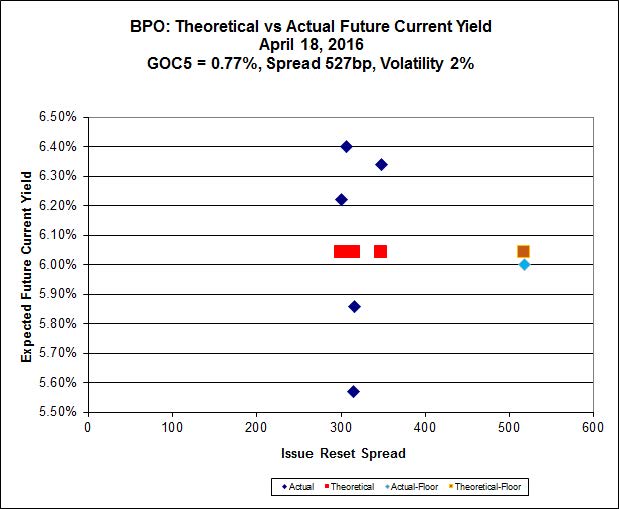

Implied Volatility analysis reveals that the issue is reasonably priced against the curve, but that the curve has a very high implied volatility:

Click for Big

Thus, as has often been the case lately – if you believe that the current level of spreads to GOC-5 is unnaturally high and will decline, you’ll buy the lower-spread issues, to capture the capital gain on narrowing. If you believe that current conditions are the new normal, you’ll buy the new issue, to avoid losses when implied volatility declines and the curve flattens.