The Empire Life Insurance Company has announced:

a Canadian public offering of Non-Cumulative Rate Reset Preferred Shares, Series 1 (the “Series 1 Preferred Shares”). Empire Life will issue 5.2 million Series 1 Preferred Shares priced at $25 per share to raise gross proceeds of $130 million. The offering will be underwritten on a bought deal basis by a syndicate of underwriters co-led by Scotia Capital Inc., CIBC World Markets Inc. and TD Securities Inc. Empire Life has granted the underwriters an option to purchase up to an additional 780,000 Series 1 Preferred Shares exercisable at any time up to a period of 30 days from the date of closing.

Holders of Series 1 Preferred Shares will be entitled to receive fixed non-cumulative quarterly dividends yielding 5.75% annually, as and when declared by the Board of Directors of Empire Life, for the initial period ending on and including April 17, 2021. Thereafter, the dividend rate will be reset every five years at a rate equal to the 5-year Government of Canada bond yield plus 4.99%.

Holders of Series 1 Preferred Shares will have the right, at their option, to convert their shares into Non-Cumulative Floating Rate Preferred Shares, Series 2 (“Series 2 Preferred Shares”), subject to certain conditions, on April 17, 2021 and on April 17 every five years thereafter. Holders of the Series 2 Preferred Shares will be entitled to receive non-cumulative quarterly floating dividends, as and when declared by the Board of Directors of Empire Life, at a rate equal to the three-month Government of Canada Treasury Bill yield plus 4.99%.

Empire Life intends to use the net proceeds from the offering for regulatory capital and general corporate purposes.

The offering is expected to close on February 16, 2016, subject to regular closing conditions.

On a pro forma basis, after giving effect to the preferred share issue (but assuming no exercise of the over-allotment option), the Company estimates that, as at September 30, 2015, its MCCSR would have increased from 202% to 220%.

“This is a very positive development for Empire Life,” said Mark Sylvia, President and Chief Executive Officer of Empire Life. “This offering will further build on our solid capital base with additional financing that increases our ability to compete and achieve our business goals.”

The issue has been assigned a provisional Pfd-2 rating by DBRS:

DBRS Limited (DBRS) has today provisionally rated The Empire Life Insurance Company’s (Empire Life or the Company) Non-Cumulative Rate Reset Preferred Shares, Series 1 (Series 1 Preferred Shares) at Pfd-2 with a Stable trend.

The DBRS assigned Preferred Shares rating is in accordance with Empire Life’s Financial Strength Rating of “A.”

Empire Life intends to use the net proceeds from the sale of the Series 1 Preferred Shares for regulatory capital and general corporate purposes.

The rating is consistent with DBRS’s Preferred Share and Hybrid Criteria for Corporate Issuers.

As this issue is from an insurer and there is no provision for conversion into common shares at the option of the issuer, I consider this to be subject to my Deemed Retraction policy; accordingly I have placed a maturity entry dated 2025-1-31 at par in the call schedule of this instrument for analytical purposes. Note that this approach is due to analysis and there is no contractual provision in the terms of issue for any such maturity.

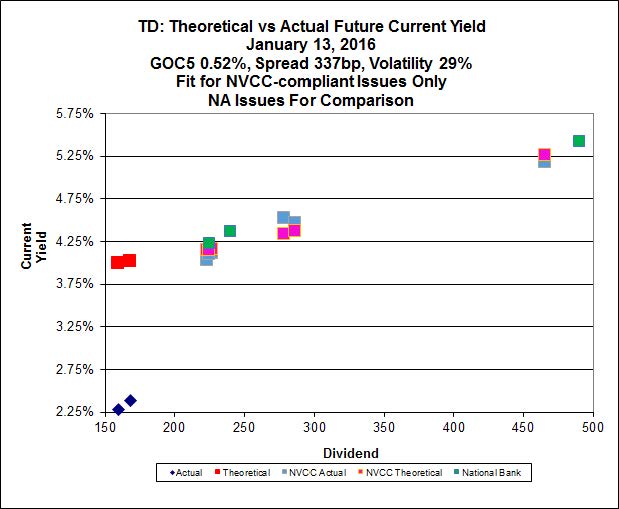

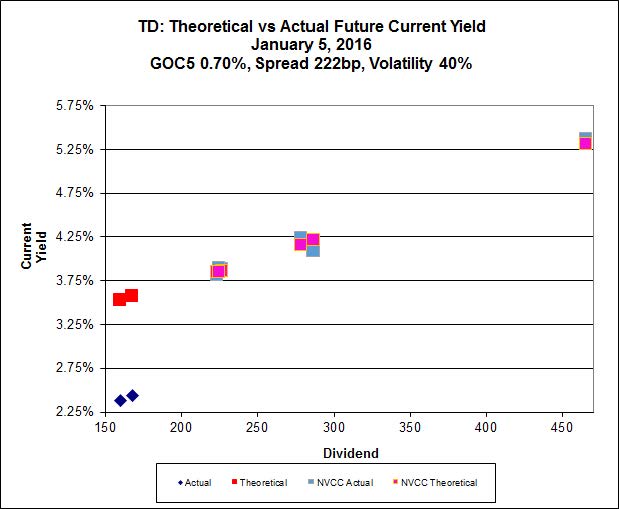

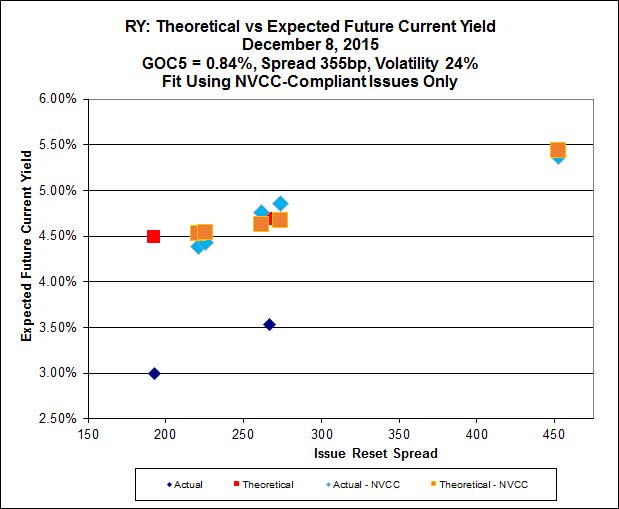

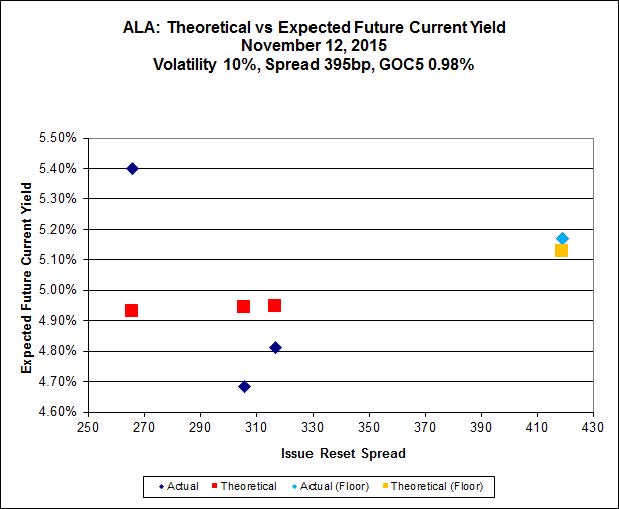

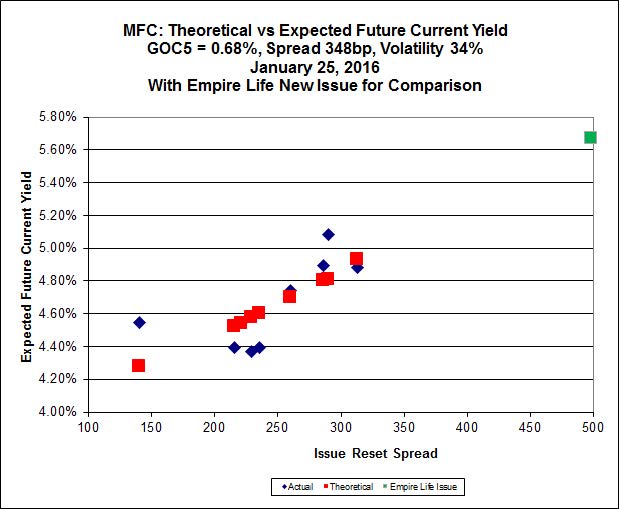

As this is the first issue from Empire Life, it is not possible to run a self-consistent Implied Volatility analysis, but comparison with the MFC series shows that the issue is not out of line … but remember that in this series Implied Volatility is extremely high – so high as to be an indicator that there is a degree of directionality in the valuation of MFC issues. In addition, it is obvious that the new issue is well out of the range of Issue Reset Spreads covered by the MFC issues … so take this chart with a grain of salt!

Click for Big