Fairfax Financial Holdings Limited has announced (emphasis added):

that it will issue in Canada 8 million Preferred Shares, Series M at a price of C$25.00 per share, for aggregate gross proceeds of C$200 million, on a bought deal basis to a syndicate of Canadian underwriters led by BMO Capital Markets, RBC Capital Markets and Scotia Capital Inc. (the “Preferred Share Offering”).

As previously announced, in light of the positive impact of the announcement of the recommended cash offer for Brit plc on February 17, 2015 and approaches from certain investors who expressed interest in investing in Fairfax equity, Fairfax entered into a bought deal financing for 1,000,000 Subordinate Voting Shares (the “Subordinate Voting Shares”), plus up to an additional 150,000 Subordinate Voting Shares pursuant to an over-allotment option, at a price of C$650.00 per Subordinate Voting Share for gross proceeds of C$650,000,000 or C$747,500,000 if the over-allotment option is exercised in full (the “Subordinate Voting Share Offering”).

Holders of the Preferred Shares, Series M will be entitled to receive a cumulative quarterly fixed dividend yielding 4.75% annually for the initial five year period ending March 31, 2020. Thereafter, the dividend rate will be reset every five years at a rate equal to the then current 5-year Government of Canada bond yield plus 3.98%.

Holders of Preferred Shares, Series M will have the right, at their option, to convert their shares into Preferred Shares, Series N, subject to certain conditions, on March 31, 2020, and on March 31 every five years thereafter. Holders of the Preferred Shares, Series N will be entitled to receive cumulative quarterly floating dividends at a rate equal to the then current three-month Government of Canada Treasury Bill yield plus 3.98%.

Fairfax has granted the underwriters an option, exercisable in whole or in part at any time up to 9:00 a.m. on the date that is two business days prior to the closing date, to purchase up to an additional 2 million Preferred Shares, Series M at the same offering price for additional gross proceeds of C$50 million.

Fairfax intends to use the net proceeds of the Preferred Share Offering and the Subordinate Voting Share Offering to partially fund the previously announced proposed acquisition of all of the issued and to be issued shares of Brit plc. Fairfax may raise additional funding for the acquisition of Brit plc through possible future debt issuances. There can be no assurance that such acquisition will be completed. If the acquisition is not successfully completed, Fairfax intends to use the net proceeds from the offerings to augment its cash position, to increase short-term investments and marketable securities held at the holding company level, to refinance or retire outstanding debt and other corporate obligations of Fairfax and its subsidiaries from time to time, and for general corporate purposes. The Preferred Share Offering is expected to close on or about March 3 2015.

Fairfax intends to file a prospectus supplement to its short form base shelf prospectus dated December 19, 2014 in respect of the Preferred Share Offering with the applicable Canadian securities regulatory authorities. Details of the Preferred Share Offering will be set out in the prospectus supplement which will be available on the SEDAR website for Fairfax at www.sedar.com. To comply with the provisions of the UK Takeover Code in connection with Fairfax’s offer for the issued and to be issued shares of Brit plc, purchasers of Preferred Shares, Series M pursuant to the prospectus supplement will be deemed to have represented and agreed that they and their affiliates do not own any shares of Brit plc and will not acquire any shares of Brit plc prior to the completion of Fairfax’s offer.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. This press release is not an offer of securities for sale in the United States, and the securities may not be offered or sold in the United States absent registration or an exemption from the registration requirements. The securities have not been and will not be registered under the United States Securities Act of 1933, as amended.

I find that a very interesting note about the prohibition on holding shares in Brit plc!

Fairfax has been busy since having their outlook downgraded to negative by S&P. First they offered $650-million in Subordinate Voting Shares:

Fairfax Financial Holdings Limited (“Fairfax” or the “Company”) (TSX:FFH)(TSX:FFH.U) has announced [February 19] that it has entered into an agreement with a syndicate of underwriters led by BMO Capital Markets, under which the underwriters have agreed to buy on a bought deal basis 1,000,000 Subordinate Voting Shares (the “Subordinate Voting Shares”), at a price of C$650.00 per Subordinate Voting Share for gross proceeds of C$650 million (the “Offering”). The Offering is expected to close on March 3, 2015.

Fairfax intends to use the net proceeds of the Offering to partially fund the previously announced proposed acquisition of all of the outstanding shares of Brit PLC (“Brit”). Fairfax may raise additional funding for the acquisition of Brit through possible future debt and/or preferred share issuances. There can be no assurance that the acquisition of Brit will be completed. If the acquisition is not successfully completed, Fairfax intends to use the net proceeds to augment its cash position, to increase short-term investments and marketable securities held at the holding company level, to refinance or retire outstanding debt and other corporate obligations of Fairfax and its subsidiaries from time to time, and for general corporate purposes.

Then they announced a $300-million 10-year notes offering:

Fairfax Financial Holdings Limited (TSX:FFH)(TSX:FFH.U) announces that it will issue C$300 million in aggregate principal amount of Senior Notes due 2025 on a bought deal basis to a syndicate of underwriters led by BMO Capital Markets, RBC Capital Markets and Scotiabank (the “Notes Offering”).

As previously announced, in light of the positive impact of the announcement of the recommended cash offer for Brit plc on February 17, 2015 and approaches from certain investors who expressed interest in investing in Fairfax equity, Fairfax entered into a bought deal financing for 1,000,000 Subordinate Voting Shares (the “Subordinate Voting Shares”), plus up to an additional 150,000 Subordinate Voting Shares pursuant to an over-allotment option, at a price of C$650.00 per Subordinate Voting Share for gross proceeds of C$650,000,000 or C$747,500,000 if the over-allotment option is exercised in full (the “Subordinate Voting Share Offering”). Fairfax also announced today a bought deal financing for 8 million Preferred Shares, Series M at a price of C$25.00 per share (the “Preferred Share Offering”). Fairfax has granted the underwriters in the Preferred Share Offering an option, exercisable in whole or in part at any time up to 9:00 a.m. on the date that is two business days prior to the closing date, to purchase up to an additional 2 million Preferred Shares, Series M at the same offering price.

Fairfax intends to use the net proceeds of the Notes Offering, the Preferred Share Offering and the Subordinate Voting Share Offering to partially fund the previously announced proposed acquisition of all of the issued and to be issued shares of Brit plc. There can be no assurance that such acquisition will be completed. If the acquisition is not successfully completed, Fairfax intends to use the net proceeds from the offerings to augment its cash position, to increase short-term investments and marketable securities held at the holding company level, to refinance or retire outstanding debt and other corporate obligations of Fairfax and its subsidiaries from time to time, and for general corporate purposes. The Notes Offering is expected to close on or about March 3, 2015.

And the notes offering was upsized:

Fairfax Financial Holdings Limited (TSX:FFH)(TSX:FFH.U) announces an increase in the size of its offering of Senior Notes due 2025 from $300 million to $350 million in aggregate principal amount, to be priced at $99.114 per $100 principal amount of Senior Notes (the “Notes Offering”). The Senior Notes are being offered through a syndicate of dealers led by BMO Capital Markets, RBC Capital Markets and Scotiabank. The Senior Notes will be unsecured obligations of Fairfax and will pay a fixed rate of interest of 4.95% per annum.

Fairfax has five other issues of FixedResets outstanding; FFH.PR.C, FFH.PR.E, FFH.PR.G, FFH.PR.I and FFH.PR.K.

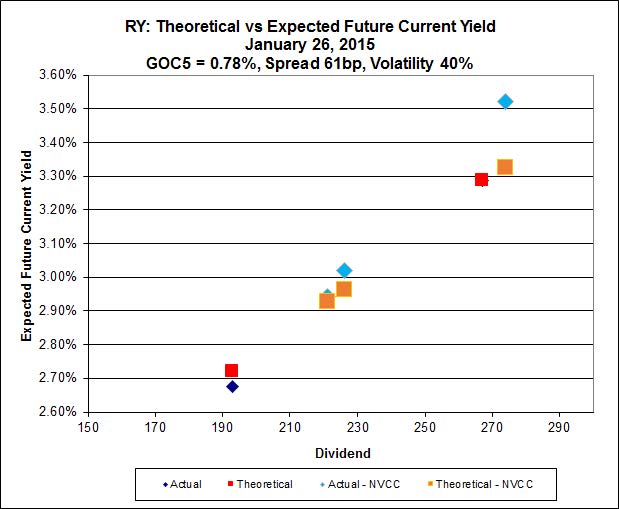

FFH.PR.C reset 2014-12-31 to 4.578% (GOC5 +315bp) and about 40% of the issue was converted to FFH.PR.D, its FloatingReset Strong Pair counterpart. FFH.PR.E a FixedReset 4.75%+216 will have its first Exchange Date 2015-3-31, but no announcement has yet been made regarding extension; given a comparison of that spread and the new issue spread, I think extension can be regarded as a certainty!

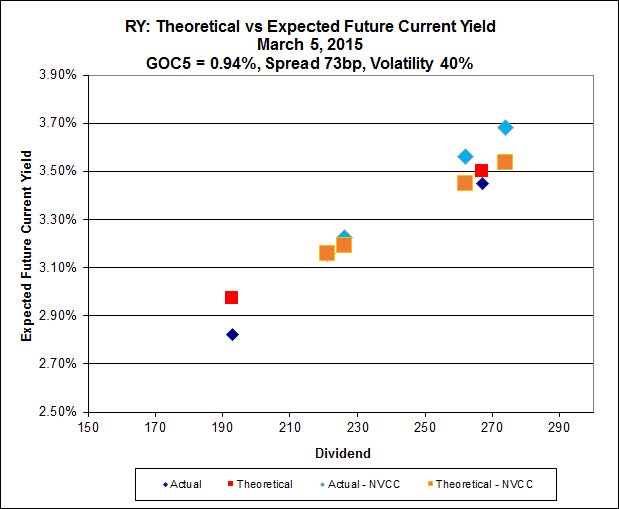

Implied Volatility theory yields the following chart:

Click for Big

Click for BigAccording to this, the new issue is $0.87 cheap, which is not as cheap as FFH.PR.I, which resets 2015-12-31 at GOC5+285bp and is currently bid at 19.01 to be $1.11 cheap.