Artis Real Estate Investment Trust has announced:

that is [sic] has entered into an agreement to sell to a syndicate of underwriters led by TD Securities Inc., RBC Capital Markets and Scotiabank (collectively the “Underwriters”), on a bought deal basis, 4,000,000 Cumulative Minimum Rate Reset Preferred Trust Units, Series I (“Series I Units”) at a price of $25.00 per Series I Unit (the “Issue Price”) for gross proceeds of $100,000,000 (the “Financing”). Artis has also granted the Underwriters an option, exercisable at any time up to 48 hours prior to the closing of the Financing, to purchase a further 1,000,000 Series I Units at the Issue Price, which, if fully exercised, would result in additional gross proceeds of $25,000,000.

The Series I Units will pay fixed cumulative preferential distributions of $1.50 per Series I Unit per annum, yielding 6.00% per annum, payable on the last day of January, April, July and October of each year, as and when declared by the board of trustees of Artis, for the initial period ending on April 30, 2023. The first quarterly distribution, if declared, will be payable on April 30, 2018 and will be $0.3750 per Series I Unit, based on the anticipated closing date of the Financing on January 31, 2018. The distribution rate will be reset on April 30, 2023 and every five years thereafter at a rate equal to the greater of (i) the sum of the then five year Government of Canada bond yield and 3.93% and (ii) 6.00%. The Series I Units are redeemable by Artis, at its option, on April 30, 2023 and on April 30 of every fifth year thereafter.

Holders of Series I Units will have the right to reclassify all or any part of their Series I Units as Cumulative Floating Rate Preferred Trust Units, Series J (the “Series J Units”), subject to certain conditions, on April 30, 2023 and on April 30 of every fifth year thereafter. Such reclassification privilege may be subject to certain tax considerations (to be disclosed in the prospectus supplement for the Financing). Holders of Series J Units will be entitled to receive a floating cumulative preferential distribution, payable on the last day of January, April, July and October of each year, as and when declared by the board of trustees of Artis, at a rate equal to the sum of the then 90-day Government of Canada Treasury Bill yield plus a spread of 3.93%.

DBRS Limited has assigned a provisional rating of Pfd-3 (low) to the Series I Units.

The Financing is being made pursuant to the REIT’s base shelf prospectus dated August 8, 2016. The terms of the offering will be described in a prospectus supplement to be filed with Canadian securities regulators. The Financing is expected to close on or about January 31, 2018 and is subject to regulatory approval.

Artis intends to use the net proceeds from the Financing to redeem its existing U.S. dollar denominated cumulative redeemable preferred trust units, Series C and for general trust purposes.

They later announced:

that as a result of strong investor demand for its previously announced offering, the underwriters have exercised their option to increase the size of the offering to 5,000,000 Cumulative Minimum Rate Reset Preferred Trust Units, Series I (“Series I Units”) to be offered on a bought deal basis to a syndicate of underwriters led by TD Securities Inc., RBC Capital Markets and Scotiabank (collectively the “Underwriters”). The Series I Units will be issued at a price of $25.00 per unit, for gross proceeds of $125,000,000 (the “Financing”).

The Financing is being made pursuant to the REIT’s base shelf prospectus dated August 8, 2016. The terms of the offering will be described in a prospectus supplement to be filed with Canadian securities regulators. The Financing is expected to close on or about January 31, 2018 and is subject to regulatory approval.

Artis intends to use the net proceeds from the Financing to redeem its existing U.S. dollar denominated cumulative redeemable preferred trust units, Series C and for general trust purposes.

The issue they intend to redeem is AX.PR.U, a FixedReset, 5.25%+446 US PAY ROC announced 2012-09-11 which commenced trading 2012-9-18, and which is callable at par on 2018-3-31.

The new issue looks quite expensive to me, according to Implied Volatility Analysis:

Click for Big

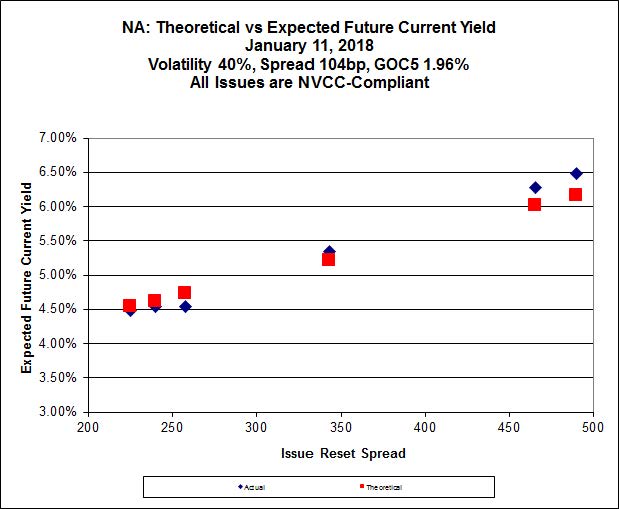

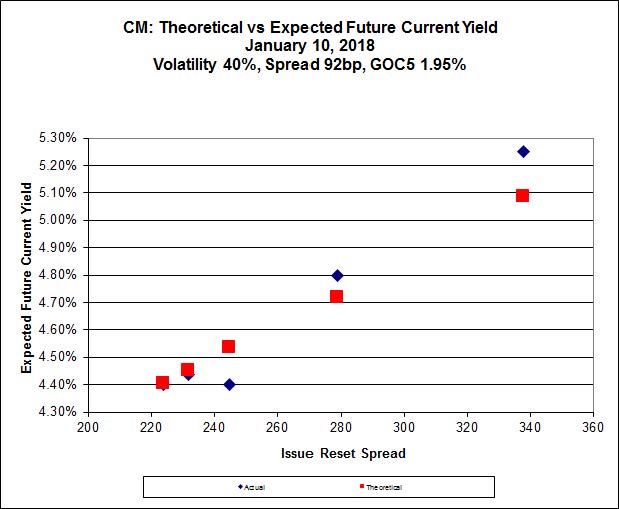

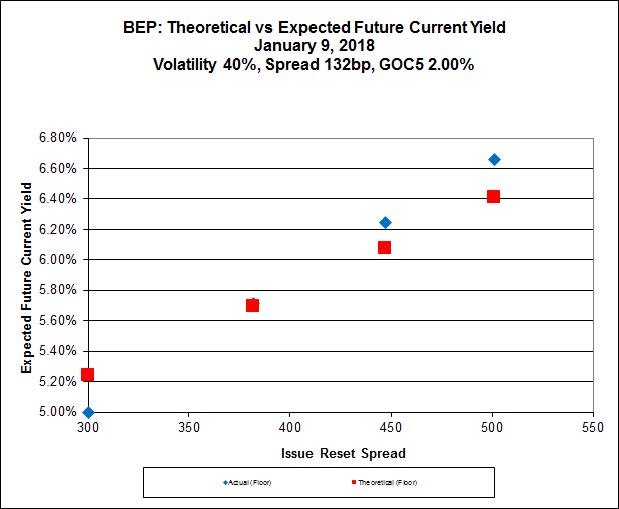

This perceived richness has a different source than the other issues discussed here recently, such as the BEP.PR.M issue, the CM.PR.S issue and the NA.PR.E, since the calculated level of Implied Volatility, 11%, is actually quite reasonable.

In this case, the richness is due to the extraordinarily high value that retail – fighting the last war, as always – has placed on the minimum reset guarantee. If, like me, you consider the guarantee to have little or no value, you will expect the new issue to be trading near the price of AX.PR.A, which has an Issue Reset Spread of 406bp (and a current coupon of 5.662%). However, this issue closed today at 23.61, indicating that retail considers the minimum rate guarantee to be worth somewhere around $1.50. Wow! That’s nearly double the value of the call option in this analysis!