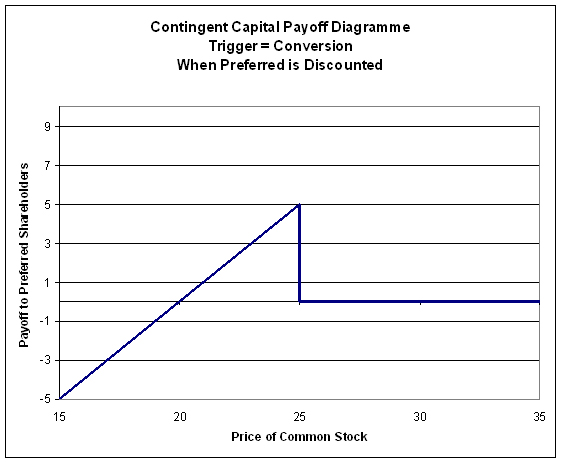

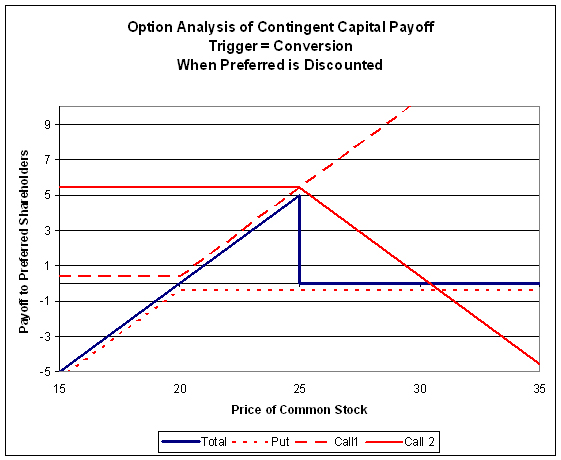

William C Dudley, President and Chief Executive Officer of the Federal Reserve Bank of New York, gave a speech at the Council of Society Business Economists Annual Dinner, London, 11 March 2010, titled The longer-term challenges ahead:

Turning to the first challenge of regulatory reform, the key issue is how to ensure that we take the right steps so that the type of financial crisis that occurred never happens again.

By me, the only way to ensure that is to reduce the earth to radioactive rubble – but maybe that’s just me.

From my perspective, I have several concerns about where the regulatory reform process is heading. First, the international consensus to harmonize standards globally appears fragile. If each country acts to strengthen its financial system in an uncoordinated way, we will be left with a balkanized system, riddled with gaps that encourage regulatory arbitrage. Second, I am concerned that the focus will be too bank-centric. Although it is clearly appropriate to strengthen the liquidity and capital standards for banks, regulatory reform needs to be comprehensive. Third, I worry that the Federal Reserve’s role with respect to bank supervision will be unduly constrained. Let me discuss each of these concerns in more detail.

Turning first to the issue of harmonization, I think it is underappreciated how important harmonization is to ensure success of the global regulatory reform effort. Without harmonized standards, financial intermediation would inevitably move toward geographies and activities where the standards are more lax. This, in turn, would provoke complaints from those who cannot make such adjustments as easily. The political process, in turn, would be sensitive to such complaints, creating pressure for liberalization, which would cause the tougher standards to unravel over time. In the discussion between countries, the emphasis would subtly shift from how to structure the regulatory regime to ensure financial stability toward negotiating a regulatory regime that works best for the institutions headquartered in each particular country.

The harmonization process has some momentum due to the sponsorship of the G-20 leadership and the efforts of the Financial Stability Board (FSB) and other international standard setters. However, the process is fragile because there are pressures to shape the standards in a way that puts the least burden on the domestic banks and financial infrastructures in one country relative to the institutions in other countries. There is understandable and genuine concern that the impact of moving to global standards will fall disproportionately on some types of firms. In my view, the way to mitigate these issues is to have a long phase-in period in the transition to the new standards rather than to soften or alter the standards to shelter those firms that happen – perhaps by historical accident – to be starting in a less advantageous position. The focus should be more on the side of all ending up in a similar place, rather than on the relative degree of difficulty in getting there.

The process is also fragile because some countries seem intent on strengthening their own set of standards before the international process has had a chance to reach consensus. Although it is understandable that countries would want to move quickly to strengthen their regulatory regimes, such actions should not be undertaken in a way that is immutable and unresponsive to the emerging international consensus.

At the end of the day, to achieve harmonized standards, each sovereign nation is going to have to bend a little bit from what it believes is best for its financial system viewed in isolation. This is necessary, of course, because a series of regulatory regimes that appear best for each individual country would likely be distinctly second-best or even worse when considered collectively. The recent crisis underscores the fact that the regulatory regime needs to be harmonized and global in nature.

These concerns echo remarks made by RBC CEO Gord Nixon at his annual meeting, reported on PrefBlog on March 3.

He is alive to the idea that over-regulating banks will lead to activities being performed by non-banks, but his answer to that is simply to regulate everything. Rather than setting ourselves the goal of eliminating financial crises – which leads to the regulation of everything and ultimately won’t work – I suggest that we define, in a clear an orderly way, just what it is that we want to protect. The payments system, definitely. But what else?

For example, he over-reaches when discussing OTC derivatives:

OTC derivatives dealers have natural incentives to favor opaque, decentralized markets that preserve their information advantage relative to other participants. The greater profit margins that derive from this advantage create incentives to favor more bespoke OTC derivatives over more standardized OTC instruments. Making more and better pricing information available to a wider range of market participants will increase competition and lessen the profit incentives that stem primarily from the opacity of these instruments and markets. Improving transparency should make the benefits that stem from standardization such as increased liquidity, reduced transaction costs, and lower counterparty risks more dominant, helping push the evolution of the OTC derivatives market in the direction of greater standardization and homogeneity.

This doesn’t mean that bespoke products will vanish. They will continue to exist. But they will exist primarily because they better serve the needs of the OTC derivatives customer, not because they create an informational asymmetry that allows rents to accrue to the securities dealer.

I suggest it’s up to the customer to decide what he wants and what’s good. Anybody who buys some of the crap developed by the dealers – FX options masquerading as bonds, for one; stock index linked GICs, for another – deserves to have their heads handed to them and the sooner the better.

If regulators had ready access to current OTC derivatives transaction information in trade repositories, I suspect that this would serve as a brake on the use of OTC derivatives that are used for more questionable purposes. For example, this includes trades undertaken to evade accounting rules or to circumvent investment charter limitations.

Is it really the role of Big Brother to monitor and enforce investment charter limitations?

{kind=link}