Forget about ambiguity. The October jobs report left little doubt the U.S. labor market is back with a vengeance after a two-month lull.

The 271,000 gain in payrolls was the biggest this year and exceeded all estimates in a Bloomberg survey of economists, a Labor Department report showed Friday. The jobless rate fell to a seven-year low of 5 percent and average hourly earnings over the past 12 months climbed by the most since 2009.

…

Investors have raised to about 70 percent the probability of a rate increase by policy makers’ December meeting, according to pricing in the federal funds futures market. That compares to 56 percent on Thursday, and assumes the effective funds rate averages 0.375 percent after liftoff.The report also showed diminishing labor-market slack. The number of Americans working part-time because of a weak economy fell to 5.7 million in October, the lowest since June 2008.

There were even some private sector jobs in Canada!

Canada added 44,000 jobs in October, a gain that blew past expectations but was likely due to temporary hiring for the federal election.

The bulk of the new jobs were in the public administration sector and coincided with the last two weeks before the election in mid-October that saw the Liberals sweep to power.

…

The country lost 9,000 construction jobs and the resources sector continued to shrink, shedding another 8,000 jobs last month, according to the government’s latest labour report.Alberta shouldered a big chunk of the losses, shedding 11,000 jobs in October.

…

Meanwhile, Ontario and British Columbia each added more than 20,000 jobs.

… so treasuries took a hit:

Yields on 10-year U.S. Treasuries surged 10 basis points to 2.33 percent, following a four-day increase as bets on a Fed move next month crept up. The rate on the more policy-sensitive 2-year note jumped six basis points to 0.89 percent.

The yield on the Bloomberg U.S. Treasury Bond Index climbed to 1.64 percent Thursday, the highest level since July 13. The gauge headed for a third weekly loss, with the decline totaling 1.2 percent.

There’s an interesting New York Fed piece on the Differences in Rent Inflation by Cost of Housing:

In this post, which is based upon our updated staff report on “The Measurement of Rent Inflation,” we present evidence that price changes for rent, which comprises a large share of consumer spending, can vary considerably across households. In particular, we show that rent inflation is consistently higher for lower-cost housing units than it is for higher-cost units. Note that since owners’ equivalent rent inflation is estimated from observed changes in rent of rental units, this finding applies to homeowners as well. While we cannot be certain about why this is the case, it appears to be at least partly related to how additional units are supplied to the housing market: in higher-price segments additional units primarily come from new construction, while most of the increase in lower-price segments comes from units that previously were occupied by higher-income households.

…

Putting these various threads together, it appears that the inverse relationship between prior rent levels and rent inflation may be related to a greater concentration of new residential construction in the higher rent level segments of the housing market, dampening the price response to a tightening in that market. As one moves down the rent level distribution, increases in the supply of housing increasingly come from previously higher-rent units, which may still have rents above the average of the incumbent units, pushing up rents more in such segments.One interesting question is how various public policies designed to influence the level of housing costs affect the growth of that cost over time. We hope to explore this issue in future work.

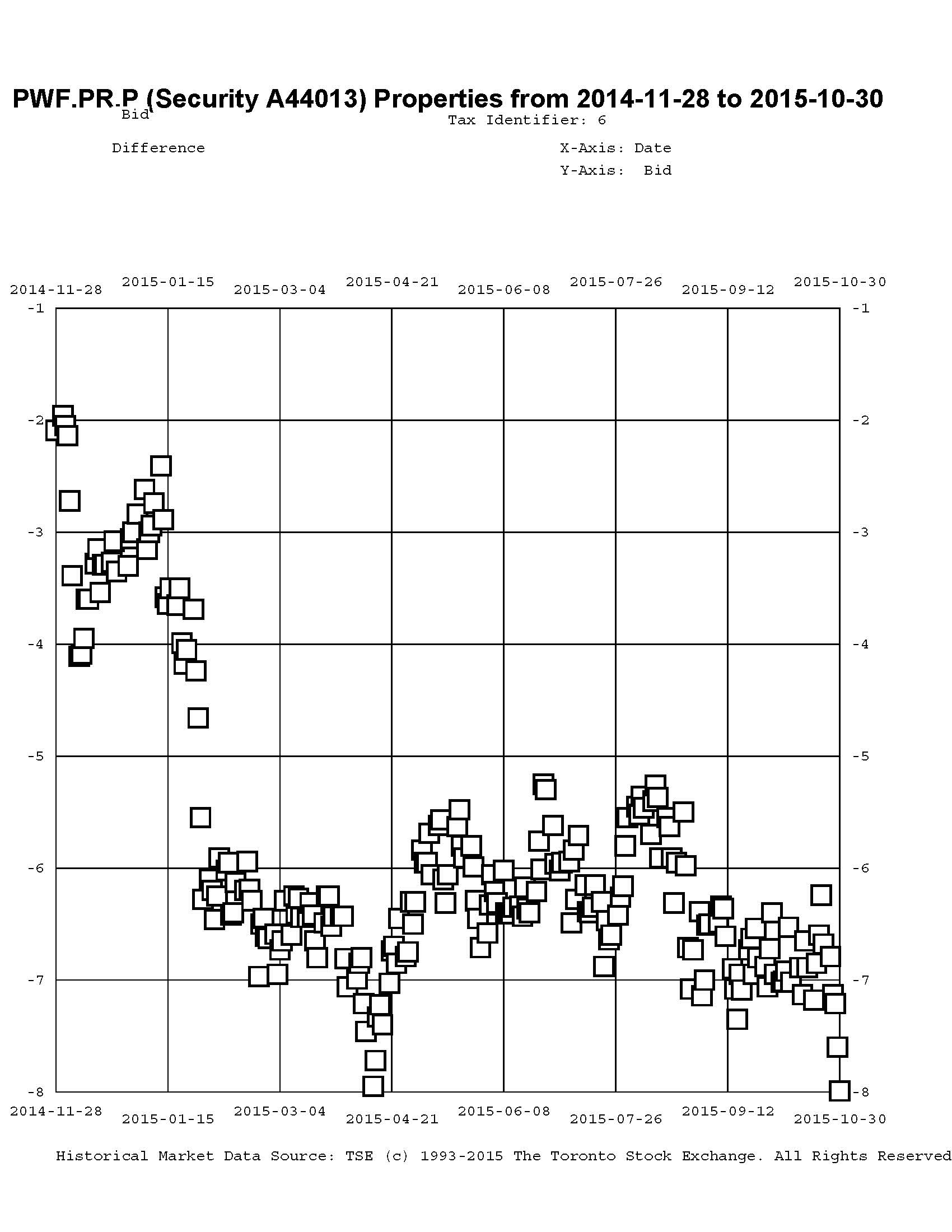

Canadian preferred share investors are making new plans for the Christmas holidays!

Click for Big

The TXPL total return index has now recovered to its late July levels, meaning that the horror of August, September and early October has been reversed. There were a few days in August in which the TXPR total return index was higher than it is today, but the broad market is also quite close to extinguishing the past three months odd. Mind you, the five year Canada is back to where it was in early June (also early May and early January, for that matter) so the preferred share market is either lagging behind its driver, or the relationship has changed, or something else.

It was a superb day for the Canadian preferred share market, with PerpetualDiscounts up 39bp, FixedResets winning an awesome 227bp and DeemedRetractibles gaining 17bp. The Performance Highlights table is, of course, ridiculously long and contains no losers at all. Volume was very extremely awfully high.

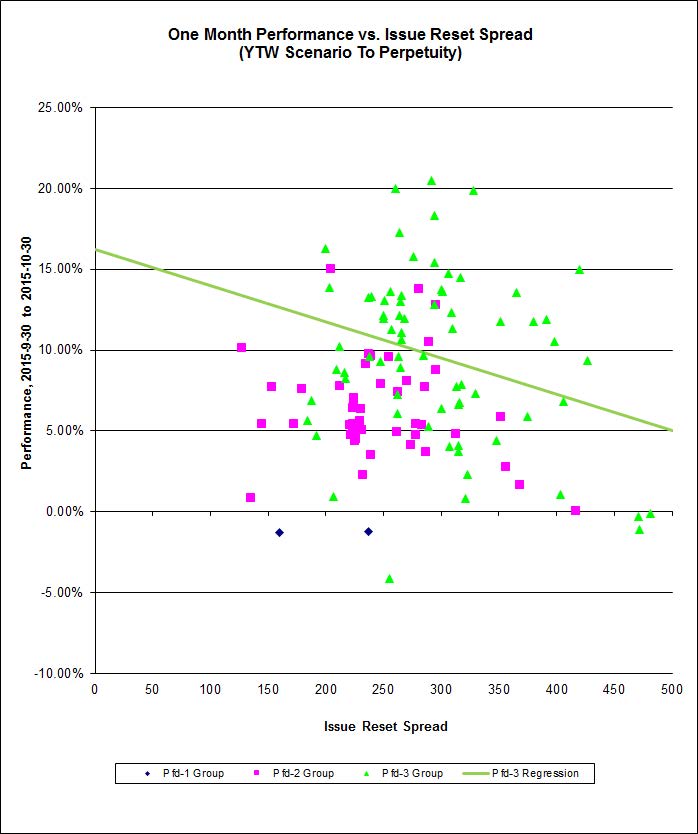

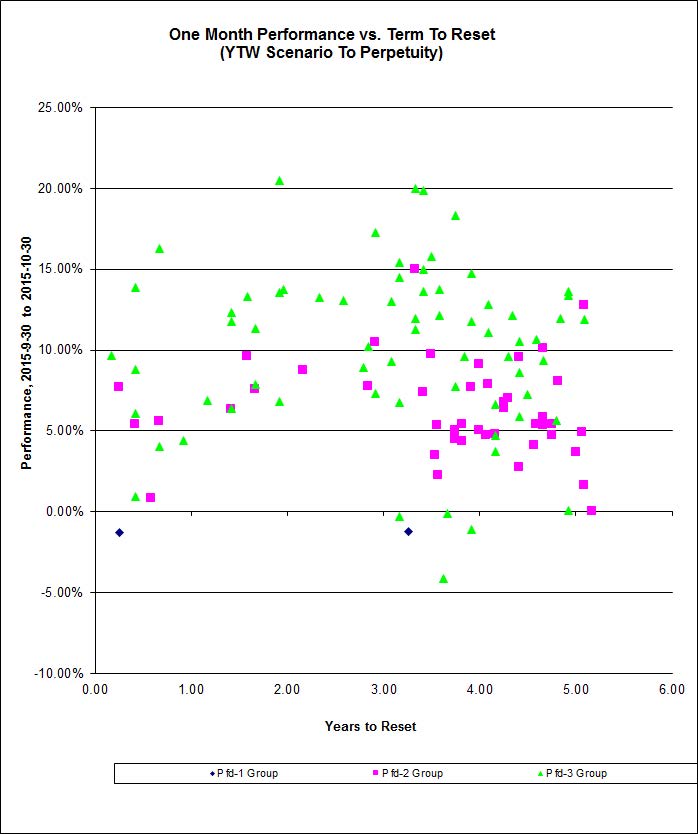

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

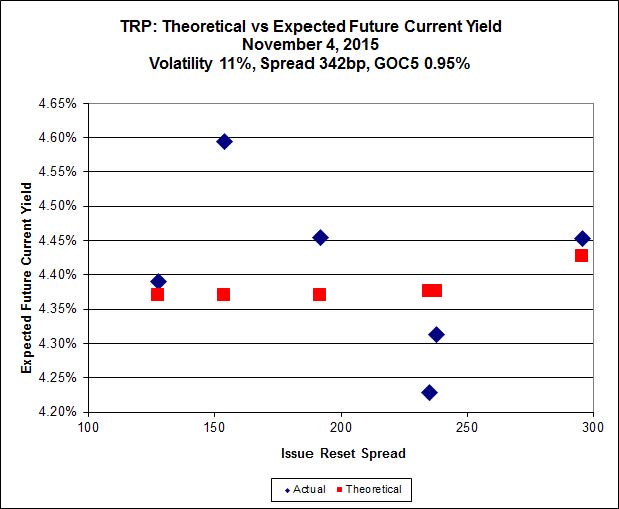

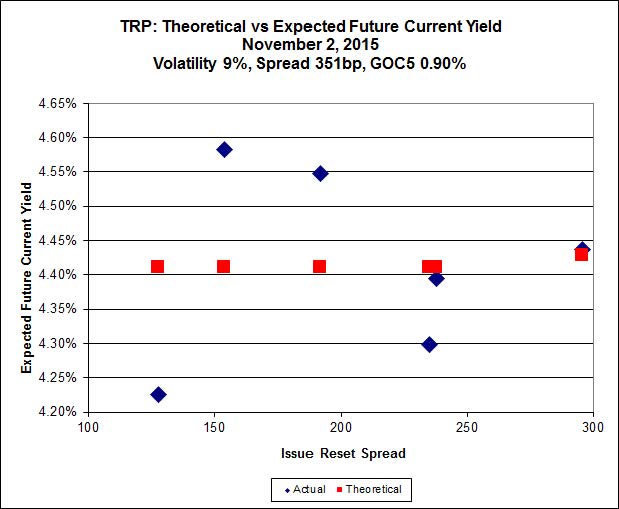

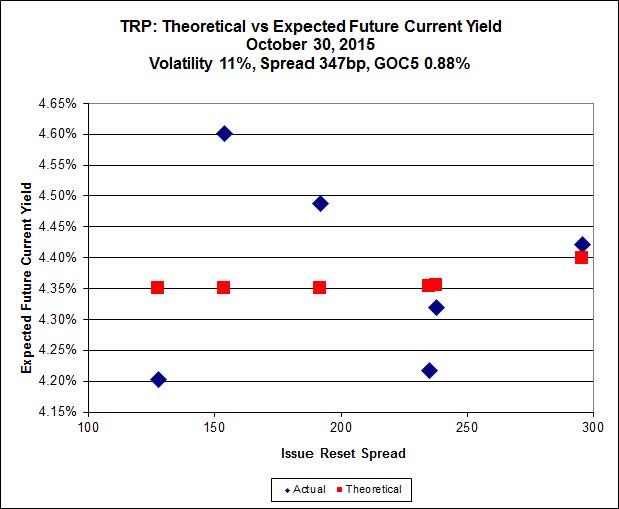

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 20.01 to be $0.45 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.51 cheap at its bid price of 14.50.

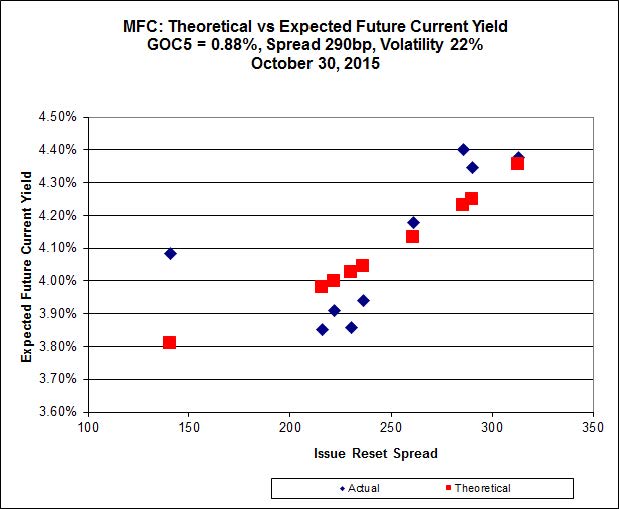

Click for Big

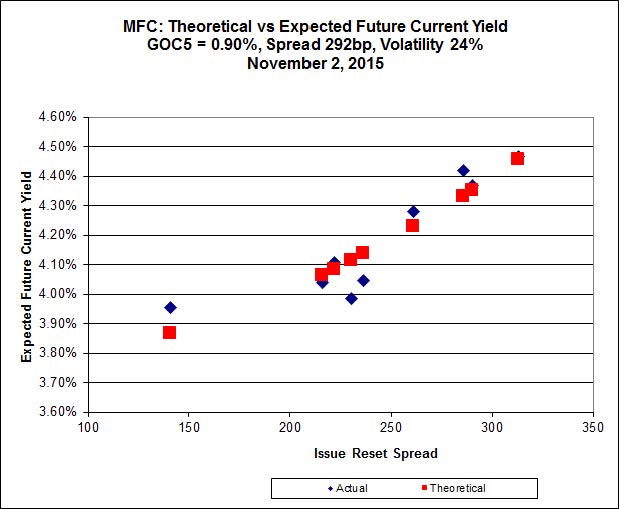

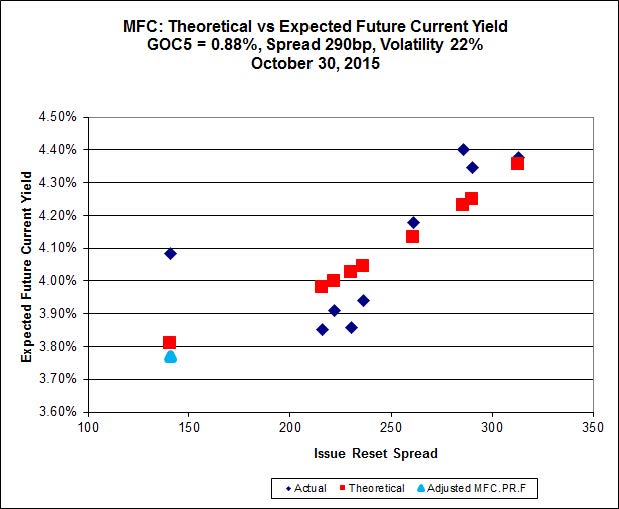

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 21.70 to be 0.84 rich, while MFC.PR.J resetting at +261bp on 2018-3-19, is bid at 21.60 to be 0.68 cheap.

Click for Big

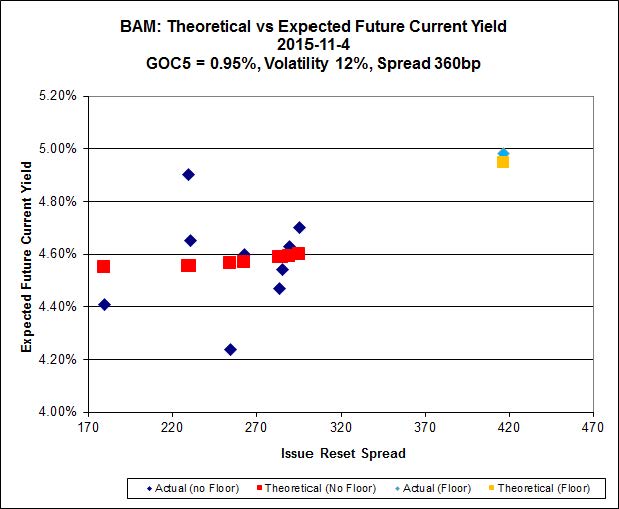

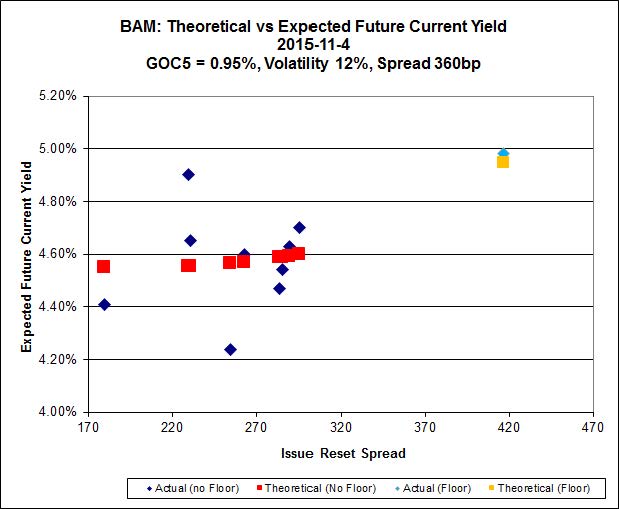

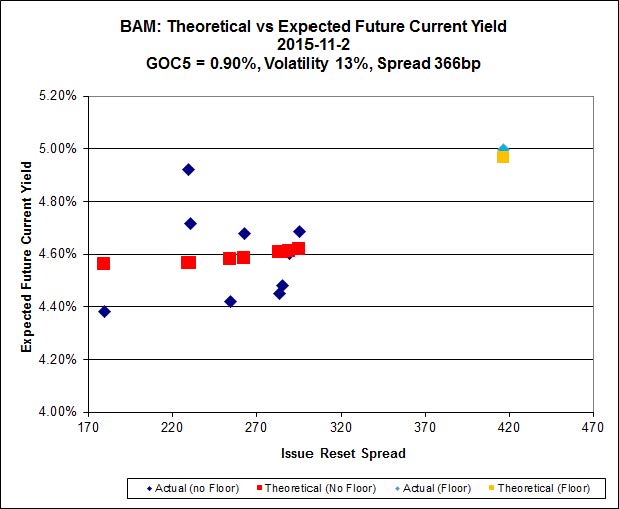

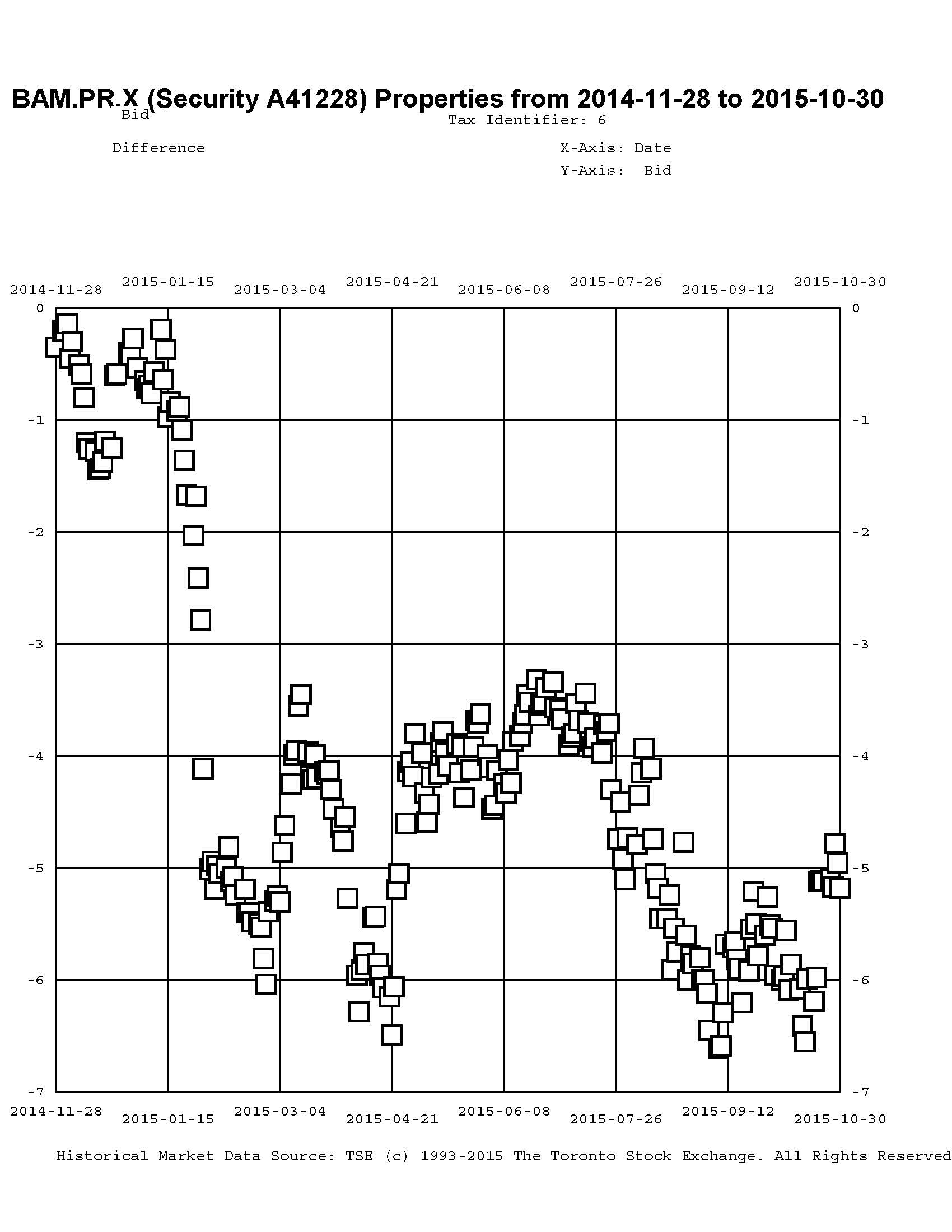

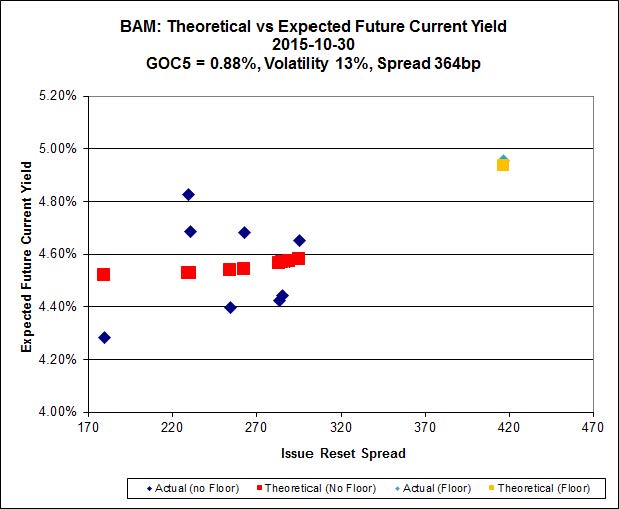

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 17.08 to be $1.57 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 21.30 and appears to be $1.30 rich.

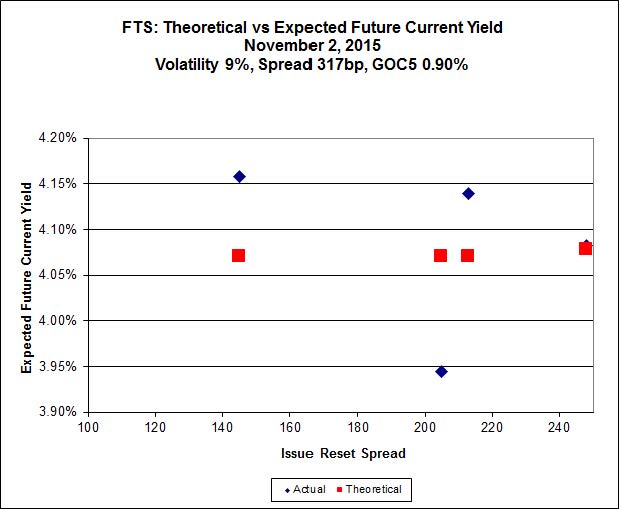

Click for Big

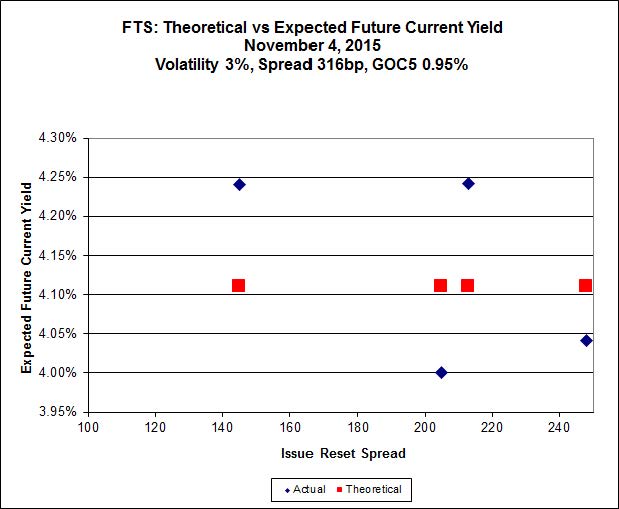

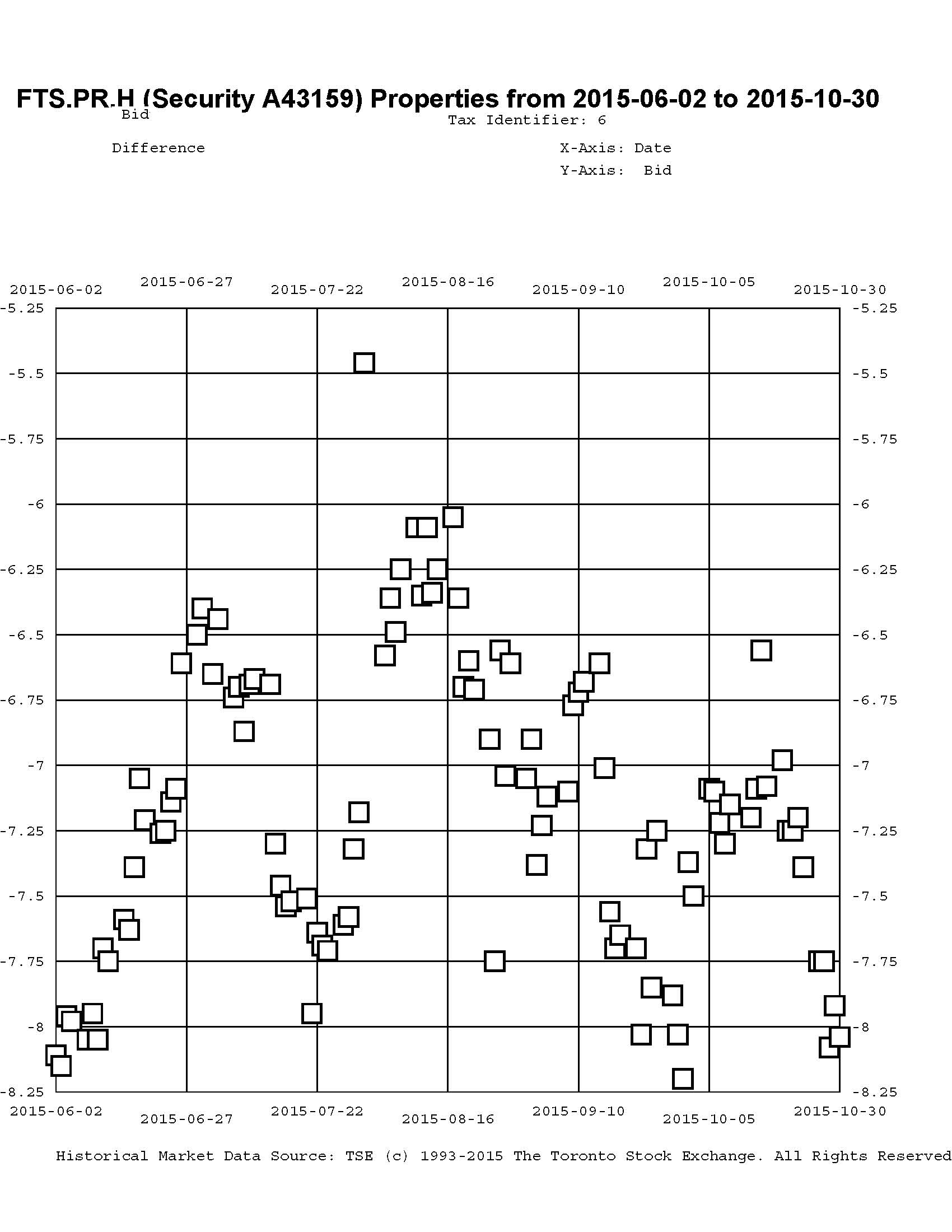

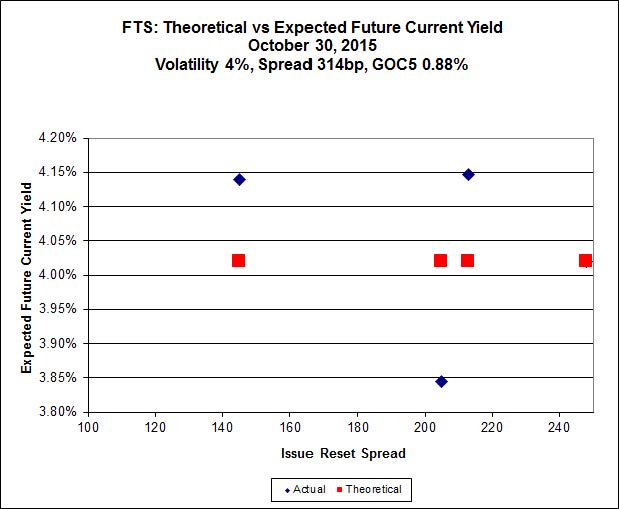

FTS.PR.K, with a spread of +205bp, and bid at 20.07, looks $0.81 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 15.02 and is $0.52 cheap.

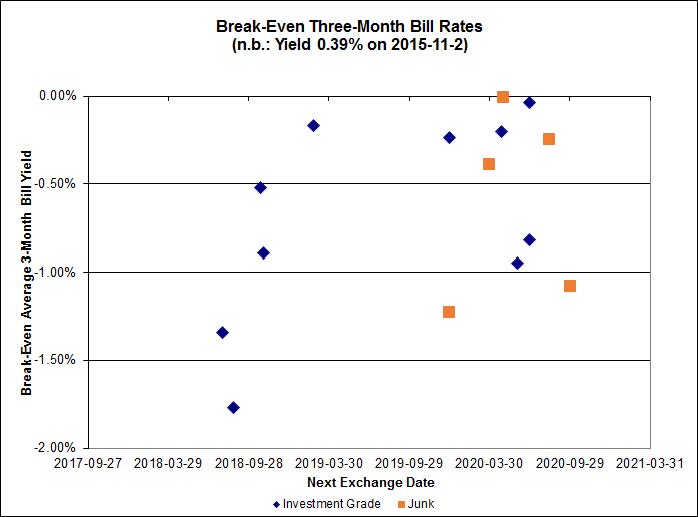

Click for Big

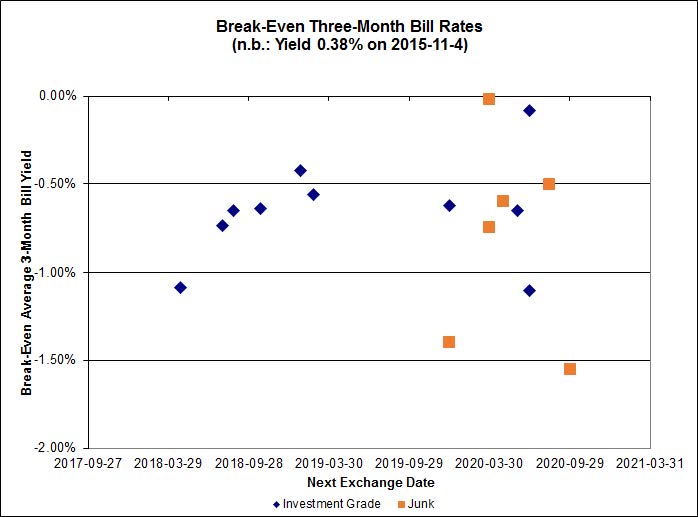

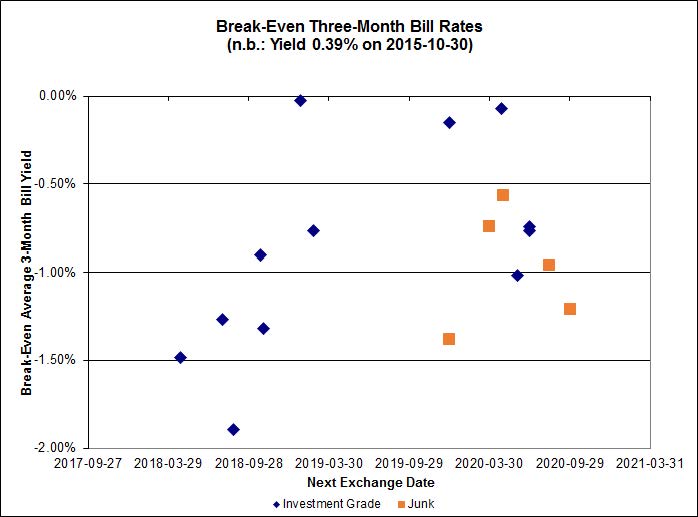

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.56%, with one outlier above 0.00%. There are two junk outliers above 0.00% and two below -2.00%.

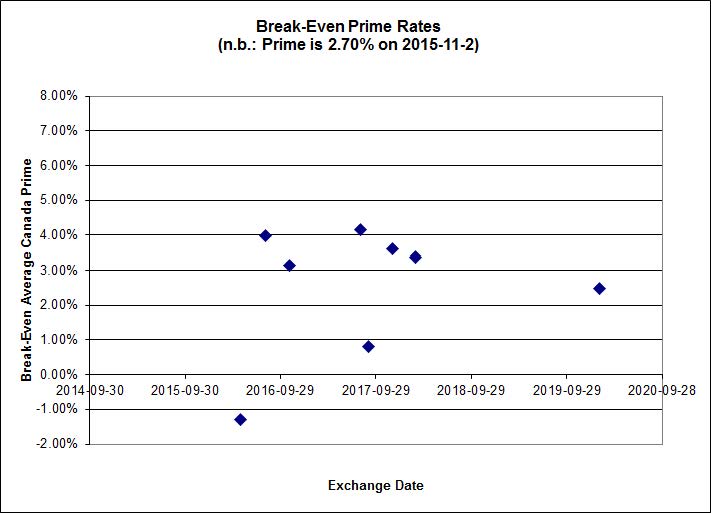

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.27 % | 5.12 % | 28,929 | 17.69 | 1 | 0.0000 % | 1,819.2 |

| FixedFloater | 5.99 % | 5.24 % | 31,249 | 17.25 | 1 | 1.8638 % | 3,256.0 |

| Floater | 4.02 % | 4.07 % | 63,387 | 17.25 | 3 | 1.7919 % | 1,962.0 |

| OpRet | 4.84 % | 4.48 % | 34,074 | 0.79 | 1 | -0.0790 % | 2,717.5 |

| SplitShare | 4.76 % | 5.76 % | 153,350 | 4.39 | 5 | -0.0246 % | 3,193.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0246 % | 2,491.5 |

| Perpetual-Premium | 5.82 % | -0.71 % | 87,549 | 0.08 | 6 | -0.1587 % | 2,497.3 |

| Perpetual-Discount | 5.51 % | 5.62 % | 83,407 | 14.47 | 33 | 0.3933 % | 2,596.9 |

| FixedReset | 4.74 % | 4.29 % | 217,266 | 15.92 | 76 | 2.2657 % | 2,156.0 |

| Deemed-Retractible | 5.16 % | 5.21 % | 110,943 | 5.42 | 34 | 0.1724 % | 2,589.4 |

| FloatingReset | 2.53 % | 3.78 % | 56,779 | 5.81 | 10 | 1.3471 % | 2,215.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TD.PR.Z | FloatingReset | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.88 Bid-YTW : 3.54 % |

| HSE.PR.G | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 22.30 Evaluated at bid price : 23.00 Bid-YTW : 4.87 % |

| MFC.PR.B | Deemed-Retractible | 1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.90 Bid-YTW : 6.59 % |

| BMO.PR.Q | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 5.31 % |

| BAM.PR.M | Perpetual-Discount | 1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.90 Evaluated at bid price : 20.90 Bid-YTW : 5.76 % |

| ELF.PR.G | Perpetual-Discount | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 5.66 % |

| CM.PR.Q | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 22.16 Evaluated at bid price : 22.77 Bid-YTW : 4.00 % |

| MFC.PR.H | FixedReset | 1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.05 Bid-YTW : 4.74 % |

| GWO.PR.G | Deemed-Retractible | 1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.86 Bid-YTW : 5.96 % |

| PWF.PR.T | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.73 Evaluated at bid price : 22.00 Bid-YTW : 3.88 % |

| BAM.PR.K | Floater | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 11.65 Evaluated at bid price : 11.65 Bid-YTW : 4.09 % |

| TRP.PR.E | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.01 Evaluated at bid price : 20.01 Bid-YTW : 4.34 % |

| BNS.PR.Y | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.78 Bid-YTW : 5.04 % |

| CU.PR.H | Perpetual-Discount | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 23.53 Evaluated at bid price : 23.85 Bid-YTW : 5.50 % |

| TD.PR.Y | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.42 Bid-YTW : 3.51 % |

| BMO.PR.R | FloatingReset | 1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.35 Bid-YTW : 3.15 % |

| BAM.PR.X | FixedReset | 1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 16.30 Evaluated at bid price : 16.30 Bid-YTW : 4.45 % |

| MFC.PR.F | FixedReset | 1.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.31 Bid-YTW : 8.75 % |

| GWO.PR.Q | Deemed-Retractible | 1.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.74 Bid-YTW : 5.98 % |

| TD.PR.T | FloatingReset | 1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.03 Bid-YTW : 3.34 % |

| FTS.PR.J | Perpetual-Discount | 1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 22.30 Evaluated at bid price : 22.70 Bid-YTW : 5.30 % |

| CU.PR.C | FixedReset | 1.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.52 Evaluated at bid price : 21.52 Bid-YTW : 3.90 % |

| BAM.PR.G | FixedFloater | 1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 25.00 Evaluated at bid price : 15.85 Bid-YTW : 5.24 % |

| BAM.PF.F | FixedReset | 1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 4.61 % |

| MFC.PR.M | FixedReset | 1.91 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.38 Bid-YTW : 5.71 % |

| BAM.PR.C | Floater | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 11.72 Evaluated at bid price : 11.72 Bid-YTW : 4.07 % |

| BAM.PR.T | FixedReset | 1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.68 % |

| VNR.PR.A | FixedReset | 2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.38 Evaluated at bid price : 21.38 Bid-YTW : 4.45 % |

| BMO.PR.W | FixedReset | 2.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 19.75 Evaluated at bid price : 19.75 Bid-YTW : 4.13 % |

| FTS.PR.M | FixedReset | 2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.30 Evaluated at bid price : 21.58 Bid-YTW : 4.14 % |

| TRP.PR.D | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 4.29 % |

| BMO.PR.M | FixedReset | 2.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.85 Bid-YTW : 3.02 % |

| BNS.PR.Z | FixedReset | 2.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.05 Bid-YTW : 5.40 % |

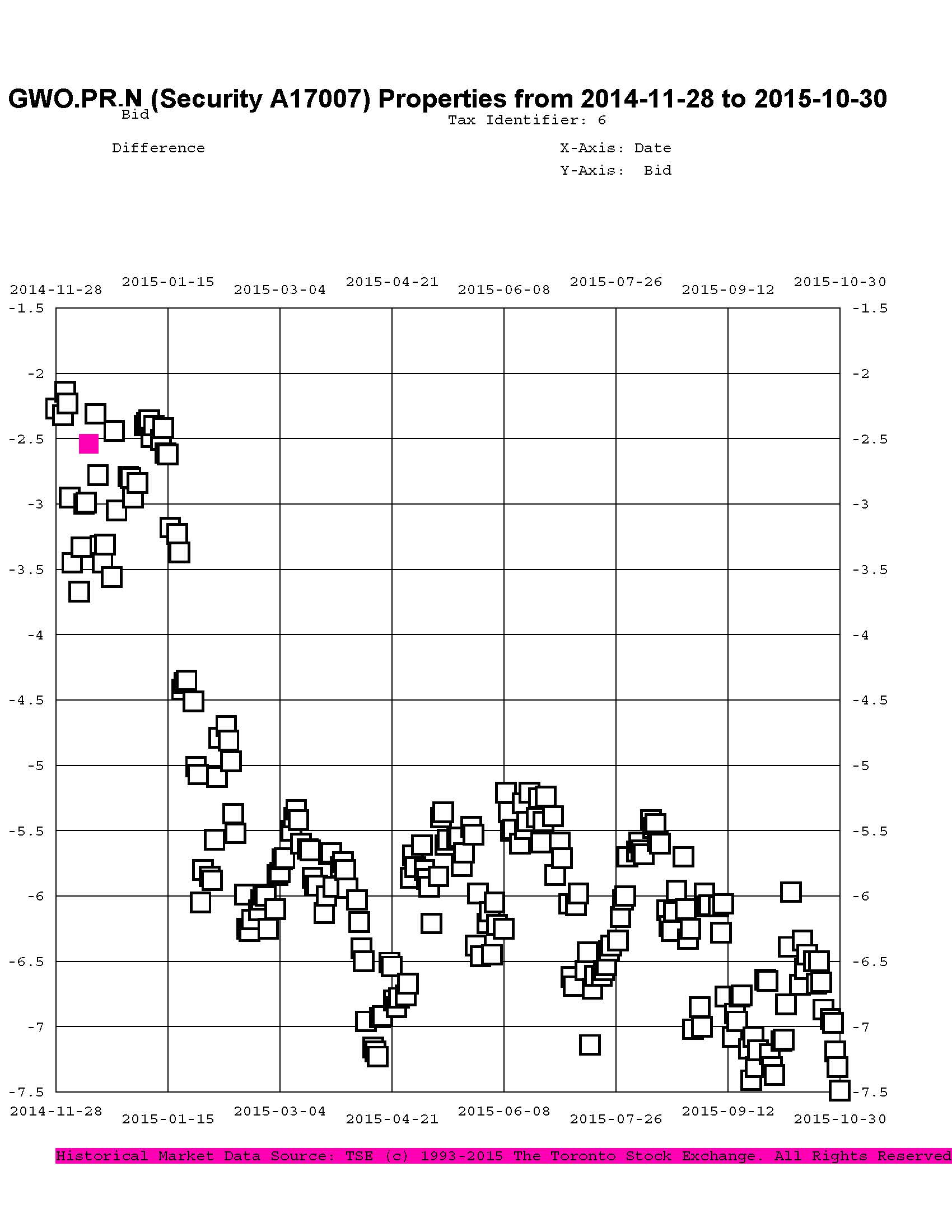

| GWO.PR.N | FixedReset | 2.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.40 Bid-YTW : 9.26 % |

| BAM.PR.B | Floater | 2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 11.85 Evaluated at bid price : 11.85 Bid-YTW : 4.02 % |

| BAM.PR.N | Perpetual-Discount | 2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.74 % |

| RY.PR.Z | FixedReset | 2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.46 Evaluated at bid price : 20.46 Bid-YTW : 4.00 % |

| TD.PF.B | FixedReset | 2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.51 Evaluated at bid price : 20.51 Bid-YTW : 4.03 % |

| RY.PR.H | FixedReset | 2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 4.05 % |

| BIP.PR.A | FixedReset | 2.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.89 Evaluated at bid price : 22.35 Bid-YTW : 5.03 % |

| BMO.PR.Y | FixedReset | 2.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 22.27 Evaluated at bid price : 22.97 Bid-YTW : 3.93 % |

| FTS.PR.F | Perpetual-Discount | 2.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 23.03 Evaluated at bid price : 23.30 Bid-YTW : 5.34 % |

| FTS.PR.K | FixedReset | 2.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.07 Evaluated at bid price : 20.07 Bid-YTW : 3.96 % |

| BAM.PF.B | FixedReset | 2.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.33 Evaluated at bid price : 20.33 Bid-YTW : 4.56 % |

| TD.PF.E | FixedReset | 2.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 22.55 Evaluated at bid price : 23.52 Bid-YTW : 3.94 % |

| BMO.PR.T | FixedReset | 2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 19.95 Evaluated at bid price : 19.95 Bid-YTW : 4.13 % |

| MFC.PR.J | FixedReset | 2.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.60 Bid-YTW : 5.66 % |

| BAM.PF.E | FixedReset | 2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 4.37 % |

| TRP.PR.A | FixedReset | 3.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 4.31 % |

| MFC.PR.K | FixedReset | 3.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.55 Bid-YTW : 5.99 % |

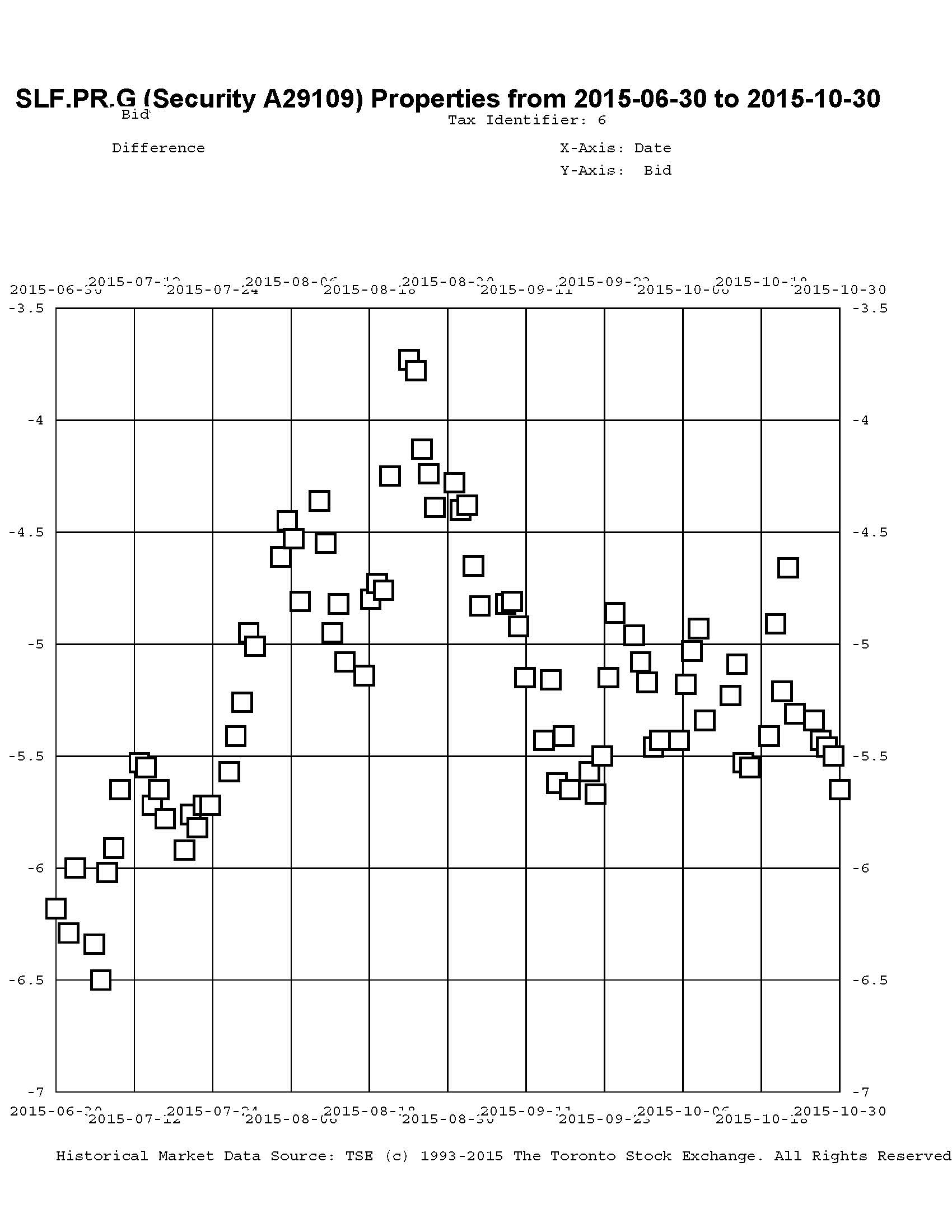

| SLF.PR.G | FixedReset | 3.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.94 Bid-YTW : 7.96 % |

| NA.PR.W | FixedReset | 3.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.26 Evaluated at bid price : 20.26 Bid-YTW : 4.10 % |

| TD.PF.A | FixedReset | 3.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.53 Evaluated at bid price : 20.53 Bid-YTW : 4.03 % |

| IFC.PR.A | FixedReset | 3.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.50 Bid-YTW : 7.82 % |

| CM.PR.P | FixedReset | 3.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.02 Evaluated at bid price : 20.02 Bid-YTW : 4.12 % |

| IAG.PR.G | FixedReset | 3.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.80 Bid-YTW : 5.15 % |

| HSE.PR.A | FixedReset | 3.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 14.67 Evaluated at bid price : 14.67 Bid-YTW : 4.64 % |

| NA.PR.S | FixedReset | 3.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.75 Evaluated at bid price : 20.75 Bid-YTW : 4.17 % |

| PWF.PR.P | FixedReset | 3.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 4.19 % |

| TD.PF.C | FixedReset | 3.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.30 Evaluated at bid price : 20.30 Bid-YTW : 4.06 % |

| CM.PR.O | FixedReset | 3.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.66 Evaluated at bid price : 20.66 Bid-YTW : 4.09 % |

| RY.PR.J | FixedReset | 3.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.93 Evaluated at bid price : 22.40 Bid-YTW : 4.02 % |

| FTS.PR.H | FixedReset | 3.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 15.02 Evaluated at bid price : 15.02 Bid-YTW : 4.03 % |

| MFC.PR.L | FixedReset | 3.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.71 Bid-YTW : 5.97 % |

| BAM.PF.G | FixedReset | 3.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.89 Evaluated at bid price : 22.35 Bid-YTW : 4.41 % |

| BAM.PF.A | FixedReset | 3.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.49 Evaluated at bid price : 21.85 Bid-YTW : 4.50 % |

| RY.PR.M | FixedReset | 3.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 21.54 Evaluated at bid price : 21.86 Bid-YTW : 4.03 % |

| FTS.PR.G | FixedReset | 4.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 19.44 Evaluated at bid price : 19.44 Bid-YTW : 4.13 % |

| MFC.PR.N | FixedReset | 4.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.70 Bid-YTW : 5.44 % |

| TRP.PR.C | FixedReset | 4.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 14.50 Evaluated at bid price : 14.50 Bid-YTW : 4.23 % |

| IFC.PR.C | FixedReset | 4.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.40 Bid-YTW : 6.38 % |

| MFC.PR.G | FixedReset | 4.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.30 Bid-YTW : 4.90 % |

| MFC.PR.I | FixedReset | 4.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.95 Bid-YTW : 5.13 % |

| SLF.PR.I | FixedReset | 4.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.04 Bid-YTW : 5.46 % |

| SLF.PR.H | FixedReset | 4.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.95 Bid-YTW : 6.81 % |

| SLF.PR.J | FloatingReset | 4.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.21 Bid-YTW : 8.74 % |

| TRP.PR.B | FixedReset | 4.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 13.56 Evaluated at bid price : 13.56 Bid-YTW : 4.05 % |

| TRP.PR.F | FloatingReset | 5.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 15.28 Evaluated at bid price : 15.28 Bid-YTW : 3.81 % |

| BAM.PR.Z | FixedReset | 6.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 22.06 Evaluated at bid price : 22.30 Bid-YTW : 4.50 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| GWO.PR.N | FixedReset | 103,089 | Desjardins crossed 19,900 at 14.45. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.40 Bid-YTW : 9.26 % |

| BMO.PR.Y | FixedReset | 54,655 | TD bought 23,200 from RBC at 23.00 and sold 10,000 to Scotia at 23.24. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 22.27 Evaluated at bid price : 22.97 Bid-YTW : 3.93 % |

| BNS.PR.Z | FixedReset | 53,664 | Nesbitt crossed 41,600 at 21.05. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.05 Bid-YTW : 5.40 % |

| RY.PR.H | FixedReset | 40,462 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 4.05 % |

| MFC.PR.I | FixedReset | 35,661 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.95 Bid-YTW : 5.13 % |

| CM.PR.O | FixedReset | 33,577 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-06 Maturity Price : 20.66 Evaluated at bid price : 20.66 Bid-YTW : 4.09 % |

| There were 70 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PF.F | FixedReset | Quote: 21.50 – 23.15 Spot Rate : 1.6500 Average : 0.9374 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 21.38 – 22.50 Spot Rate : 1.1200 Average : 0.7547 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 15.31 – 16.00 Spot Rate : 0.6900 Average : 0.4621 YTW SCENARIO |

| BAM.PR.T | FixedReset | Quote: 18.00 – 18.68 Spot Rate : 0.6800 Average : 0.4932 YTW SCENARIO |

| CM.PR.Q | FixedReset | Quote: 22.77 – 23.25 Spot Rate : 0.4800 Average : 0.3074 YTW SCENARIO |

| BAM.PF.B | FixedReset | Quote: 20.33 – 20.80 Spot Rate : 0.4700 Average : 0.3116 YTW SCENARIO |