The top news of the day is the unchanged BoC overnight rate:

The Bank of Canada today announced that it is maintaining its target for the overnight rate at 1/2 per cent. The Bank Rate is correspondingly 3/4 per cent and the deposit rate is 1/4 per cent.

Inflation has evolved in line with the outlook in the Bank’s July Monetary Policy Report (MPR). Total CPI inflation remains near the bottom of the target range, reflecting year-over-year price declines for consumer energy products. Core inflation has been close to 2 per cent, with disinflationary pressures from economic slack being offset by transitory effects of the past depreciation of the Canadian dollar and some sector-specific factors. The dynamics of GDP growth in Canada outlined in July’s MPR also remain intact. The stimulative effects of previous monetary policy actions are working their way through the Canadian economy.

Canada’s resource sector continues to adjust to lower prices for oil and other commodities, with some spillover to the rest of the economy. These adjustments are complex and are expected to take considerable time. Economic activity continues to be underpinned by solid household spending and a firm recovery in the United States, with particular strength in the sectors of the U.S. economy that are important for Canadian exports.

Increasing uncertainty about growth prospects for China and other emerging-market economies, in contrast, is raising questions about the pace of the global recovery. This has contributed to heightened financial market volatility and lower commodity prices. Movements in the Canadian dollar are helping to absorb some of the impact of lower commodity prices and are facilitating the adjustments taking place in Canada’s economy. While the overall export picture is still uncertain, the latest data confirm that exchange rate-sensitive exports are regaining momentum.

Meanwhile, risks to financial stability are evolving as expected. Taking all of these developments into consideration, the Bank judges that the risks to the outlook for inflation remain within the zone for which the current stance of monetary policy is appropriate. Therefore, the target for the overnight rate remains at 1/2 per cent.

Nice piece in the NYT magazine about the state of American campuses:

As Benjamin Ginsberg details in his 2011 book, ‘‘The Fall of the Faculty: The Rise of the All-Administrative University and Why It Matters,’’ a constantly expanding layer of university administrative jobs now exists at an increasing remove from the actual academic enterprise. It’s not unheard-of for colleges now to employ more senior administrators than professors. There are, of course, essential functions that many university administrators perform, but such an imbalance is absurd — try imagining a high school with more vice principals than teachers. This legion of bureaucrats enables a world of pitiless surveillance; no segment of campus life, no matter how small, does not have some administrator who worries about it. Piece by piece, every corner of the average campus is being slowly made congruent with a single, totalizing vision. The rise of endless brushed-metal-and-glass buildings at Purdue represents the aesthetic dimension of this ideology. Bent into place by a small army of apparatchiks, the contemporary American college is slowly becoming as meticulously art-directed and branded as a J. Crew catalog. Like Niketown or Disneyworld, your average college campus now leaves the distinct impression of a one-party state.

In the interest of fairness, here’s something for people who hate drones:

A new laser weapon that can burn up targets in just a few seconds recently melted and destroyed a test drone flying over California.

Known as the Compact Laser Weapons System, the futuristic, drone-shooting weapon is a smaller, more versatile version of the High Energy Laser Mobile Demonstrator (HEL MD), a system developed by Boeing to be mounted on top of U.S. Army vehicles.

It was another good day for the Canadian preferred share market, with PerpetualDiscounts gaining 24bp, FixedResets up 26bp and DeemedRetractibles winning 27bp. The lengthy Performance Highlights table was notable for a large population of winning FixedResets, but Floaters made a triumphant appearance at the summit. Volume was very low.

PerpetualDiscounts now yield 5.52%, equivalent to 7.18% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.2%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 300bp, unchanged from the level reported September 2.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.93 to be $0.76 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $1.13 cheap at its bid price of 13.29.

Click for Big

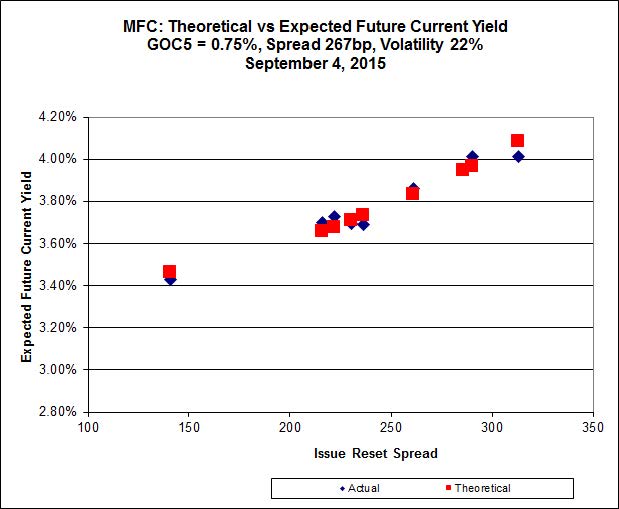

Another good fit today for MFC, with Implied Volatility rising a bit today.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 24.01 to be 0.32 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 19.92 to be 0.41 cheap.

Click for Big

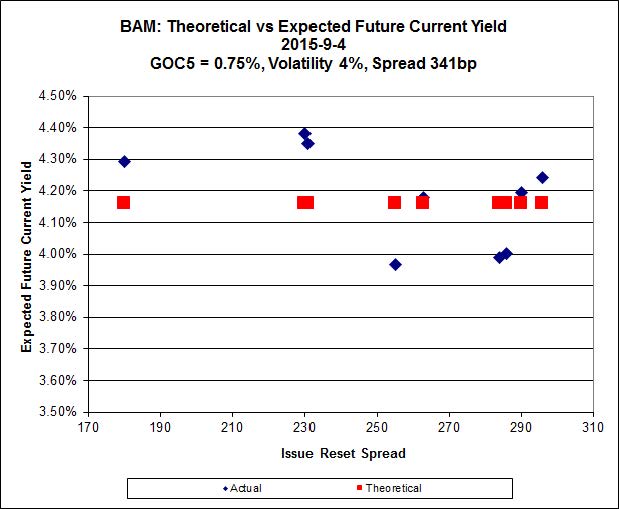

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 17.32 to be $1.10 cheap. BAM.PF.F, resetting at +286bp on 2019-9-30 is bid at 22.70 and appears to be $0.93 rich.

Click for Big

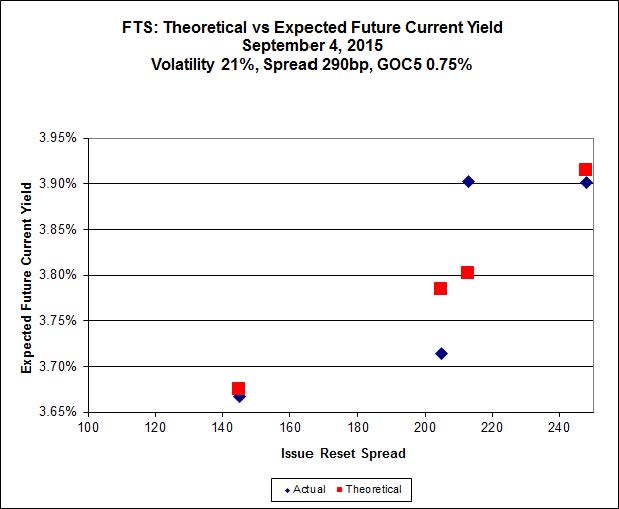

FTS.PR.K, with a spread of +205bp, and bid at 19.27, looks $0.30 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.67 and is $0.79 cheap.

Click for Big

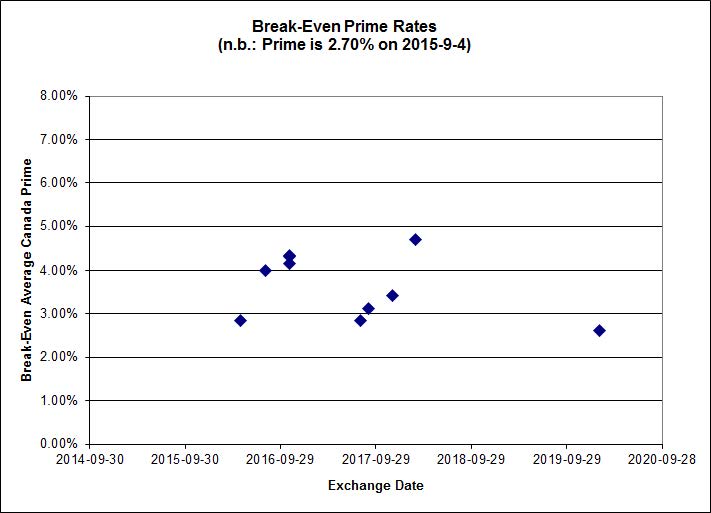

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.13%, with no outliers. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -1.29% and the unregulated issues averaging -0.91%. There are two junk outliers below -2.00% and one above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 2.6165 % | 1,664.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 2.6165 % | 2,910.5 |

| Floater | 4.41 % | 4.46 % | 58,021 | 16.40 | 3 | 2.6165 % | 1,769.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1493 % | 2,773.0 |

| SplitShare | 4.64 % | 5.03 % | 66,212 | 3.09 | 3 | 0.1493 % | 3,249.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1493 % | 2,535.7 |

| Perpetual-Premium | 5.72 % | 2.69 % | 57,783 | 0.08 | 8 | 0.0297 % | 2,489.5 |

| Perpetual-Discount | 5.42 % | 5.52 % | 72,447 | 14.60 | 30 | 0.2415 % | 2,607.2 |

| FixedReset | 4.68 % | 4.12 % | 177,218 | 15.89 | 74 | 0.2629 % | 2,172.8 |

| Deemed-Retractible | 5.14 % | 5.21 % | 97,239 | 5.50 | 33 | 0.2663 % | 2,584.9 |

| FloatingReset | 2.44 % | 3.84 % | 55,594 | 5.93 | 9 | 0.2709 % | 2,177.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BIP.PR.A | FixedReset | -2.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 21.54 Evaluated at bid price : 21.85 Bid-YTW : 5.01 % |

| SLF.PR.J | FloatingReset | -2.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.00 Bid-YTW : 8.70 % |

| BAM.PF.E | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 20.46 Evaluated at bid price : 20.46 Bid-YTW : 4.49 % |

| TRP.PR.C | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 13.29 Evaluated at bid price : 13.29 Bid-YTW : 4.48 % |

| PWF.PR.K | Perpetual-Discount | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 22.80 Evaluated at bid price : 23.08 Bid-YTW : 5.42 % |

| POW.PR.B | Perpetual-Discount | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 24.05 Evaluated at bid price : 24.30 Bid-YTW : 5.59 % |

| SLF.PR.C | Deemed-Retractible | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.29 Bid-YTW : 6.59 % |

| GWO.PR.S | Deemed-Retractible | 1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.73 Bid-YTW : 5.39 % |

| BMO.PR.Q | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.60 Bid-YTW : 4.76 % |

| BNS.PR.Y | FixedReset | 1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.45 Bid-YTW : 4.43 % |

| SLF.PR.B | Deemed-Retractible | 1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.29 Bid-YTW : 6.35 % |

| MFC.PR.J | FixedReset | 1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.81 Bid-YTW : 5.32 % |

| BAM.PR.X | FixedReset | 1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 15.06 Evaluated at bid price : 15.06 Bid-YTW : 4.72 % |

| MFC.PR.B | Deemed-Retractible | 1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 6.39 % |

| BAM.PF.A | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 21.52 Evaluated at bid price : 21.90 Bid-YTW : 4.41 % |

| TRP.PR.F | FloatingReset | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 14.85 Evaluated at bid price : 14.85 Bid-YTW : 3.81 % |

| BMO.PR.T | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 21.55 Evaluated at bid price : 21.82 Bid-YTW : 3.66 % |

| MFC.PR.F | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.25 Bid-YTW : 7.66 % |

| MFC.PR.L | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.85 Bid-YTW : 6.33 % |

| SLF.PR.A | Deemed-Retractible | 1.65 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.20 Bid-YTW : 6.35 % |

| FTS.PR.H | FixedReset | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 15.35 Evaluated at bid price : 15.35 Bid-YTW : 3.75 % |

| BNS.PR.D | FloatingReset | 1.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.35 Bid-YTW : 4.74 % |

| BAM.PR.C | Floater | 2.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 10.60 Evaluated at bid price : 10.60 Bid-YTW : 4.52 % |

| BAM.PR.B | Floater | 2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 10.82 Evaluated at bid price : 10.82 Bid-YTW : 4.43 % |

| FTS.PR.M | FixedReset | 2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 21.36 Evaluated at bid price : 21.66 Bid-YTW : 3.97 % |

| BAM.PR.K | Floater | 3.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 10.74 Evaluated at bid price : 10.74 Bid-YTW : 4.46 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PF.B | FixedReset | 129,791 | RBC sold 10,000 to Scotia at 20.30 and crossed blocks of 38,300 and 38,000 at the same price. Scotia crossed 25,000 at the same price again. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 20.32 Evaluated at bid price : 20.32 Bid-YTW : 4.48 % |

| TD.PF.F | Perpetual-Discount | 34,543 | RBC crossed 15,000 at 24.49. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 24.09 Evaluated at bid price : 24.45 Bid-YTW : 5.06 % |

| SLF.PR.J | FloatingReset | 32,490 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.00 Bid-YTW : 8.70 % |

| BMO.PR.S | FixedReset | 27,938 | Nesbitt crossed 22,600 at 22.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 21.93 Evaluated at bid price : 22.32 Bid-YTW : 3.66 % |

| BMO.PR.Z | Perpetual-Discount | 26,116 | RBC crossed 15,000 at 24.88. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-09 Maturity Price : 24.43 Evaluated at bid price : 24.82 Bid-YTW : 5.08 % |

| GWO.PR.F | Deemed-Retractible | 22,960 | Scotia crossed 20,000 at 25.21. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-10-09 Maturity Price : 25.00 Evaluated at bid price : 25.16 Bid-YTW : -5.91 % |

| There were 13 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.N | FixedReset | Quote: 20.70 – 21.45 Spot Rate : 0.7500 Average : 0.5631 YTW SCENARIO |

| MFC.PR.K | FixedReset | Quote: 19.92 – 20.41 Spot Rate : 0.4900 Average : 0.3350 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 19.93 – 20.49 Spot Rate : 0.5600 Average : 0.4057 YTW SCENARIO |

| BNS.PR.Z | FixedReset | Quote: 21.50 – 21.83 Spot Rate : 0.3300 Average : 0.2019 YTW SCENARIO |

| MFC.PR.H | FixedReset | Quote: 24.01 – 24.48 Spot Rate : 0.4700 Average : 0.3673 YTW SCENARIO |

| BMO.PR.R | FloatingReset | Quote: 22.37 – 22.70 Spot Rate : 0.3300 Average : 0.2318 YTW SCENARIO |