Nothing happened today.

It was a horrid day for the Canadian preferred share market, with PerpetualDiscounts down 56bp, FixedResets losing 71bp and DeemedRetractibles off 27bp. A very lengthy Performance Highlights table is dominated by losers. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

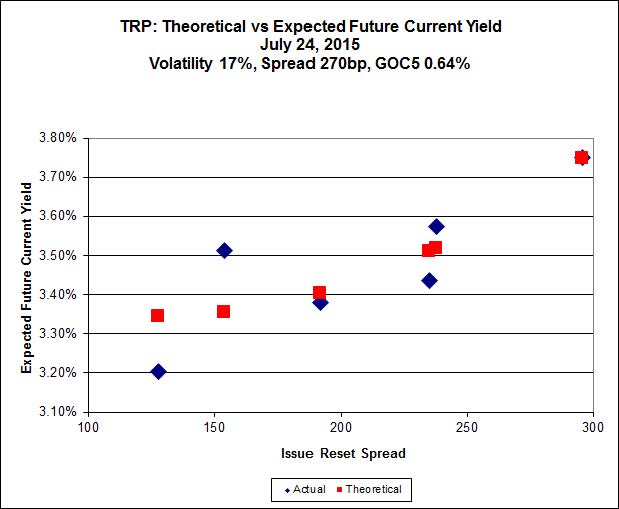

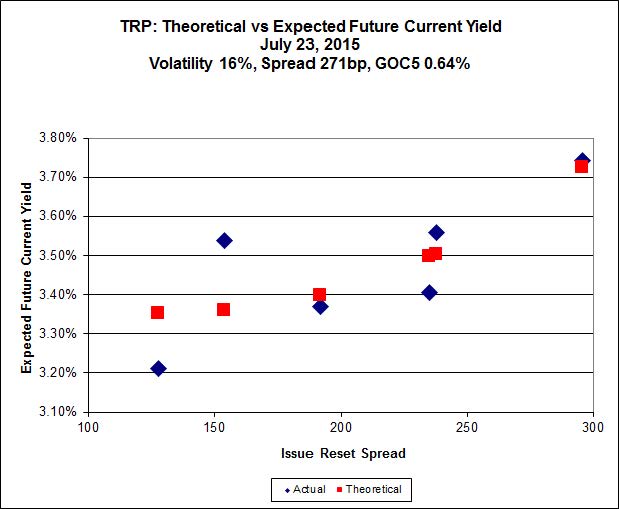

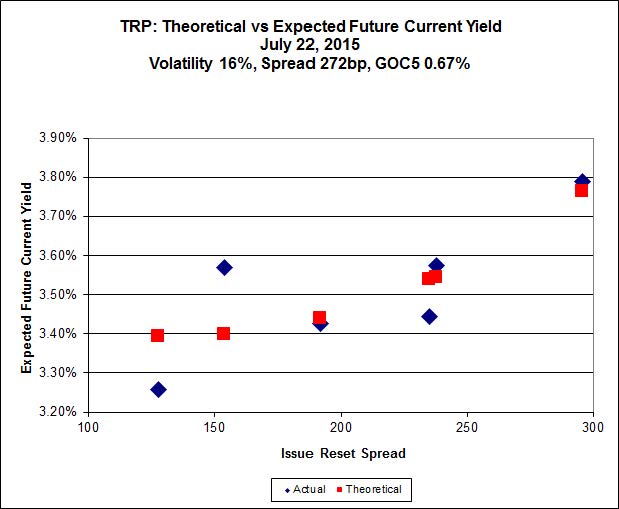

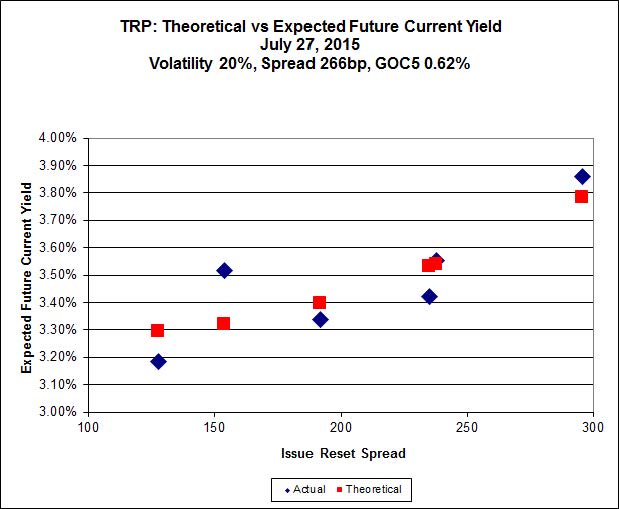

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 21.70 to be $0.67 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.93 cheap at its bid price of 15.40.

Click for Big

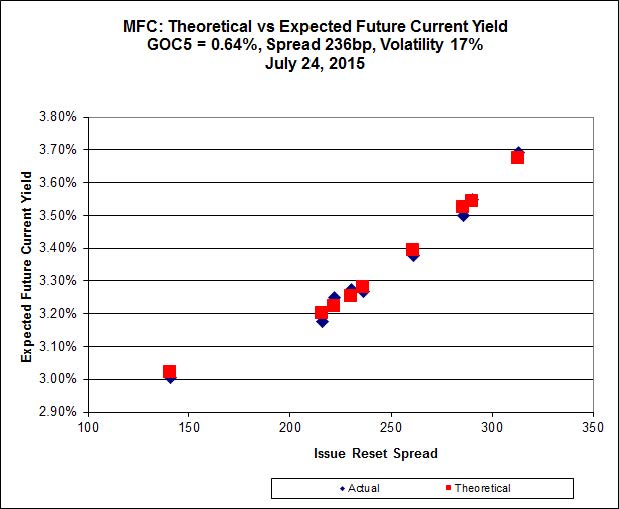

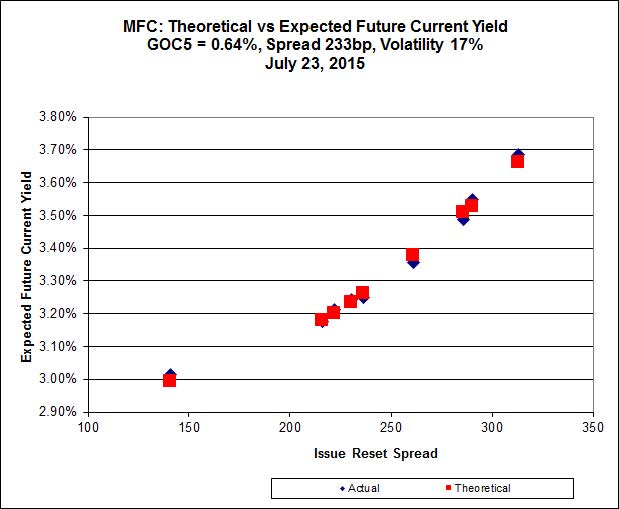

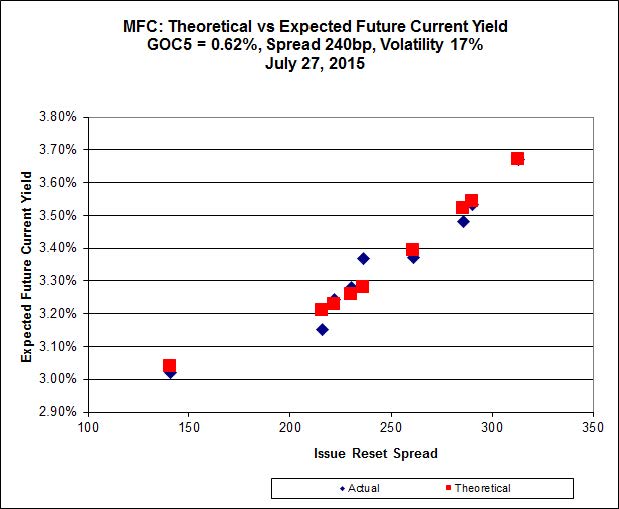

Another good fit today!

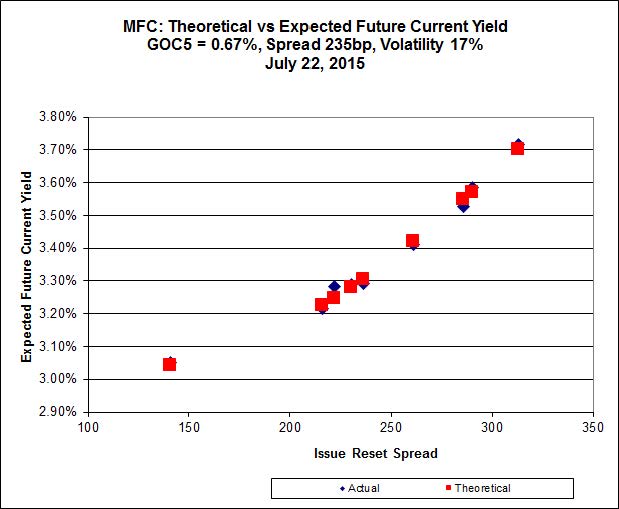

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 22.06 to be $0.40 rich, while MFC.PR.M, resetting at +236bp on 2019-12-19, is bid at 22.12 to be $0.60 cheap.

Click for Big

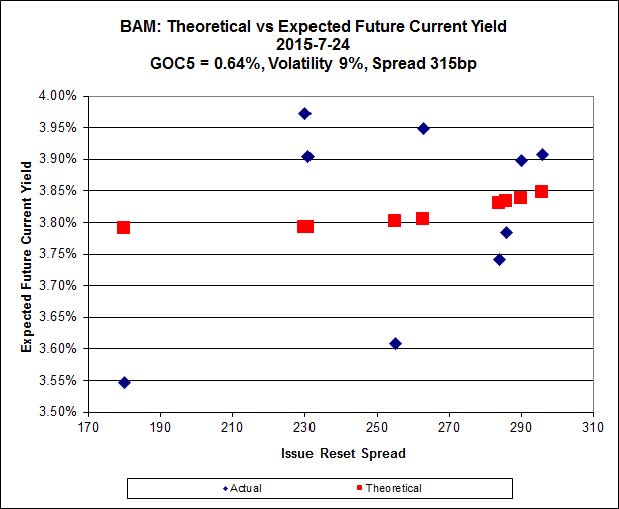

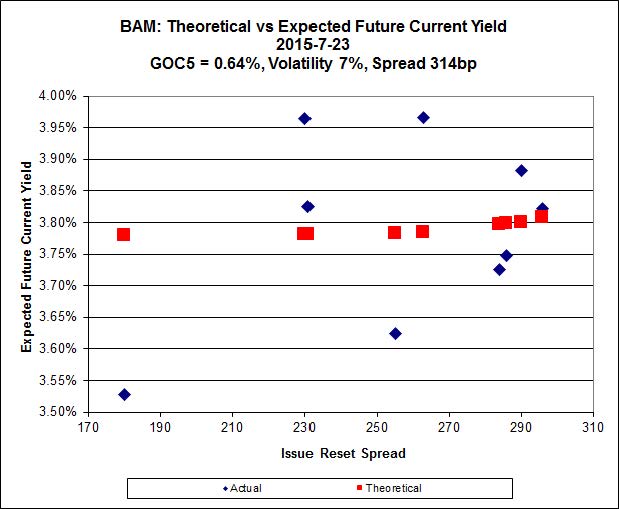

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 18.30 to be $0.86 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 22.20 and appears to be $1.42 rich.

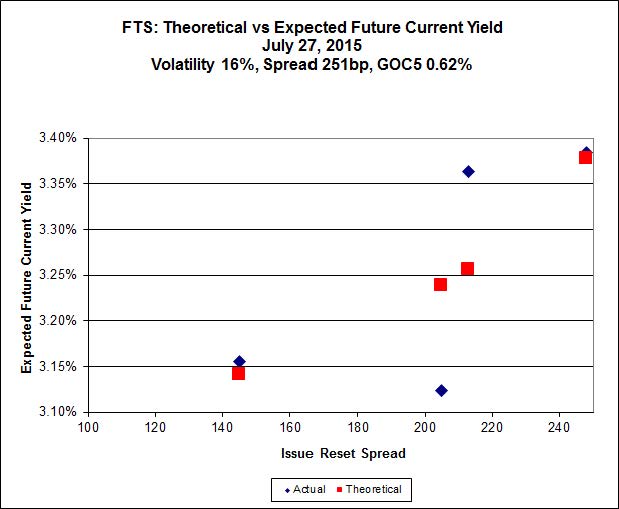

Click for Big

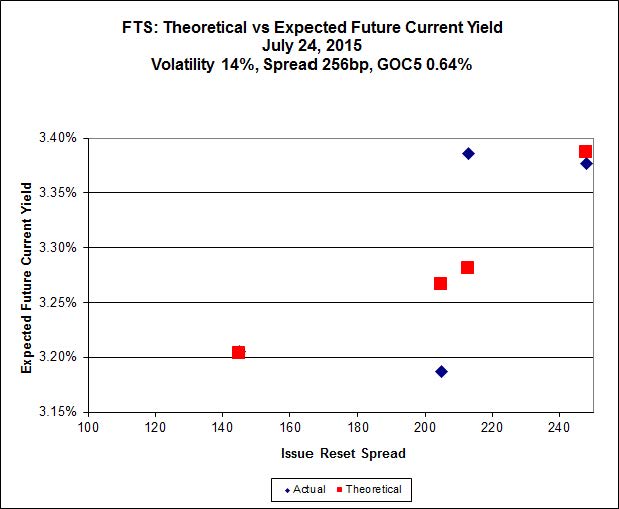

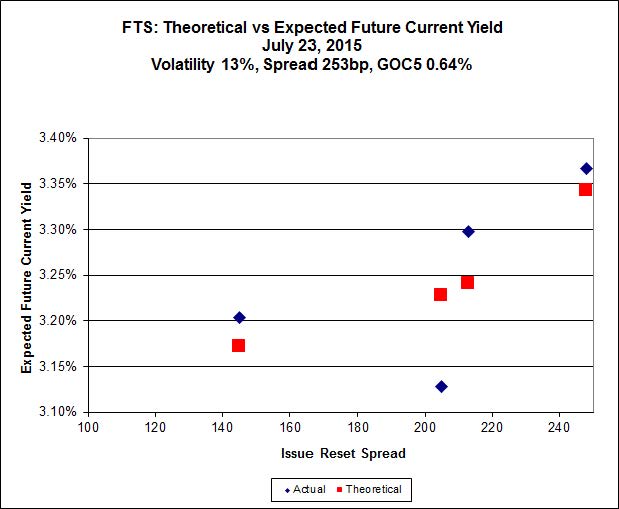

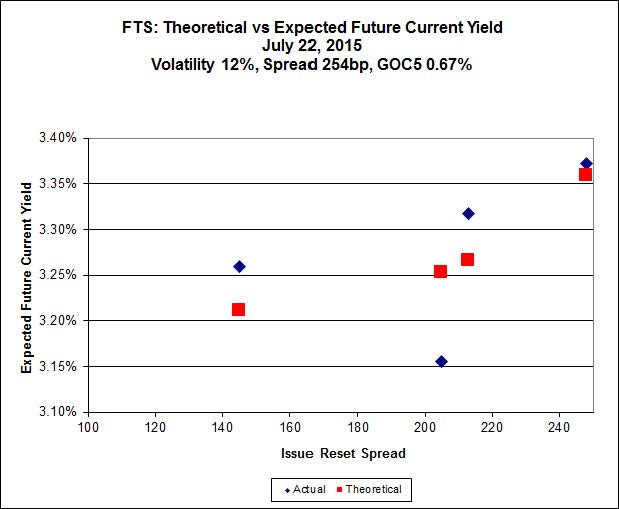

FTS.PR.K, with a spread of +205bp, and bid at 21.37, looks $0.76 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 20.44 and is $0.68 cheap.

Click for Big

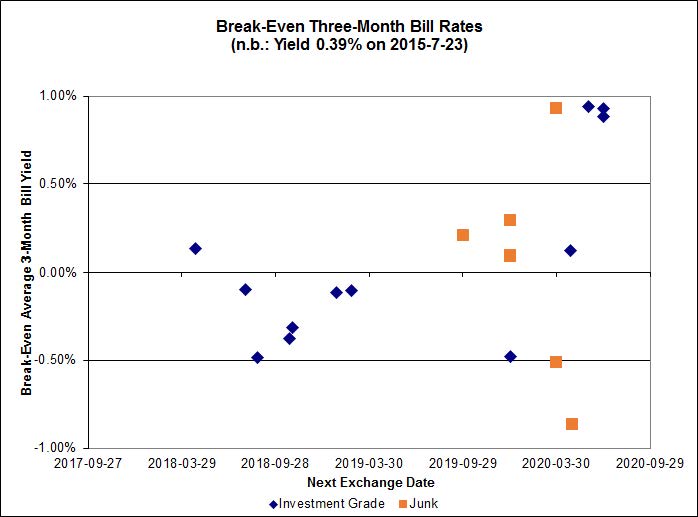

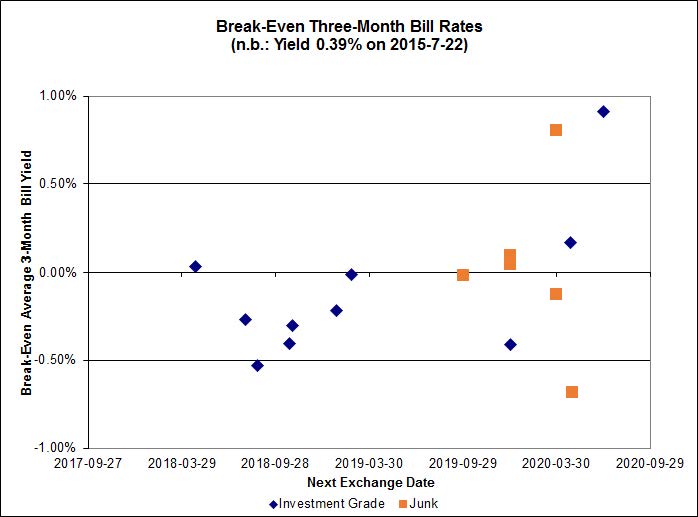

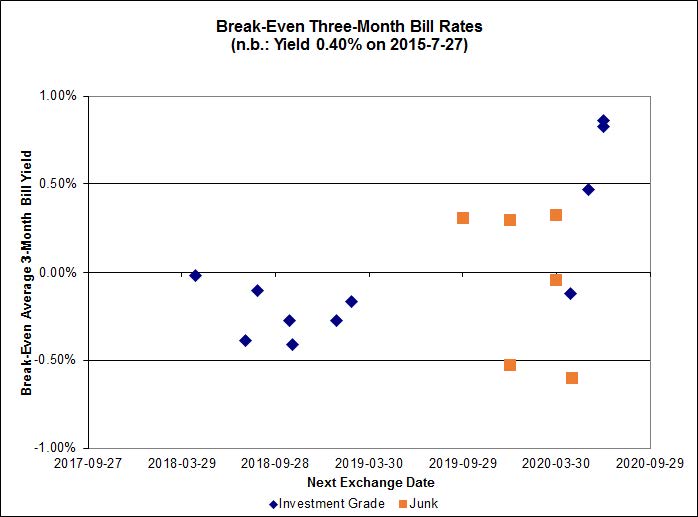

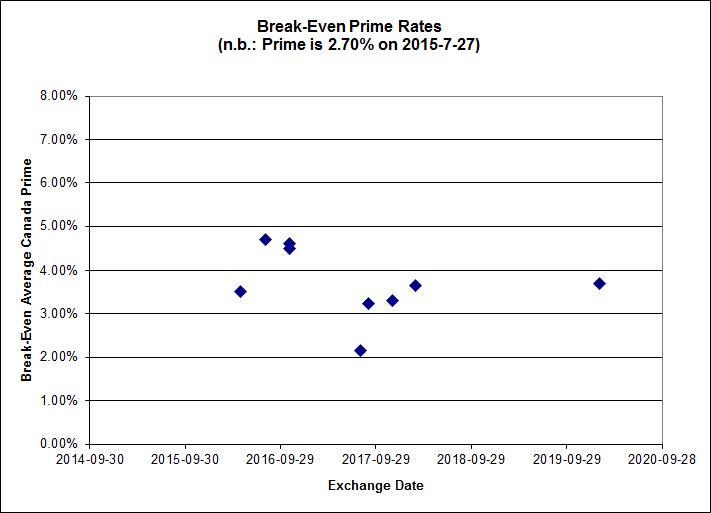

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.11%, with one outlier below -1.00% (and even then, only with the help of a dummy bid!). There are no junk outliers.

Click for Big

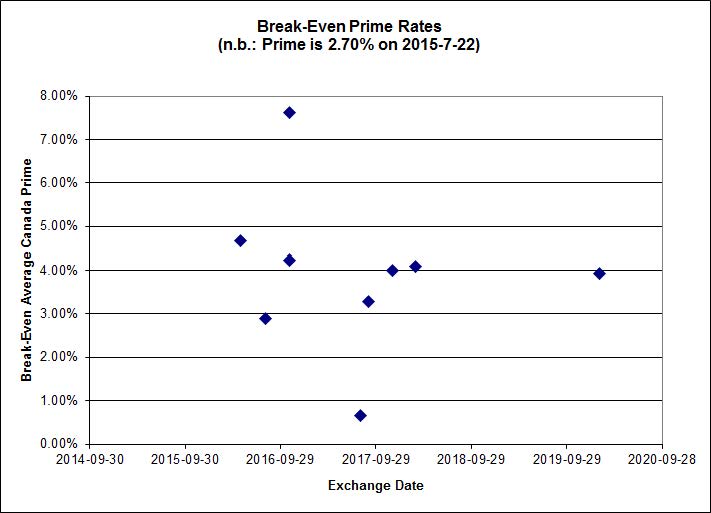

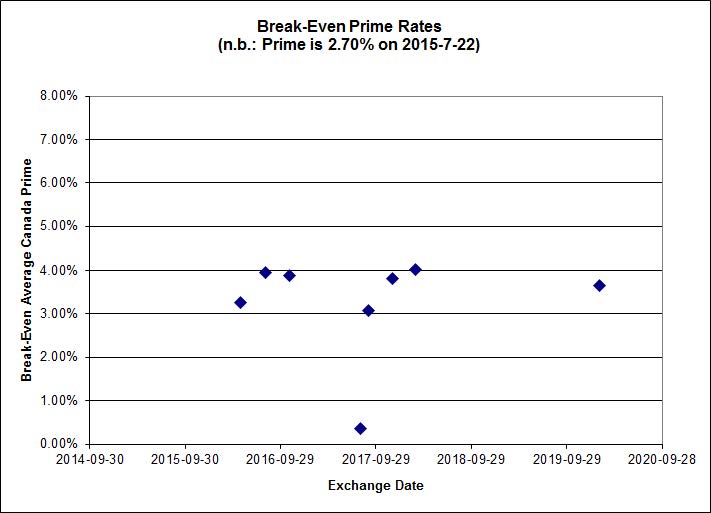

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0979 % | 2,115.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0979 % | 3,699.6 |

| Floater | 3.47 % | 3.47 % | 59,232 | 18.59 | 3 | 0.0979 % | 2,249.4 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0669 % | 2,778.1 |

| SplitShare | 4.58 % | 4.87 % | 62,717 | 3.17 | 3 | 0.0669 % | 3,255.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0669 % | 2,540.3 |

| Perpetual-Premium | 5.54 % | 5.04 % | 70,203 | 4.13 | 13 | -0.0917 % | 2,504.7 |

| Perpetual-Discount | 5.34 % | 5.33 % | 89,167 | 14.84 | 23 | -0.5602 % | 2,662.6 |

| FixedReset | 4.66 % | 3.72 % | 216,014 | 16.27 | 88 | -0.7114 % | 2,258.1 |

| Deemed-Retractible | 5.06 % | 4.98 % | 106,723 | 5.50 | 34 | -0.2719 % | 2,604.5 |

| FloatingReset | 2.40 % | 3.09 % | 43,352 | 6.05 | 10 | -0.8626 % | 2,261.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.F | FloatingReset | -5.29 % | Not real; the issue traded 10,456 shares today in a range of 16.98-10 and the Toronto Stock Exchange reports “No Bid” on their closing quotations (so I have input a dummy bid $1.00 below the ask). I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 16.11 Evaluated at bid price : 16.11 Bid-YTW : 3.63 % |

| IFC.PR.C | FixedReset | -4.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.26 Bid-YTW : 5.50 % |

| BAM.PR.X | FixedReset | -3.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 16.55 Evaluated at bid price : 16.55 Bid-YTW : 4.01 % |

| MFC.PR.M | FixedReset | -3.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.12 Bid-YTW : 5.06 % |

| TRP.PR.G | FixedReset | -3.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 22.36 Evaluated at bid price : 23.18 Bid-YTW : 3.92 % |

| IAG.PR.A | Deemed-Retractible | -2.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.41 Bid-YTW : 6.13 % |

| ENB.PF.A | FixedReset | -2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 18.55 Evaluated at bid price : 18.55 Bid-YTW : 4.86 % |

| IFC.PR.A | FixedReset | -2.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.02 Bid-YTW : 7.11 % |

| BAM.PR.C | Floater | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 13.21 Evaluated at bid price : 13.21 Bid-YTW : 3.60 % |

| NA.PR.S | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 22.36 Evaluated at bid price : 23.00 Bid-YTW : 3.44 % |

| ENB.PF.E | FixedReset | -1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 18.61 Evaluated at bid price : 18.61 Bid-YTW : 4.89 % |

| ENB.PR.J | FixedReset | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 18.19 Evaluated at bid price : 18.19 Bid-YTW : 4.80 % |

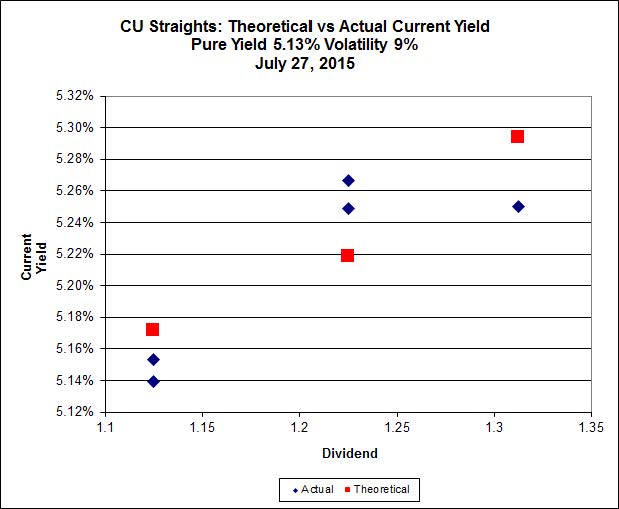

| CU.PR.G | Perpetual-Discount | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.59 Evaluated at bid price : 21.89 Bid-YTW : 5.20 % |

| BIP.PR.A | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.75 Evaluated at bid price : 22.15 Bid-YTW : 4.84 % |

| RY.PR.H | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.79 Evaluated at bid price : 22.15 Bid-YTW : 3.44 % |

| TD.PF.E | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 22.97 Evaluated at bid price : 24.51 Bid-YTW : 3.51 % |

| CU.PR.F | Perpetual-Discount | -1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.55 Evaluated at bid price : 21.83 Bid-YTW : 5.22 % |

| ENB.PR.N | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 17.65 Evaluated at bid price : 17.65 Bid-YTW : 4.91 % |

| MFC.PR.F | FixedReset | -1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.80 Bid-YTW : 7.14 % |

| TD.PF.C | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.45 Evaluated at bid price : 21.72 Bid-YTW : 3.51 % |

| BNS.PR.D | FloatingReset | -1.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.30 Bid-YTW : 3.95 % |

| BAM.PF.C | Perpetual-Discount | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.31 Evaluated at bid price : 21.31 Bid-YTW : 5.76 % |

| ENB.PF.G | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 18.76 Evaluated at bid price : 18.76 Bid-YTW : 4.89 % |

| BMO.PR.W | FixedReset | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.55 Evaluated at bid price : 21.84 Bid-YTW : 3.51 % |

| BAM.PR.T | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 18.65 Evaluated at bid price : 18.65 Bid-YTW : 4.18 % |

| POW.PR.D | Perpetual-Discount | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 23.09 Evaluated at bid price : 23.35 Bid-YTW : 5.39 % |

| ENB.PR.P | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 17.44 Evaluated at bid price : 17.44 Bid-YTW : 4.80 % |

| SLF.PR.I | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.01 Bid-YTW : 4.62 % |

| RY.PR.Z | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.87 Evaluated at bid price : 22.25 Bid-YTW : 3.38 % |

| ENB.PR.T | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 4.80 % |

| BAM.PF.A | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 22.04 Evaluated at bid price : 22.42 Bid-YTW : 4.11 % |

| TD.PF.A | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.73 Evaluated at bid price : 22.08 Bid-YTW : 3.46 % |

| SLF.PR.E | Deemed-Retractible | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.18 Bid-YTW : 6.16 % |

| PWF.PR.S | Perpetual-Discount | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 22.75 Evaluated at bid price : 23.05 Bid-YTW : 5.22 % |

| RY.PR.O | Perpetual-Discount | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 23.86 Evaluated at bid price : 24.20 Bid-YTW : 5.08 % |

| BAM.PR.R | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 4.18 % |

| SLF.PR.C | Deemed-Retractible | -1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.01 Bid-YTW : 6.21 % |

| BMO.PR.Q | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.02 Bid-YTW : 3.62 % |

| BMO.PR.M | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.90 Bid-YTW : 2.99 % |

| TRP.PR.C | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 15.35 Evaluated at bid price : 15.35 Bid-YTW : 3.60 % |

| HSE.PR.G | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 22.42 Evaluated at bid price : 23.26 Bid-YTW : 4.58 % |

| SLF.PR.H | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.50 Bid-YTW : 6.07 % |

| FTS.PR.K | FixedReset | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.37 Evaluated at bid price : 21.37 Bid-YTW : 3.44 % |

| BAM.PR.K | Floater | 1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 13.71 Evaluated at bid price : 13.71 Bid-YTW : 3.47 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| FTS.PR.H | FixedReset | 120,914 | TD crossed 110,000 at 16.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 16.40 Evaluated at bid price : 16.40 Bid-YTW : 3.35 % |

| TRP.PR.B | FixedReset | 100,361 | TD crossed 92,400 at 15.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 14.91 Evaluated at bid price : 14.91 Bid-YTW : 3.31 % |

| PWF.PR.T | FixedReset | 99,242 | RBC crossed 70,000 at 24.65; TD crossed 24,400 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 23.18 Evaluated at bid price : 24.65 Bid-YTW : 3.12 % |

| TRP.PR.D | FixedReset | 47,545 | RBC crossed 25,000 at 21.15. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 21.10 Evaluated at bid price : 21.10 Bid-YTW : 3.79 % |

| BAM.PR.Z | FixedReset | 36,803 | TD crossed 25,000 at 23.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 22.54 Evaluated at bid price : 23.05 Bid-YTW : 4.06 % |

| TD.PF.E | FixedReset | 34,679 | RBC crossed 24,900 at 24.80. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-27 Maturity Price : 22.97 Evaluated at bid price : 24.51 Bid-YTW : 3.51 % |

| There were 33 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| IFC.PR.C | FixedReset | Quote: 21.26 – 22.39 Spot Rate : 1.1300 Average : 0.6807 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 16.11 – 17.11 Spot Rate : 1.0000 Average : 0.6391 YTW SCENARIO |

| MFC.PR.M | FixedReset | Quote: 22.12 – 22.88 Spot Rate : 0.7600 Average : 0.4740 YTW SCENARIO |

| IAG.PR.A | Deemed-Retractible | Quote: 22.41 – 23.01 Spot Rate : 0.6000 Average : 0.4209 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 16.55 – 17.00 Spot Rate : 0.4500 Average : 0.2913 YTW SCENARIO |

| BAM.PF.F | FixedReset | Quote: 22.94 – 23.49 Spot Rate : 0.5500 Average : 0.3915 YTW SCENARIO |