YiLi Chien of the St. Louis Fed writes a piece titled What Drives Long-Run Economic Growth?:

It has been shown, both theoretically and empirically, that technological progress is the main driver of long-run growth. The explanation is actually quite straightforward. Holding other input factors constant, the additional output obtained when adding one extra unit input of capital or labor will eventually decline, according to the law of diminishing returns. As a result, a country cannot maintain its long-run growth by simply accumulating more capital or labor. Therefore, the driver of long-run growth has to be technological progress.

Click for Legible

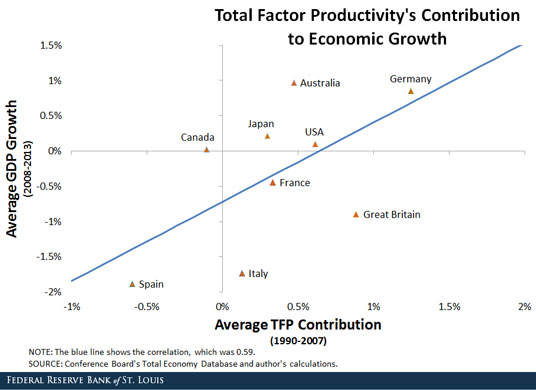

Good work by Canada, eh? We managed to beat Spain!

Nouriel Roubini, aka “Dr. Doom”, showed his total ignorance of markets:

So what accounts for the combination of macro liquidity and market illiquidity?

…

For starters, in equity markets, high-frequency traders (HFTs), who use algorithmic computer programs to follow market trends, account for a larger share of transactions. This creates, no surprise, herding behavior. Indeed, trading in the US nowadays is concentrated at the beginning and the last hour of the trading day, when HFTs are most active; for the rest of the day, markets are illiquid, with few transactions.A second cause lies in the fact that fixed-income assets – such as government, corporate, and emerging-market bonds – are not traded in more liquid exchanges, as stocks are. Instead, they are traded mostly over the counter in illiquid markets.

Third, not only is fixed income more illiquid, but now most of these instruments – which have grown enormously in number, owing to the mushrooming issuance of private and public debts before and after the financial crisis – are held in open-ended funds that allow investors to exit overnight. Imagine a bank that invests in illiquid assets but allows depositors to redeem their cash overnight: if a run on these funds occurs, the need to sell the illiquid assets can push their price very low very fast, in what is effectively a fire sale.

Fourth, before the 2008 crisis, banks were market makers in fixed-income instruments. They held large inventories of these assets, thus providing liquidity and smoothing excess price volatility. But, with new regulations punishing such trading (via higher capital charges), banks and other financial institutions have reduced their market-making activity. So, in times of surprise that move bond prices and yields, the banks are not present to act as stabilizers.

…

This is the paradoxical result of the policy response to the financial crisis. Macro liquidity is feeding booms and bubbles; but market illiquidity will eventually trigger a bust and collapse.

With respect to his second point: exchange trading harms liquidity. It’s been shown time and time again … on an exchange, you get tighter spreads, but much less depth.

With respect to his fourth point … true enough as far as it goes, but it doesn’t go very far. Banks have been willing to keep large inventories for a few days, but not for much longer than that; and even then, only when their market intelligence gives them cause to believe that it’s just a greater than usual dose of greed or fear that’s causing a transient market move. When things are wild, they increase their spreads just as much as anybody else; when something fundamental is happening, they don’t stand in the way of the freight train. Their ability to smooth out transient spikes has been impaired by post-crisis regulation; they never had any ability to do more.

My own view is that post-crisis regulation has directly harmed liquidity of corporate bonds by the restrictions on inventory; but that it is financial repression that has harmed liquidity of Treasuries. New regulation has both increased the requirement for banks to hold treasuries, while the Fed’s low policy yields have decreased the incentive for anybody else to hold them. In fact, I will suggest that there are exactly two classes of investor holding US and Canadian government debt in significant size at the moment:

- Regulated entities

- Idiots

Remember the quotation from April 20:

Moreover, Gluskin Sheff + Associates chief economist David Rosenberg pointed out in a note to clients that 80 per cent of the new Treasuries supply over the past year have been bought by foreign central banks, pension funds, insurers, banks, and insurance companies.

If you want a liquid market, the most efficacious way of getting it is to ensure that the population of potential investors is heterogeneous … as much as possible, you want to ensure that no matter what is going on in the economy or in the marketplace, there is a broad group of participants who have a good reason to sell and a broad group of participants who have a good reason to buy. Treasury and Canada markets don’t have that at the moment.

But, on cue, there is some bearish growling from Europe:

Another bond market meltdown is brewing where the initial one began in April, in signs of a reinflating European economy.

Traders piled on sell orders from Germany to Italy on Tuesday as the first increase in consumer prices in the euro zone in six months suggests growth in the 19-nation economy and the risk of the return of the main nemesis of fixed-income investors: inflation.

SEC Commissioner Michael S. Piwowar made an interesting speech titled Capital Unbound: Remarks at the Cato Summit on Financial Regulation:

Over thirty years ago, economist Bruce Yandle famously coined the term “Bootleggers and Baptists” to describe a public choice theory of economics, which observes that, for regulation to endure, groups that otherwise have opposite points of view choose a regulatory structure that results in private benefits for both but perhaps is suboptimal for society.[1] In Yandle’s illustration, Baptists support laws that shut down all bars and liquor stores on Sundays. Bootleggers are also in favor of such laws, but for entirely different reasons. If Sunday closing laws are in place, both parties get their preferred outcome, and the rules are easy to administer. But if the problem is consumption of alcohol, Sunday closing laws merely shift the production and distribution of alcohol from one group — bars and liquor stores — to bootleggers, while giving a false impression that the public interest is being served. No pun intended.

Yandle described this regulatory approach as making complete sense, when viewed from the regulator’s perspective. A regulator, Yandle reasoned, is most focused on minimizing its costs, rather than the overall costs of the regulation. One example is the regulator’s cost of enforcement. A regulator may be inclined to favor rules that minimize the number of circumstances in which a mistake can be made; for instance, unless a lawmaker confuses the day of the week, it is clear under a Sunday closing law whether a bar or liquor store is required to be closed. It is less costly for a regulator to adopt simple, across-the-board rules that are easy to monitor and enforce than alternatives that take into account economic efficiency and distributional effects — how costs and benefits are distributed among different groups. One area where we see this result is private securities offerings.

I hadn’t realized that this concept was a formal economic theory!

I want to move beyond the artificial distinction between so-called “accredited” and “non-accredited” investors and challenge the notion that non-accredited investors are “being protected” when the government prohibits them from investing in high-risk securities. Here, I appeal to two well-known concepts from the field of financial economics. The first is the risk-return tradeoff. Because most investors are risk averse, riskier securities must offer investors higher returns. This means that prohibiting non-accredited investors from investing in high-risk securities is the same thing as prohibiting them from investing in high-return securities.

The second economic concept is modern portfolio theory. By holding a diversified portfolio of assets, investors reap the benefits of diversification; that is, the risk of the portfolio as a whole is lower than the risk of any individual asset. I do not have the time today to give a full lecture on the mathematics and statistics of portfolio diversification, so I will just assure you the correlation of returns is key. When adding higher-risk, higher-return securities to an existing portfolio, as long as the returns from the new securities are not perfectly positively correlated with (move in exactly the same direction as) the existing portfolio, investors can reap higher returns with little or no change in overall portfolio risk. In fact, if the correlations are low enough, the overall portfolio risk could actually decrease.

These two concepts show how even a well-intentioned investor protection policy can ultimately harm the very investors the policy is intended to protect. Moreover, restricting the number of accredited investors in the “privileged class” can have additional (or what economists call “second-order”) effects. The accredited investors may enjoy even higher returns because the non-accredited investors are prohibited from buying and bidding up the price of, high-risk, high-return securities. Remarkably, if you think about it, by allowing only high-income and high-net-worth individuals to reap the risk and return benefits from investing in certain securities, the government may actually exacerbate wealth inequality.

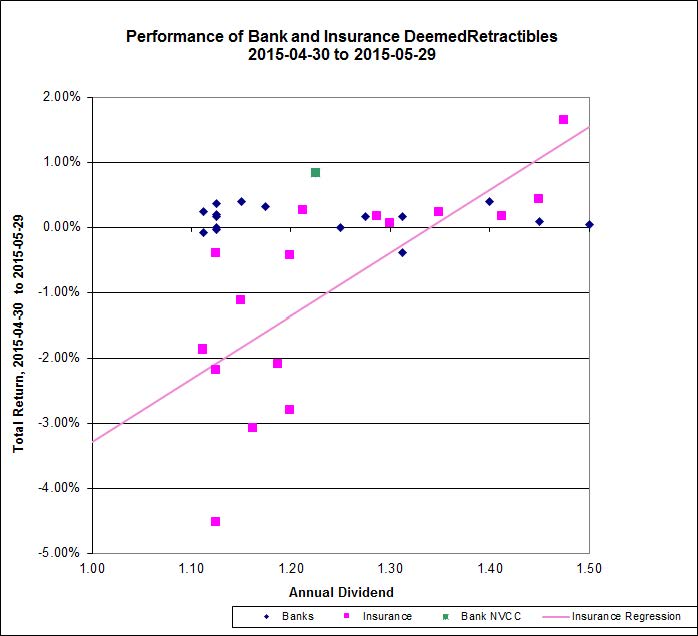

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 23bp, FixedResets off 7bp and DeemedRetractibles down 9bp. Floaters got hammered (and, unusually, featured in the Volume Highlights, suggesting that somebody really wanted out!), but otherwise the Performance Highlights table is much shorter than has been the norm for the past six months! Volume was well below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

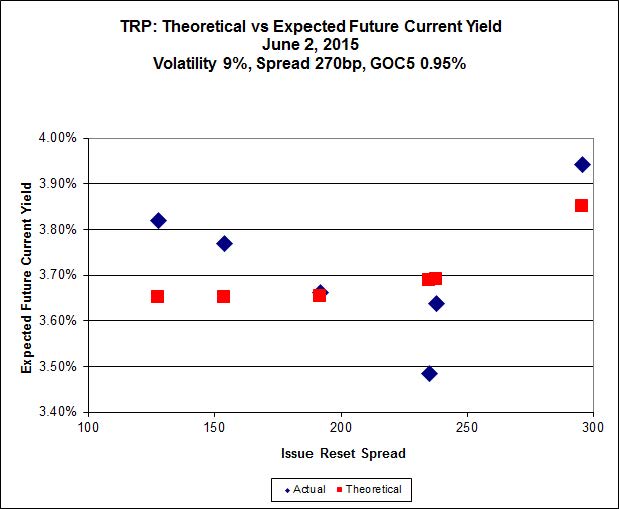

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 23.68 to be $1.30 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.59 cheap at its bid price of 24.80.

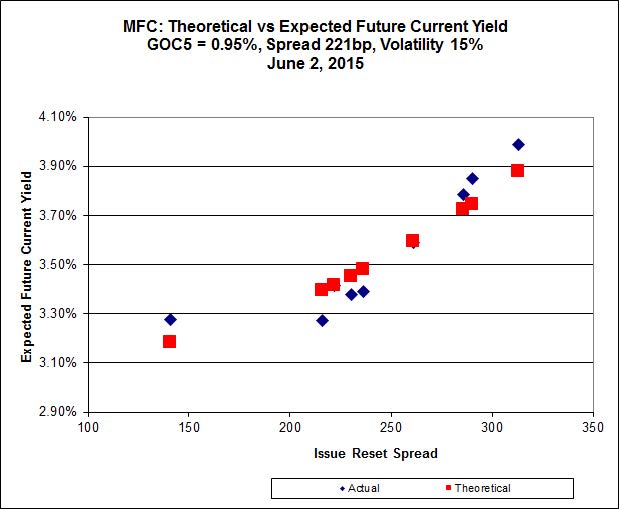

Click for Big

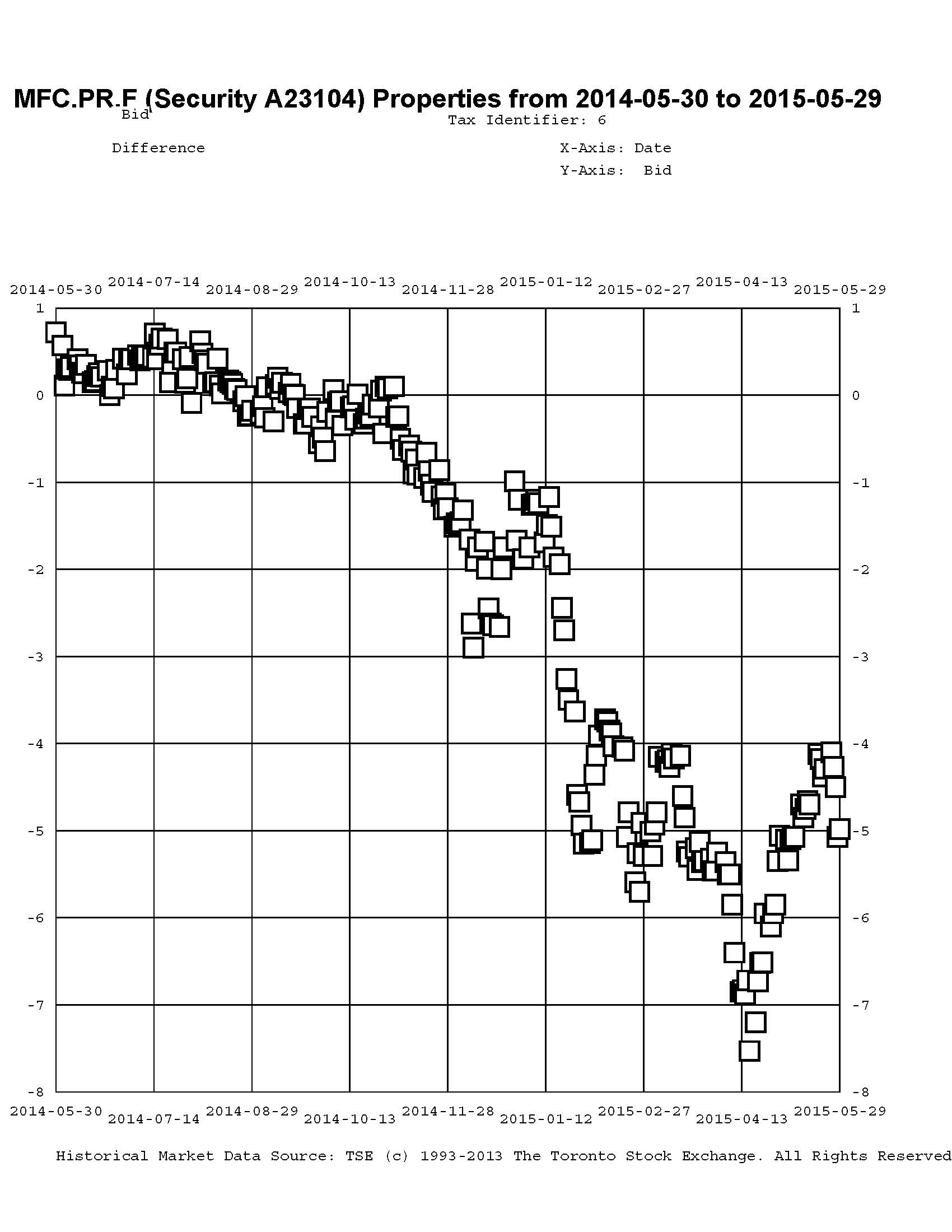

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule). It is clear that the lowest spread issue, MFC.PR.F, is well off the relationship defined by the other issues, but this doesn’t resolve the conundrum – it just makes it more conundrous.

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 23.75 to be $0.84 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.00 to be $0.72 cheap.

Click for Big

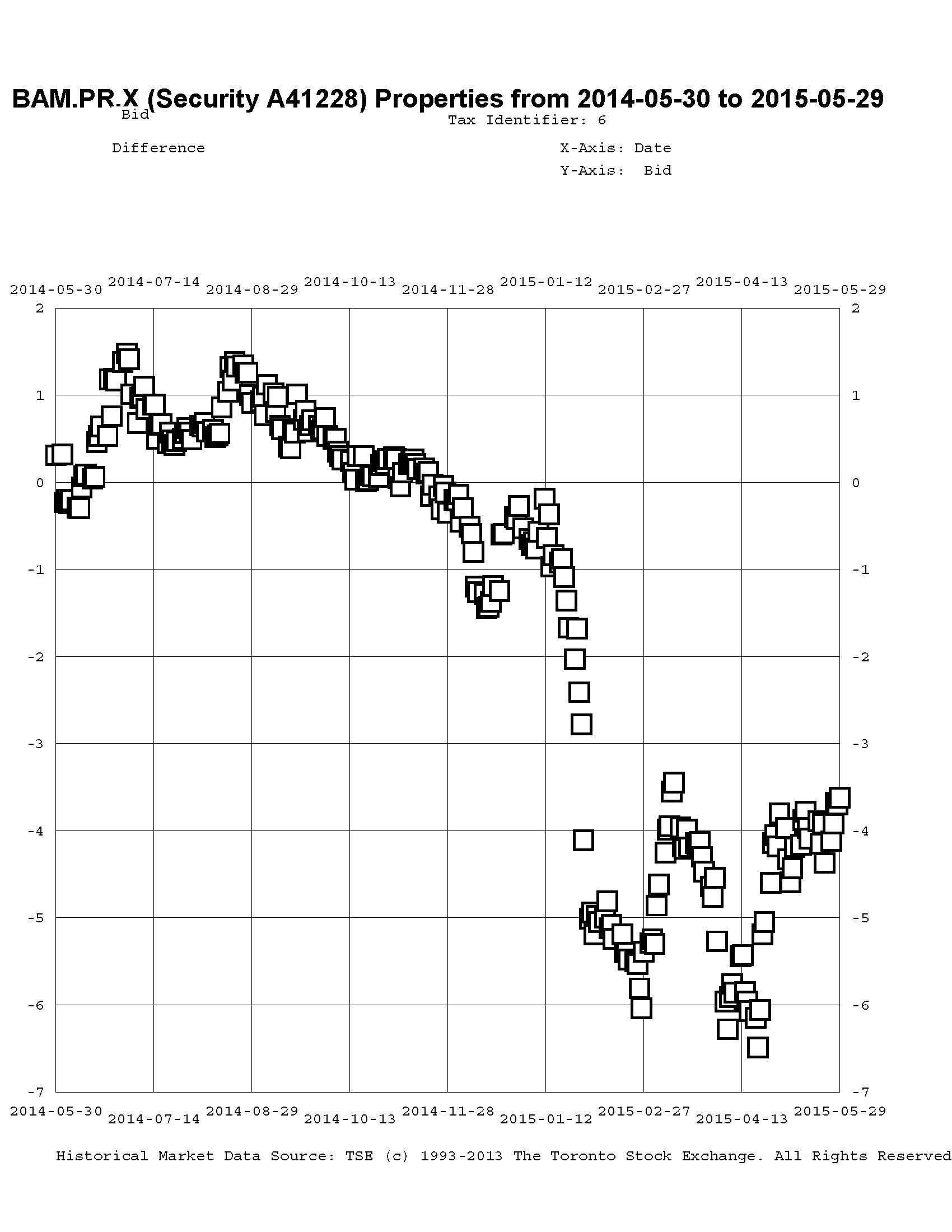

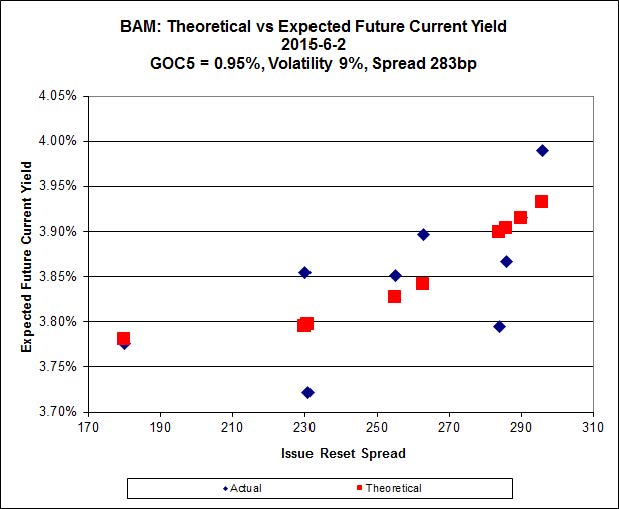

The cheapest issue relative to its peers is BAM.PR.Z, resetting at +296bp on 2017-12-31, bid at 24.50 to be $0.36 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.97 and appears to be $0.67 rich.

Click for Big

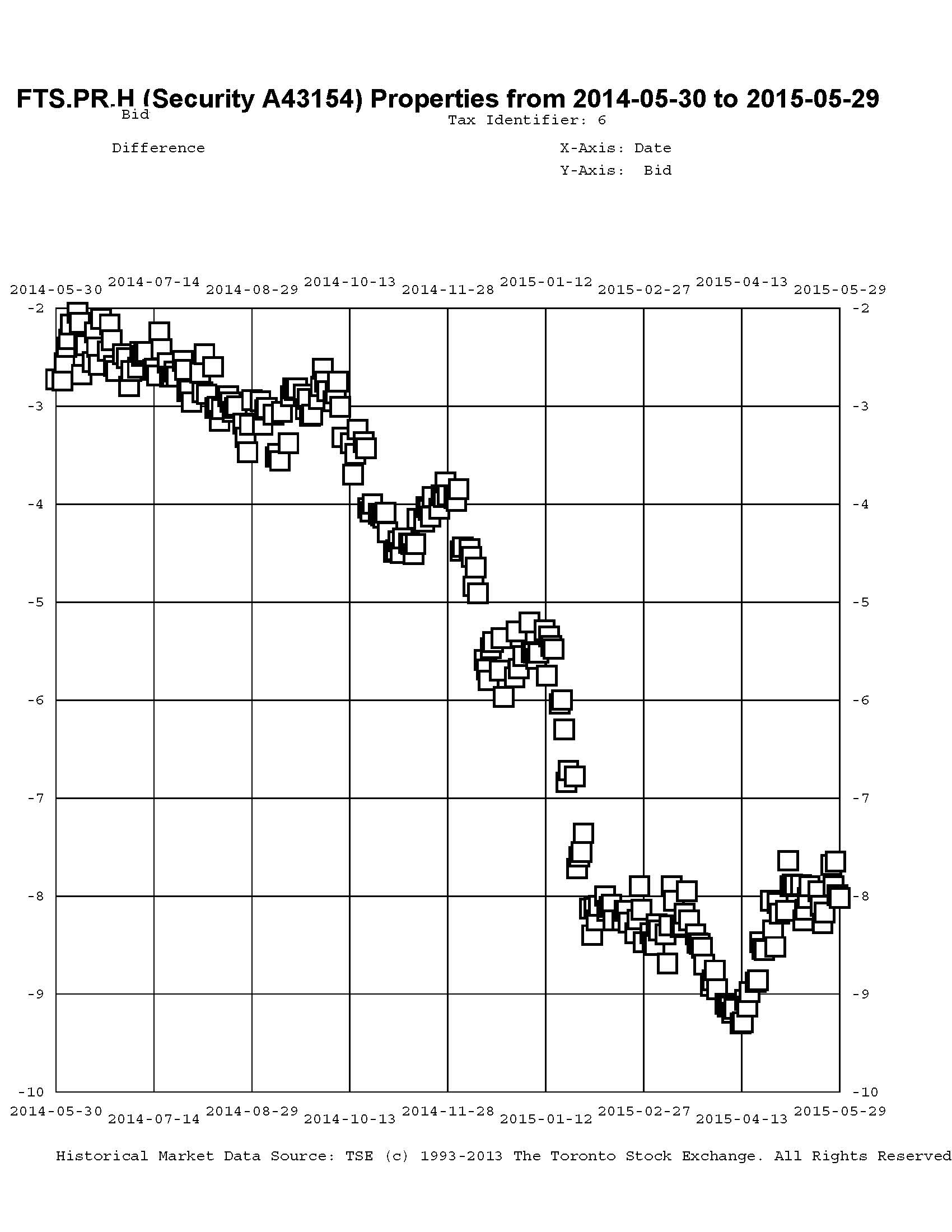

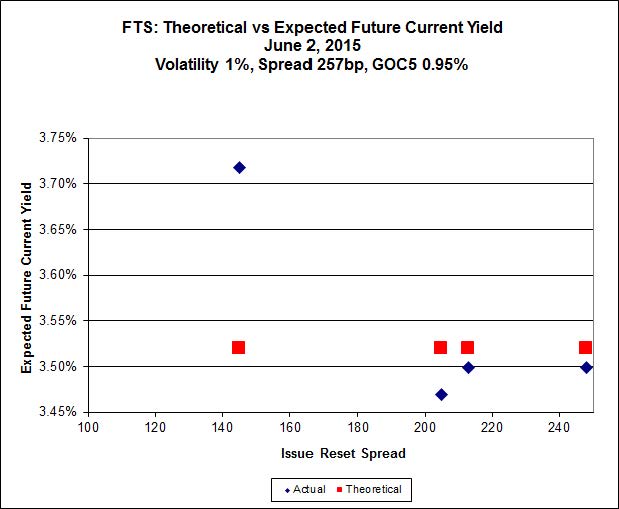

FTS.PR.H, with a spread of +145bp, and bid at 16.14, looks $0.91 cheap and resets 2020-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 21.62 and is $0.31 rich.

Click for Big

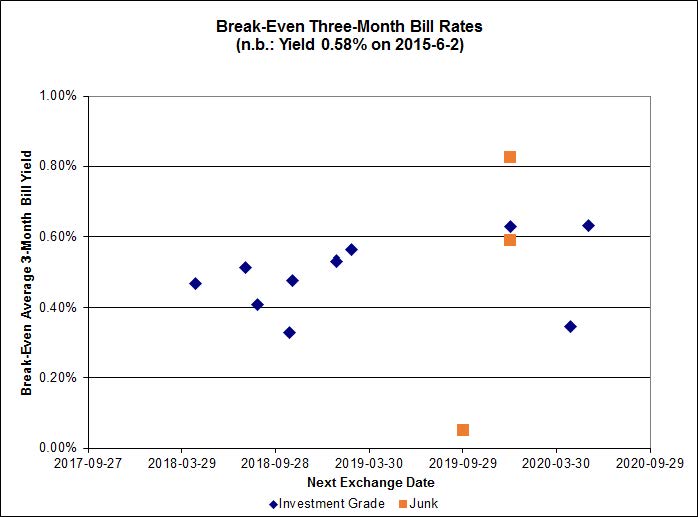

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of about 0.50%, and are very nicely clustered today. On the junk side, three pairs are outside the range of the graph: FFH.PR.E / FFH.PR.F at -0.97%; AIM.PR.A / AIM.PR.B at -1.43%; and BRF.PR.A / BRF.PR.B at -1.38%.

Click for Big

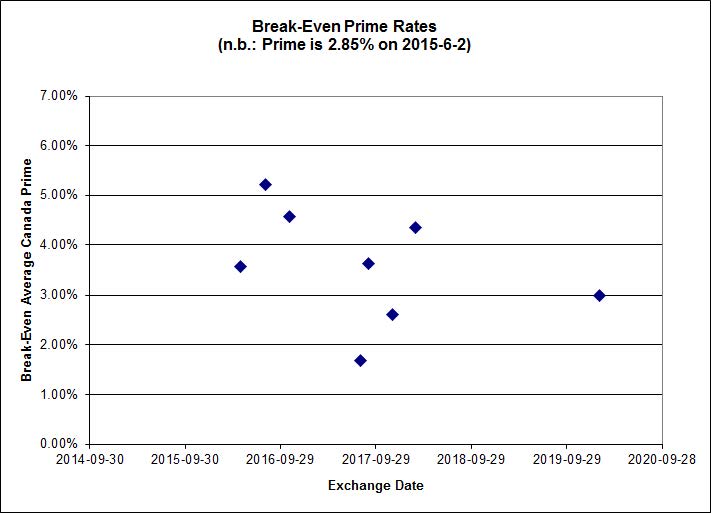

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -2.8091 % | 2,165.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -2.8091 % | 3,785.6 |

| Floater | 3.54 % | 3.60 % | 60,998 | 18.24 | 3 | -2.8091 % | 2,301.7 |

| OpRet | 4.44 % | -14.09 % | 28,776 | 0.09 | 2 | 0.0000 % | 2,782.9 |

| SplitShare | 4.60 % | 4.47 % | 70,145 | 3.32 | 3 | -0.2545 % | 3,242.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,544.7 |

| Perpetual-Premium | 5.45 % | 4.72 % | 64,156 | 1.50 | 19 | -0.1406 % | 2,517.2 |

| Perpetual-Discount | 5.07 % | 5.04 % | 115,590 | 15.44 | 14 | 0.2329 % | 2,771.1 |

| FixedReset | 4.45 % | 3.74 % | 260,257 | 16.56 | 86 | -0.0721 % | 2,385.0 |

| Deemed-Retractible | 4.98 % | 3.42 % | 110,781 | 0.88 | 34 | -0.0902 % | 2,633.5 |

| FloatingReset | 2.49 % | 2.90 % | 54,947 | 6.16 | 9 | -0.1656 % | 2,332.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.K | Floater | -3.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 13.90 Evaluated at bid price : 13.90 Bid-YTW : 3.63 % |

| BAM.PR.B | Floater | -3.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 14.29 Evaluated at bid price : 14.29 Bid-YTW : 3.53 % |

| BAM.PR.C | Floater | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 14.02 Evaluated at bid price : 14.02 Bid-YTW : 3.60 % |

| BAM.PF.E | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 22.12 Evaluated at bid price : 22.72 Bid-YTW : 4.08 % |

| HSE.PR.A | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 4.16 % |

| TRP.PR.C | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 16.52 Evaluated at bid price : 16.52 Bid-YTW : 3.83 % |

| ENB.PF.E | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 20.48 Evaluated at bid price : 20.48 Bid-YTW : 4.65 % |

| ENB.PF.A | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 20.59 Evaluated at bid price : 20.59 Bid-YTW : 4.60 % |

| TRP.PR.F | FloatingReset | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 18.91 Evaluated at bid price : 18.91 Bid-YTW : 3.29 % |

| BAM.PF.C | Perpetual-Discount | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 22.48 Evaluated at bid price : 22.88 Bid-YTW : 5.37 % |

| BAM.PR.M | Perpetual-Discount | 1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 22.24 Evaluated at bid price : 22.54 Bid-YTW : 5.35 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| ENB.PR.T | FixedReset | 86,200 | RBC crossed blocks of 35,000 and 34,700, both at 19.35. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 19.31 Evaluated at bid price : 19.31 Bid-YTW : 4.60 % |

| ENB.PR.F | FixedReset | 71,061 | Nesbitt crossed 60,000 at 19.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 18.97 Evaluated at bid price : 18.97 Bid-YTW : 4.66 % |

| BAM.PR.C | Floater | 54,189 | TD crossed 47,400 at 14.15. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 14.02 Evaluated at bid price : 14.02 Bid-YTW : 3.60 % |

| RY.PR.D | Deemed-Retractible | 52,290 | RBC crossed 50,000 at 25.30. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-02-24 Maturity Price : 25.00 Evaluated at bid price : 25.26 Bid-YTW : 3.20 % |

| BAM.PR.B | Floater | 39,484 | TD crossed 24,500 at 14.58. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 14.29 Evaluated at bid price : 14.29 Bid-YTW : 3.53 % |

| ENB.PF.A | FixedReset | 28,475 | Nesbitt crossed 12,000 at 20.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-02 Maturity Price : 20.59 Evaluated at bid price : 20.59 Bid-YTW : 4.60 % |

| There were 20 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CM.PR.O | FixedReset | Quote: 24.13 – 24.65 Spot Rate : 0.5200 Average : 0.3823 YTW SCENARIO |

| BAM.PF.D | Perpetual-Discount | Quote: 22.96 – 23.47 Spot Rate : 0.5100 Average : 0.4108 YTW SCENARIO |

| PVS.PR.D | SplitShare | Quote: 24.26 – 24.62 Spot Rate : 0.3600 Average : 0.2639 YTW SCENARIO |

| CU.PR.E | Perpetual-Discount | Quote: 24.58 – 24.85 Spot Rate : 0.2700 Average : 0.1743 YTW SCENARIO |

| CM.PR.P | FixedReset | Quote: 23.49 – 23.89 Spot Rate : 0.4000 Average : 0.3051 YTW SCENARIO |

| ELF.PR.F | Perpetual-Premium | Quote: 25.05 – 25.36 Spot Rate : 0.3100 Average : 0.2170 YTW SCENARIO |