Inflation picked up a little in the US:

The U.S. cost of living excluding what households pay for food and fuel climbed more than forecast in April, indicating inflation is gravitating toward the Federal Reserve’s goal.

The core consumer-price index rose 0.3 percent, the biggest gain since January 2013 and reflecting broad-based increases, a Labor Department report showed Friday. In the last three months, core inflation advanced an annualized 2.6 percent, the most since August 2011. Including food and fuel, the gauge was up a more moderate 0.1 percent as prices fell at grocery stores and gas stations.

…

Inflation will need to keep rising in order for Fed officials to be “reasonably confident” that progress on their price stability mandate is sufficient to allow for an increase in the benchmark interest rate. The Fed’s preferred measure of price growth, the personal consumption expenditures gauge, rose 0.3 percent in the year ended March and hasn’t met the bank’s goal since April 2012.

And Yellen sees a gradual tightening commencing this year:

Federal Reserve Chair Janet Yellen said she still expects to raise interest rates this year if the economy meets her forecasts, with a gradual pace of tightening to follow.

While the labor market is nearing full strength, “we are not there yet,” she said Friday in a speech in Providence, Rhode Island.

“If the economy continues to improve as I expect, I think it will be appropriate at some point this year to take the initial step to raise the federal funds rate,” she said.

Even after the first rate increase since 2006, “I anticipate that the pace of normalization is likely to be gradual,” Yellen, 68, said.

…

She also repeated the Fed’s two criteria for raising rates, which have been kept near zero since December 2008: “I will need to see continued improvement in labor market conditions, and I will need to be reasonably confident that inflation will move back to 2 percent over the medium term.”

Assiduous Reader prefhound sent me a wonderful link in the Economist:

So-called contingent convertible bonds, or “cocos”, turn into equity when a bank is struggling, trimming its debts and interest payments. Coco issuance has soared since 2010, as banks have sought to keep regulators happy by bolstering their ability to withstand losses. These fancy bonds have the upsides of debt in good times, but provide a cushion in a crisis.

Or so the theory goes. Cocos usually convert when regulators decree that a bank’s capital has fallen below some threshold. In the height of a crisis, that puts regulators in a bind: announcing that a bank is weak can cause panic. A conversion also imposes sudden losses on bondholders, who find themselves holding shares worth much less than the bonds that spawned them. If the bondholders are themselves in distress, those losses can reverberate around the financial system.

Jeremy Bulow of Stanford University and Paul Klemperer of Oxford University see a way to overcome these problems with a new instrument called an equity recourse note, or ERN. Like a coco, an ERN functions as debt in normal times. But the trigger for the conversion is the bank’s share price, rather than a regulatory measure of capital. When the share price falls by enough—say, to 25% of its initial value—the bank can make repayments on the bond with new shares rather than with cash.

…

This avoids several problems with cocos. There is no uncertainty about how regulators will behave. Abrupt losses are minimised: investors can see when the share price is nearing the trigger, and if it recovers, cash payments resume. Because the new shares are worth no more than the cash saved, ERN conversions should shore up a bank’s share price (by contrast, when cocos convert, enough new shares are created to push the price down).

The source paper is Equity Recourse Notes: Creating Counter-cyclical Bank Capital. I will try to give this its own dedicated post soon.

So the Dalhousie Dentistry Debacle has come to a conclusion:

“There was an immense amount of trying to find out what happened here and then the next stage was how did the facts matter, what was the impact,” said Jennifer Llewellyn, the law school professor who led the restorative justice process that began in December.

Twelve of the 13 male dentistry students in the group were involved in that process and participated in more than 150 hours each of seminars, workshops and discussions with their male and female classmates, faculty, staff and community members. The 12 have now met professionalism standards and are eligible to graduate if they complete their clinical work, the university said.

…

Friday’s report is only the first of several to come. A separate, independent task force led by University of Ottawa law professor Constance Backhouse will release its own report at the end of June.

And this crap, boys and girls, is why university education is so expensive. The best part, however, comes from an Ontario regulator:

“I have always taken the position that just because a university gives out a dental degree does not mean I have to give out a licence,” said Irwin Fefergrad, registrar of the Royal College of Dental Surgeons of Ontario.

In January, the college changed the application form required for every applicant who wants to practise in the province to include a question about whether they have ever been the subject of an inquiry or investigation by a university. If the answer is yes, the College will collect information on that inquiry before issuing a licence, Mr. Fefergrad said.

So the useless parasite will trust a University to grant a dental degree, but not to come to acceptable conclusions following an inquiry or investigation; he intends to gather information and, presumably, weigh it carefully. Nice work if you can get it! Particularly since anybody who wants to be a dentist in Ontario had damn well better be very polite to wise Mr. Fefergrad.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 1bp, FixedResets off 2bp and DeemedRetractibles down 4bp. Volatility was higher than one might expect, given the calm overall figures, with ENB FixedResets prominent on the downside. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

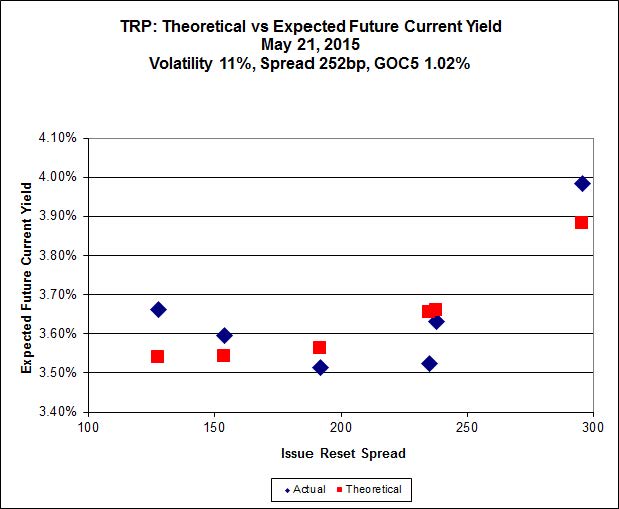

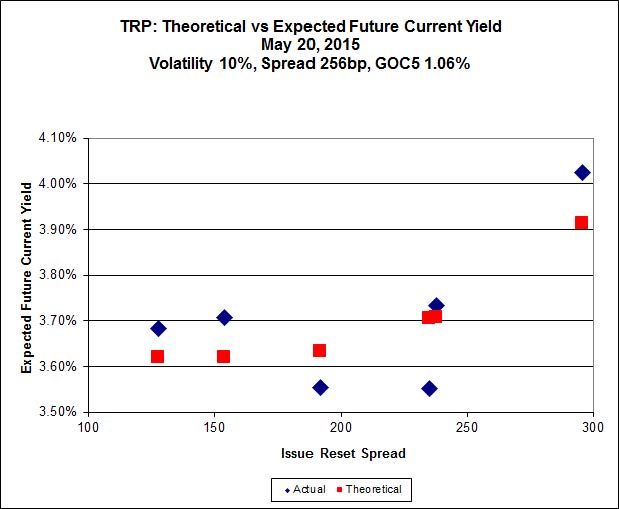

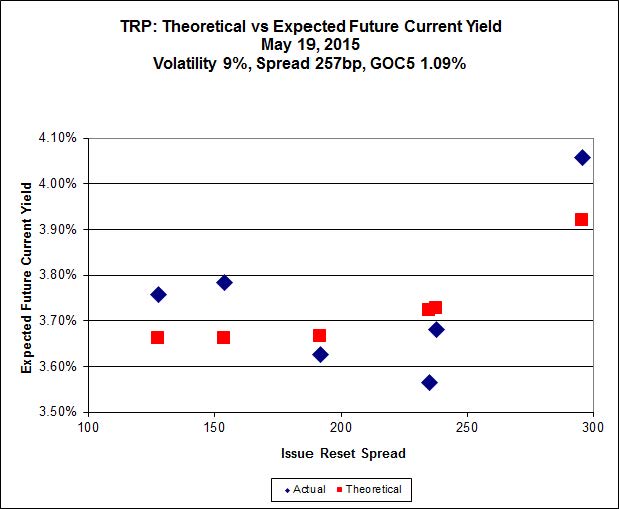

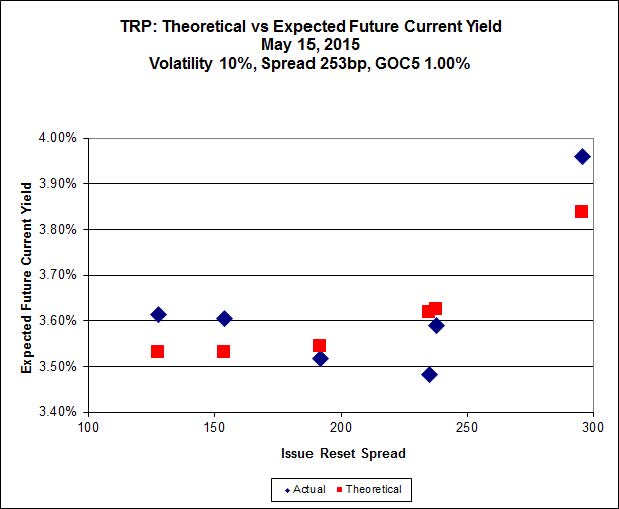

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.03 to be $0.87 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.82 cheap at its bid price of 24.98.

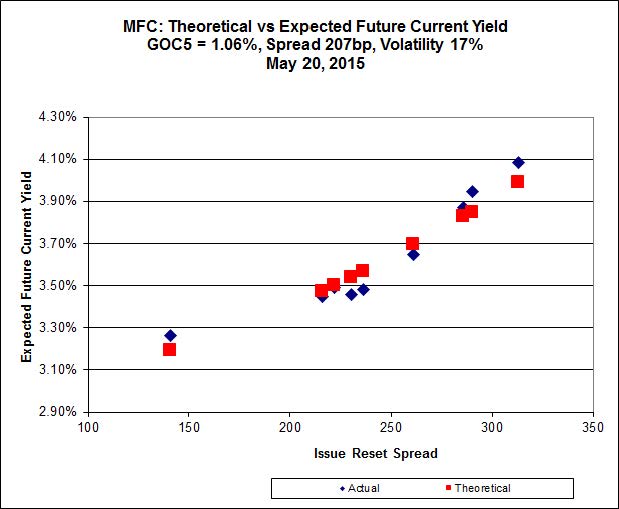

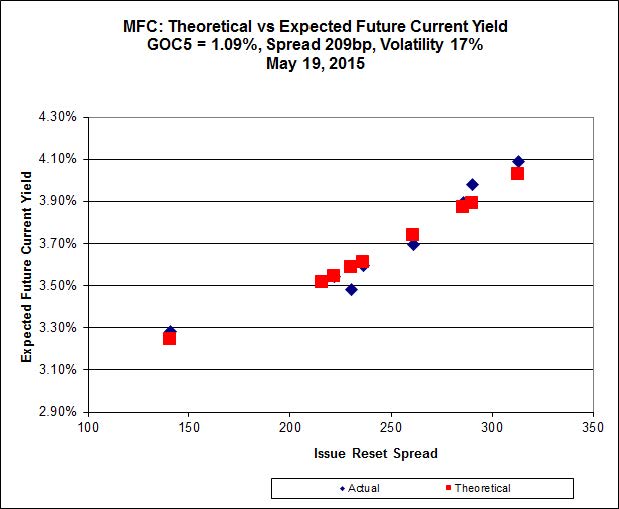

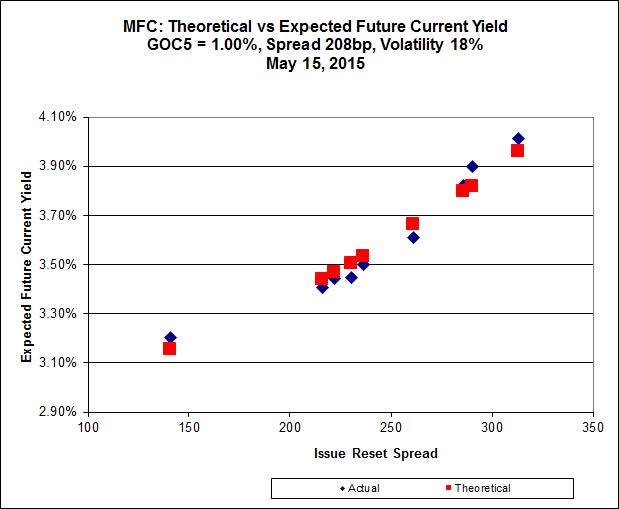

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.N, resetting at +230 on 2020-3-19, bid at 24.30 to be $0.63 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.10 to be $0.54 cheap.

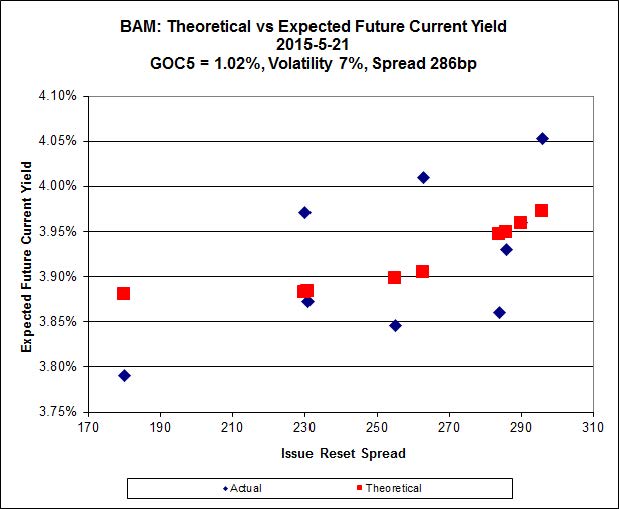

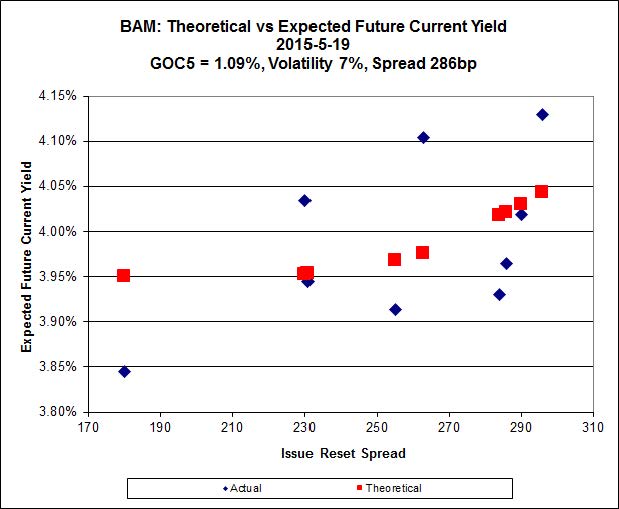

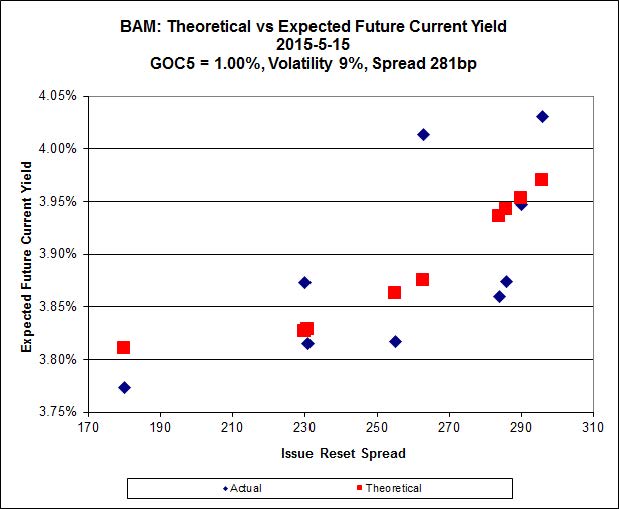

Click for Big

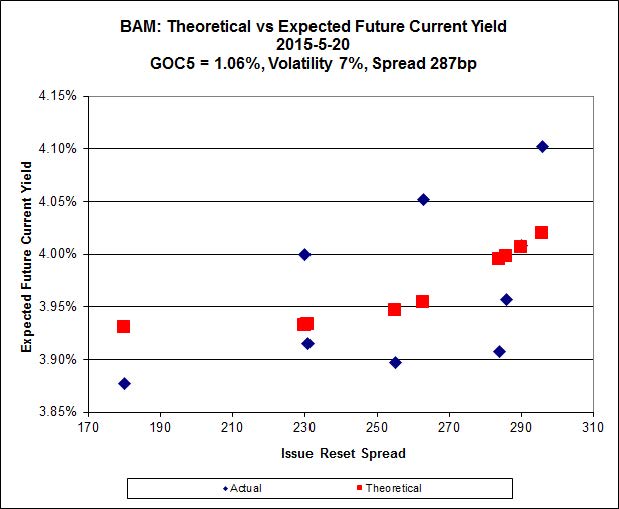

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.77 to be $0.51 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.96 and appears to be $0.53 rich.

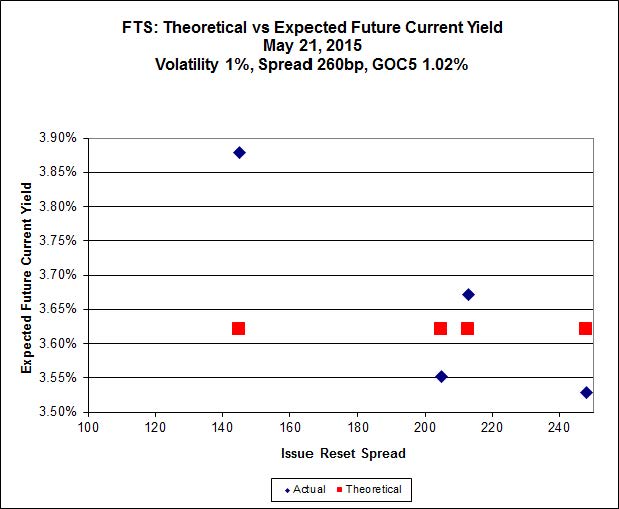

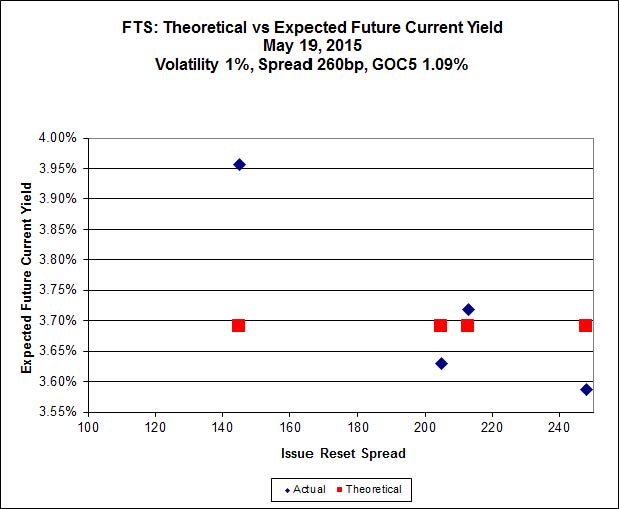

Click for Big

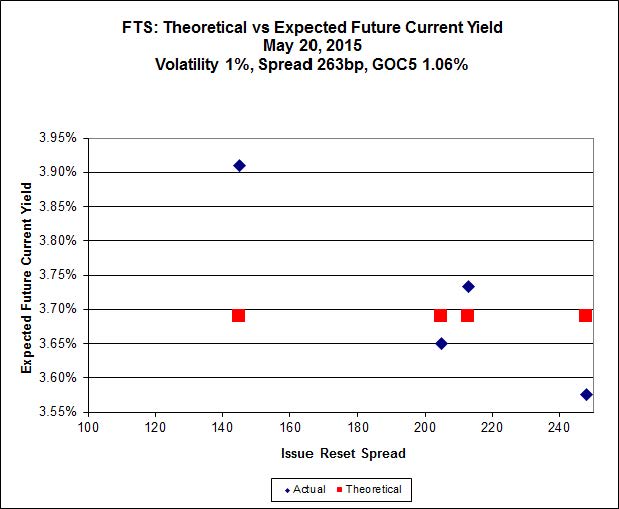

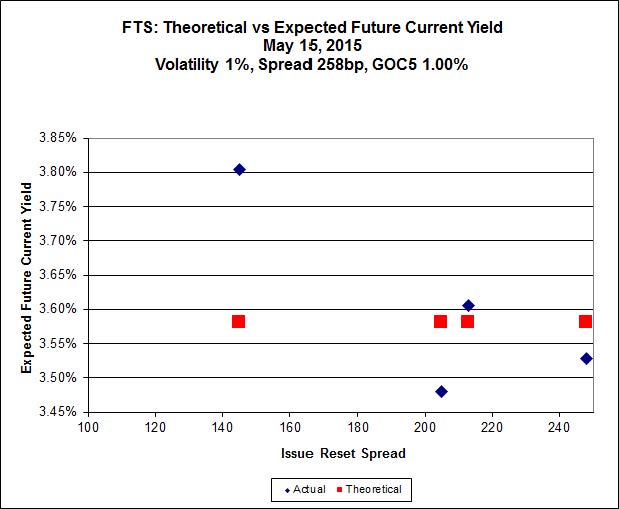

FTS.PR.H, with a spread of +145bp, and bid at 16.07, looks $1.13 cheap and resets 2015-6-1. FTS.PR.M, with a spread of +248bp and resetting 2019-12-1, is bid at 25.00 and is $0.69 rich.

Click for Big

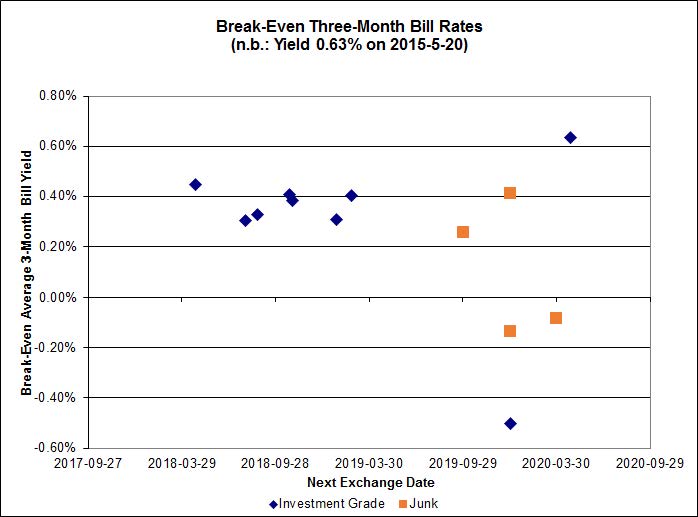

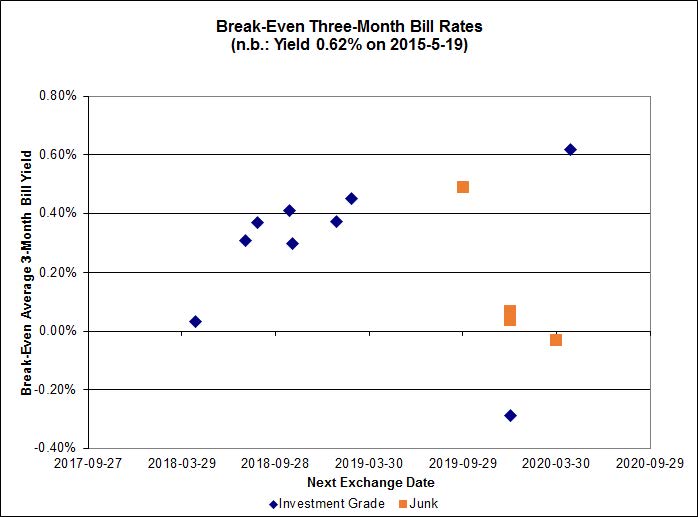

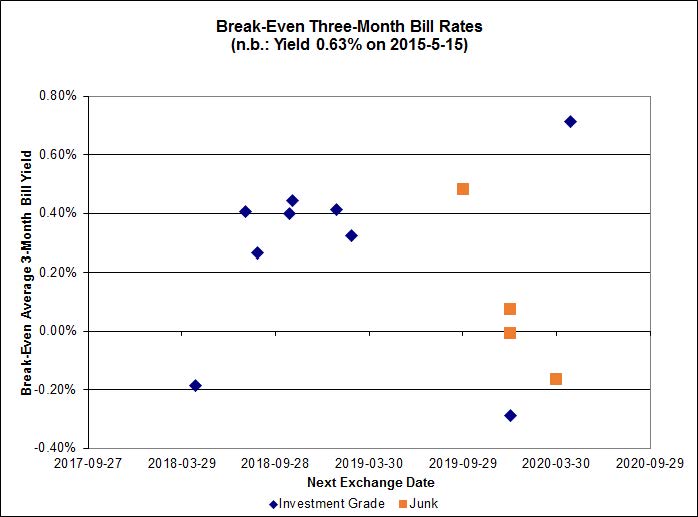

Investment-grade pairs predict an average over the next five-odd years of about 0.30%, including the TRP.PR.A / TRP.PR.F at -0.55%. On the junk side, the FFH.PR.E / FFH.PR.F pair is at -1.18%.

Click for Big

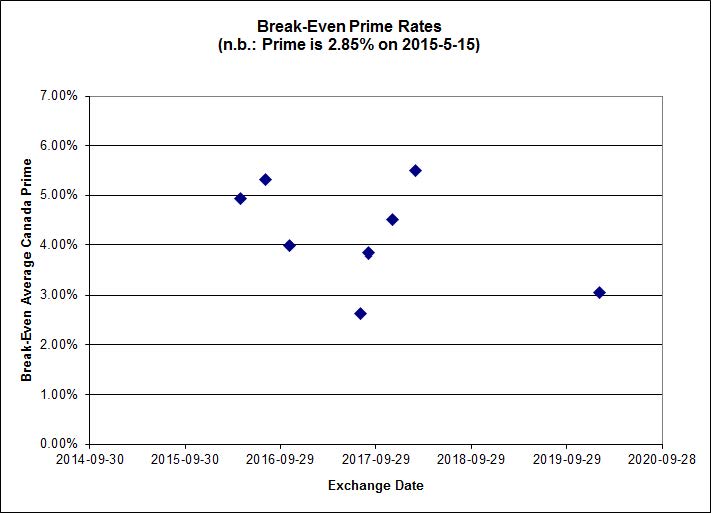

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3028 % | 2,290.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3028 % | 4,004.9 |

| Floater | 3.17 % | 3.33 % | 53,861 | 18.87 | 4 | 0.3028 % | 2,435.0 |

| OpRet | 4.45 % | -8.74 % | 33,209 | 0.11 | 2 | 0.0792 % | 2,779.1 |

| SplitShare | 4.60 % | 4.77 % | 63,567 | 3.35 | 3 | -0.0269 % | 3,240.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0792 % | 2,541.2 |

| Perpetual-Premium | 5.46 % | 2.54 % | 63,683 | 0.08 | 18 | 0.0349 % | 2,517.8 |

| Perpetual-Discount | 5.06 % | 5.06 % | 117,647 | 15.37 | 15 | 0.0112 % | 2,782.3 |

| FixedReset | 4.41 % | 3.80 % | 271,221 | 16.02 | 86 | -0.0239 % | 2,413.3 |

| Deemed-Retractible | 4.94 % | 3.49 % | 107,955 | 0.83 | 35 | -0.0389 % | 2,635.3 |

| FloatingReset | 2.56 % | 2.92 % | 57,844 | 6.16 | 7 | 0.0852 % | 2,335.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.M | FixedReset | -2.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.97 Bid-YTW : 4.18 % |

| BAM.PR.X | FixedReset | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 4.30 % |

| ENB.PR.D | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 18.78 Evaluated at bid price : 18.78 Bid-YTW : 4.73 % |

| ENB.PR.P | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 19.45 Evaluated at bid price : 19.45 Bid-YTW : 4.74 % |

| SLF.PR.A | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.01 Bid-YTW : 5.40 % |

| TRP.PR.C | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 17.61 Evaluated at bid price : 17.61 Bid-YTW : 3.84 % |

| RY.PR.M | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 22.75 Evaluated at bid price : 24.00 Bid-YTW : 3.80 % |

| ENB.PR.Y | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.68 % |

| MFC.PR.F | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.01 Bid-YTW : 5.97 % |

| FTS.PR.G | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 21.42 Evaluated at bid price : 21.75 Bid-YTW : 3.81 % |

| TRP.PR.B | FixedReset | 1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 3.76 % |

| SLF.PR.G | FixedReset | 2.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.00 Bid-YTW : 6.52 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.T | FixedReset | 128,880 | Desjardins crossed blocks of 50,000 and 11,000, both at 24.72. Nesbitt crossed 40,000 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 23.09 Evaluated at bid price : 24.62 Bid-YTW : 3.39 % |

| TD.PF.B | FixedReset | 104,491 | TD crossed blocks of 24,700 and 25,000 at 24.50. Desjardins crossed blocks of 21,700 and 10,500 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 23.03 Evaluated at bid price : 24.45 Bid-YTW : 3.45 % |

| IFC.PR.C | FixedReset | 57,304 | Nesbitt crossed 50,000 at 24.80. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.75 Bid-YTW : 4.03 % |

| TD.PF.D | FixedReset | 57,258 | TD crossed 50,000 at 24.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 23.09 Evaluated at bid price : 24.84 Bid-YTW : 3.76 % |

| CM.PR.Q | FixedReset | 52,190 | Scotia crossed 25,000 at 25.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 23.15 Evaluated at bid price : 25.00 Bid-YTW : 3.73 % |

| ENB.PR.N | FixedReset | 51,912 | Scotia crossed 40,000 at 20.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-22 Maturity Price : 20.13 Evaluated at bid price : 20.13 Bid-YTW : 4.73 % |

| There were 32 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.M | FixedReset | Quote: 23.97 – 24.60 Spot Rate : 0.6300 Average : 0.4011 YTW SCENARIO |

| RY.PR.M | FixedReset | Quote: 24.00 – 24.70 Spot Rate : 0.7000 Average : 0.5309 YTW SCENARIO |

| BAM.PF.D | Perpetual-Discount | Quote: 23.28 – 23.65 Spot Rate : 0.3700 Average : 0.2162 YTW SCENARIO |

| ENB.PR.P | FixedReset | Quote: 19.45 – 19.74 Spot Rate : 0.2900 Average : 0.1751 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 18.20 – 18.53 Spot Rate : 0.3300 Average : 0.2252 YTW SCENARIO |

| CU.PR.D | Perpetual-Discount | Quote: 24.92 – 25.33 Spot Rate : 0.4100 Average : 0.3475 YTW SCENARIO |