John Hull has published an essay titled The Credit Crunch of 2007: What Went Wrong? Why? What Lessons Can Be Learned?:

This paper explains the events leading to the credit crisis that began in 2007 and the products that were created from residential mortgages. It explains the multiple levels of securitization that were involved. It argues that the inappropriate incentives led to a short‐term focus in the decision making of traders and a failure to evaluate the risks being taken. The products that were created lacked transparency with the payoffs from one product depending on the performance of many other products. Market participants relied on the AAA ratings assigned to products without evaluating the models used by rating agencies. The paper considers the steps that can be taken by financial institutions and their regulators to avoid similar crises in the future. It suggests that companies should be required to retain some of the risk in each instrument that is created when credit risk is transferred. The compensation plans within financial institutions should be changed so that they have a longer term focus. Collateralization through either clearinghouses or two‐way collateralization agreements should become mandatory. Risk management should involve more managerial judgment and rely less on the mechanistic application of value‐at‐risk models.

With respect to tranche retention, Dr. Hull argues:

The present crisis might have been less severe if the originators of mortgages (and other assets where credit risk is transferred) were required by regulators to keep, say, 20% of each tranche created. This would have better aligned the interests of originators with the interests of the investors who bought the tranches.

…

The most important reason why originators should have a stake in all the tranches created is that this encourages the originators to make the same lending decisions that the investors would make. Another reason is that the originators often end up as administrators of the mortgages (collecting interest, making foreclosure decisions, etc). It is important that their decisions as administrators are made in the best interests of investors.

…

This idea might have reduced the market excesses during the period leading up to the credit crunch of 2007. However, it should be acknowledged that one of the ironies of the credit crunch is that securitization did not in many instances get the mortgages off the books of originating banks. Often AAA-rated senior tranches created by one part of a bank were bought by other parts of the bank. Because banks were both investors in and originators of mortgages, one might expect a reasonable alignment of the interests of investors and originators. But the part of the bank investing in the mortgages was usually far removed from the part of the bank originating the mortgages and there appears to have been little information flow from one to the other.

Assiduous Readers will not be surprised to learn that I don’t like this idea. In my role as bond trader I have never bought a securitization … I would if the spreads were high enough, but generally spreads are compressed by other buyers.

When I buy a bond, I want to know somebody’s on the hook for it. I like the idea that if the borrower is a day late or a dollar short, I can force an operating company into bankruptcy and cause great anguish and financial ill effects on the deadbeats. Securitizations tend to be highly correllated; while this is claimed to be counterbalanced by the overcollateralization (or tranche subordination, which is simply a formalization of the process) I confess I have a great preference for keeping actual bonds in my bond portfolios.

Tranche retention is simply a methodology whereby securitizations become more bond-like. I object to such blurring of the lines, especially when enforced by governmental regulatory fiat. What I am being told, in a world where such retention is mandated, is that if something has been issued that I – for good reasons or bad – wish to buy and that the security originator wishes to sell, we’ll both go to jail if we consummate the transaction.

I will also point out the logical implications of tranche retention: when I sell 100 shares of SLF.PR.A, I should be forced to retain 20 of them, so that the buyer will know they’re OK. That’s crazy. The buyer should do his own damn homework and make up his own mind.

The world has learned over and over that while regulation is very nice, the only thing that works really well is caveat emptor. I do not want some 20-year old regulator with a college certificate in boxtickingology telling me what I may and may not buy.

Dr. Hull has underemphasized the heart of the matter: one of the ironies of the credit crunch is that securitization did not in many instances get the mortgages off the books of originating banks. Often AAA-rated senior tranches created by one part of a bank were bought by other parts of the bank..

In this context, I will repeat some of Sheila Bair’s testimony to the Crisis Committee:

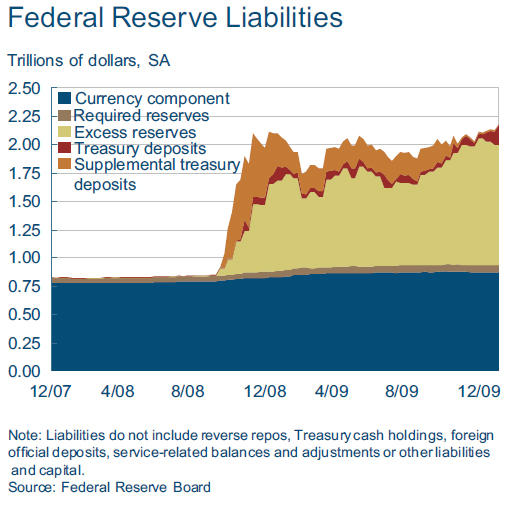

In the mid-1990s, bank regulators working with the Basel Committee on Banking Supervision (Basel Committee) introduced a new set of capital requirements for trading activities. The new requirements were generally much lower than the requirements for traditional lending under the theory that banks’ trading-book exposures were liquid, marked-to-market, mostly hedged, and could be liquidated at close to their market values within a short interval—for example 10 days.

The market risk rule presented a ripe opportunity for capital arbitrage, as institutions began to hold growing amounts of assets in trading accounts that were not marked-to-market but “marked-to-model.” These assets benefitted from the low capital requirements of the market risk rule, even though they were in some cases so highly complex, opaque and illiquid that they could not be sold quickly without loss. Indeed, in late 2007 and through 2008, large write-downs of assets held in trading accounts weakened the capital positions of some large commercial and investment banks and fueled market fears.

I see the basic problem as one that happens when traders try to be investors. Traders do not typically know a lot about the market – although they can talk a good game – and when they try their hand at actual investing, bad things will happen more often than not. It’s a totally different mindset.

I didn’t make a penny during the tech bubble – never bought any of it. I have numerous friends, however, who made out like bandits and set themselves up for life during those years. The difference between us was not the knowledge that that stuff was garbage … we all knew it was garbage. But I could not sleep at night knowing I had garbage in my portfolio; they were fine with the idea, so long as there was lots of positive chatter and prices kept going up.

A long, long time ago – so long I can’t remember the reference – I read an interview with a big wheel (perhaps the proprietor) of a small NASDAQ trading firm. The interview was interupted when one of his staff burst in with the news that another brokerage (XYZ brokers) wanted to sell a large block of stock (45,000 shares, if I remember correctly) in ABC Company and was willing to do so at a discount to market. So they look at the recent price/volume history, check the news and the deal gets done. When the interview resumed, the interviewer asked “So … what’s ABC Company?”. The trader replied, patienty and wearily: “Its something XYZ wanted to sell 45,000 shares of.”

Now that’s trading!

Despite constant interviews by the media, there is not really much correlation between trading ability and investing ability.

So anyway, I will suggest that when considering a regulatory response to the Credit Crunch, a clearer distinction between trading and investing activities is what’s required. As I have previously suggested, there should be no bright-line between investment banks and vanilla banks; but the difference should be recognized in the capital rules. Investment banks should have low capital requirements for trading inventory and higher ones for investment positions; the reverse for vanilla banks. And for heaven’s sake, make sure that there’s no jiggery-pokery with aging positions on the trading books! Hold it for thirty days, and the capital charge goes up progressively! Start trading too many “investment” positions and you’ll find your investment portfolio reclassified.

As far as bonus deferral is concerned … it’s suitable for investors, not so much for traders. Bonus deferral requires a lot of trust by the employee, trust that is all too often unjustified as exemplified by the Citigroup case discussed January 7 and, here in Canada, by the case of David Berry. The major effect of bonus deferral, I believe, will be to spawn a migration of talent to hedge funds and boutiques.

Dr. Hull suggests:

One idea is the following. At the end of each year a financial institution awards a “bonus accrual” (positive or negative) to each employee reflecting the employee’s contribution to the business. The actual cash bonus received by an employee at the end of a year would be the average bonus accrual over the previous five years or zero, whichever is higher. For the purpose of this calculation, bonus accruals would be set equal to zero for years prior to the employee joining the financial institution (unless the employee manages to negotiate otherwise) and bonuses would not be paid after an employee leaves it. Although not perfect, this type of plan would motivate employees to use a multi-year time horizon when making decisions.

One problem I have with that is vesting. Is the vesting of this bonus iron-clad or not? Is it held by a mutually agreed-upon third party in treasury bills? And what happens if the employee leaves the firm and somebody else starts trading his book? Who takes any future losses then?

Another problem, of course, is trust (assuming the vesting is not iron-clad). When a relationship turns sour – or somebody gets greedy – things can turn nasty in a hurry. It should always be remembered that the purpose of regulation is not to protect anybody. The purpose of regulation is to ensure that everybody is guilty of something.

I have twice been offered jobs with the stupidest incentive scheme in the world. Not only would my bonus be determined by how well the firm did – putting me on the hook for decisions made by people I didn’t even know – but because of deferral, up-front transfers and discretion, I could have worked there for five years and paid them for the privilege. Those negotiations didn’t take long!