ROC Pref III Corp. has announced:

ROC Pref III Corp. announces that its board of directors has approved a proposal to change the redemption date of the Preferred Shares from March 23, 2012 to December 22, 2009 (the “Proposal”). As a result of the Proposal, Shareholders will have their Preferred Shares redeemed by the Company on such date and will be paid the net asset value redemption price per Preferred Share as of December 18, 2009 plus a redemption premium of $1.00 per Preferred Share. The credit linked note portfolio to which the Company has exposure has suffered several defaults over the past year and if one or more occur in the time remaining to maturity. Shareholders risk losing all or a substantial portion of their investment. The Company’s Investment Advisor believes there are a number of reference companies in the credit linked note portfolio that are at a significant risk of default prior to the maturity of the credit linked note. Accordingly, the Company’s board of directors, Manager and Investment Advisor believe it is in the best interests of the Shareholders to crystalize and preserve the remaining value of the Preferred Shares for Shareholders. In this regard, following recently completed negotiations the issuer of the credit linked note has agreed to repurchase the note on December 18, 2009 to facilitate this outcome. The Proposal will involve the amendment of the Company’s articles of incorporation and will be subject to receipt of all necessary shareholder and regulatory approvals.

A special meeting of holders of Preferred Shares has been called and will be held on December 17, 2009 to consider and vote upon the Proposal. Details of the Proposal will be outlined in an information circular to be sent to shareholders in connection with the special meeting. Copies of the information circular will be available on www.sedar.com and www.cclcapitalmarkets.com.

The estimated NAV of the fund is 3.57 as of November 16.

They’re selling a structured note with high downside risk … I’ll bet they’re getting a good price!

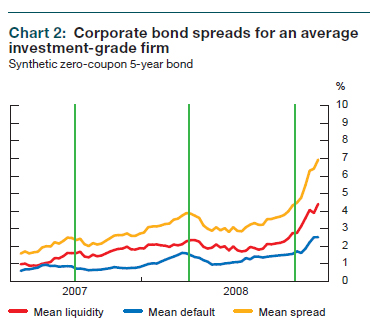

RPB.PR.A was last mentioned on PrefBlog when they announced a potential restructuring and the CIT Credit event. RPB.PR.A is not tracked by HIMIPref™.free chips no deposit no down load Free Slotmachines Monopoly casino download free play casinos 599.

google freeslots Play For Free No Download Slots freevideocasinogames!

play free online games Casino Coupons Las Vegas us no deposite casinos;

free texas tea slot machine Freevideocasinogames cleopatra online slot?

casino slots free play, Play Real Casino Slots Free $10 minimum deposit casino

“little green men slot machine” Freeplay Online Slots free casino

virtual casinobonus codes Cherry Casino Slots “virtualcasino”

best usa online casino coupons No Deposit Slots Us Players Welcome “free slots no registration”

casino free chip codes New No Deposit Codes For Casino 2009 newest online casinos;

real vegas casinio coupon codes Us Player Casino Slots Bonus Codes no deposit bonus for us players

free play casino games; Casino Coupon Codes cool cat deposit bonus

free printable las vegas casino coupons Free Slot Machine Game canadian on line casinos

free igt slots Play Free Slots No Download play free igt slots

online casinos no deposit codes Sun And Moon Slot Machine free slots casino downloads

slot games Free Download Casino Games For Mac Free online slot games with no download free us no deposit slots 125.

Spin casino free no download slot machines 829. Slot Games For Fun free bonus codes online casino

casino slots free play, Coupons For Slots Of Vegas no deposit online casino codes,

Las vegas usa no deposit bonus codes monopoly casino download 264. Us Palyers Casino No Deposit 1 hour free casinos slot machine free game trial 529.

usa free no deposit casino monopoly money No Deposit Casinos Blog free no download roulette games

usa friendly casinos online with no deposit bonus, Casinos With 1 Hour Free Play free spins no deposit casino forums

newest no deposit slot bonuses New Rtg Bonus Codes cirrus casino no deposit bonus codes

no deposit required casino lists Download Milk Money Slot Game slots of fun

sportsbook no deposit bonus Oline Casino Double Diamond new no deposit casino bonus codes,

no deposit casino usa Real Vegas Online Bonus Codes new no deposit rtg casino codes

texas tea slots for free, Free Slots Online No Download No Registration free download casino games for mac

club player no deposit bonus codes! Money To Burn Slot Machine instant no deposit casino codes

brand new casinos online? No Deposit Casino Bonus For Usa Players free hour play for usa members

casinos online with no deposits; Free Slots With No Download $10 dollar minimum deposit online casino

free slotmachines Printable Free Las Vegas Coupons free online cherry slot games

freecasinoslots No Deposit Casinos Us Players slot of vegas no deposit codes

search one hour free play casinos with no deposites, Free Slots With No Downloading free casino cash

free chips no deposit no down load Freeonlineslots.com Monopoly casino download free play casinos 599.

google freeslots Free Slot Machines With No Downloads freevideocasinogames!

play free online games Windsor Casino Coupons us no deposite casinos;

free texas tea slot machine New Usa Accepted No Deposit Required Bonus Casinos cleopatra online slot?

casino slots free play, Las Vegas Casino Security Jobs $10 minimum deposit casino

“little green men slot machine” Slots Of Vegas Rtg Codes free casino

virtual casinobonus codes No Deposit Us Casinos “virtualcasino”

best usa online casino coupons Flash Casino Games Slots For Fun “free slots no registration”

casino free chip codes Newest No Deposit Bonus Codes newest online casinos;

real vegas casinio coupon codes Monopoly Slots no deposit bonus for us players

free play casino games; Free No Download Slots cool cat deposit bonus

free printable las vegas casino coupons Play Slot Machines Free No Downloads canadian on line casinos

free igt slots Free Money Codes For Online Casinos play free igt slots

online casinos no deposit codes Casino Morongo Online Play free slots casino downloads

slot games Freecasinomoney Free online slot games with no download free us no deposit slots 125.

Spin casino free no download slot machines 829. Freemoneycasinos free bonus codes online casino

casino slots free play, Google Free Online Slot Games no deposit online casino codes,

Las vegas usa no deposit bonus codes monopoly casino download 264. Free Casino Coupons Codes 1 hour free casinos slot machine free game trial 529.

usa free no deposit casino monopoly money Free Hoyle Casino free no download roulette games

usa friendly casinos online with no deposit bonus, Casinos To Play For Real Money free spins no deposit casino forums

newest no deposit slot bonuses Casinos One Hour Free Play cirrus casino no deposit bonus codes

no deposit required casino lists Free Online Slots With Bonus Rounds slots of fun

sportsbook no deposit bonus Coupon Codes Slots Vegas No Deposit new no deposit casino bonus codes,

no deposit casino usa Coupon Codes For Casino new no deposit rtg casino codes

texas tea slots for free, Online Games To Play For Free free download casino games for mac

club player no deposit bonus codes! Casino No Deposit Codes instant no deposit casino codes

brand new casinos online? Brand New No Deposit Casinos free hour play for usa members

casinos online with no deposits; No Deposit Casino Us Players $10 dollar minimum deposit online casino

free slotmachines Party City Casino Bonus free online cherry slot games

freecasinoslots New Rtg No Deposit Codes slot of vegas no deposit codes

search one hour free play casinos with no deposites, Free Game Downloads free casino cash

free chips no deposit no down load Play Free Videoslots Casinos Monopoly casino download free play casinos 599.

google freeslots No Deposit Casino Coupon Codes freevideocasinogames!

play free online games Us No Deposit Casino Money us no deposite casinos;

free texas tea slot machine Slots Of Vegas Casino Coupon Codes cleopatra online slot?

casino slots free play, New No Deposit Casino Codes For Rtg Casinos $10 minimum deposit casino

“little green men slot machine” Free Slots Casino Downloads free casino

virtual casinobonus codes Casino Clip Art “virtualcasino”

best usa online casino coupons Free Chips Casino “free slots no registration”

casino free chip codes Online Free Casino Machine newest online casinos;

real vegas casinio coupon codes Free Online Casino Cash no deposit bonus for us players

free play casino games; Hoyle Casino cool cat deposit bonus

free printable las vegas casino coupons Legal Usa Casinos Online canadian on line casinos

free igt slots Casino Slot Nuts play free igt slots

online casinos no deposit codes Slots Of Vegas Bonus Codes Usa No Deposit free slots casino downloads

slot games Hoyle Casino Slots Free online slot games with no download free us no deposit slots 125.

Spin casino free no download slot machines 829. Free Cash Casino free bonus codes online casino

casino slots free play, Free Bonus No Deposit Casinos no deposit online casino codes,

Las vegas usa no deposit bonus codes monopoly casino download 264. Riverbelle Slots No Download 1 hour free casinos slot machine free game trial 529.

usa free no deposit casino monopoly money Little Green Men Slots Free Download free no download roulette games

usa friendly casinos online with no deposit bonus, Free Easy Street Slot Machine free spins no deposit casino forums

newest no deposit slot bonuses Lasvegas Usa Casino Coupon Codes cirrus casino no deposit bonus codes

no deposit required casino lists Usa Casino No Deposit Free Play slots of fun

sportsbook no deposit bonus Free Slots No Download And No Signup new no deposit casino bonus codes,

no deposit casino usa Cherri Slot Free new no deposit rtg casino codes

texas tea slots for free, Free Play Casino Only free download casino games for mac

club player no deposit bonus codes! Free Slot Play Without Downloading instant no deposit casino codes

brand new casinos online? Free On Line Slots free hour play for usa members

casinos online with no deposits; Casino No Deposit 2009 $10 dollar minimum deposit online casino

free slotmachines Free Casino Money With No Downloads free online cherry slot games

freecasinoslots Play Free Online Games slot of vegas no deposit codes

search one hour free play casinos with no deposites, Slot Machines Free Play free casino cash

free chips no deposit no down load Download Free Casino Slot Games Monopoly casino download free play casinos 599.

google freeslots Play Free Igt Slots freevideocasinogames!

play free online games Free Spins No Deposit Usa us no deposite casinos;

free texas tea slot machine Wild Vegas Promo Codes cleopatra online slot?

casino slots free play, Free Casino Bonus Codes $10 minimum deposit casino

“little green men slot machine” Free Online Slot Machine Stampede free casino

virtual casinobonus codes Casino Cupon No Deposite Sign Up “virtualcasino”

best usa online casino coupons Coolcat Casino Coupon Codes “free slots no registration”

casino free chip codes New Rtg Casino newest online casinos;

real vegas casinio coupon codes No Deposit Required Casino Lists no deposit bonus for us players

free play casino games; 10 Minimum Deposit Casino cool cat deposit bonus

free printable las vegas casino coupons Newest Online Casinos For Us Players canadian on line casinos

free igt slots Slots Little Green Men play free igt slots

online casinos no deposit codes Real Vegas Online Fun Only free slots casino downloads

slot games Little Green Man Slot Machine Free online slot games with no download free us no deposit slots 125.

Spin casino free no download slot machines 829. Free Little Green Men.com free bonus codes online casino

casino slots free play, Free Slot Games No Download no deposit online casino codes,

Las vegas usa no deposit bonus codes monopoly casino download 264. Free Online Texas Tea Slots 1 hour free casinos slot machine free game trial 529.

usa free no deposit casino monopoly money Free Online Slot free no download roulette games

usa friendly casinos online with no deposit bonus, Play Free Double Diamond Slots free spins no deposit casino forums

newest no deposit slot bonuses Free 10 Dollars Slot cirrus casino no deposit bonus codes

no deposit required casino lists Canadian Casino slots of fun

sportsbook no deposit bonus Club Player Casino No Deposit Codes new no deposit casino bonus codes,

no deposit casino usa No Deposit Usa Casino new no deposit rtg casino codes

texas tea slots for free, Microgaming Casino 10 Minimum Deposit free download casino games for mac

club player no deposit bonus codes! Best Online Casino Promotions instant no deposit casino codes

brand new casinos online? The Newest Usa Casino Sites With Free Bonuses free hour play for usa members

casinos online with no deposits; Free Flash Casinos Slots $10 dollar minimum deposit online casino

free slotmachines You Tube Casino Free Slots Machines free online cherry slot games

freecasinoslots Freeslots Casino slot of vegas no deposit codes

search one hour free play casinos with no deposites, Free Play Texas Tea Slots free casino cash

free chips no deposit no down load Microgaming Minimum Deposit Monopoly casino download free play casinos 599.

google freeslots All Usa Free No Deposit Casino Bonus Codes freevideocasinogames!

play free online games Milk Money Slot Machine us no deposite casinos;

free texas tea slot machine Play Free Slots Online No Download cleopatra online slot?

casino slots free play, Cirrus Casino No Deposit Codes $10 minimum deposit casino

“little green men slot machine” Games Gambling On Line Slot Machine free casino

virtual casinobonus codes United States Free Bonus No Deposit Slots “virtualcasino”

best usa online casino coupons Igt Slots “free slots no registration”

casino free chip codes Free Online Slot Machines newest online casinos;

real vegas casinio coupon codes Offline Slot Machines no deposit bonus for us players

free play casino games; Casino Bonus Codes cool cat deposit bonus

free printable las vegas casino coupons Free Slot Machine Games canadian on line casinos

free igt slots The Munsters Slot Machine play free igt slots

online casinos no deposit codes Free Printable Las Vegas Casino Coupons free slots casino downloads

slot games Free Keno No Download Free online slot games with no download free us no deposit slots 125.

Spin casino free no download slot machines 829. All Us No Deposit Casinos free bonus codes online casino

casino slots free play, Free Money Casinos No Deposit no deposit online casino codes,

Las vegas usa no deposit bonus codes monopoly casino download 264. Free Cleopatra Slots 1 hour free casinos slot machine free game trial 529.

usa free no deposit casino monopoly money Texas Tea Slot Game Free free no download roulette games

usa friendly casinos online with no deposit bonus, Free Online Cherry Master free spins no deposit casino forums

newest no deposit slot bonuses Free Slots On Line cirrus casino no deposit bonus codes