The IMF has released a working paper by Peter Stella, The Federal Reserve System Balance Sheet: What Happened and Why it Matters:

The recent expansion of the balance sheet of the consolidated Federal Reserve Banks (FRB) is analyzed in an historical context. The analysis reveals that the nature of Fed involvement in U.S. financial markets has changed dramatically and its expansion is several orders of magnitude beyond what is usually reported. The associated fiscal risks and potential exit strategies are then considered. Although risks are considerable in certain unlikely scenarios, FRB capital, earnings capacity, and reserves are more than ample to preserve their financial independence. Nevertheless, the occurrence of losses or a significant drop in FRB profit might lead to an eventual curtailment of Fed operational independence. The paper concludes by considering options to enhance FRB risk management and to assign responsibilities for monetary, financial stability and fiscal policies once the current crisis is overcome.

Bank of America expects to complete its capital raise shortly:

Bank of America Corporation today said it has raised almost $33 billion towards the $33.9 billion capital buffer identified by the Federal Reserve’s Supervisory Capital Assessment Program (SCAP) and now believes it will comfortably exceed that number.

To date, Bank of America has entered into agreements with certain holders of (non-government) perpetual preferred shares to exchange their holdings of approximately $9.5 billion of perpetual preferred stock into approximately 704 million shares of common stock. This results in a total benefit to Tier 1 common capital of $9.5 billion.

Their exchange offer was announced May 28:

Bank of America is offering to issue shares of common stock in the exchange offer in the applicable consideration amount per depositary share specified in the table below. The number of shares of common stock issuable for each exchanged depositary share will be equal to this consideration amount divided by the average of the daily per share volume-weighted average price of Bank of America common stock for each of the five consecutive trading days ending on and including June 22, 2009 (the second business day prior to the scheduled expiration date of the exchange offer). Bank of America will announce this common stock average price no later than 9 a.m., New York City time, on June 23, 2009. One of the conditions of the exchange offer that must be satisfied or waived is that the common stock average price be $10 or greater.

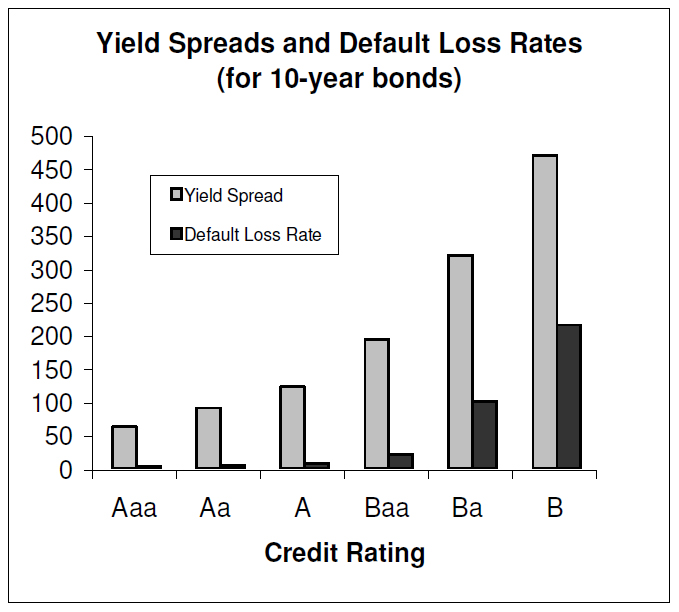

To give you an idea of the rates, the consideration for the Series I is $17.50; it pays 1.65624 annually.

DBRS has changed the trend on Ontario’s long-term debt to negative:

DBRS has today changed the trend on the long-term debt rating of the Province of Ontario (the Province or Ontario) to Negative from Stable. The trend on the Province’s short-term rating remains Stable. The rating action reflects the material erosion observed in the Province’s already depressed fiscal outlook since the beginning of the fiscal year, due in part to the larger-than-expected government bailouts recently announced for two large North American auto companies, amidst significant economic and fiscal uncertainty. As a result, while DBRS takes comfort in the economic diversification and moderately low debt burden of the Province, concerns have increased with respect to the Province’s ability to weather the global recession and the crisis of its auto sector without unduly weakening its credit metrics.

Hardly a surprise. The charlatans of the mid-90’s to mid-00’s cut the good-time surplus to nothing and the current bozos felt they had to compete. The lesson of 1994 has been forgotten; I’d say we’ll hit it again in 10-20 years.

I had a quick look for a historical budgetary balance graph that would include Rae’s recession … unfortunately, no politician wants to admit that the good-time surplus was derisory – the Conservatives because it betrays their fiscal ineptitude, the Liberals because they’ve made a point of complaining about the ever-so-horrible spending reductions in that period, the NDP because they don’t understand the question.

Fortunately, by the time we hit the wall, we’ll be able to push our expensive electric cars to work instead of taking the expensive hybrid busses. But at least we’ll be precious.

The Globe and Mail reports:

Unable to win over the recalcitrant investors, sources said GM Canada officials called for help. Their plea went to Ottawa. Could the government help break the stalemate?

The answer came at shortly after 8 p.m. ET Sunday, when the government announced that Prime Minister Stephen Harper, Industry Minister Tony Clement and Ontario Premier Dalton McGuinty would be speaking at 1 p.m. yesterday in Toronto. No public explanation was offered for the news conference. Privately, however, sources said General Motors officials and their advisers worked the phones through the night to warn the investors that the notice meant the Prime Minister was preparing to single out the bondholders for failing to support a bailout of the troubled auto maker.

“We told the bondholders that the Prime Minister of Canada was going to stand up before the country and say that a reasonable corporate solution had failed and the Canadian operations had landed in bankruptcy proceedings because of the bondholders,” said one person involved in the discussions.

Assuming that these unsupported and anonymous allegations are correct, it’s not clear who is more contemptible: GM Canada, for even thinking of the idea; What-Debt?, for enthusiastically offering to attack on command; the Portfolio Managers, for knuckling under instead of representing their clients; or the regulators who, you may be sure, will not be investigating the matter for possible breach of duty.

The immediate practical implications are, I suggest, an increased chance of increased credit notching for Tier 1 (and equivalent) capital; which is to say, lower credit quality. Throwing your weight around in the capital markets is like eating peanuts…

Knock-on implications – which have probably been ignored when making these decisions – are interesting. I suggest that Recovery-Lock Credit Default Swaps will become more popular.

The preferred share market squeaked out another win today, on continued heavy volume.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0491 % |

1,301.3 |

| FixedFloater |

7.15 % |

5.71 % |

29,468 |

15.99 |

1 |

0.0000 % |

2,108.5 |

| Floater |

2.90 % |

3.36 % |

78,708 |

18.79 |

3 |

0.0491 % |

1,625.7 |

| OpRet |

5.01 % |

3.95 % |

146,397 |

2.56 |

14 |

0.0769 % |

2,167.1 |

| SplitShare |

5.92 % |

6.35 % |

53,111 |

4.27 |

3 |

-0.0311 % |

1,840.8 |

| Interest-Bearing |

6.00 % |

7.46 % |

26,431 |

0.56 |

1 |

0.0000 % |

1,987.2 |

| Perpetual-Premium |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0873 % |

1,726.6 |

| Perpetual-Discount |

6.36 % |

6.34 % |

163,604 |

13.45 |

71 |

0.0873 % |

1,590.2 |

| FixedReset |

5.71 % |

4.88 % |

487,063 |

4.44 |

37 |

0.2703 % |

1,990.1 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| TD.PR.O |

Perpetual-Discount |

-1.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 19.93

Evaluated at bid price : 19.93

Bid-YTW : 6.17 % |

| PWF.PR.L |

Perpetual-Discount |

-1.33 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 19.25

Evaluated at bid price : 19.25

Bid-YTW : 6.73 % |

| SLF.PR.D |

Perpetual-Discount |

-1.12 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 16.76

Evaluated at bid price : 16.76

Bid-YTW : 6.65 % |

| CM.PR.E |

Perpetual-Discount |

1.08 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 21.49

Evaluated at bid price : 21.49

Bid-YTW : 6.61 % |

| GWO.PR.I |

Perpetual-Discount |

1.15 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 17.53

Evaluated at bid price : 17.53

Bid-YTW : 6.43 % |

| BNS.PR.Q |

FixedReset |

1.19 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 24.65

Evaluated at bid price : 24.70

Bid-YTW : 4.28 % |

| W.PR.J |

Perpetual-Discount |

1.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 21.49

Evaluated at bid price : 21.49

Bid-YTW : 6.63 % |

| BMO.PR.J |

Perpetual-Discount |

1.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 18.88

Evaluated at bid price : 18.88

Bid-YTW : 6.01 % |

| PWF.PR.E |

Perpetual-Discount |

1.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 21.36

Evaluated at bid price : 21.36

Bid-YTW : 6.53 % |

| BAM.PR.M |

Perpetual-Discount |

1.90 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 15.00

Evaluated at bid price : 15.00

Bid-YTW : 8.12 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| CM.PR.K |

FixedReset |

71,519 |

Desjardins bought 40,000 from CIBC at 25.06.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 24.95

Evaluated at bid price : 25.00

Bid-YTW : 4.74 % |

| TD.PR.O |

Perpetual-Discount |

65,310 |

TD crossed 11,800 at 20.20.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 19.93

Evaluated at bid price : 19.93

Bid-YTW : 6.17 % |

| MFC.PR.D |

FixedReset |

50,909 |

National bought 20,000 from TD at 26.75.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-07-19

Maturity Price : 25.00

Evaluated at bid price : 26.66

Bid-YTW : 5.09 % |

| CM.PR.I |

Perpetual-Discount |

43,329 |

Nesbitt crossed 27,500 at 18.25.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-06-02

Maturity Price : 18.32

Evaluated at bid price : 18.32

Bid-YTW : 6.51 % |

| BAM.PR.H |

OpRet |

40,463 |

Nesbitt crossed 11,000 at 24.75.

YTW SCENARIO

Maturity Type : Soft Maturity

Maturity Date : 2012-03-30

Maturity Price : 25.00

Evaluated at bid price : 24.85

Bid-YTW : 6.41 % |

| NA.PR.P |

FixedReset |

40,000 |

National crossed 20,000 at 27.00.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-03-17

Maturity Price : 25.00

Evaluated at bid price : 26.94

Bid-YTW : 4.89 % |

| There were 55 other index-included issues trading in excess of 10,000 shares. |