Julia Dickson of OSFI gave a speech to the ABA clearly demonstrating her contempt for investors, the despised third pillar of the banking system. The role of investors – and their reliance on mandated disclosures – was, basically, ignored.

Bloomberg has reported on the Fed’s response to the controversy regarding the size and nature of its emergency actions:

Former Fed Chairman Paul Volcker said Congress will probably review the authority granted to the Fed following the expansion in its assets.

“I don’t think the political system will tolerate the degree of activity that the Federal Reserve, in conjunction with the Treasury, has taken,” Volcker, head of President Barack Obama’s Economic Recovery Advisory Board, said in remarks to the conference at Vanderbilt University.

U.S. lawmakers from both political parties, including House Financial Services Committee Chairman Barney Frank, have expressed concern in recent months that the central bank has overstepped its authority by providing emergency credit.

In his speech, Vice Chairman Donald L. Kohn said:

For the credit facilities that we make available to multiple firms, we are not taking significant credit risk that might end up being absorbed by the taxpayer. For almost all the loans made by the Federal Reserve, we look first to sound borrowers for repayment and then to underlying collateral. Moreover, we lend less than the value of the collateral, with the size of the “haircuts” depending on the riskiness of the collateral and on the availability of market prices for the collateral. Some of our lending programs involve nonrecourse loans that look primarily to the collateral rather than to the borrower for repayment in the event that the value of the collateral falls below the amount loaned. In these circumstances, we insist on taking only the very highest quality collateral, lend less than the face amount of the collateral, and typically have other sources to absorb any losses that might nonetheless occur–for example, Treasury capital for our lending against securitized loans.

…

Will These Policies Lead to a Future Surge in Inflation?

No, and the key to preventing inflation will be reversing the programs, reducing reserves, and raising interest rates in a timely fashion. Our balance sheet has grown rapidly, the amount of reserves has skyrocketed, and announced plans imply further huge increases in Federal Reserve assets and bank reserves. Nonetheless, the size of our balance sheet will not preclude our raising interest rates when that becomes appropriate for macroeconomic stability. Many of the liquidity programs are authorized only while circumstances in the economy and financial markets are “unusual and exigent,” and such programs will be terminated when conditions are no longer so adverse. Those programs and others have been designed to be unattractive in normal market conditions and will naturally wind down as markets improve.

All this is Central Banking 101; we have to rely on the Fed to execute the theory correctly – and this will be fodder for academic arguments for the next century.

Bloomberg notes that inflation concerns are driving down bill yields:

Rates on three-month bills turned negative in December for the first time since the government began selling them in 1929 as investors sacrificed returns to preserve principal. After increasing at the start of the year, rates have dropped 0.20 percentage point since the beginning of February to 0.13 percent on April 17.

Demand for bills is rising again because investors including foreign central banks are snapping up the shortest- term U.S. securities as the Federal Reserve buys Treasuries to drive down borrowing costs in a policy of so-called quantitative easing. China, the largest U.S. creditor, with $744 billion of debt, has questioned the practice and shifted purchases to bills from longer-maturity securities.

“There’s a group of investors out there who are looking at what the Fed is doing and the policy action they’ve taken and the asset purchases, and saying ultimately this is inflationary,” said Stuart Spodek, co-head of U.S. bonds in New York at BlackRock Inc., which manages $483 billion in debt. “You’re going to invest in very short-term bills because you absolutely need not just the quality but also the absolute liquidity.”

An alleged leak of the US bank stress tests has been touted on the Web but frankly, it doesn’t look too credible. We shall see!

Today’s excitement was the DBRS Mass Review-Negative of bank prefs; this was not released in time to have an effect on the market, but we will see what tomorrow brings.

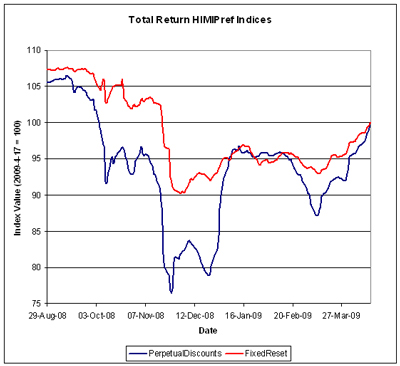

The PerpetualDiscount winning-streak came to an end today; sorry folks, that was my fault. I shouldn’t have posted about it after Friday’s gain. The market was well behaved, with few individual issues showing price changes of much note, on continued good volume.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0583 % |

955.0 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0583 % |

1,544.4 |

| Floater |

5.11 % |

5.13 % |

66,620 |

15.28 |

2 |

-0.0583 % |

1,193.1 |

| OpRet |

5.10 % |

4.44 % |

141,561 |

3.70 |

15 |

0.0322 % |

2,132.0 |

| SplitShare |

6.67 % |

8.82 % |

45,464 |

5.64 |

3 |

0.0000 % |

1,732.9 |

| Interest-Bearing |

6.15 % |

9.99 % |

26,637 |

0.67 |

1 |

-0.1025 % |

1,937.5 |

| Perpetual-Premium |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0150 % |

1,631.0 |

| Perpetual-Discount |

6.69 % |

6.80 % |

145,691 |

12.83 |

71 |

-0.0150 % |

1,502.1 |

| FixedReset |

5.93 % |

5.29 % |

681,946 |

7.63 |

35 |

0.0958 % |

1,900.6 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| BNA.PR.C |

SplitShare |

-2.21 % |

BAM Split has still not updated their NAV, so I’m still reporting the 1.7-:1 asset coverage figure from the February 28 NAV they do deign to provide.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2019-01-10

Maturity Price : 25.00

Evaluated at bid price : 12.82

Bid-YTW : 13.75 % |

| HSB.PR.D |

Perpetual-Discount |

-1.73 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 17.56

Evaluated at bid price : 17.56

Bid-YTW : 7.21 % |

| SLF.PR.C |

Perpetual-Discount |

-1.45 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 15.65

Evaluated at bid price : 15.65

Bid-YTW : 7.20 % |

| BNS.PR.M |

Perpetual-Discount |

-1.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 17.50

Evaluated at bid price : 17.50

Bid-YTW : 6.47 % |

| GWO.PR.I |

Perpetual-Discount |

-1.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 16.32

Evaluated at bid price : 16.32

Bid-YTW : 6.98 % |

| NA.PR.N |

FixedReset |

-1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 24.25

Evaluated at bid price : 24.31

Bid-YTW : 4.26 % |

| BAM.PR.J |

OpRet |

-1.02 % |

YTW SCENARIO

Maturity Type : Soft Maturity

Maturity Date : 2018-03-30

Maturity Price : 25.00

Evaluated at bid price : 21.38

Bid-YTW : 7.77 % |

| ENB.PR.A |

Perpetual-Discount |

1.07 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 24.26

Evaluated at bid price : 24.56

Bid-YTW : 5.67 % |

| RY.PR.H |

Perpetual-Discount |

1.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 22.84

Evaluated at bid price : 22.98

Bid-YTW : 6.26 % |

| PWF.PR.J |

OpRet |

1.18 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2010-05-30

Maturity Price : 25.50

Evaluated at bid price : 25.65

Bid-YTW : 3.97 % |

| NA.PR.K |

Perpetual-Discount |

1.41 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 21.55

Evaluated at bid price : 21.55

Bid-YTW : 6.81 % |

| TD.PR.O |

Perpetual-Discount |

1.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 19.18

Evaluated at bid price : 19.18

Bid-YTW : 6.36 % |

| BMO.PR.M |

FixedReset |

1.57 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 23.18

Evaluated at bid price : 23.26

Bid-YTW : 4.09 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| RY.PR.L |

FixedReset |

114,875 |

TD crossed 10,000 at 24.95; Nesbitt bought two blocks (13,900 & 10,000 shares) from National at 24.98; National crossed 30,000 at 24.99.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 24.85

Evaluated at bid price : 24.90

Bid-YTW : 4.84 % |

| RY.PR.D |

Perpetual-Discount |

75,370 |

Nesbitt bought 10,000 from TD at 17.98; Nesbitt crossed 28,000 at 18.00.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 18.00

Evaluated at bid price : 18.00

Bid-YTW : 6.38 % |

| MFC.PR.D |

FixedReset |

57,043 |

Desjardins crossed 15,700 at 25.66.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-07-19

Maturity Price : 25.00

Evaluated at bid price : 25.60

Bid-YTW : 6.29 % |

| RY.PR.X |

FixedReset |

50,326 |

Recent new issue.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-09-23

Maturity Price : 25.00

Evaluated at bid price : 25.80

Bid-YTW : 5.67 % |

| HSB.PR.E |

FixedReset |

50,274 |

Recent new issue.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-07-30

Maturity Price : 25.00

Evaluated at bid price : 25.43

Bid-YTW : 6.35 % |

| BNS.PR.M |

Perpetual-Discount |

44,625 |

Anonymous crossed (? Not necessarily the same anonymous on each side) 16,000 at 17.32.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-04-20

Maturity Price : 17.50

Evaluated at bid price : 17.50

Bid-YTW : 6.47 % |

| There were 37 other index-included issues trading in excess of 10,000 shares. |