BMO is buying AIG’s Canadian life insurance business. Nice to see the balance sheet of a Canadian bank being put to work.

Professor Axel Leijonhufvud has written a two part series on Vox (commencing yesterday) in which he concludes in part:

Two elements of a reconstructed system of regulatory control may be suggested.

First, re-impose effective reserve requirements on deposit-taking banks and extend them to all types of institutions that carry demand liabilities (e.g. money market funds).

Assiduous Readers will remember that I have called for bank-sponsored money market funds to be consolidated in their sponsors’ balance sheets for risk measurement purposes.

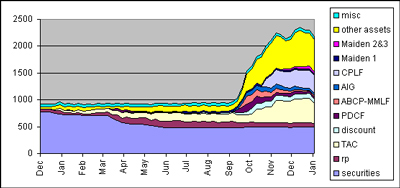

The ABCP soap-opera appears to be finally grinding to a resolution as the restructuring has received final approval. Investor Advocates will be pleased to learn that regulators now have judicial imprimatur to restrict investments even further:

Judge Campbell urged regulators to be more watchful about complicated products such as ABCP in the future.

He questioned whether investors and investment advisers “truly understood” what they were selling, and he went on to “urge regulators to sort out what investments should be available to whom.”

Soon only mutual funds will be legal for retail because, you know, you’re just not smart enough for anything else. The government says so, and they’re here to help you.

PerpetualDiscounts returned to their winning ways today.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 6.98 % | 7.60 % | 27,778 | 13.44 | 2 | -2.5076 % | 867.1 |

| FixedFloater | 7.31 % | 6.99 % | 152,508 | 13.76 | 8 | 0.4653 % | 1,402.1 |

| Floater | 5.43 % | 5.15 % | 35,822 | 15.27 | 4 | 0.2444 % | 1,123.6 |

| OpRet | 5.33 % | 4.76 % | 130,809 | 4.08 | 15 | 0.1401 % | 2,014.2 |

| SplitShare | 6.16 % | 9.85 % | 81,384 | 4.16 | 15 | 0.1221 % | 1,805.0 |

| Interest-Bearing | 7.19 % | 9.27 % | 42,872 | 0.92 | 2 | 0.2353 % | 1,967.8 |

| Perpetual-Premium | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.6360 % | 1,577.6 |

| Perpetual-Discount | 6.78 % | 6.83 % | 246,616 | 12.75 | 71 | 0.6360 % | 1,453.0 |

| FixedReset | 5.84 % | 4.85 % | 710,319 | 15.33 | 18 | 0.3165 % | 1,827.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BCE.PR.Y | Ratchet | -2.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 25.00 Evaluated at bid price : 14.12 Bid-YTW : 7.89 % |

| LBS.PR.A | SplitShare | -2.38 % | Asset coverage of 1.5-:1 as of January 8 according to Brompton Group. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2013-11-29 Maturity Price : 10.00 Evaluated at bid price : 8.20 Bid-YTW : 10.08 % |

| BCE.PR.S | Ratchet | -2.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 25.00 Evaluated at bid price : 14.65 Bid-YTW : 7.60 % |

| ALB.PR.A | SplitShare | -2.30 % | Asset coverage of 1.3-:1 as of January 8 according to Scotia Managed Companies. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2011-02-28 Maturity Price : 25.00 Evaluated at bid price : 20.77 Bid-YTW : 14.09 % |

| BAM.PR.G | FixedFloater | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 25.00 Evaluated at bid price : 10.50 Bid-YTW : 10.61 % |

| FFN.PR.A | SplitShare | -2.00 % | Asset coverage of 1.2+:1 as of December 31 according to the company. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2014-12-01 Maturity Price : 10.00 Evaluated at bid price : 7.85 Bid-YTW : 10.34 % |

| BNA.PR.C | SplitShare | -1.66 % | Asset coverage of 1.8+:1 as of December 31 according to the company. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 10.69 Bid-YTW : 16.34 % |

| BCE.PR.Z | FixedFloater | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 25.00 Evaluated at bid price : 15.26 Bid-YTW : 7.48 % |

| BCE.PR.F | FixedFloater | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 25.00 Evaluated at bid price : 15.52 Bid-YTW : 6.44 % |

| BMO.PR.H | Perpetual-Discount | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 20.01 Evaluated at bid price : 20.01 Bid-YTW : 6.75 % |

| SLF.PR.C | Perpetual-Discount | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 15.71 Evaluated at bid price : 15.71 Bid-YTW : 7.17 % |

| GWO.PR.J | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 24.31 Evaluated at bid price : 24.36 Bid-YTW : 5.36 % |

| DFN.PR.A | SplitShare | -1.14 % | Asset coverage of 1.7-:1 as of December 31 according to the company. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2014-12-01 Maturity Price : 10.00 Evaluated at bid price : 8.65 Bid-YTW : 8.30 % |

| BCE.PR.I | FixedFloater | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 25.00 Evaluated at bid price : 16.48 Bid-YTW : 6.85 % |

| PWF.PR.K | Perpetual-Discount | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 17.86 Evaluated at bid price : 17.86 Bid-YTW : 6.96 % |

| TD.PR.S | FixedReset | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 23.76 Evaluated at bid price : 23.82 Bid-YTW : 3.90 % |

| MFC.PR.C | Perpetual-Discount | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 17.11 Evaluated at bid price : 17.11 Bid-YTW : 6.67 % |

| BNS.PR.O | Perpetual-Discount | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 21.24 Evaluated at bid price : 21.52 Bid-YTW : 6.52 % |

| TD.PR.O | Perpetual-Discount | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 19.17 Evaluated at bid price : 19.17 Bid-YTW : 6.35 % |

| MFC.PR.B | Perpetual-Discount | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 18.24 Evaluated at bid price : 18.24 Bid-YTW : 6.46 % |

| PWF.PR.E | Perpetual-Discount | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 20.44 Evaluated at bid price : 20.44 Bid-YTW : 6.76 % |

| PWF.PR.H | Perpetual-Discount | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 7.01 % |

| BAM.PR.J | OpRet | 1.46 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2018-03-30 Maturity Price : 25.00 Evaluated at bid price : 17.40 Bid-YTW : 10.80 % |

| POW.PR.A | Perpetual-Discount | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 20.26 Evaluated at bid price : 20.26 Bid-YTW : 6.97 % |

| BNS.PR.K | Perpetual-Discount | 1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 18.86 Evaluated at bid price : 18.86 Bid-YTW : 6.39 % |

| PWF.PR.L | Perpetual-Discount | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 7.00 % |

| BCE.PR.C | FixedFloater | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 25.00 Evaluated at bid price : 16.21 Bid-YTW : 7.13 % |

| TD.PR.A | FixedReset | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 22.96 Evaluated at bid price : 23.00 Bid-YTW : 4.40 % |

| BCE.PR.A | FixedFloater | 1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 25.00 Evaluated at bid price : 17.19 Bid-YTW : 6.73 % |

| FBS.PR.B | SplitShare | 1.93 % | Asset coverage of 1.2-:1 as of January 8 according to TD Securities. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2011-12-15 Maturity Price : 10.00 Evaluated at bid price : 8.46 Bid-YTW : 11.32 % |

| POW.PR.D | Perpetual-Discount | 1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 18.35 Evaluated at bid price : 18.35 Bid-YTW : 6.87 % |

| BAM.PR.N | Perpetual-Discount | 1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 13.05 Evaluated at bid price : 13.05 Bid-YTW : 9.24 % |

| W.PR.H | Perpetual-Discount | 2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 18.36 Evaluated at bid price : 18.36 Bid-YTW : 7.56 % |

| POW.PR.C | Perpetual-Discount | 2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 21.29 Evaluated at bid price : 21.29 Bid-YTW : 6.87 % |

| BNS.PR.R | FixedReset | 2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 22.46 Evaluated at bid price : 22.50 Bid-YTW : 4.43 % |

| BNA.PR.A | SplitShare | 2.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2010-09-30 Maturity Price : 25.00 Evaluated at bid price : 22.51 Bid-YTW : 13.50 % |

| NA.PR.K | Perpetual-Discount | 2.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 20.95 Evaluated at bid price : 20.95 Bid-YTW : 6.99 % |

| NA.PR.M | Perpetual-Discount | 3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 21.78 Evaluated at bid price : 21.86 Bid-YTW : 6.87 % |

| TD.PR.Q | Perpetual-Discount | 3.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 21.88 Evaluated at bid price : 21.96 Bid-YTW : 6.40 % |

| ELF.PR.G | Perpetual-Discount | 3.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 7.99 % |

| BCE.PR.R | FixedFloater | 3.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 25.00 Evaluated at bid price : 16.04 Bid-YTW : 7.06 % |

| SBC.PR.A | SplitShare | 5.72 % | Asset coverage of 1.5+:1 as of January 8 according to Brompton Group. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2012-11-30 Maturity Price : 10.00 Evaluated at bid price : 8.50 Bid-YTW : 10.08 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| IGM.PR.A | OpRet | 168,991 | Scotia crossed 80,000 at 25.15; RBC bought 75,000 at 25.05 from anonymous. YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2013-06-29 Maturity Price : 25.00 Evaluated at bid price : 25.06 Bid-YTW : 5.78 % |

| GWO.PR.G | Perpetual-Discount | 124,550 | TD crossed 45,000 at 18.50, then another 58,700 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 18.42 Evaluated at bid price : 18.42 Bid-YTW : 7.14 % |

| BMO.PR.J | Perpetual-Discount | 64,650 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 17.01 Evaluated at bid price : 17.01 Bid-YTW : 6.74 % |

| CM.PR.J | Perpetual-Discount | 46,530 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-01-13 Maturity Price : 16.22 Evaluated at bid price : 16.22 Bid-YTW : 6.98 % |

| PPL.PR.A | SplitShare | 45,100 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2012-12-01 Maturity Price : 10.00 Evaluated at bid price : 9.00 Bid-YTW : 8.08 % |

| BAM.PR.O | OpRet | 33,027 | National crossed 14,500 at 17.98. YTW SCENARIO Maturity Type : Option Certainty Maturity Date : 2013-06-30 Maturity Price : 25.00 Evaluated at bid price : 17.92 Bid-YTW : 13.87 % |

| There were 36 other index-included issues trading in excess of 10,000 shares. | |||