I wouldn’t normally post on such a routine matter as dividend declarations, but having made an issue of the matter I will note that dividends for these issues have been declared.

ex-Date: 5/20

record-Date: 5/22

pay-Date: 6/7

I wouldn’t normally post on such a routine matter as dividend declarations, but having made an issue of the matter I will note that dividends for these issues have been declared.

ex-Date: 5/20

record-Date: 5/22

pay-Date: 6/7

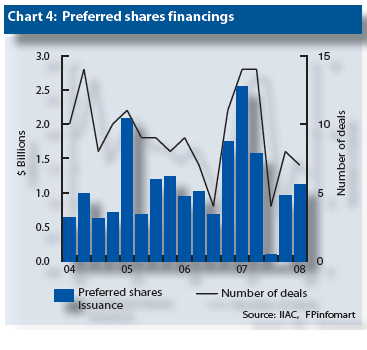

The IIAC has issued its 1Q08 Review of Equity New Issues and Trading, noting:

Preferred share issues were one of the brighter spots in the quarter – increasing by 17% from last quarter and raising $1.1 billion in capital on just seven offerings. This is attributed to financial institutions re-strengthening their capital base (Chart 4).

They report that the $1.1-billion in seven issues is down 56.5% by dollar value and 50% by number from 1Q07. I have previously suggested that heavy issuance in 1H07 was at least partly responsible for 2007’s horrible performance.

Hat tip: Streetwise Blog.

Ontario Superior Court Justice Colin Campbell had promised this week after two days of hearings to rule as soon as possible, but said in an endorsement issued Friday afternoon that he is not prepared to make a decision without further information.

…

“I am not satisfied that the release proposed as part of the plan, which is broad enough to encompass release from fraud, is in the circumstances of this case at this time properly authorized by the CCAA, or is necessarily fair and reasonable,” he wrote. “I simply do not have sufficient facts at this time on which to reach a conclusion one way or another.”The delay puts at risk the nine-month-long restructuring process, because banks that are backing the plan to swap the frozen notes for new bonds have said they will walk away without the releases.

But the judge said that if he lets the plan go ahead with the releases there’s a chance it will fall apart later because it may not “stand up to the scrutiny of being within the jurisdiction of the court within the CCAA.” Because of that, he wants the parties to come up with a solution for the fraud issue by May 30.

“In my view, within the spirit of the CCAA there is an urgent need for, and there can be a solution by which, the plan can be approved,” he wrote.

There’s a lot going on here that I don’t understand. If the Canadian banks are threatening to walk away without the release, what has the committee done to line up other banks? I was under the – possibly mistaken – impression that the advisor to the Committee, Morgan Stanley, was willing to backstop the lines all along. Surely, for a sufficient fee, a few major world banks would be willing to extend the required line of credit.

DBRS has announced:

has today confirmed the ratings on Great-West Lifeco (GWO or the Company) and its affiliated operating subsidiaries at current levels with Stable trends. The ratings on GWO are no longer Under Review with Developing Implications where they were placed on February 1, 2007 with the announcement that GWO was making a largely debt-financed US$3.9 billion acquisition of Putnam Investments Trust (Putnam).

Over the past year, the Company has made significant progress in reducing the debt incurred to acquire Putnam. Most notably, in November 2007, GWO announced the sale, which closed on April 1, of its U.S. health-care business with almost $1.6 billion in cash proceeds being made available to pay down outstanding credit facilities. In addition, the Company has also issued $1 billion of innovative subordinated debentures, the proceeds of which have been used to retire the bridge financing facilities. Giving some equity treatment to the hybrid subordinated debt issues, DBRS calculates a reported double leverage, pro forma the sale of the U.S. health care segment, which is not significantly higher than that of its peers. While Great-West Lifeco continues to be more aggressively capitalized than its peers at the holding company level, debt-service coverage remains adequate for the rating on a consolidated basis and on a cash flow basis at the holding company level. However, DBRS observes that the Company’s financial flexibility is currently impaired by relatively high financial leverage and the intense use of innovative debt instruments. Should financial leverage increase from current levels, the ratings on the Company are likely to come under downward pressure.

The existing ratings for the Company and its operating subsidiaries reflect the contribution from a diversified portfolio of businesses, including leading market shares across the Canadian insurance industry and attractive market niches in Europe, in the U.S. financial services market and in reinsurance. Although it accounts for a relatively small portion of the total earnings, Putnam should, in the long run, represent an attractive opportunity in the wealth management space given its entrenched distribution network of independent financial advisors, even though current market developments and lagging fund performance has recently reduced Putnam’s level of assets under management (AUM) and reduced prospects for an early recovery. DBRS believes that the Putnam acquisition has better strategic fit and is more complementary with the Company’s chosen strategy than the U.S. healthcare platform.

As an integral component of the Power Financial group of companies, the Company benefits from its parent’s implicit financial support and its strong governance and risk management controls and procedures.

The financing of the Putnam purchase has been previously discussed, as was the DBRS response to the purchase itself.

GWO has the following direct issues outstanding: GWO.PR.E, GWO.PR.F, GWO.PR.G, GWO.PR.H, GWO.PR.I & GWO.PR.X, all of which remain at Pfd-1(low). S&P has rated them P-1(low) all along.

Related issuers are POW, PWF & CL.

I’m becoming more and more convinced that the Credit Crunch has evolved from its fundamental role as Reducer of Excesses to a new position as Political Football.

My thoughts on this are influenced by many things. For instance, compare the sub-prime credit loss estimates of the Bank of England with those of the IMF. These estimates are, as has been noted, not just wildly at variance with each other, but prepared without even taking note of each other. For all my respect for these two institutions, this smacks of intellectual dishonesty – and in my book, there is no greater crime.

Quite frankly, I believe the methodology of the IMF report (which leaned heavily on the paper by Greenlaw et al.) to be deeply flawed; and not just deeply flawed but deliberately skewed. So why would the IMF adopt it? They have a lot of smart people on staff; I won’t be the only person in the world to have noticed the dicey bits; why was this methodology used holus-bolus instead of simply providing the top end of a range of estimates?

My hypothesis is that it’s simply politics. The two basic factions in the investment world are those who want lots of regulation to save us from the evil Bonfire of the Vanities and those who feel that over-regulation is simply promoting inefficiency of the capital markets. These opposing forces are not comprised exclusively of idealogically pure crusaders, either! In Canada, for instance, the banks can be counted upon to promote wise regulation, not too much, not too little …. as long as whatever happens favours capital markets players who have deep, deep pockets.

There will be members of both factions on staff at the IMF, and at any regulatory group or ultimately responsibile government. Sometimes you win, sometimes you lose, in general things proceed in an ultimately half-way reasonable manner, albeit with one step back for each two steps forward. Forecasting the effects of regulation is no easier than forecasting markets … and at least when you attempt to forecast the market you have a pretty good idea of your ultimate objective!

The hard-liners in either faction are never satisfied, however – and the more cynical players, taking whatever position best serves their business will always be looking for more. Thus, every development in the capital markets is carefully examined to determine its value as a weapon in the struggle.

Canadian ABCP? It’s been used to justify a call for higher pay for regulators, to justify calls for the OSFI to expand its mandate to ensure nobody ever loses money on anything and to justify a federal regulator. The Bank of Canada has brought forth some rules to ensure that the banks never again have to worry about competition in the ABCP market from snot-nosed small corporation scum.

And so it is with Bear Stearns. I wrote about the Econbrowser post yesterday. The Econbrowser piece wanted Bernanke (i.e., the Fed) to Do Something about leverage in the brokerage industry … which is not the Fed’s purview at all, it’s in the SEC’s bailiwick. There was a note from Dave Altig of the Atlanta Fed in the Econbrowser comments, drawing attention to the Fed’s preventative measures … and still, not a word about the SEC. You can find inumerable instances of hand-wringing on the web, bewailing the fact that the Fed is (sort-of) forced to backstop a system over which it has no direct supervisory function – although, as I have pointed out, separation of lending/monetary functions and bank supervision functions are more standard throughout the world than otherwise.

The more I think about it, the more convinced I am that most of the discussion of Bear Stearns has absolutely nothing to do with a genuine desire for better regulation (you want more margin and less leverage? OK, how much more margin and how much less leverage? Let’s discuss it!) and a lot more to do with a desire to change the identities of the regulators. It’s a world-wide bureaucratic turf fight; the credit crunch, sub-prime and Bear Stearns are merely the latest weapons of convenience.

For the record, my position at the moment is that supervisory responsibility for the brokerage sector should remain with the SEC. Assiduous Readers will by now be sick and tired of reading this, but I believe the brokerages should represent a riskier and less constrained layer surrounding a banking core in the financial system. If the Central Bank has supervisory functions, there will be both a higher degree of expectation of emergency assistance in times of stress and a higher probability as well, since staff at the Central Bank – however upright and angelic their characters – will be somewhat more inclined to double-down with assistance from the discount window than to admit a possible failure of regulation and let an insolvent firm go bankrupt.

I might work this up into a formal article at some point. Remember, you read it on PrefBlog first!

As remarked by Accrued Interest, now that reports are increasing that the credit crunch is over and companies might actually be able to pay back some money, there are also growing concerns that the money we get might not be worth very much:

Bernanke and San Francisco Fed President Janet Yellen, in separate speeches yesterday, said markets remain “far from normal” after some improvement since March. Yellen, Cleveland Fed President Sandra Pianalto, Kansas City Fed President Thomas Hoenig and the Dallas Fed’s Richard Fisher said they’re concerned about rising prices.

…

Yellen, 61, who doesn’t vote on rates this year, also said she anticipates consumer prices will moderate as the labor market weakens and “commodity prices level off.”The Fed can’t be “complacent about inflation,” she told the CFA Institute Annual Conference. Recent measures of price expectations “highlight the risk that our attempts to deal with problems in the real economy could lead to higher inflation expectations and an erosion of our credibility,” she said.

Fisher, speaking in Midland, Texas, said the U.S. may be in for a “prolonged” period of slow growth, which may end with faster-than-desirable inflation.

“How deep that slowdown will be is a question mark,” said Fisher, who voted against the last three rate cuts. “I am not sure it will be very deep at all, but it may be prolonged, because we have to correct the excesses of this credit crisis.”

Naked Capitalism notes a post by Willem Buiter, who burnishes his monetarist credentials:

In a fiat money world, central banks cause inflation, or, more precisely, only central banks are resposible for inflation. Other shocks, real and nominal, can influence the general price level if the central bank does not respond swiftly and determinedly, but these non-central bank-induced changes in the general price level can always be offset by the central bank, given enough time, freedom to act and courage.

But, in the medium and long term (at horizons of two years and over, say) central banks choose the average rate of inflation. Not globalisation; not indirect taxes; not bad harvests; not OPEC and the price of oil; not the Chinese and their exchange rate management. There is no oil inflation, food inflation or cost-push inflation. There is just inflation. Inflation may be accompanied by changes in key relative prices – in the real prices of oil, of food, of oil and of labour for instance – if other relative demand and supply shocks accompany the inflationary impulses created by the central bank. Large increases in the real price of food will be bad news to food importers (including most urban households) and good news to rural food producers and exporters. But don’t confuse it with inflation.

In the petty annoyances department, Andrew Willis discusses the Sprott IPO:

Brokers are using the “anonymous” function on the TSX to do much of their selling, with 1.5 million shares sold this way. Disguising orders by not disclosing the name of the brokerage house doing the transaction fits that segment of the hedge fund and dealer crowd that prefers to be discreet. Dealers are sensitive to the issue of flipping an IPO from a money manager who also counts as a major trading client.

Does Mr. Willis know or care that it would be grossly unethical for Sprott to allow annoyance with IPO selling to influence – in any way – its trading with client money?

From Prefblog’s Out-of-time-here’s-the-links Department:

Floaters finally had a bad day … they are now up a mere 8.26% on the month.

BNS issues did well:

| BNS Straight Perpetuals Prices & Performance 5/15 |

|||

| Issue | Bid | Yield | Day’s Return |

| BNS.PR.L | 20.70 | 5.49% | +0.7299% |

| BNS.PR.M | 20.80 | 5.46% | +1.2165% |

| BNS.PR.K | 21.91 | 5.53% | +0.7356% |

| BNS.PR.N | 24.01 | 5.51% | +1.7373% |

| BNS.PR.J | 24.42 | 5.34% | +1.2858% |

| BNS.PR.O | 25.12 | 5.61% | 0.0000% |

In general, volume dropped off a little, but it was a very strong day.

| Note that these indices are experimental; the absolute and relative daily values are expected to change in the final version. In this version, index values are based at 1,000.0 on 2006-6-30 | |||||||

| Index | Mean Current Yield (at bid) | Mean YTW | Mean Average Trading Value | Mean Mod Dur (YTW) | Issues | Day’s Perf. | Index Value |

| Ratchet | 4.83% | 4.86% | 48,893 | 15.81 | 1 | 0.0000% | 1,081.9 |

| Fixed-Floater | 4.67% | 4.61% | 63,642 | 16.08 | 7 | -0.0175% | 1,069.6 |

| Floater | 4.14% | 4.18% | 61,665 | 17.01 | 2 | -0.4926% | 911.7 |

| Op. Retract | 4.82% | 2.53% | 89,447 | 2.59 | 15 | +0.0724% | 1,055.7 |

| Split-Share | 5.26% | 5.55% | 70,913 | 4.15 | 13 | +0.0620% | 1,053.1 |

| Interest Bearing | 6.13% | 6.09% | 52,905 | 3.81 | 3 | 0.0000% | 1,105.5 |

| Perpetual-Premium | 5.88% | 5.10% | 139,428 | 4.38 | 9 | +0.1151% | 1,022.9 |

| Perpetual-Discount | 5.65% | 5.69% | 304,062 | 13.88 | 63 | +0.3378% | 926.0 |

| Major Price Changes | |||

| Issue | Index | Change | Notes |

| BAM.PR.B | Floater | -1.0345% | |

| WFS.PR.A | SplitShare | +1.1000% | Asset coverage of 1.8+:1 as of May 8, according to Mulvihill. Now with a pre-tax bid-YTW of 5.12% based on a bid of 10.11 and a hardMaturity 2011-6-30 at 10.00. |

| HSB.PR.D | PerpetualDiscount | +1.1416% | Now with a pre-tax bid-YTW of 5.73% based on a bid of 22.15 and a limitMaturity. |

| BNS.PR.M | PerpetualDiscount | +1.2165% | Now with a pre-tax bid-YTW of 5.46% based on a bid of 20.80 and a limitMaturity. |

| BNA.PR.C | SplitShare | +1.2500% | Asset coverage of just under 3.2:1 as of April 30, according to the company. The ex-date of the current dividend is not yet known. Now with a pre-tax bid-YTW of 6.57% based on a bid of 21.06 cum dividend and a hardMaturity 2019-1-10 at 25.00. |

| BNS.PR.J | PerpetualDiscount | +1.2858% | Now with a pre-tax bid-YTW of 5.34% based on a bid of 24.42 and a limitMaturity. |

| BNS.PR.N | PerpetualDiscount | +1.7373% | Now with a pre-tax bid-YTW of 5.51% based on a bid of 24.42 and a limitMaturity. |

| RY.PR.A | PerpetualDiscount | +2.3210% | Now with a pre-tax bid-YTW of 5.40% based on a bid of 20.72 and a limitMaturity. |

| Volume Highlights | |||

| Issue | Index | Volume | Notes |

| FTS.PR.E | Scraps (Would be OpRet, but there are credit concerns) | 200,000 | CIBC crossed two lots of 100,000 shares each at 25.45. Now with a pre-tax bid-YTW of 4.67% based on a bid of 25.38 and a softMaturity 2016-8-31 at 25.00. |

| SLF.PR.B | PerpetualDiscount | 198,300 | Nesbitt bought 77,100 from National Bank at 21.90, TD crossed 50,000 at 21.91, then TD crossed another 40,000 at 21.91. Now with a pre-tax bid-YTW of 5.56% based on a bid of 21.90 and a limitMaturity. |

| TD.PR.P | PerpetualDiscount | 92,638 | CIBC crossed 35,000 at 24.25. Now with a pre-tax bid-YTW of 5.46% based on a bid of 24.20 and a limitMaturity. |

| BMO.PR.J | PerpetualDiscount | 64,995 | Now with a pre-tax bid-YTW of 5.60% based on a bid of 20.13 and a limitMaturity. |

| BMO.PR.K | PerpetualDiscount | 58,235 | Now with a pre-tax bid-YTW of 5.73% based on a bid of 23.00 and a limitMaturity. |

| GWO.PR.I | PerpetualDiscount | 54,725 | Desjardins crossed 15,000 at 20.85, then Nesbitt crossed 30,000 at 21.00. Now with a pre-tax bid-YTW of 5.47% based on a bid of 20.86 and a limitMaturity. |

There were nineteen other index-included $25-pv-equivalent issues trading over 10,000 shares today.

R Split III Corp, which recently had its rating confirmed at Pfd-2(low) by DBRS, has announced:

that it has called 2,032 Preferred Shares for cash redemption on May 30, 2008 (in accordance with the Company’s Articles) representing approximately 0.090% of the outstanding Preferred Shares as a result of the special annual retraction of 16,444 Capital Shares by the holders thereof. The Preferred Shares shall be redeemed on a pro rata basis, so that each holder of Preferred Shares of record on May 29, 2008 will have approximately 0.090% of their Preferred Shares redeemed. The redemption price for the Preferred Shares will be $29.22 per share.

Holders of Preferred Shares that are on record for dividends but have been called for redemption will be entitled to receive dividends thereon which have been declared but remain unpaid up to but not including May 30, 2008.

Payment of the amount due to holders of Preferred Shares will be made by the Company on May 30, 2008. From and after May 30, 2008 the holders of Preferred Shares that have been called for redemption will not be entitled to dividends or to exercise any rights in respect of such shares except to receive the amount due on redemption.

0.09%? So if you own 10,000 shares, 9 of them will be called? It’s certainly not the company’s fault, but this is more of a nuisance than anything else!

Fitch Ratings has released a Special Report: Subprime Mortgage-Related Losses – A Moving Target which endorses the relatively high loss estimates of Greenlaw et al. and the IMF and contradicts the Bank of England Estimate.

Fitch, bless ’em, explicitly states that their calculation is restricted to the USD 1.4-trillion-odd of securitized subprime mortgage assets – one problem in drawing up comparable figures is determining whether the asset universes are comparable. Europe also went nuts over real-estate, particularly Spain and the UK!

Given the size of the subprime market, estimated to have originated as much as USD1.4trn of loans in the last three years (2005: USD625bn; 2006: USD600bn; and 2007: USD179bn), the poor underwriting standards deployed in originating these loans and the deteriorating economic environment, Fitch estimates total losses for the market to be in the region of USD400bn. Alternative methods of calculating the potential losses using index prices suggest potentially higher losses up to a high of USD550bn.

This compares with Greenlaw et al. (USD 400-billion); the IMF (USD 565-billion) [“Aggregate losses are on the order of $565 billion for U.S. residential loans (nonprime and prime) and securities and $240 billion on commercial real estate securities.”]; and the BoE (USD 170-billion by credit analysis vs. USD 381-billion by market price vs USD USD 317-billion by model-estimated credit-component of market price).

Of great interest to investors will be Fitch’s related conclusion that, notwithstanding that their estimate is on the low side of their mark-to-market range:

- Approximately 50% of total subprime mortgage related losses, totalling USD200bn, are estimated to reside within the banking sector. The balance 50% of losses is distributed among financial guarantors, insurance companies, asset managers and hedge funds. To the extent that institutions have effectively

hedged their exposures with financially sound counterparties, these loss estimates may be over‐estimated. However, in the absence of detailed disclosures, it is difficult to get an accurate estimate of net losses.- Reported losses by banks at USD165.3bn indicate that over 80% of losses stemming from ABS‐CDO and subprime RMBS exposures have been disclosed.

- As a significant proportion of the losses have been disclosed, further ratings action arising from ABS‐CDO and subprime RMBS exposures is likely to be minimal.

It’s a good paper, with a fair amount of detail provided regarding how they calculated their numbers.

Update: As noted on March 11, Fitch is very proud of how tough they are on subprime:

The full Bloomberg story explains the Fitch discrepency a little better:

“We have built in 20 percent more home price declines from the end of ’07,” said Glenn Costello, managing director for residential mortgage-backed securities at Fitch. “When you build in that much home price decline, I feel good when I pick up the paper and I see that home prices are only down another 3 percent. My ratings are still good.”

The BoC Review for Spring 2008 is now available, comprised of three articles:

I regret that I am not much interested in Foreign Exchange, but the third article, reporting on a Financial Stability conference, is most interesting. Most of the papers presented are available on the BoC website and I’ll be working through them – slowly! – in the course of the next few weeks.

Update, 2008-5-23: One paper discussed the previously reported Stress Testing on Australian Banks : Housing Implosion. I have updated that post.

Sorry, people! I spent most my reading time today looking at Leverage, Bear Stearns & Econbrowser, so there won’t be much commentary here.

The potential for repricing of the BCE / Teachers’ deal was discussed in the comments to May 12; now Desjardins is saying a repricing is more likely than not:

Joseph MacKay of Desjardins Securities says an agreement between Clear Channel and its private equity purchasers, which will reduce the takeout price by more than eight per cent, may put pressure on BCE to follow suit.

…

However, the chance of re-pricing the deal has also increased, MacKay wrote in a report.

…

“We would advise investors to assume a potential re-price in the five to 8.16 per cent range,” he wrote.

Accrued Interest is nonplussed by seemingly contradictory reports, but is sticking with his recessionary views.

Another good strong day in the market, with volume continuing to show signs of life. I note that PerpetualDiscounts are now up 0.98% month-to-date, while long corporates are up 0.91%.

| Note that these indices are experimental; the absolute and relative daily values are expected to change in the final version. In this version, index values are based at 1,000.0 on 2006-6-30 | |||||||

| Index | Mean Current Yield (at bid) | Mean YTW | Mean Average Trading Value | Mean Mod Dur (YTW) | Issues | Day’s Perf. | Index Value |

| Ratchet | 4.87% | 4.90% | 45,727 | 15.74 | 1 | -0.0806% | 1,081.9 |

| Fixed-Floater | 4.67% | 4.63% | 64,275 | 16.05 | 7 | +0.0060% | 1,069.8 |

| Floater | 4.12% | 4.16% | 62,061 | 17.05 | 2 | +0.5493% | 916.2 |

| Op. Retract | 4.83% | 2.57% | 89,700 | 2.59 | 15 | +0.1216% | 1,054.9 |

| Split-Share | 5.27% | 5.52% | 70,139 | 4.15 | 13 | +0.1432% | 1,052.4 |

| Interest Bearing | 6.13% | 6.08% | 53,116 | 3.82 | 3 | -0.0336% | 1,105.5 |

| Perpetual-Premium | 5.89% | 5.61% | 140,685 | 5.60 | 9 | +0.0178% | 1,021.8 |

| Perpetual-Discount | 5.67% | 5.71% | 304,127 | 13.98 | 63 | +0.1590% | 922.9 |

| Major Price Changes | |||

| Issue | Index | Change | Notes |

| LFE.PR.A | SplitShare | -1.0659% | Asset coverage of just under 2.5:1 as of April 30, according to the company. Now with a pre-tax bid-YTW of 4.79% based on a bid of 10.21 and a hardMaturity 2012-12-1 at 10.00. |

| DFN.PR.A | SplitShare | +1.0753% | Asset coverage of just under 2.5:1 as of April 30, according to the company. Now with a pre-tax bid-YTW of 4.70% based on a bid of 10.34 and a hardMaturity 2014-12-1 at 10.00. |

| BNA.PR.B | SplitShare | +1.4630% | Asset coverage of just under 3.2:1 as of April 30, according to the company. Timing of the current dividend is unclear. Now with a pre-tax bid-YTW of 7.55% based on a bid of 21.50 cum dividend and a hardMaturity 2016-3-25 at 25.00. Compare with BNA.PR.A (6.07% to 2010-9-30) and BNA.PR.C (6.73% to 2019-1-10). |

| CIU.PR.A | PerpetualDiscount | +1.6782% | Now with a pre-tax bid-YTW of 5.60% based on a bid of 20.60 and a limitMaturity. |

| BAM.PR.M | PerpetualDiscount | +2.6616% | Now with a pre-tax bid-YTW of 6.39% based on a bid of 18.90 and a limitMaturity. |

| Volume Highlights | |||

| Issue | Index | Volume | Notes |

| BNS.PR.M | PerpetualDiscount | 255,135 | Nesbitt crossed 208,600 at 20.55. Now with a pre-tax bid-YTW of 5.53% based on a bid of 20.55 and a limitMaturity. |

| PWF.PR.H | PerpetualDiscount | 211,900 | Now with a pre-tax bid-YTW of 5.78% based on a bid of 25.05 and a limitMaturity. |

| CM.PR.D | PerpetualDiscount | 204,047 | Now with a pre-tax bid-YTW of 5.89% based on a bid of 24.60 and a limitMaturity. |

| BAM.PR.N | PerpetualDiscount | 180,960 | Now with a pre-tax bid-YTW of 6.57% based on a bid of 18.38 and a limitMaturity. |

| NA.PR.K | PerpetualDiscount | 170,600 | Now with a pre-tax bid-YTW of 5.95% based on a bid of 24.70 and a limitMaturity. |

| BMO.PR.I | OpRet | 164,000 | TD crossed 59,300 at 25.10, then Nesbitt crossed 100,000 at the same price. Now with a pre-tax bid-YTW of -0.07% based on a bid of 25.06 and a call 2008-6-13 at 25.00. |

| POW.PR.D | PerpetualDiscount | 107,190 | Nesbitt crossed 100,000 at 21.85. Now with a pre-tax bid-YTW of 5.79% based on a bid of 21.80 and a limitMaturity. |

| BNS.PR.L | PerpetualDiscount | 105,500 | Nesbitt crossed 50,000 at 20.55, then TD crossed the same number at the same price. Now with a pre-tax bid-YTW of 5.53% based on a bid of 20.55 and a limitMaturity. |

There were twenty-seven other index-included $25-pv-equivalent issues trading over 10,000 shares today.

I’m not very happy with the Directors of BAM Split Corp..

The last dividend on their preferred shares went ex on February 20. They have not yet declared a current dividend, according to the Toronto Stock Exchange. This follows last year’s fiasco with the first BNA.PR.C dividend, an eMail sent on the weekend (not answered) and a voice mail message left today (not answered).

The company is sitting on client money of about $1.7-billion. This inattention to detail isn’t good enough, guys.