The Royal Bank of Canada has announced:

an inaugural Basel III-compliant domestic public offering of $200 million of Non-Cumulative, 5-Year Rate Reset Preferred Shares Series AZ.

Royal Bank of Canada will issue 8 million Preferred Shares Series AZ priced at $25 per share and holders will be entitled to receive a non-cumulative quarterly fixed dividend for the initial period ending May 24, 2014 in the amount of $0.3123 per share, to yield 4.00 per cent annually. The bank has granted the Underwriters an option, exercisable in whole or in part, to purchase up to an additional 2 million Preferred Shares Series AZ at the same offering price.

Subject to regulatory approval, on or after May 24, 2019, the bank may redeem the Preferred Shares Series AZ in whole or in part at par. Thereafter, the dividend rate will reset every five years at a rate equal to 2.21 per cent over the 5-year Government of Canada bond yield. Holders of Preferred Shares Series AZ will, subject to certain conditions, have the right to convert all or any part of their shares to Non-Cumulative Floating Rate Preferred Shares Series BA on May 24, 2019 and on May 24 every five years thereafter.

Holders of the Preferred Shares Series BA will be entitled to receive a non-cumulative quarterly floating dividend at a rate equal to the 3-month Government of Canada Treasury Bill yield plus 2.21 per cent. Holders of Preferred Shares Series BA will, subject to certain conditions, have the right to convert all or any part of their shares to Preferred Shares Series AZ on May 24, 2024 and on May 24 every five years thereafter.

The offering will be underwritten by a syndicate led by RBC Capital Markets. The expected closing date is January 30, 2014.

We routinely undertake funding transactions to maintain strong capital ratios and a cost effective capital structure. Net proceeds from this transaction will be used for general business purposes.

Sales were good! They later announced:

that as a result of strong investor demand for its previously announced domestic public offering of Non-Cumulative, 5-Year Rate Reset Preferred Shares Series AZ, the size of the offering has been increased to 20 million shares. The gross proceeds of the offering will now be $500 million. The offering will be underwritten by a syndicate led by RBC Capital Markets. The expected closing date is January 30, 2014.

We routinely undertake funding transactions to maintain strong capital ratios and a cost effective capital structure. Net proceeds from this transaction will be used for general business purposes.

As noted, the new issue is NVCC compliant. I have a term sheet that states:

Series AZ Preferred Share will be automatically and immediately converted, on a full and permanent basis, without the consent of the holder thereof, into the number of fully-paid and freely-tradable common shares of the Bank (“Common Shares”) determined in accordance with the Contingent Conversion Formula set out below (the “Contingent Conversion”).

“Trigger Event” has the meaning set out in the Office of the Superintendent of Financial Institutions Canada (“OSFI”) Guideline for Capital Adequacy Requirements (CAR), Chapter 2 ‒ Definition of Capital, effective January 2013, as such term may be amended or superseded by OSFI from time to time, which term currently provides that each of the following constitutes a Trigger Event:

(a) the Superintendent publicly announces that the Bank has been advised, in writing, that the Superintendent is of the opinion that the Bank has ceased, or is about to cease, to be viable and that, after the conversion of the Series AZ Preferred Shares and all other contingent instruments issued by the Bank and taking into account any other factors or circumstances that are considered relevant or appropriate, it is reasonably likely that the viability of the Bank will be restored or maintained; or

(b) a federal or provincial government in Canada publicly announces that the Bank has accepted or agreed to accept a capital injection, or equivalent support, from the federal government or any provincial government or political subdivision or agent or agency thereof without which the Bank would have been determined by the Superintendent to be non-viable.

The first step is the big gulp – the Superintendent has full discretion.

The “Contingent Conversion Formula” is: (Multiplier x Share Value) ÷ Conversion Price = number of Common Shares into which each Series AZ Preferred Share shall be converted.

The “Multiplier” is 1.0.

The “Share Value” of a Series AZ Preferred Share is $25.00 plus declared and unpaid dividends on such Series AZ Preferred Share.

The “Conversion Price” of each Series AZ Preferred Share is the greater of (i) a floor price of $5.00, and (ii) the Current Market Price of the Common Shares.

“Current Market Price” of the Common Shares means the volume weighted average trading price of the Common Shares on the Toronto Stock Exchange (the “TSX”), if such shares are then listed on the TSX, for the 10 consecutive trading days ending on the trading day preceding the date of the Trigger Event. If the Common Shares are not then listed on the TSX, for the purpose of the foregoing calculation reference shall be made to the principal securities exchange or market on which the Common Shares are then listed or quoted or, if no such trading prices are available, “Current Market Price” shall be the fair value of the Common Shares as reasonably determined by the board of directors of the Bank.

They’ve thought about prohibited owners:

The terms and conditions of the Series AZ Preferred Shares will include mechanics to permit holders of such shares that are prohibited pursuant to certain restrictions set out therein or pursuant to the Bank Act (Canada) from taking delivery of Common Shares issued upon a Trigger Event and to allow the Bank to attempt to facilitate a sale of such Common Shares on behalf of such persons. The net proceeds received from the Bank from the sale of any such Common Shares will be divided among the applicable persons in proportion to the number of Common Shares that would otherwise have been delivered to them upon the Contingent Conversion after deducting the costs of sale and any applicable withholding taxes.

For the official regulations governing NVCC, see the official Capital Adequacy Requirements.

Rated Pfd-2 by DBRS (emphasis added):

DBRS has today provisionally rated Royal Bank of Canada’s (the Bank or RBC) non-cumulative five-year rate reset first preferred shares, Series AZ (NVCC preferred shares Series AZ or Series AZ) at Pfd-2 with a Stable trend.

DBRS assigned the NVCC preferred shares Series AZ a rating equal to that Bank’s intrinsic assessment less four rating notches because the Series AZ has only an Office of the Superintendent of Financial Institutions (OSFI)-compliant non-viable contingent capital (NVCC) trigger, which is consistent with the OSFI requirements for NVCC instruments, and no additional triggers.

The rating is consistent with DBRS’s criteria, titled, “DBRS Criteria: Rating Bank Capital Securities – Subordinated, Hybrid, Preferred & Contingent Capital Securities.”

For more information on DBRS’s methodologies and criteria or the banking industry, visit www.dbrs.com or contact us at info@dbrs.com.

Rated P-2(high) by S&P (emphasis added):

Standard & Poor’s Ratings Services today said it assigned its ‘BBB+’ global scale and ‘P-2(High)’ Canada scale rating to Royal Bank of Canada’s (RBC) proposed tier 1 noncumulative five-year rate reset first preferred shares series AZ.

“In accordance with our criteria for hybrid capital instruments, the ratings reflect our analysis of the proposed instrument, and our assessment of RBC’s stand-alone credit profile of ‘a+’,” said Standard & Poor’s credit analyst Lidia Parfeniuk. (For more information, see “Bank Hybrid Capital Methodology And Assumptions,” published Nov. 1, 2011, on RatingsDirect).

The ‘BBB+’ rating stands three notches below the stand-alone credit profile (SACP), incorporating:

- •A deduction of two notches, the minimum downward notching from the SACP under our criteria for a bank hybrid capital instrument; and

- •The deduction of an additional notch to reflect that the preferred shares feature a contingent conversion trigger provision. Should a trigger event occur (as defined by The Office of the Superintendent of Financial Institutions’ [OSFI] guideline for Capital Adequacy Requirements, Chapter 2), each preferred share outstanding will automatically and immediately be converted, without the holder’s consent, into a number of fully paid and freely tradable common shares of the bank determined in accordance with a conversion formula.

…

Because we expect this instrument’s conversion to occur at or near the point of the banks’ nonviability, we view this mechanism as a nonviability trigger.We expect to assign “intermediate” equity content to these preferred shares, reflecting RBC’s full discretion to suspend dividends on the instrument.

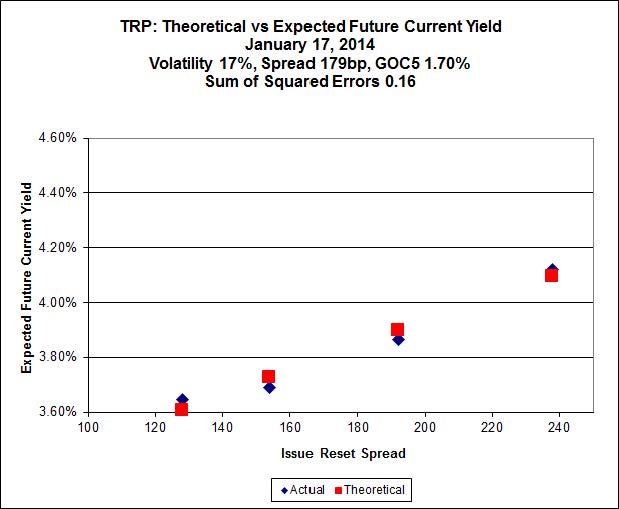

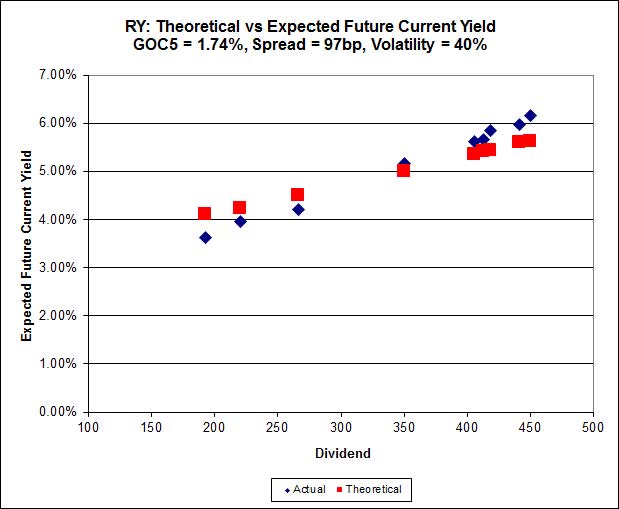

The pricing seems in line with the other RY FixedResets according to Implied Volatility theory, with the caveats that:

- The standard simplifying assumption that all options have three years until exercise date is wrong, and

- The calculated Implied Volatility is in excess of 40%, which means that Implied Volatility theory doesn’t really work, and

- The new issue is the only one of the set that is NVCC compliant.

Click for Big

The Break-Even Rate Shock for this issue (compared with RY.PR.W, which is NVCC-eligible) is 1.35%.