Fischer doesn’t want the Fed to trigger a global depression:

Federal Reserve Vice Chairman Stanley Fischer said policy makers will consider global growth as they begin to raise interest rates, and that they could increase them more gradually should the world economy falter.

“If foreign growth is weaker than anticipated, the consequences for the U.S. economy could lead the Fed to remove accommodation more slowly than otherwise,” Fischer said in a speech prepared for delivery Tuesday at Tel Aviv University.

The Fed will weigh how raising rates will affect other nations, said Fischer, 71, a former governor of the Bank of Israel. While tightening will probably will cause spillovers, the Fed is working to communicate policy changes clearly to smooth the transition, and emerging market economies are in better shape to endure the shift than in recent years, he said.

Meanwhile the all-important data seems to be strengthening the hands of Fed hawks:

U.S. stocks fell the most in three weeks, as better-than-forecast economic data and comments by Federal Reserve officials bolstered bets for an interest-rate increase this year.

…

A better-than-forecast increase in capital goods orders and new-home sales came after Federal Reserve Chair Janet Yellen indicated the central bank will raise borrowing costs this year if the economy improves as she expects. Fed Bank of Cleveland President Loretta Mester echoed her comments on Monday, saying the U.S. economy is close to the point where it can support higher rates.

But there’s always a counter-argument:

For years, the $12.6 trillion U.S. Treasury market has signaled — correctly — that the Federal Reserve was too optimistic in its outlook for the economy and interest rates.

That’s no different now even though policy makers have moved closer to how traders view the world, which is to say that it wouldn’t be surprising if the central bank failed to lift borrowing costs this year.

Despite the backup in yields in recent weeks, bond prices still signal the unexpected slowdown in the economy was more than just the result of some bad weather that kept Americans indoors and idled factories in the first quarter. Regardless of when the first increase comes, futures show traders don’t see rates exceeding 1 percent by the end of 2016, versus the Fed’s estimate of 1.875 percent.

I can’t say I’m very happy about Yellen’s deprecation of the Jackson Hole conference:

It turns out that being the first woman to head the Federal Reserve is not the only tradition Janet Yellen is breaking. The Fed said Tuesday that she plans on skipping this year’s gathering of the world’s central bankers at Jackson Hole, Wyoming.

…

The faithful attendance of Yellen’s three predecessors — Paul Volcker, Alan Greenspan and Ben Bernanke — made the conference sponsored by the Kansas City Federal Reserve Bank a widely sought invitation by central bankers from around the globe. Kansas City Fed officials said they would have no comment on Yellen’s decision.

There’s a rather opaque story on Bloomberg about corporate bonds – I think it’s just a little chatter about capturing new issue concessions:

However, one place where alpha can be generated is in the corporate bond market where big companies sell their debt. The reason is simple. When companies sell a new bond there is typically a lag between the bond being issued and when it’s included in benchmark fixed income indexes.

If the bonds perform well during that one month, then investment managers lucky enough to have purchased the debt have an immediate leg-up on the benchmark, or pure alpha.

Citigroup credit strategist Jason Shoup estimates that investors can add 20 basis points of alpha, as measured by annual excess returns, to their portfolios just by purchasing new-issue bonds. In a world of low and even negative interest rates, that is a not insignificant opportunity and it’s one that investors have been eager to take advantage of in recent years.

Click for Big

So my first thought is that it’s about capturing the new issue concession … the extra yield the issuers have to pay in order for investors to bother buying the issue. It is also possible that there is a duration effect – for instance, somebody investing in medium term bonds is restricted to 5-10 years maturity (maybe with some cheating) and new issues will tend to be at the top of that range. But it’s not clear!

Note that there is typically a new issue concession for Canadian preferred shares … but typically it’s the investors who pay it!

I don’t know if I can take much more of this. Yesterday a financial regulator did something useful; today, the Federal Conservatives have had a good idea:

Sorry, finding money to save for retirement remains strictly your problem. But choosing the right investments for your retirement savings would be radically simplified under the government’s proposal to allow people to voluntarily contribute additional money to the Canada Pension Plan beyond the required amounts.

Baffled by the choice of mutual funds, exchange-traded funds, closed-end funds, hedge funds, structured products, term deposits and individual stocks and bonds? Put some extra money into the CPP instead.

…

Mr. [Fred] Vettese [chief actuary at the benefits consulting firm Morneau Shepell] said voluntary extra payments would especially look good in comparison to investing in mainstream mutual funds, where the cost of ownership can run between 2 and 3 per cent. “My estimate would be that over a lifetime, the additional pension that people would be able to earn [through the voluntary CPP option] would be an extra 25 to 30 per cent on the same level of contributions.”

Yes, post-secondary education costs are going through the roof. And yes, I am highly indignant about this. But it’s an ill wind…:

Ivy League presidential pay is looking more like the big leagues.

Columbia University paid President Lee Bollinger $4.6 million in 2013, a 36 percent increase from the year before, according to a tax filing released Tuesday. Yale University recently revealed it paid former President Richard Levin a bonus of $8.5 million when he retired in 2013 after 20 years.

Presidential pay at elite universities is increasingly resembling that of corporate America, with performance bonuses and exit packages.

Another day, another slaughter, as us preferred share investors like to say! However it was, technically, a mixed day for the Canadian preferred share market, with PerpetualDiscounts off 23bp, FixedResets down 33bp and DeemedRetractibles gaining 7bp. A lengthy Performance Highlights table is dominated by losers. Volume was quite high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

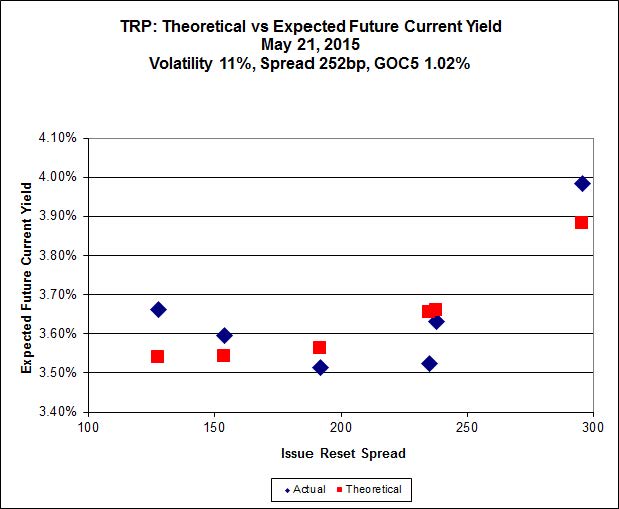

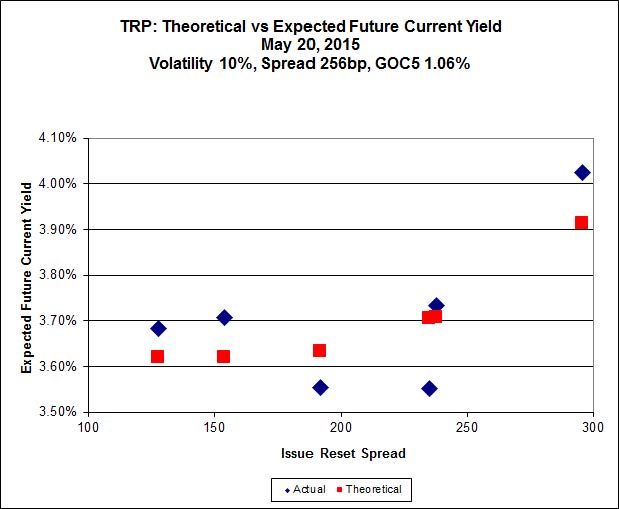

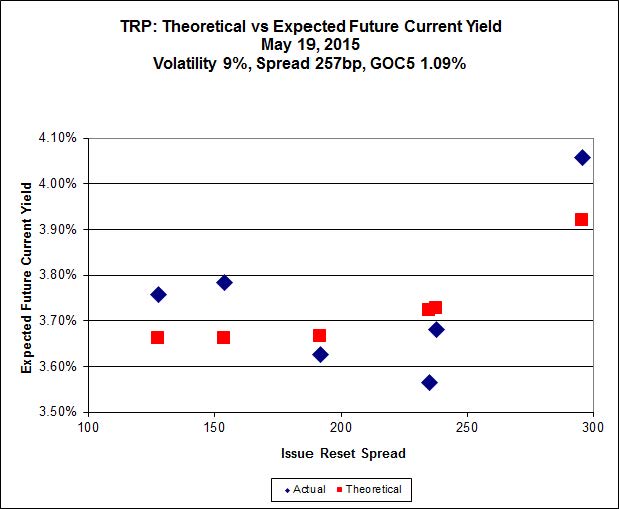

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.06 to be $1.02 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.85 cheap at its bid price of 24.90.

Click for Big

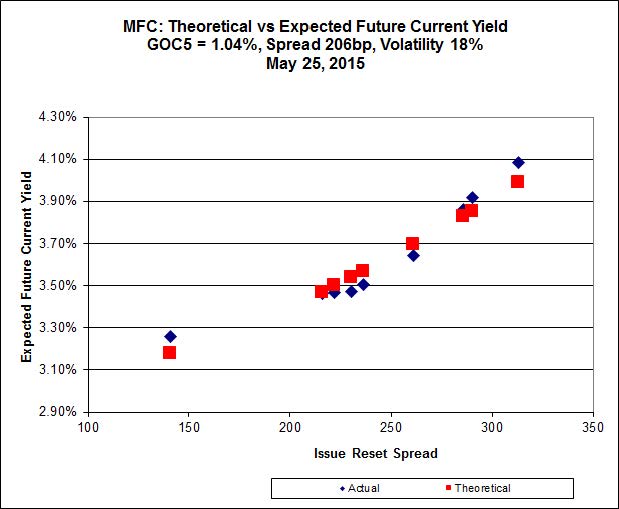

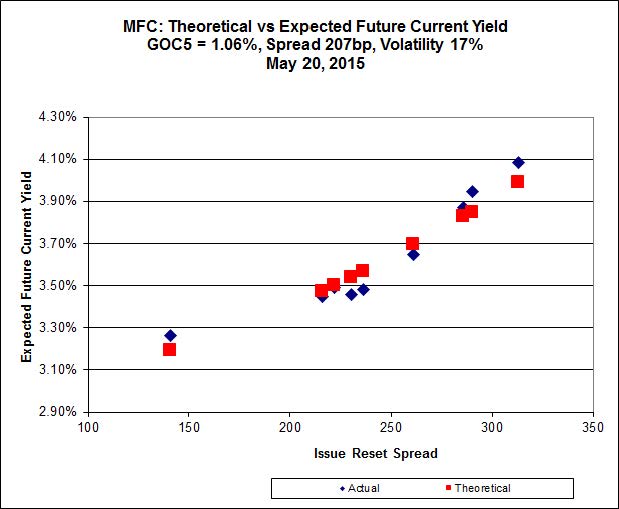

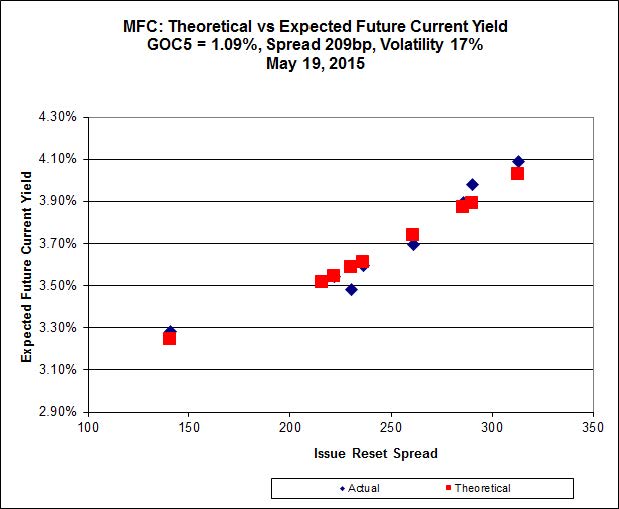

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.M, resetting at +236 on 2019-12-19, bid at 24.26 to be $0.51 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.05 to be $0.53 cheap.

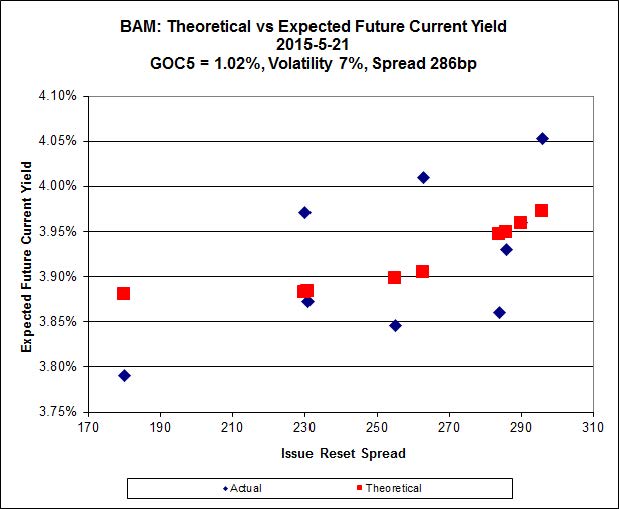

Click for Big

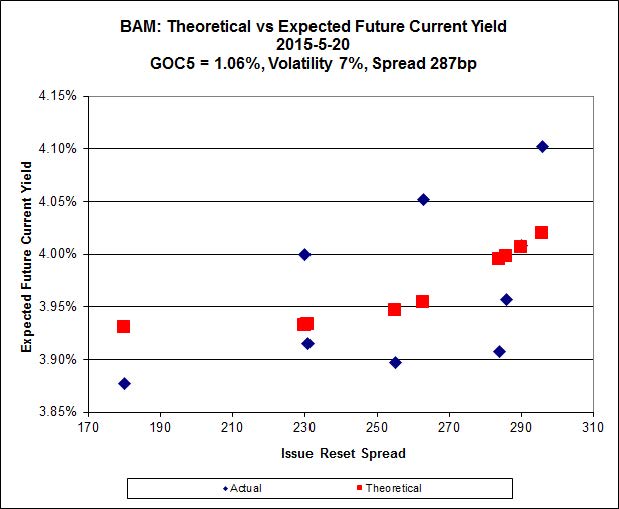

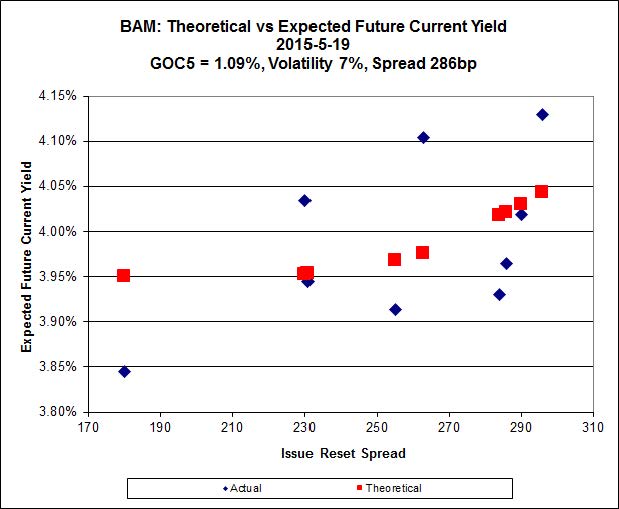

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.75 to be $0.46 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.65 and appears to be $0.43 rich.

Click for Big

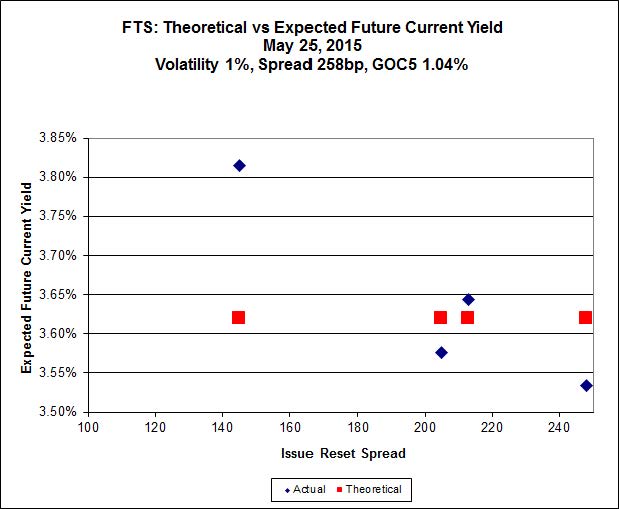

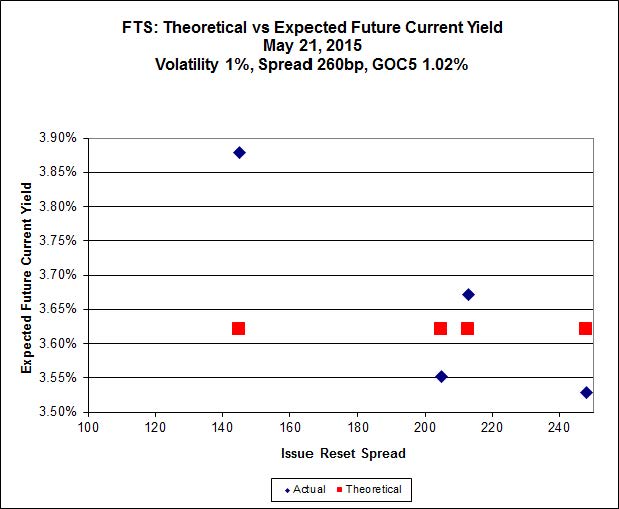

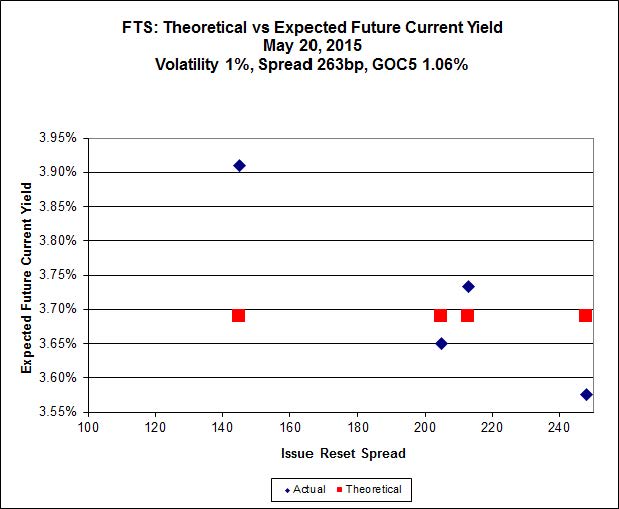

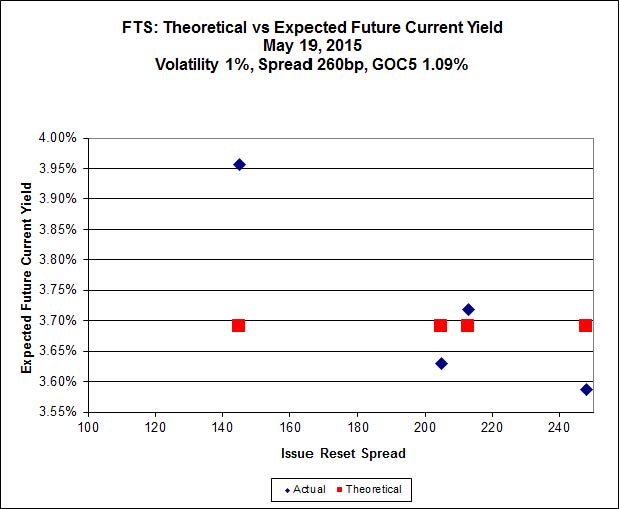

FTS.PR.H, with a spread of +145bp, and bid at 16.40, looks $0.76 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 21.77 and is $0.37 rich.

Click for Big

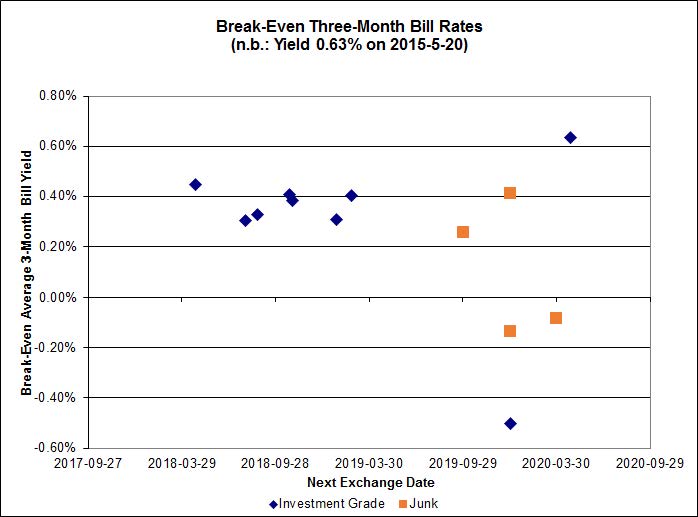

Investment-grade pairs predict an average over the next five-odd years of about 0.45%, including the TRP.PR.A / TRP.PR.F at -0.23%. On the junk side, the FFH.PR.E / FFH.PR.F pair is at -1.22%, while DC.PR.B / DC.PR.D is at -1.01.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.5762 % | 2,249.8 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.5762 % | 3,933.6 |

| Floater | 3.23 % | 3.42 % | 52,565 | 18.65 | 4 | -1.5762 % | 2,391.7 |

| OpRet | 4.45 % | -10.44 % | 30,931 | 0.10 | 2 | 0.0198 % | 2,780.2 |

| SplitShare | 4.60 % | 4.72 % | 65,593 | 3.34 | 3 | -0.0939 % | 3,241.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0198 % | 2,542.2 |

| Perpetual-Premium | 5.47 % | 2.92 % | 62,382 | 0.43 | 18 | 0.0197 % | 2,516.2 |

| Perpetual-Discount | 5.09 % | 5.04 % | 120,522 | 15.33 | 15 | -0.2300 % | 2,764.1 |

| FixedReset | 4.44 % | 3.76 % | 272,260 | 16.40 | 86 | -0.3268 % | 2,398.1 |

| Deemed-Retractible | 4.98 % | 3.44 % | 102,505 | 0.74 | 34 | 0.0680 % | 2,623.4 |

| FloatingReset | 2.55 % | 2.91 % | 58,102 | 6.15 | 7 | 0.0243 % | 2,340.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ENB.PF.G | FixedReset | -2.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 20.73 Evaluated at bid price : 20.73 Bid-YTW : 4.75 % |

| BAM.PR.K | Floater | -2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 14.45 Evaluated at bid price : 14.45 Bid-YTW : 3.48 % |

| SLF.PR.G | FixedReset | -2.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.55 Bid-YTW : 6.69 % |

| TRP.PR.B | FixedReset | -2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 15.72 Evaluated at bid price : 15.72 Bid-YTW : 3.76 % |

| BAM.PR.B | Floater | -1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 14.71 Evaluated at bid price : 14.71 Bid-YTW : 3.42 % |

| HSE.PR.A | FixedReset | -1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 16.87 Evaluated at bid price : 16.87 Bid-YTW : 4.29 % |

| ENB.PR.Y | FixedReset | -1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 18.74 Evaluated at bid price : 18.74 Bid-YTW : 4.77 % |

| ENB.PF.A | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 20.68 Evaluated at bid price : 20.68 Bid-YTW : 4.71 % |

| MFC.PR.F | FixedReset | -1.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.48 Bid-YTW : 6.28 % |

| BAM.PR.C | Floater | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 14.65 Evaluated at bid price : 14.65 Bid-YTW : 3.44 % |

| ENB.PF.C | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 20.71 Evaluated at bid price : 20.71 Bid-YTW : 4.69 % |

| ENB.PF.E | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 20.75 Evaluated at bid price : 20.75 Bid-YTW : 4.71 % |

| MFC.PR.N | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.75 Bid-YTW : 4.21 % |

| BAM.PF.D | Perpetual-Discount | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 22.55 Evaluated at bid price : 22.95 Bid-YTW : 5.40 % |

| TRP.PR.A | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 20.75 Evaluated at bid price : 20.75 Bid-YTW : 3.71 % |

| BAM.PF.G | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 23.03 Evaluated at bid price : 24.65 Bid-YTW : 4.05 % |

| BAM.PF.F | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 23.00 Evaluated at bid price : 24.42 Bid-YTW : 4.10 % |

| BAM.PR.M | Perpetual-Discount | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 21.85 Evaluated at bid price : 22.13 Bid-YTW : 5.44 % |

| TD.PF.B | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 22.88 Evaluated at bid price : 24.10 Bid-YTW : 3.48 % |

| BIP.PR.A | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 23.02 Evaluated at bid price : 24.61 Bid-YTW : 4.64 % |

| CM.PR.P | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 22.66 Evaluated at bid price : 23.70 Bid-YTW : 3.53 % |

| TD.PR.S | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.85 Bid-YTW : 3.16 % |

| FTS.PR.G | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 21.73 Evaluated at bid price : 22.00 Bid-YTW : 3.73 % |

| BAM.PR.T | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 21.31 Evaluated at bid price : 21.60 Bid-YTW : 4.05 % |

| FTS.PR.J | Perpetual-Discount | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 23.89 Evaluated at bid price : 24.30 Bid-YTW : 4.89 % |

| IAG.PR.A | Deemed-Retractible | 1.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.55 Bid-YTW : 5.51 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.E | FixedReset | 127,870 | TD crossed 50,000 at 25.05. Scotia crossed 40,000 at the same price; RBC crossed 18,000 at the same price again. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 23.13 Evaluated at bid price : 25.00 Bid-YTW : 3.76 % |

| FTS.PR.M | FixedReset | 96,330 | RBC crossed 71,900 at 24.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 23.10 Evaluated at bid price : 24.71 Bid-YTW : 3.59 % |

| FTS.PR.G | FixedReset | 91,359 | RBC crossed 75,000 at 22.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 21.73 Evaluated at bid price : 22.00 Bid-YTW : 3.73 % |

| ENB.PR.T | FixedReset | 90,999 | RBC crossed 50,000 at 19.35. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 19.26 Evaluated at bid price : 19.26 Bid-YTW : 4.76 % |

| BAM.PF.F | FixedReset | 85,779 | TD crossed 80,000 at 24.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 23.00 Evaluated at bid price : 24.42 Bid-YTW : 4.10 % |

| ENB.PR.F | FixedReset | 71,619 | TD crossed 50,000 at 19.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-26 Maturity Price : 19.26 Evaluated at bid price : 19.26 Bid-YTW : 4.74 % |

| There were 48 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.L | FixedReset | Quote: 23.10 – 23.88 Spot Rate : 0.7800 Average : 0.5524 YTW SCENARIO |

| HSE.PR.A | FixedReset | Quote: 16.87 – 17.43 Spot Rate : 0.5600 Average : 0.3851 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 23.75 – 24.42 Spot Rate : 0.6700 Average : 0.5094 YTW SCENARIO |

| TD.PF.C | FixedReset | Quote: 23.86 – 24.40 Spot Rate : 0.5400 Average : 0.4025 YTW SCENARIO |

| ENB.PF.G | FixedReset | Quote: 20.73 – 21.10 Spot Rate : 0.3700 Average : 0.2331 YTW SCENARIO |

| ENB.PR.D | FixedReset | Quote: 18.65 – 19.08 Spot Rate : 0.4300 Average : 0.2941 YTW SCENARIO |