As noted in MAPF Portfolio Composition: April 2015, the fund now has a large allocation to FixedResets, mostly of relatively low spread.

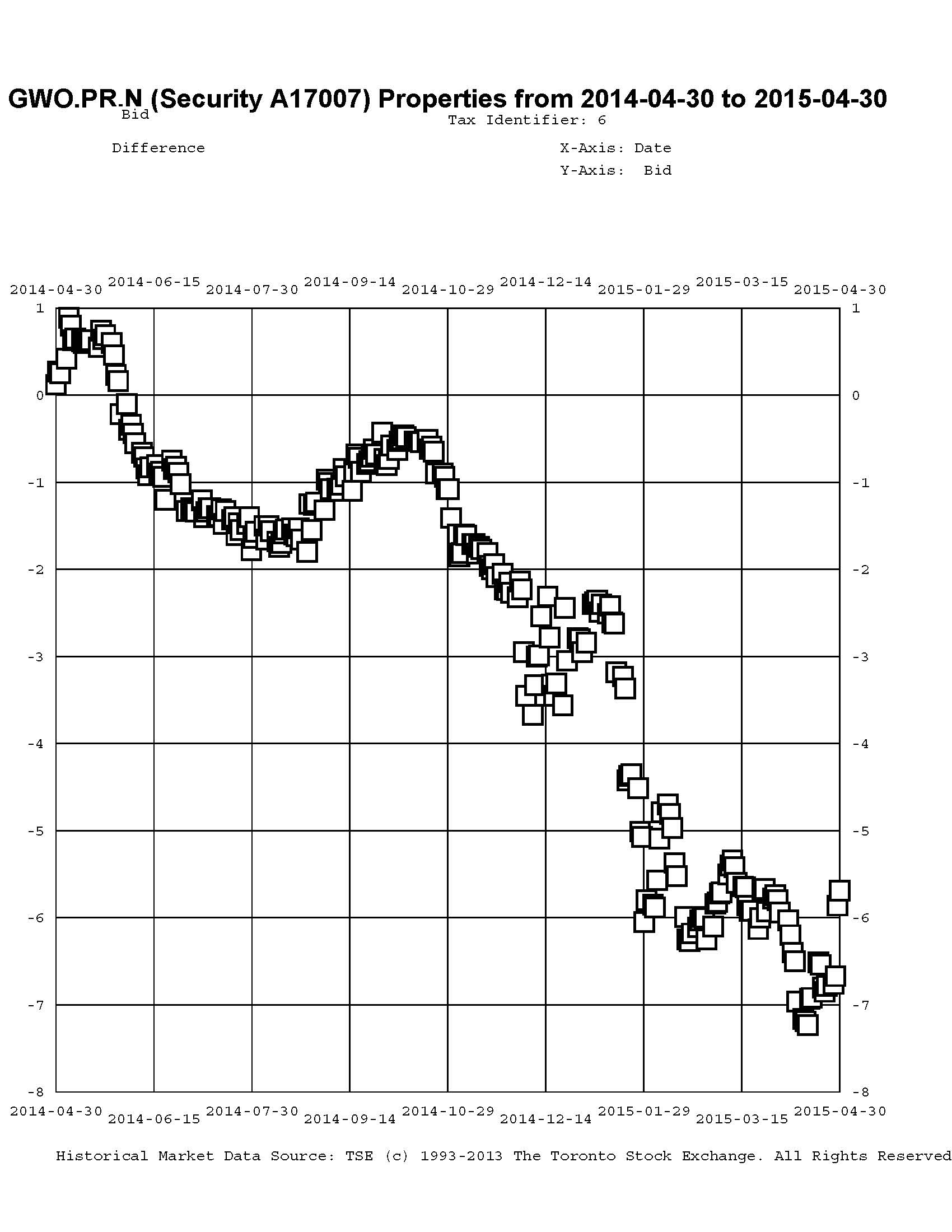

Many of these were largely purchased with proceeds of sales of DeemedRetractibles from the same issuer; it is interesting to look at the price trend of some of the Straight/FixedReset pairs. We’ll start with GWO.PR.N / GWO.PR.I; the fund sold the latter to buy the former at a takeout of about $1.00 in mid-June, 2014; relative prices over the past year are plotted as:

Click for Big

Given that the April month-end take-out was $5.69, this is clearly a trade that has not worked out very well.

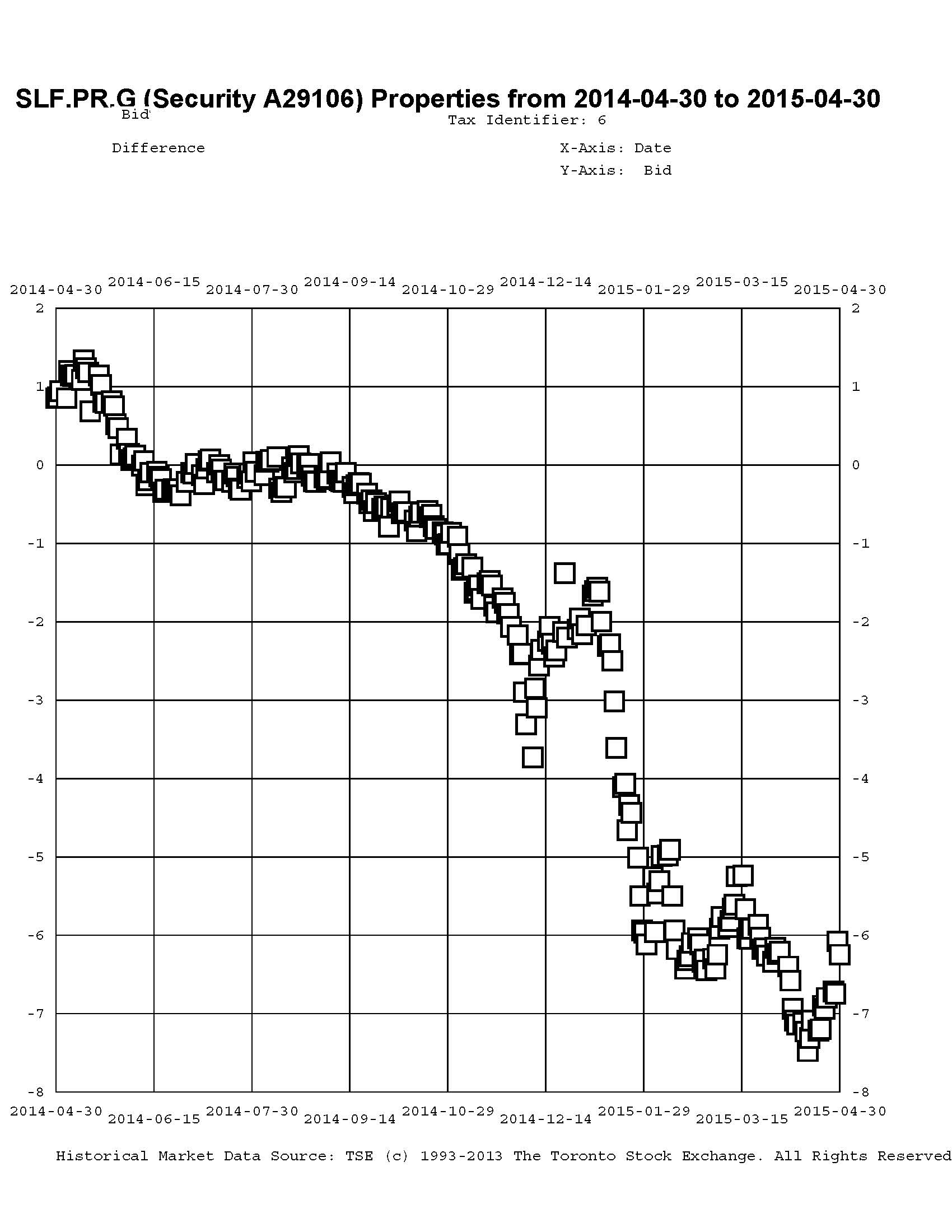

In July, 2014, I reported sales of SLF.PR.D to purchase SLF.PR.G at a take-out of about $0.15:

Click for Big

There were similar trades in August, 2014 (from SLF.PR.C) at a take-out of $0.35. The April month-end take-out (bid price SLF.PR.D less bid price SLF.PR.G) was $6.25, so that hasn’t worked very well either.

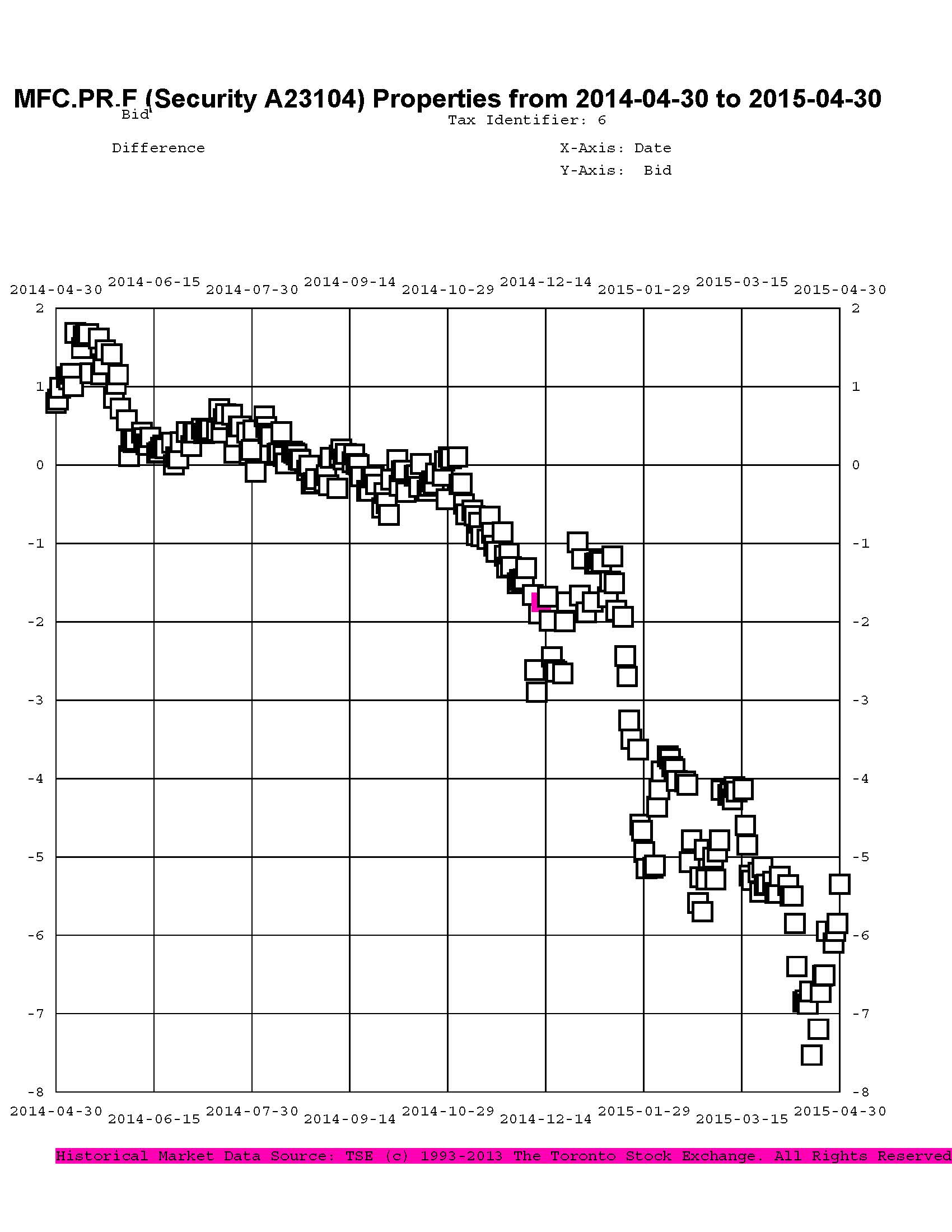

November saw the third insurer-based sector swap, as the fund sold MFC.PR.C to buy the FixedReset MFC.PR.F at a post-dividend-adjusted take-out of about $0.85 … given a February month-end take-out of about $5.29, that’s another regrettable trade, although another piece executed in December at a take-out of $1.57 has less badly.

Click for Big

This trend is not restricted to the insurance sector, which I expect will become subject to NVCC rules in the relatively near future and are thus subject to the same redemption assumptions I make for DeemedRetractibles. Other pairs of interest are BAM.PR.X / BAM.PR.N:

Click for Big

… and FTS.PR.H / FTS.PR.J:

Click for Big

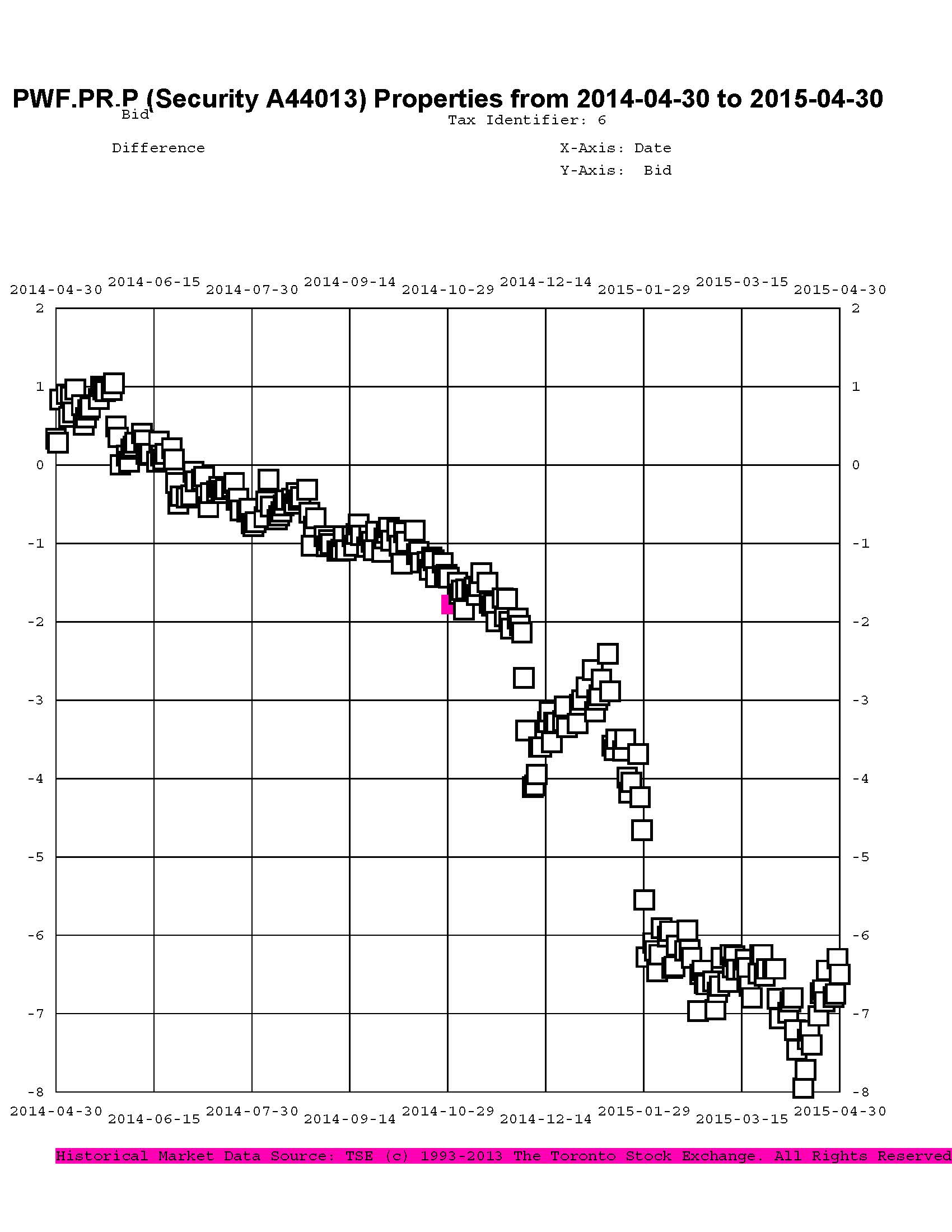

… and PWF.PR.P / PWF.PR.S:

Click for Big

I will agree that the fund’s trades highlighted in this post may be decried as cases of monumental bad timing, but I should point out that in May, 2014, the fund was 63.9% Straight / 9.5% FixedReset while in April 2015 the fund was 10% Straight / 85% FixedReset, FloatingReset and FixedFloater (The latter figures include allocations from those usually grouped as ‘Scraps’). Given that the indices are roughly 30% Straight / 60% FixedReset & FloatingReset, it is apparent that the fund was extremely overweighted in Straights / underweighted in FixedResets in May 2014 but this situation has now reversed. HIMIPref™ analytics have been heavily favouring low-spread issues and the fund’s holdings are overwhelmingly of this type.

Summarizing the charts above in tabular form, we see:

| FixedReset | Straight | Take-out December 2013 |

Take-out MAPF Trade |

Take-out December 2014 |

Take-out March 2015 | Take-out April 2015 |

| GWO.PR.N 3.65%+130 |

GWO.PR.I 4.5% |

($0.04) | $1.00 | $2.95 | $5.74 | $5.69 |

| SLF.PR.G 4.35%+141 |

SLF.PR.D 4.45% |

($1.29) | $0.25 | $2.16 | $6.16 | $6.25 |

| MFC.PR.F 4.20%+141 |

MFC.PR.C 4.50% |

($1.29) | $0.86 | $1.20 | $5.46 | $5.35 |

| BAM.PR.X 4.60%+180 |

BAM.PR.N 4.75% |

($2.06) | $0.17 | $4.76 | $4.18 | |

| FTS.PR.H 4.25%+145 |

FTS.PR.J 4.75% |

$0.60 | $5.68 | $8.86 | $8.07 | |

| PWF.PR.P 4.40%+160 |

PWF.PR.S 4.80% |

($0.67) | $3.00 | $6.43 | $6.50 | |

| The ‘Take-Out’ is the bid price of the Straight less the bid price of the FixedReset; approximate execution prices are used for the “MAPF Trade” column. Bracketted figures in the ‘Take-Out’ columns indicate a ‘Pay-Up’ | ||||||

There was not much change from March month-end to April month-end, although the charts show some great excitement in mid-March, with spreads widening dramatically. The following chart shows the normalized total return of the HIMIPref™ FixedReset index through the month:

Click for Big

So why is all this happening? One should take care in explaining market movements, but it is my belief that in the latter half of 2013 we were dealing with the ‘taper tantrum’ – the market’s fears that Fed tapering and subsequent tapering would lead to massive spikes in yields; this led to a great preference for FixedResets over Straights. Now, with the economic news getting less inflationary with every news story and Europe and Japan desperately trying to reflate their sluggish economies, the market seems to think that these rate increases are still a long way off … leading to a great preference for Straights over FixedResets.

In addition, the graphs show a sharp spike in early December, during which the low-spread FixedResets were very badly hurt; I believe this to be due to a combination of tax-loss selling and a panicky response to the 29% reduction in the TRP.PR.A dividend.

And in January it just got worse with Canada yields plummeting after the Bank of Canada rate cut with speculation rife about future cuts although this slowly died away.

And in late March / early April it got worse again, with one commenter attributing at least some of the blame to the John Heinzl piece in which I pointed out the expected reduction in dividend payouts! Insofar as I am willing to guess what motivates ‘the market’, I will guess that the rally in the latter half of April is due to a feeling that the previously scheduled European deflation has been cancelled, which in turn encouraged an increase in Treasury yields which fed through to the Canadian market.

There was some good discussion about the declining phase in the comments to the January 29 market action report. I take the view that we’ve seen this show before: during the Credit Crunch, Floaters got hit extremely badly (to the point at which their fifteen year total return was negative) because (as far as I can make out) their dividend rate was dropping (as it was linked to Prime) while the yields on other perpetual preferred instruments were skyrocketing (due to credit concerns). Thus, at least some investors insisted on getting long term corporate yields from rates based (indirectly and with a lag, in the case of FixedResets) on short-term government policy rates. And it’s happening again!

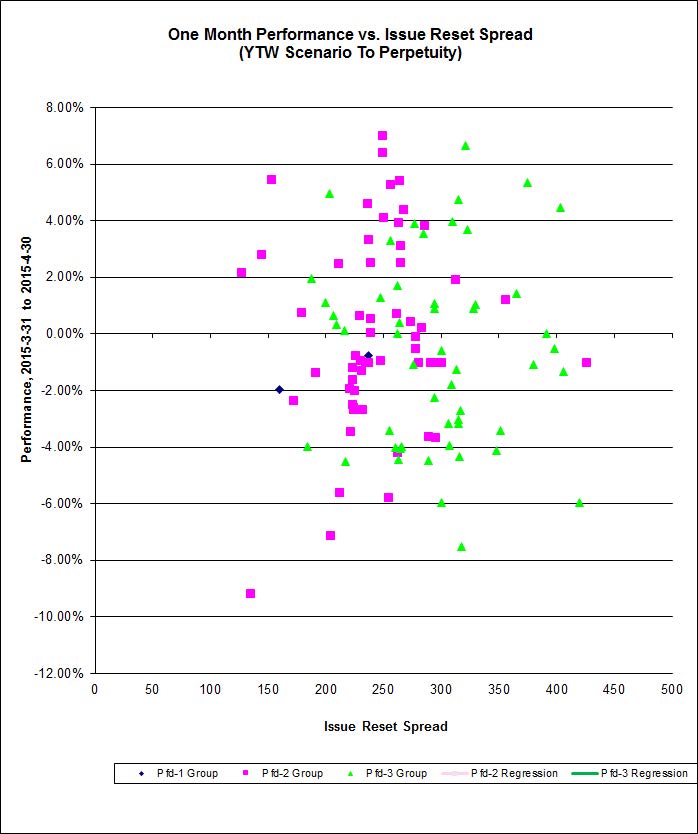

Here’s the April performance for FixedResets that had a YTW Scenario of ‘To Perptuity’ at mid-month.:

Click for Big

The end-of-month rally has been rather disorderly; correlations between Issue Reset Spread and monthly performance for April are basically zero.

“I take the view that we’ve seen this show before: during the Credit Crunch, Floaters got hit extremely badly”

During the Credit Crunch US fixed income was also hit “extremely badly”. This time US floaters and US fixed-to-floaters have been doing just fine — the preferred shares market irrationality has been entirely limited to Canada. The spread between US 5Yr and CA 5Yr did widen from 0.2% to 0.8% in early 2015 (and is now back down to 0.45%). It was logical for this to cause a reasonable drop in variable rate Canadian preferred shares, but not a market route. Even after their rally in the last couple of weeks, I believe that low spread FixedResets are still selling at a remarkable discount to their value relative to other fixed income instruments worldwide.

Thanks for the international angle! There is at least some feeling in Canada that the only uncertainty with preferreds is how you’re going to lose your money:

Worth quoting the next post:

The above was written on April 17, 2015: it may prove to be pretty close to the bottom.

all i have to say, is Thank You James, for your daily posts, and monthly newsletter. it’s been invaluable to me in navigating the world of Preferred shares.

Hi there. I have enjoyed all of your posts and wonderful wisdom in prefs.

I own fortis pref series h. With the reset coming, I would assume your recommendation in this market would be to convert to the floating series I?

You have commented about moving from the fixed to the resets, but limited comments about your position on the reset dates.

Considering your extensive knowledge, I would love to hear your opinion.

I’ve given a preliminary opinion on FTS.PR.H / FTS.PR.I, but a final recommendation won’t be made until closer to the notification deadline.

Market conditions have generally been such that FloatingResets are expected to trade at lower prices than their FixedReset siblings. However, in December, 2014, with fears of hyperinflation roiling the markets, I recommended conversion of AZP.PR.B, TRP.PR.A & FFH.PR.C.

Note that these recommendations do not incorporate my views likely five-year averages of three-month bill rates; it is quite reasonable to do one thing with the company and immediately do the other thing in the market; which – assuming there are no big changes in the market in the interim – will allow a small trading profit.