Singapore is being affected by low growth in Asia:

Singapore’s central bank eased monetary policy for the second time this year as the economy narrowly avoided a technical recession, saying weakening prospects for global growth will pose “headwinds” in the coming months.

The Monetary Authority of Singapore, which uses the currency rather than interest rates as its main policy tool, said Wednesday it will reduce “slightly” the pace of appreciation in the local dollar versus those of its trading partners. Gross domestic product unexpectedly rose an annualized 0.1 percent in the three months through September from the previous quarter, when it shrank a revised 2.5 percent, the trade ministry said in a separate statement.

“The Singapore economy is projected to expand at a modest pace in 2015 and 2016, with growth slightly weaker than earlier envisaged,” the central bank said. “The subdued global growth will exert a drag on the external-oriented sectors in Singapore in the quarters ahead.”

On a brighter note, today we learned what millennials do at the office all day, which has heretofore been very mysterious:

Last year, Playboy.com cleaned up its website to make it “safe for work,” and has since seen its monthly unique Web visitors rise fivefold. The median age of those visitors dropped to 30 years-old from 47 as a result — “an attractive demographic for advertisers,” the company said.

Of all the do-gooder strategies ever devised, there has never been anything as cruel as income-geared pricing. This mechanism traps the poor inextricably in their circumstances, since any incremental improvements they can make to income – by getting a slightly better job, or by working slightly more hours – will immediately be taxed away by reduction of benefits. So, naturally, guess what Toronto City Council is plotting?

As the TTC board contemplates another New Year’s fare increase — the seventh in as many years — there’s growing concern that the rising cost of transportation is eating through the empty pockets of its neediest riders at a disproportionate rate.

Many cities offer an income-based concession pass. Is it time for Toronto to do the same?

Still, it was nice to see Canadian preferred share investors waving the flag today:

Click for Big

It was a hideous day for the Canadian preferred share market, with PerpetualDiscounts off 27bp, FixedResets losing a stunning 186bp and DeemedRetractibles down 31bp. An extraordinarily long Performance Highlights table is dominated by losing FixedResets, as might be expected. Volume was extremely high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

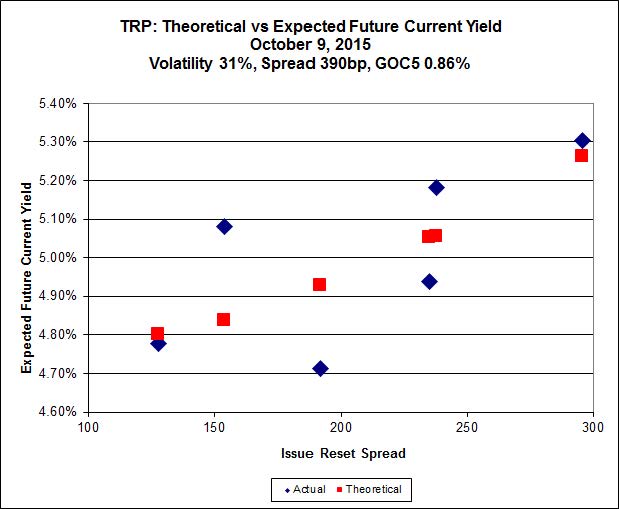

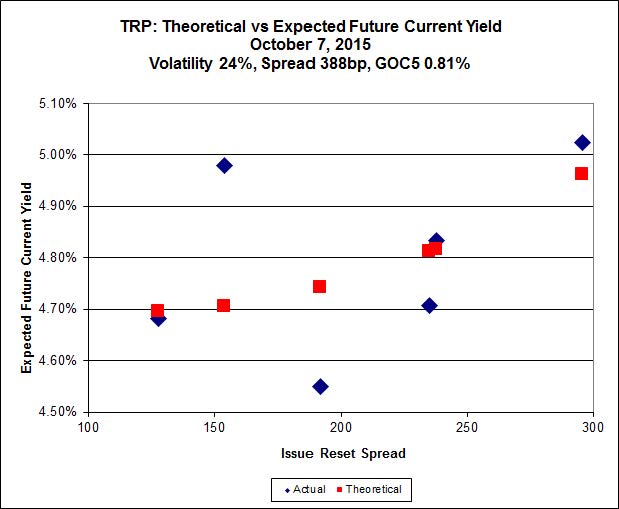

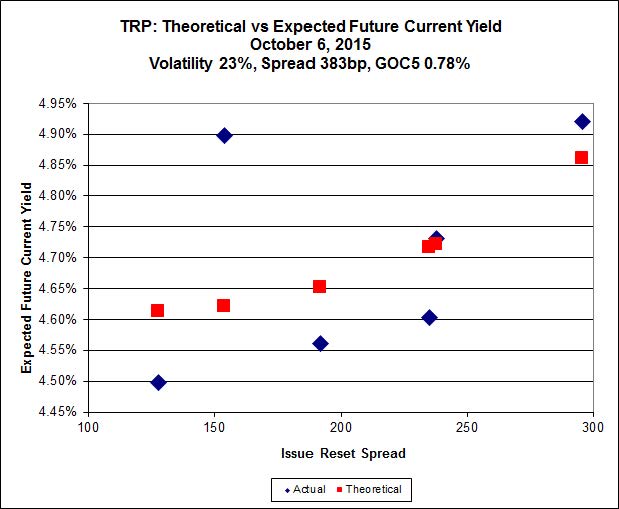

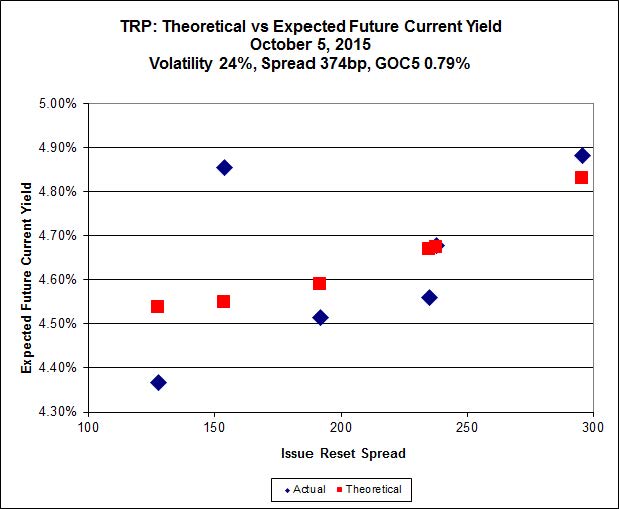

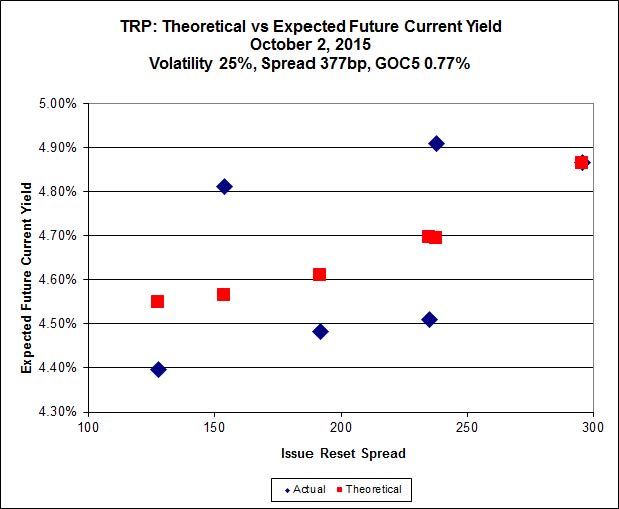

Here’s TRP:

Click for Big

Implied Volatility remained ridiculous.

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 14.83 to be $0.52 rich, while TRP.PR.D, resetting 2019-4-30 at +238, is $0.61 cheap at its bid price of 15.86.

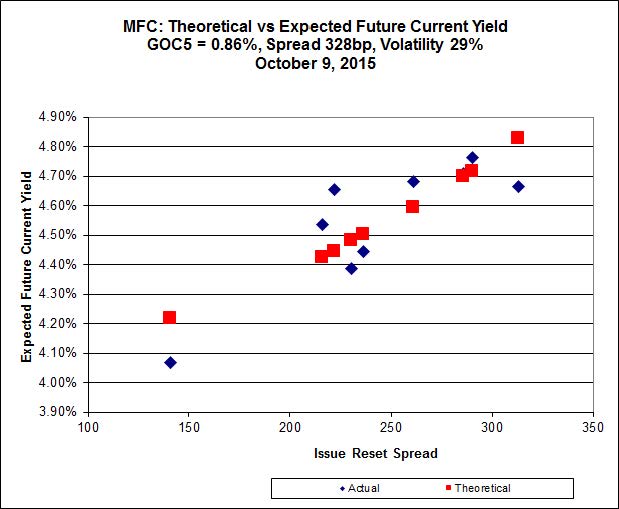

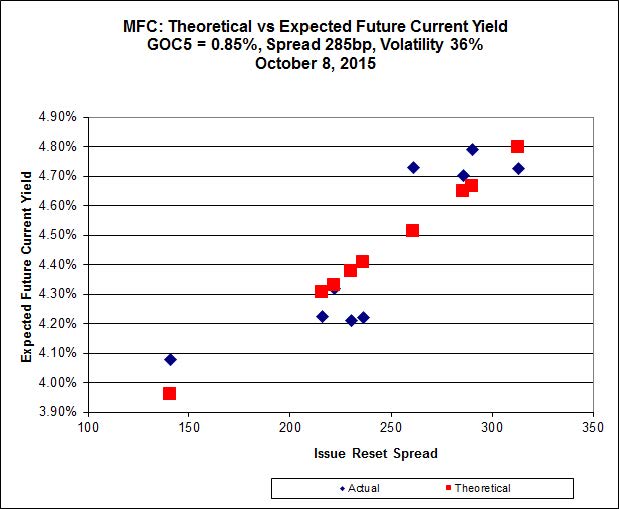

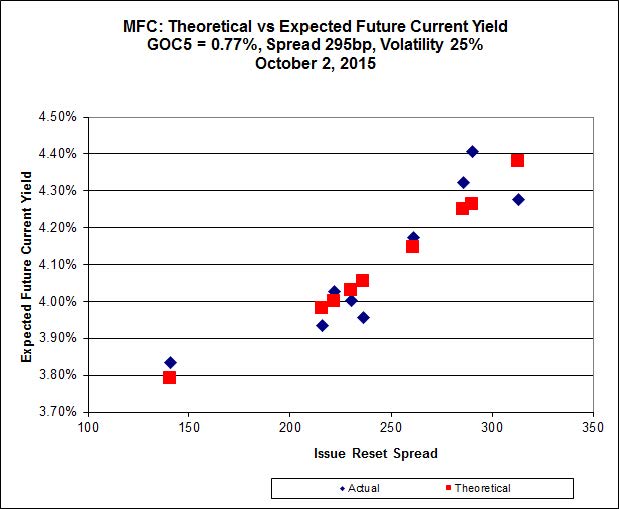

Click for Big

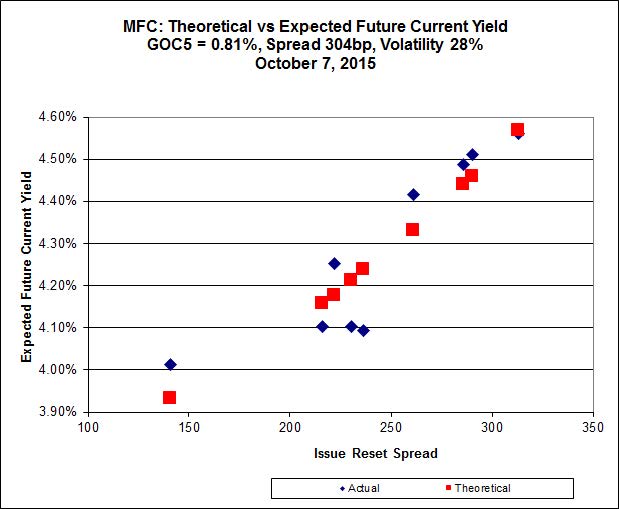

Implied Volatility re-established itself at higher levels today following the precipitous decline on Friday.

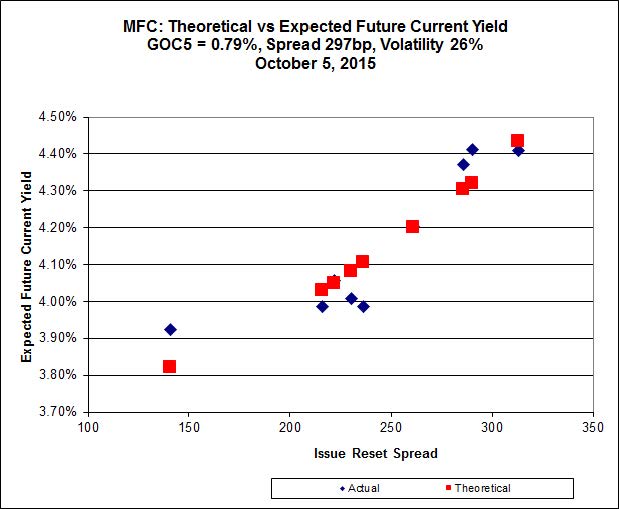

Most expensive is MFC.PR.F, resetting at +141bp on 2016-6-19, bid at 13.69 to be 0.59 rich, while MFC.PR.K resetting at +222bp on 2018-9-19, is bid at 16.01 to be 0.74 cheap.

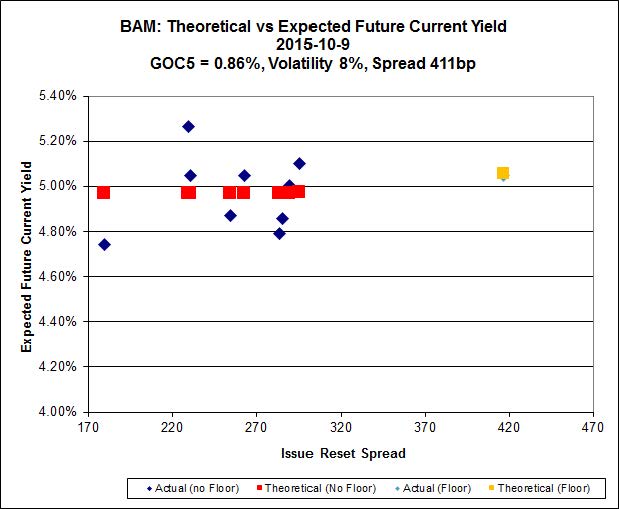

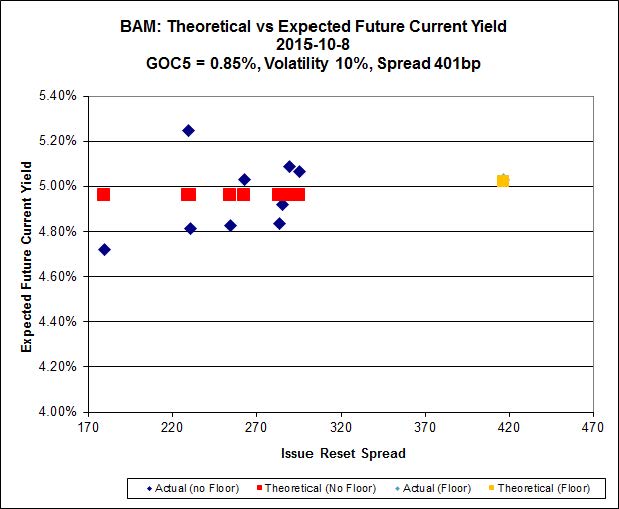

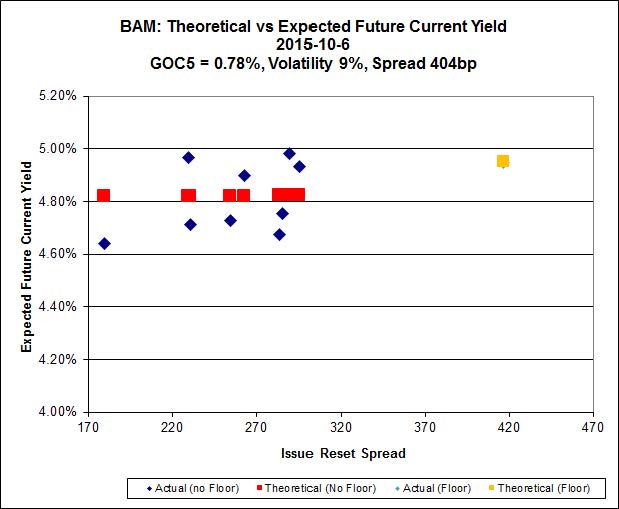

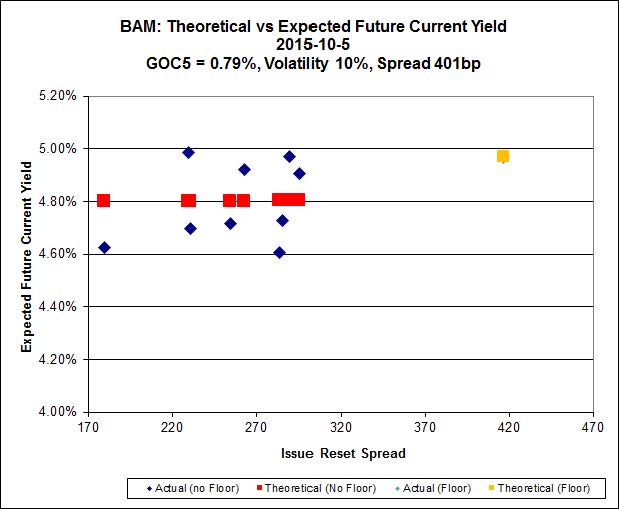

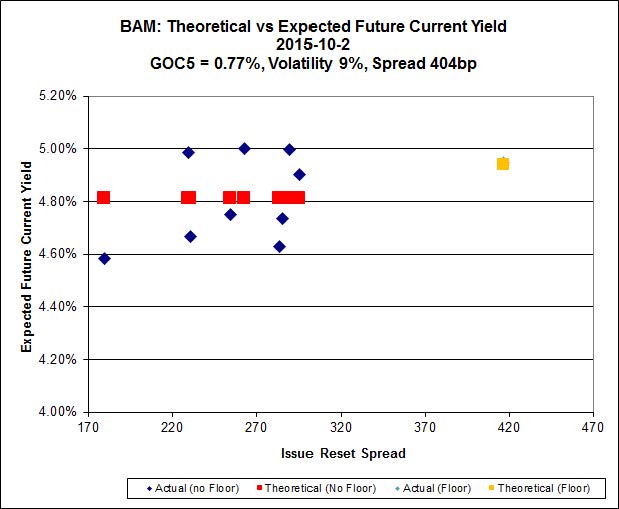

Click for Big

The fit on the BAM issues continues to be horrible!

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 14.92 to be $0.82 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.01 and appears to be $0.69 rich.

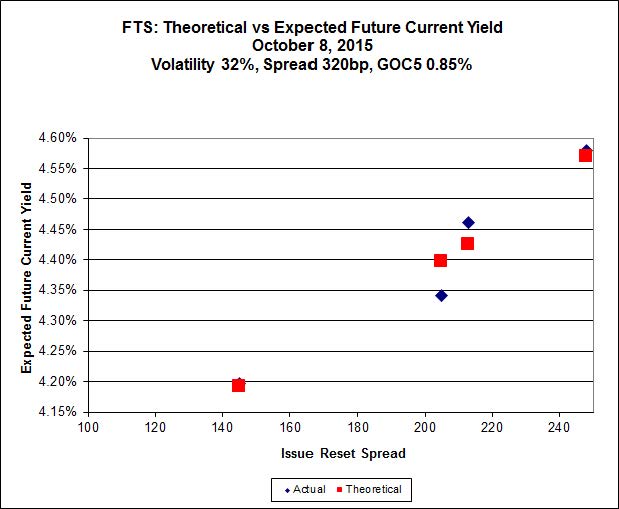

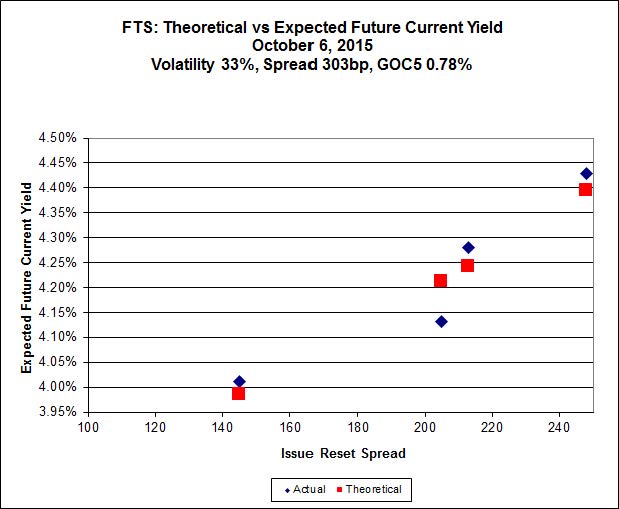

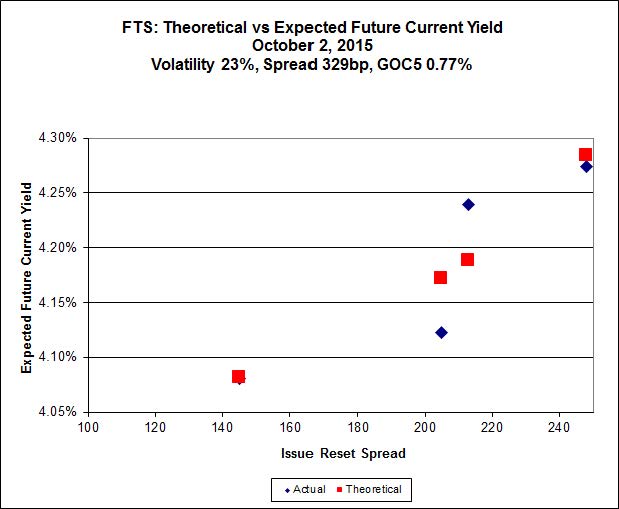

Click for Big

Implied Volatility edged up again today and is ridiculously high.

FTS.PR.K, with a spread of +205bp, and bid at 16.51, looks $0.23 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.16 and is $0.46 cheap.

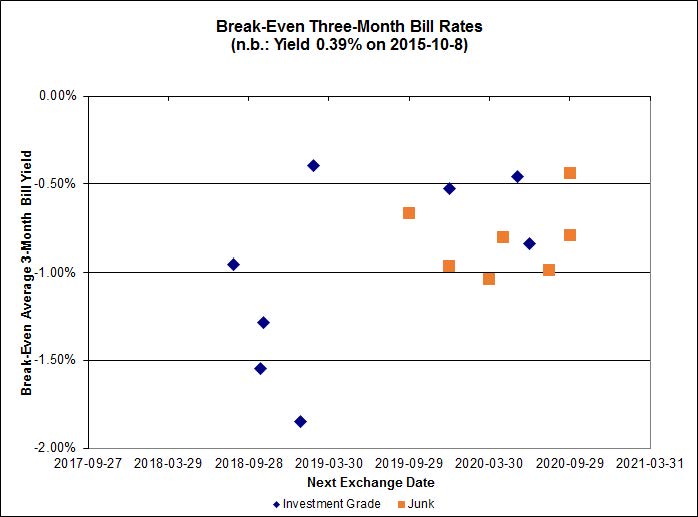

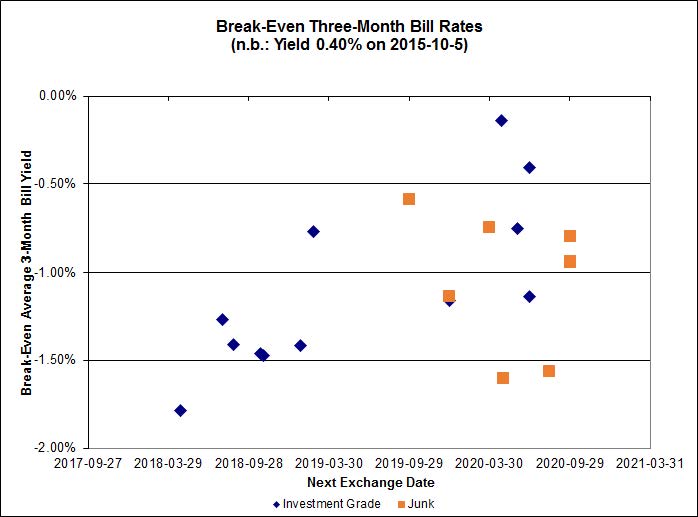

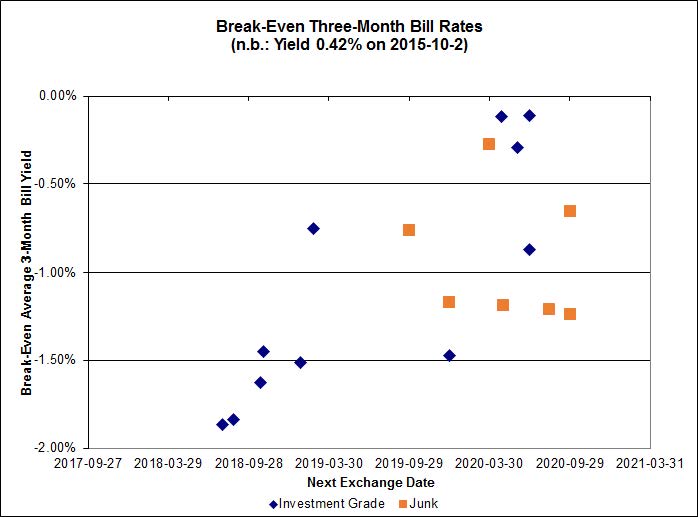

Click for Big

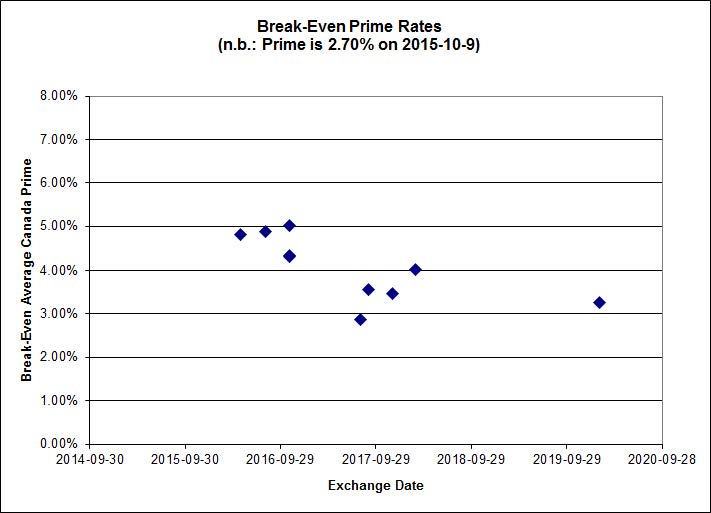

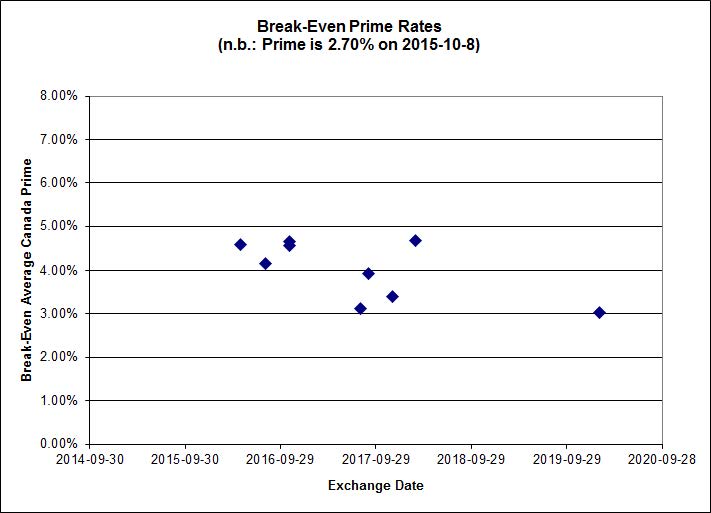

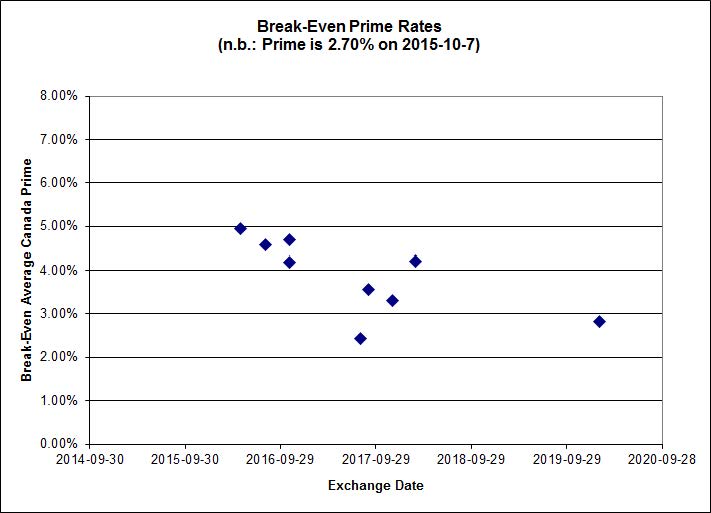

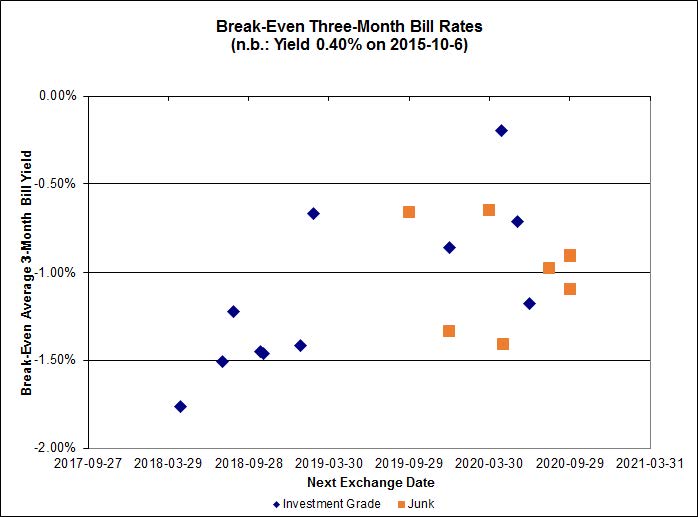

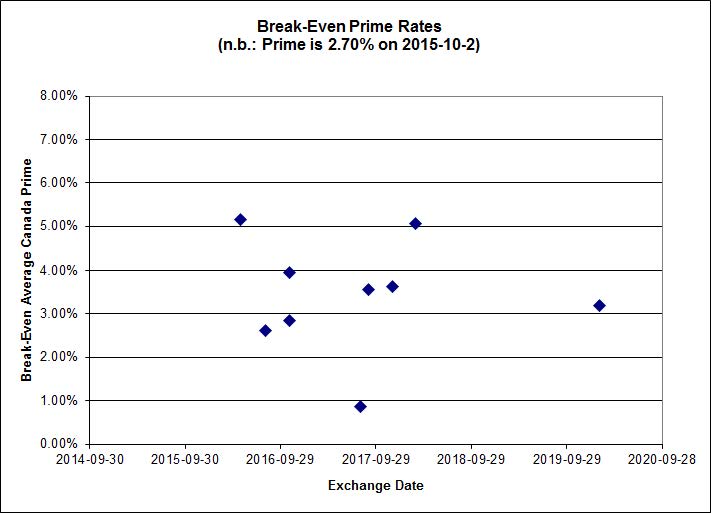

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.58%, with four outliers above 0.00% and none below -2.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -0.90% and other issues averaging -0.13%. There are three junk outliers above 0.00%.

Click for Big

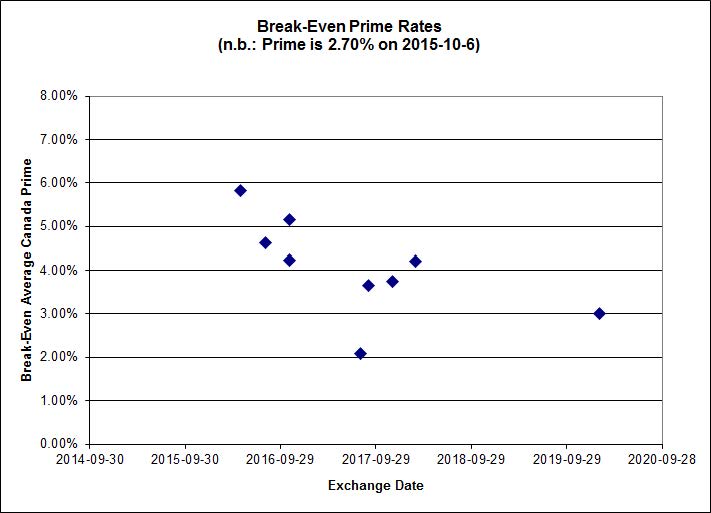

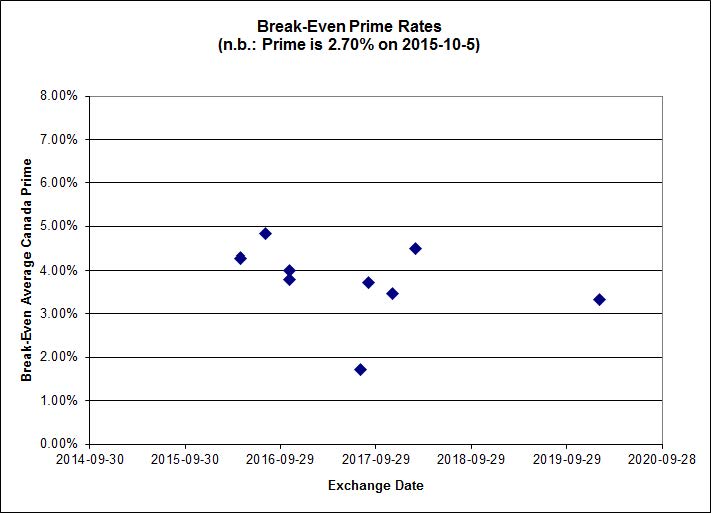

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3640 % | 1,589.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3640 % | 2,779.0 |

| Floater | 4.67 % | 4.72 % | 63,636 | 16.03 | 3 | 0.3640 % | 1,689.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3399 % | 2,754.7 |

| SplitShare | 4.35 % | 5.28 % | 73,962 | 2.99 | 5 | -0.3399 % | 3,228.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3399 % | 2,518.8 |

| Perpetual-Premium | 5.99 % | 6.03 % | 59,538 | 13.89 | 5 | -0.7537 % | 2,430.0 |

| Perpetual-Discount | 5.78 % | 5.84 % | 79,185 | 14.12 | 33 | -0.2720 % | 2,465.8 |

| FixedReset | 5.46 % | 4.97 % | 195,954 | 14.70 | 76 | -1.8643 % | 1,867.7 |

| Deemed-Retractible | 5.36 % | 5.38 % | 102,075 | 5.46 | 33 | -0.3074 % | 2,486.6 |

| FloatingReset | 2.66 % | 4.76 % | 65,454 | 5.82 | 9 | 0.0867 % | 2,048.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| RY.PR.I | FixedReset | -6.19 % | Not real. The issue traded 6,499 shares today in a range of 23.10-42 before closing at 21.81-23.42 (!). There were three trades in the last ten minutes at 23.10, totalling 2,500 shares. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.81 Bid-YTW : 5.76 % |

| MFC.PR.H | FixedReset | -6.17 % | Real enough! The issue traded 10,477 shares in a range of 20.01-21.68 before closing at 20.06-25. There were eleven trades in the market’s last hour, totalling 3,040 shares, in a range of 20.23-26. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.06 Bid-YTW : 7.12 % |

| MFC.PR.M | FixedReset | -5.52 % | Reasonably real. The issue traded 17,011 shares today in a range of 17.26-10 before closing at 17.11-42. There were seven trades in the last ten minutes, totalling 1,300 shares, in a range of 17.26-47. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.11 Bid-YTW : 8.67 % |

| GWO.PR.N | FixedReset | -5.21 % | Real! The issue traded 92,216 shares in a range of 13.30-93 before closing at 13.27-30. It looks like the market just ran of bids … there were at least eighteen trades totalling 38,800 shares timestamped between 3:35 and 3:43, then there was a pause, then seven trades totalling 2,200 shares timestamped at 3:58-3:59 in a range of 13.30-48. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.27 Bid-YTW : 10.20 % |

| TD.PF.C | FixedReset | -5.03 % | Real enough! The issue traded 21,902 shares in a range of 16.55-50 before closing at 16.63-94. There were 7 trades in the last six minutes, five of them totalling 933 shares at or below 16.62, two of them totalling 200 shares at or above 16.94. On a more reasonable day for the market I would fault the market-maker for allowing a spread of almost 2%, but on a day like this … I’ll give him a pass. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 16.63 Evaluated at bid price : 16.63 Bid-YTW : 4.91 % |

| IAG.PR.G | FixedReset | -4.97 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.72 Bid-YTW : 7.73 % |

| CM.PR.P | FixedReset | -4.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 16.65 Evaluated at bid price : 16.65 Bid-YTW : 4.91 % |

| SLF.PR.I | FixedReset | -4.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.10 Bid-YTW : 8.04 % |

| MFC.PR.L | FixedReset | -4.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.93 Bid-YTW : 9.48 % |

| MFC.PR.N | FixedReset | -4.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.25 Bid-YTW : 8.47 % |

| NA.PR.W | FixedReset | -3.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 16.66 Evaluated at bid price : 16.66 Bid-YTW : 4.95 % |

| TD.PF.B | FixedReset | -3.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 4.78 % |

| NA.PR.S | FixedReset | -3.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 16.97 Evaluated at bid price : 16.97 Bid-YTW : 5.05 % |

| PWF.PR.T | FixedReset | -3.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 18.86 Evaluated at bid price : 18.86 Bid-YTW : 4.52 % |

| TD.PF.A | FixedReset | -3.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 17.21 Evaluated at bid price : 17.21 Bid-YTW : 4.77 % |

| CM.PR.O | FixedReset | -3.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 17.38 Evaluated at bid price : 17.38 Bid-YTW : 4.81 % |

| VNR.PR.A | FixedReset | -3.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 5.31 % |

| BMO.PR.W | FixedReset | -3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 16.91 Evaluated at bid price : 16.91 Bid-YTW : 4.87 % |

| MFC.PR.K | FixedReset | -3.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.01 Bid-YTW : 9.30 % |

| TD.PR.S | FixedReset | -3.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.09 Bid-YTW : 4.27 % |

| IFC.PR.C | FixedReset | -3.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.02 Bid-YTW : 7.96 % |

| BMO.PR.Z | Perpetual-Discount | -2.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 22.10 Evaluated at bid price : 22.43 Bid-YTW : 5.67 % |

| TRP.PR.C | FixedReset | -2.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 11.49 Evaluated at bid price : 11.49 Bid-YTW : 5.25 % |

| BMO.PR.S | FixedReset | -2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 18.01 Evaluated at bid price : 18.01 Bid-YTW : 4.72 % |

| NA.PR.Q | FixedReset | -2.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.00 Bid-YTW : 4.92 % |

| BIP.PR.A | FixedReset | -2.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 19.60 Evaluated at bid price : 19.60 Bid-YTW : 5.72 % |

| RY.PR.H | FixedReset | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 4.70 % |

| BMO.PR.Y | FixedReset | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 18.67 Evaluated at bid price : 18.67 Bid-YTW : 5.01 % |

| MFC.PR.G | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.31 Bid-YTW : 7.35 % |

| BMO.PR.M | FixedReset | -2.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.51 Bid-YTW : 4.10 % |

| RY.PR.Z | FixedReset | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 17.81 Evaluated at bid price : 17.81 Bid-YTW : 4.64 % |

| IGM.PR.B | Perpetual-Premium | -2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 23.96 Evaluated at bid price : 24.25 Bid-YTW : 6.09 % |

| FTS.PR.G | FixedReset | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 16.16 Evaluated at bid price : 16.16 Bid-YTW : 4.92 % |

| RY.PR.W | Perpetual-Discount | -1.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 21.98 Evaluated at bid price : 22.21 Bid-YTW : 5.59 % |

| TRP.PR.G | FixedReset | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 17.67 Evaluated at bid price : 17.67 Bid-YTW : 5.48 % |

| MFC.PR.F | FixedReset | -1.86 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.69 Bid-YTW : 10.11 % |

| MFC.PR.I | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.39 Bid-YTW : 7.33 % |

| FTS.PR.K | FixedReset | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 16.51 Evaluated at bid price : 16.51 Bid-YTW : 4.78 % |

| BMO.PR.T | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 17.21 Evaluated at bid price : 17.21 Bid-YTW : 4.82 % |

| TD.PF.E | FixedReset | -1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 4.86 % |

| BAM.PF.E | FixedReset | -1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 17.24 Evaluated at bid price : 17.24 Bid-YTW : 5.38 % |

| MFC.PR.J | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.25 Bid-YTW : 7.86 % |

| SLF.PR.A | Deemed-Retractible | -1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.30 Bid-YTW : 7.69 % |

| BAM.PF.G | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 19.01 Evaluated at bid price : 19.01 Bid-YTW : 5.19 % |

| POW.PR.G | Perpetual-Discount | -1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 23.23 Evaluated at bid price : 23.63 Bid-YTW : 5.94 % |

| SLF.PR.H | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.76 Bid-YTW : 9.18 % |

| MFC.PR.B | Deemed-Retractible | -1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.89 Bid-YTW : 7.88 % |

| BAM.PF.B | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 17.05 Evaluated at bid price : 17.05 Bid-YTW : 5.39 % |

| RY.PR.M | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 18.01 Evaluated at bid price : 18.01 Bid-YTW : 4.95 % |

| SLF.PR.B | Deemed-Retractible | -1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.53 Bid-YTW : 7.58 % |

| BAM.PF.A | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 18.55 Evaluated at bid price : 18.55 Bid-YTW : 5.28 % |

| IFC.PR.A | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.03 Bid-YTW : 9.81 % |

| CU.PR.D | Perpetual-Discount | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 21.33 Evaluated at bid price : 21.33 Bid-YTW : 5.83 % |

| BNS.PR.D | FloatingReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.61 Bid-YTW : 6.32 % |

| HSE.PR.A | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 13.15 Evaluated at bid price : 13.15 Bid-YTW : 5.08 % |

| TD.PF.F | Perpetual-Discount | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 21.96 Evaluated at bid price : 22.25 Bid-YTW : 5.51 % |

| BNS.PR.P | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.63 Bid-YTW : 4.08 % |

| SLF.PR.D | Deemed-Retractible | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.33 Bid-YTW : 8.03 % |

| RY.PR.L | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.52 Bid-YTW : 4.41 % |

| BNS.PR.R | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.70 Bid-YTW : 4.27 % |

| CU.PR.C | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 18.26 Evaluated at bid price : 18.26 Bid-YTW : 4.61 % |

| SLF.PR.C | Deemed-Retractible | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.35 Bid-YTW : 8.01 % |

| BNS.PR.Q | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.34 Bid-YTW : 4.29 % |

| MFC.PR.C | Deemed-Retractible | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.54 Bid-YTW : 7.96 % |

| CU.PR.H | Perpetual-Discount | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 22.51 Evaluated at bid price : 22.83 Bid-YTW : 5.85 % |

| BAM.PF.D | Perpetual-Discount | 1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 20.49 Evaluated at bid price : 20.49 Bid-YTW : 6.04 % |

| TRP.PR.D | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 15.86 Evaluated at bid price : 15.86 Bid-YTW : 5.37 % |

| HSE.PR.E | FixedReset | 1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 21.96 Evaluated at bid price : 22.43 Bid-YTW : 4.97 % |

| SLF.PR.J | FloatingReset | 5.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.30 Bid-YTW : 9.51 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| GWO.PR.N | FixedReset | 92,216 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.27 Bid-YTW : 10.20 % |

| BAM.PF.H | FixedReset | 70,006 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 23.14 Evaluated at bid price : 24.98 Bid-YTW : 4.96 % |

| CM.PR.P | FixedReset | 51,217 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 16.65 Evaluated at bid price : 16.65 Bid-YTW : 4.91 % |

| BMO.PR.Z | Perpetual-Discount | 48,707 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 22.10 Evaluated at bid price : 22.43 Bid-YTW : 5.67 % |

| CM.PR.Q | FixedReset | 37,747 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 19.08 Evaluated at bid price : 19.08 Bid-YTW : 4.78 % |

| FTS.PR.M | FixedReset | 35,691 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-13 Maturity Price : 18.06 Evaluated at bid price : 18.06 Bid-YTW : 4.93 % |

| There were 65 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| RY.PR.I | FixedReset | Quote: 21.81 – 23.00 Spot Rate : 1.1900 Average : 0.7621 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 18.72 – 19.35 Spot Rate : 0.6300 Average : 0.4000 YTW SCENARIO |

| CU.PR.D | Perpetual-Discount | Quote: 21.33 – 21.85 Spot Rate : 0.5200 Average : 0.3449 YTW SCENARIO |

| TD.PF.D | FixedReset | Quote: 18.80 – 19.39 Spot Rate : 0.5900 Average : 0.4502 YTW SCENARIO |

| PWF.PR.G | Perpetual-Premium | Quote: 24.50 – 24.94 Spot Rate : 0.4400 Average : 0.3011 YTW SCENARIO |

| PVS.PR.B | SplitShare | Quote: 24.31 – 24.74 Spot Rate : 0.4300 Average : 0.2925 YTW SCENARIO |