Apparently, somebody important has told Lapdog Carney to talk about climate change:

Mark Carney, the governor of the Bank of England, declared that the warming climate presented major risks for the global economy and global financial stability, and that businesses and regulators needed to move more quickly to try to contain the potential economic damage even though it may seem uncertain and far off.

His warning, delivered in a 4,400-word speech with ample footnotes on Tuesday, is the latest example of how climate change has moved beyond theoretical scientific debates to the start of practical planning for safeguarding the economy and business.

“We don’t need an army of actuaries to tell us that the catastrophic impacts of climate change will be felt beyond the traditional horizons of most actors — imposing a cost on future generations that the current generation has no direct incentive to fix,” he said. “In other words, once climate change becomes a defining issue for financial stability, it may already be too late.”

SEC Commissioner Kara M. Stein has displayed total ignorance of the practical side of software development with her speech titled Market Structure in the 21st Century: Bringing Light to the Dark:

In addressing this challenge, I come back to the basic fact that behind every algorithm, order type, and electronic trading network are human beings: individuals program computers, individuals design trading algorithms, and individuals market products. Individuals supervise and design compliance structures. Regardless of the advancement of technology and innovation in our securities markets, humans – individuals – are necessary to what we do each and every day.

All market participants need to be responsible for their work and, at the same time, its collateral consequences. To do that, every individual within a securities organization – from the coder to the cybersecurity officer, the salesperson to the CEO – needs to understand the new electronic marketplace. Everyone needs to be cognizant of how the work he or she is doing could affect the market as a whole, including from a technological and operational perspective.

Everyone involved also needs to know the rules of the road. Without that, we lose transparency, we do not know who to trust, and confidence in the system diminishes. Just as we license drivers and ensure that vehicles have basic requirements of safety and soundness, we should consider whether certain personnel are so vital in our increasingly “robotic” securities market that they should be licensed. In a world where programming errors are just as damaging to investors as improper sales practices, our regulatory approach may need to evolve.

Complex organizational charts should not shield individuals from accountability. It cannot continue to be the case that so-called “technological glitches” set off a series of finger pointing within firms. Opacity must be replaced with transparency, including within firms themselves. I will be following this issue closely and would like to see firms take it upon themselves to make these changes proactively.

So she wants everybody, from some teeny-bopper programmer to the salesman pushing the button, to “understand the new electronic marketplace”. A laudable objective, but in practice totally divorced from reality.

My strength as a programmer is that I’m also a portfolio manager. My strength as a portfolio manager is that I’m also a programmer. Twenty-five-odd years in the business have given me a pretty good feel for just how rare that combination is.

The things she dismisses as ‘so-called “technological glitches”‘ are, more often than not, just that. They’re bugs. Bugs are inevitable in any complex software project. What does she intend, to hold some $50,000 p.a. teeny-bopper programmer 100% accountable for a bug that bursts the market some day? She’s going to really enjoy destroying some helpless scapegoat for typing “<" when he should have typed ">“?

Bugs is bugs is bugs. I will certainly agree that accountability should exist, but it is entirely appropriate for this accountability – as far as the SEC and the justice system are concerned – to remain at firm level. Nail the firm for not having sufficiently robust error checking and debugging. It is not realistic to hold any individual on any given level of the pyramid 100% accountable for a bug. Theoretically, sure it’s possible. Practically? Give me a break. It’s a recipe for either never getting anything done or for scapegoating some poor sucker who made a good faith effort. Put this woman in charge of the European Space Agency – and then, finally, somebody body will be HELD ACCOUNTABLE for the problems with the Philae Lander.

This is not to say there should be a total carte-blanche for software, of course. Salesmen should have a “reasonable” knowledge of what their software does; there must be “reasonable” documentation of who told who to do what when; and there will, from time to time, be clear indications that somebody was deliberately doing something naughty with software, as discussed on August 12 … but total individual accountability is nothing more than a pipe dream.

William C Dudley of the New York Fed made a speech titled Regulation and Liquidity Provision, which makes some points about corporate bond liquidity:

To investigate corporate bond market liquidity in more detail, let’s examine three liquidity measures: the average trade size, “effective” bid-ask spreads and price impact. The evidence on the average trade size for investment grade corporate bonds indicates a slight reduction from between $700,000 to $800,000 in the early 2000s to around $500,000 in the last few years. (Exhibit 6) However, price measures of corporate bond liquidity do not substantiate the trend in this quantity measure. The effective bid-ask spread has been trending down since the early 2000s, around the same time that TRACE reporting was introduced. The spread spiked during the financial crisis, but is now lower than its pre-crisis levels. (Exhibit 7) Similarly, price impact—the effect on price from a $1 million trade—has also been trending down since the early 2000s apart from the jump during the financial crisis. (Exhibit 8)

One metric he leaves out of his assessment is trading intensity, which might also be described as market turnover:

At the moment, trading indicators give the appearance of robust normality. Trading volumes are high, particularly in bonds where they are at record levels. Spreads (the difference between the bid and offer price for a security) are small. The emergence of electronic trading and also a variety of investors gives the impression of a highly liquid market.

But market turnover – the volume of trading relative to outstanding securities – in bonds and shares has fallen significantly.

Government and corporate bond turnover is down about 50 percent, in part reflecting the massive growth in issuance.

In other words, maybe price impact is holding steady because traders and managers are taking longer to do their trades. It is reasonable to suppose that, for instance, if you really want to extend duration in your GE bonds but that costs too much, you’ll extend duration somewhere else, instead – like Treasuries, for instance. You won’t do the GE trade because it’s too expensive – so price impact remains unchanged, but GE market turnover goes down. Liquidity is a very tricky thing to define; what’s worse, it means different things to different people, according to their individual objectives.

Sometimes even different things to the same person! Say I have a PerpetualDiscount that I can trade in size within ten cents, either way, of the midpoint. Well, that’s a liquid issue, right? But it’s yielding 310bp over long term bonds! That’s a great big liquidity premium!

It has also been claimed, quite reasonably, that:

Since 2009 the number of issuers in the high-grade corporate bond market has almost doubled. These “new issuers” tend to have less overall debt outstanding (almost four times less), fewer securities, and don’t trade as frequently. For example, within the JP Morgan U.S. Liquid Corporate Bond Index, bonds that represent over 0.5% of the index had a 31% higher turnover ratio than issuers that fell below the 0.5% threshold.

So what are we to conclude about that?

This was all brought to my attention by Assiduous Reader JP (you know, he’s the guy who sends me interesting links, while the rest of bums think Deep Thoughts with your eyes closed), who sent me a link to a story titled Market Moves That Aren’t Supposed to Happen Keep Happening:

While the New York Fed president argued that there’s little evidence so far that new financial regulation has cut into the ease of trading U.S. Treasuries, TD analysts Priya Misra and Gennadiy Goldberg think otherwise. They point to daily, wild swings in the bond market as evidence of diminished liquidity.

Our findings show that daily changes in 10-year Treasury yields exceeded one standard deviation (σ) 58% of the time so far in 2015—considerably higher than the 49% observed last year (Figure 2). The 58% measure is the highest reading going back to 1975, suggesting that recent volatility in Treasury markets is unprecedented. As if a record number of “choppy” days were not enough, 10-year yield movements also exceeded 3σ in as many as 9% of trading days this year. This is higher than the average of 6% of days since 1975.

…

While Dudley finds little evidence of average bond market liquidity having deteriorated, TD reckons the problem lies in so-called “tail events,” in which increased regulation and changes to market structure exacerbate the potential for extreme moves. Looking at average liquidity conditions won’t show much evidence of a problem, therefore. That might go some way toward explaining why all those market moves that are supposed to not happen very often keep occurring with some regularity.

Here’s TD’s thinking:

The issue, as reflected by our sigma measure, may very well be one of “fat tails problems” and lower liquidity during these tail events due to lower dealer risk appetite. The argument is that an unexpected macro event or large-sized risk transfer has the potential of creating much larger market moves today compared with the past. This would be consistent with a greater number of days in recent months exhibiting 1σ or 3σ sigma moves.

I hope everybody is sitting down because … it was actually a pretty good day for the Canadian preferred share market! PerpetualDiscounts gained 55bp, FixedResets were up 64bp and DeemedRetractibles won 82bp. There’s good representation of each group on the good side of the lengthy Performance Highlights table. Volume was above average.

PerpetualDiscounts now yield 5.74%, equivalent to 7.46% interest at the standard equivalency factor of 1.3x. Long corporates yield about 4.2%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 325bp, a significant rise from the 310bp reported September 23. It was a good day, but one swallow doesn’t make a summer!

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

Here’s TRP:

Click for Big

Click for BigImplied Volatility edged up again today.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.55 to be $0.58 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $0.65 cheap at its bid price of 12.21.

Click for Big

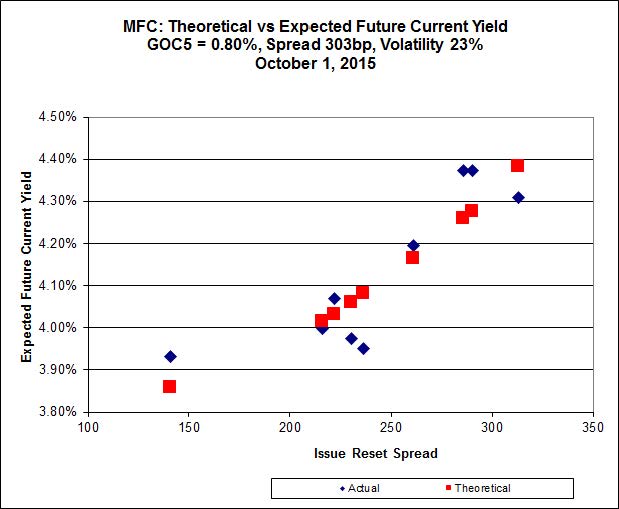

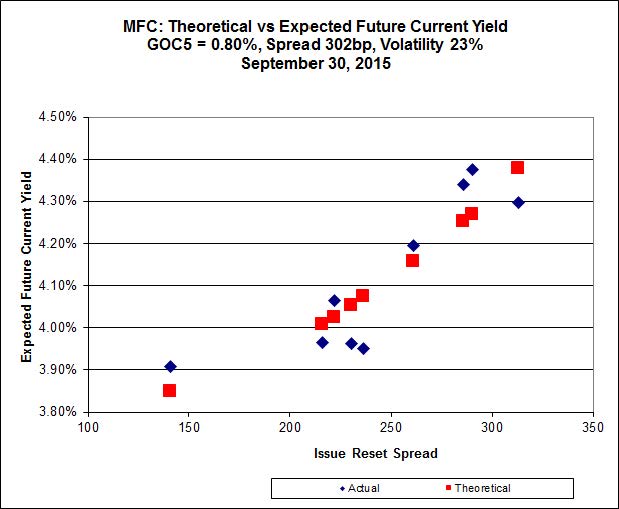

Click for BigAnother good fit today for MFC, with Implied Volatility edging downward.

Most expensive is MFC.PR.M, resetting at +236bp on 2019-12-19, bid at 20.00 to be 0.60 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 21.14 to be 0.53 cheap.

Click for Big

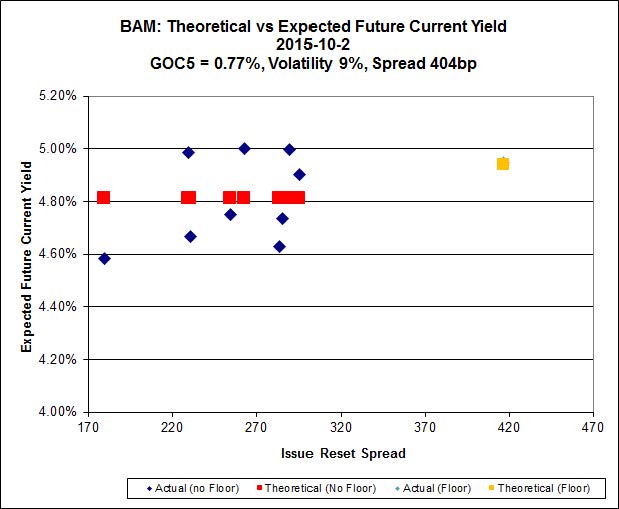

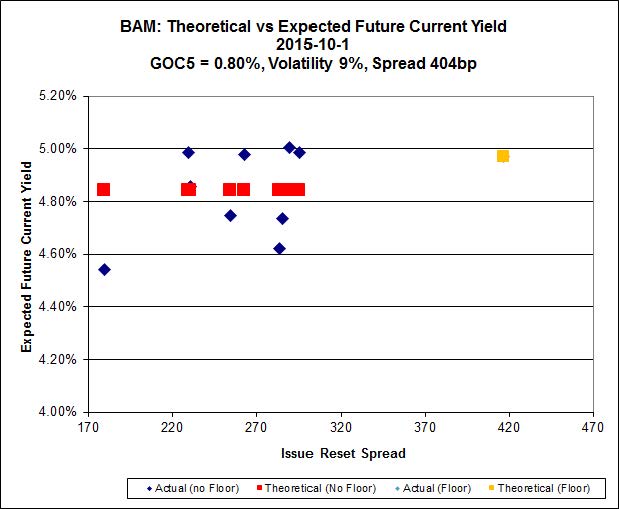

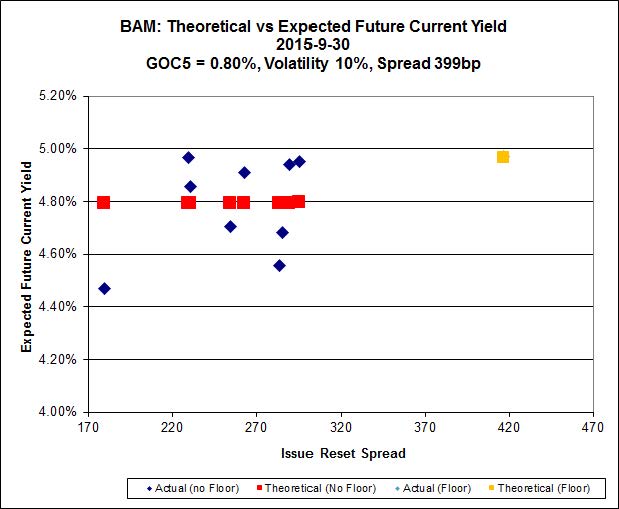

Click for BigThe fit on the BAM issues continues to be horrible. Note that the pending new issue has been added with a price of 25.00; the valuation effects of the rate floor have been ignored.

The cheapest issue relative to its peers is BAM.PR.Z, resetting at +296bp on 2017-12-31, bid at 19.00 to be $0.62 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.97 and appears to be $0.98 rich.

Click for Big

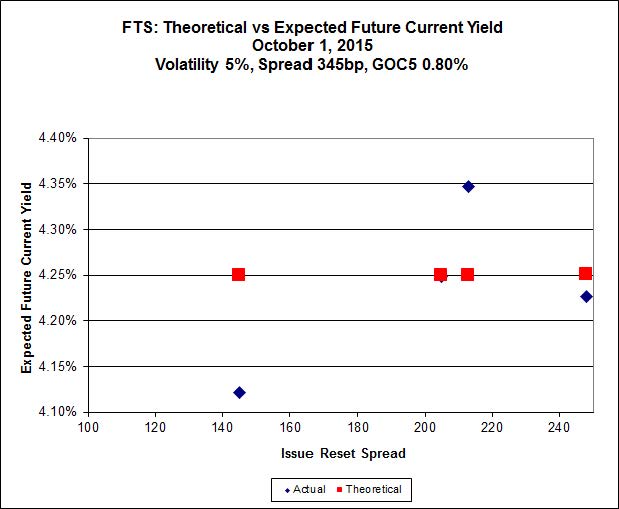

Click for BigFTS.PR.M, with a spread of +248bp, and bid at 19.37, looks $0.21 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.85 and is $0.26 cheap.

Click for Big

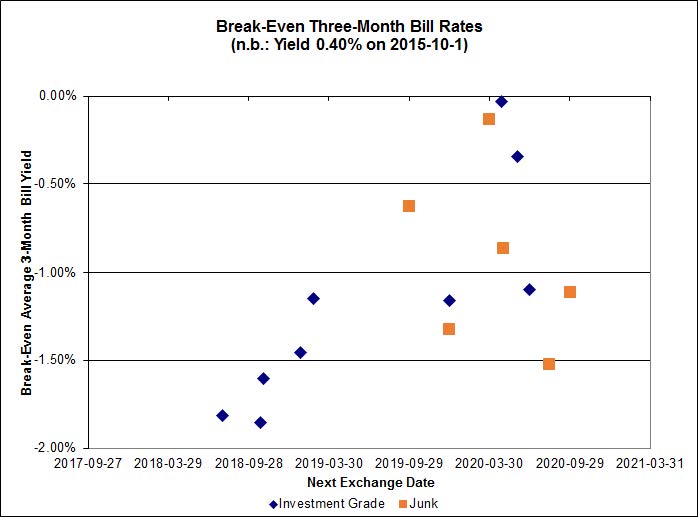

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.11%, with one outlier above 0.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -1.57% and other issues averaging -0.47%. There are three junk outliers above 0.00%, including all three of the new Strong Pairs that came into existence today.

Click for Big

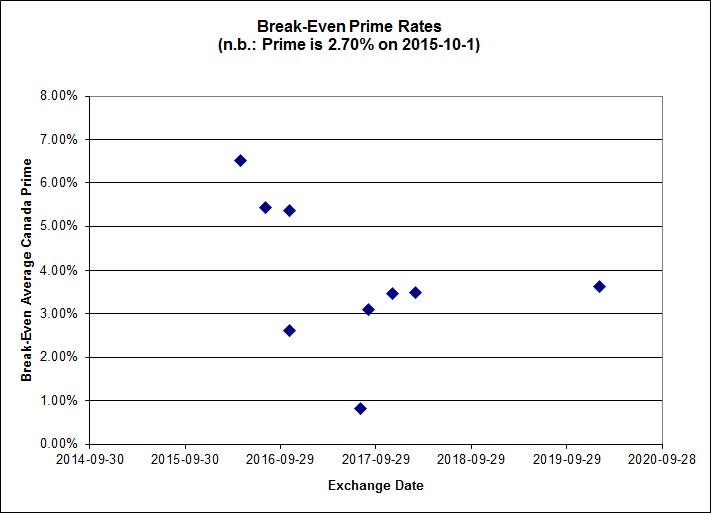

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.4765 % |

1,641.8 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.4765 % |

2,870.6 |

| Floater |

4.52 % |

4.55 % |

61,744 |

16.32 |

3 |

-0.4765 % |

1,745.3 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0508 % |

2,762.8 |

| SplitShare |

4.49 % |

4.73 % |

64,971 |

3.02 |

4 |

0.0508 % |

3,237.8 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0508 % |

2,526.3 |

| Perpetual-Premium |

5.82 % |

5.87 % |

68,535 |

14.03 |

8 |

0.1461 % |

2,463.4 |

| Perpetual-Discount |

5.68 % |

5.74 % |

72,000 |

14.22 |

30 |

0.5517 % |

2,501.7 |

| FixedReset |

5.16 % |

4.65 % |

182,272 |

15.33 |

75 |

0.6440 % |

1,973.1 |

| Deemed-Retractible |

5.23 % |

5.28 % |

98,396 |

5.47 |

33 |

0.8215 % |

2,541.4 |

| FloatingReset |

2.63 % |

4.48 % |

60,623 |

5.84 |

9 |

0.5265 % |

2,066.7 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| CM.PR.Q |

FixedReset |

-1.92 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 20.40

Evaluated at bid price : 20.40

Bid-YTW : 4.39 % |

| W.PR.H |

Perpetual-Discount |

-1.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 22.80

Evaluated at bid price : 23.08

Bid-YTW : 5.97 % |

| CU.PR.H |

Perpetual-Discount |

-1.51 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 22.57

Evaluated at bid price : 22.90

Bid-YTW : 5.81 % |

| GWO.PR.N |

FixedReset |

-1.49 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.89

Bid-YTW : 9.44 % |

| FTS.PR.M |

FixedReset |

-1.42 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 19.37

Evaluated at bid price : 19.37

Bid-YTW : 4.49 % |

| BAM.PR.B |

Floater |

-1.13 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 10.54

Evaluated at bid price : 10.54

Bid-YTW : 4.49 % |

| PWF.PR.T |

FixedReset |

-1.08 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 21.73

Evaluated at bid price : 22.01

Bid-YTW : 3.81 % |

| PVS.PR.B |

SplitShare |

1.03 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2019-01-10

Maturity Price : 25.00

Evaluated at bid price : 24.50

Bid-YTW : 5.14 % |

| GWO.PR.R |

Deemed-Retractible |

1.07 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.75

Bid-YTW : 6.74 % |

| GWO.PR.L |

Deemed-Retractible |

1.07 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.57

Bid-YTW : 5.93 % |

| SLF.PR.G |

FixedReset |

1.07 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.08

Bid-YTW : 8.51 % |

| BAM.PR.M |

Perpetual-Discount |

1.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 20.05

Evaluated at bid price : 20.05

Bid-YTW : 5.97 % |

| SLF.PR.H |

FixedReset |

1.11 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.25

Bid-YTW : 7.83 % |

| RY.PR.H |

FixedReset |

1.13 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 18.86

Evaluated at bid price : 18.86

Bid-YTW : 4.31 % |

| SLF.PR.B |

Deemed-Retractible |

1.17 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.63

Bid-YTW : 6.82 % |

| BAM.PF.A |

FixedReset |

1.19 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 18.72

Evaluated at bid price : 18.72

Bid-YTW : 5.13 % |

| GWO.PR.G |

Deemed-Retractible |

1.20 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.85

Bid-YTW : 6.48 % |

| BAM.PR.Z |

FixedReset |

1.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 18.98

Evaluated at bid price : 18.98

Bid-YTW : 5.16 % |

| SLF.PR.D |

Deemed-Retractible |

1.25 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.25

Bid-YTW : 7.34 % |

| POW.PR.D |

Perpetual-Discount |

1.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 21.55

Evaluated at bid price : 21.81

Bid-YTW : 5.74 % |

| RY.PR.Z |

FixedReset |

1.29 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 18.87

Evaluated at bid price : 18.87

Bid-YTW : 4.27 % |

| CU.PR.F |

Perpetual-Discount |

1.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 20.01

Evaluated at bid price : 20.01

Bid-YTW : 5.69 % |

| FTS.PR.K |

FixedReset |

1.35 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 16.57

Evaluated at bid price : 16.57

Bid-YTW : 4.65 % |

| NA.PR.S |

FixedReset |

1.35 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 19.50

Evaluated at bid price : 19.50

Bid-YTW : 4.36 % |

| BMO.PR.T |

FixedReset |

1.37 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 18.50

Evaluated at bid price : 18.50

Bid-YTW : 4.38 % |

| TD.PF.B |

FixedReset |

1.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 18.90

Evaluated at bid price : 18.90

Bid-YTW : 4.30 % |

| TRP.PR.F |

FloatingReset |

1.40 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 13.00

Evaluated at bid price : 13.00

Bid-YTW : 4.47 % |

| BNS.PR.P |

FixedReset |

1.42 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.21

Bid-YTW : 3.73 % |

| GWO.PR.Q |

Deemed-Retractible |

1.46 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.90

Bid-YTW : 6.40 % |

| GWO.PR.P |

Deemed-Retractible |

1.50 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.75

Bid-YTW : 6.15 % |

| RY.PR.N |

Perpetual-Discount |

1.50 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 22.61

Evaluated at bid price : 22.94

Bid-YTW : 5.47 % |

| PWF.PR.K |

Perpetual-Discount |

1.52 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 21.85

Evaluated at bid price : 22.09

Bid-YTW : 5.69 % |

| BAM.PR.N |

Perpetual-Discount |

1.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 20.06

Evaluated at bid price : 20.06

Bid-YTW : 5.96 % |

| BAM.PR.T |

FixedReset |

1.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 16.01

Evaluated at bid price : 16.01

Bid-YTW : 5.07 % |

| MFC.PR.G |

FixedReset |

1.68 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.14

Bid-YTW : 6.01 % |

| GWO.PR.I |

Deemed-Retractible |

1.69 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.10

Bid-YTW : 6.82 % |

| FTS.PR.F |

Perpetual-Discount |

1.85 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 21.75

Evaluated at bid price : 22.00

Bid-YTW : 5.62 % |

| BAM.PR.R |

FixedReset |

1.89 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 15.60

Evaluated at bid price : 15.60

Bid-YTW : 5.10 % |

| SLF.PR.E |

Deemed-Retractible |

1.93 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.62

Bid-YTW : 7.14 % |

| SLF.PR.A |

Deemed-Retractible |

2.03 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.58

Bid-YTW : 6.79 % |

| GWO.PR.S |

Deemed-Retractible |

2.05 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.35

Bid-YTW : 6.23 % |

| MFC.PR.B |

Deemed-Retractible |

2.10 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.40

Bid-YTW : 6.82 % |

| POW.PR.B |

Perpetual-Discount |

2.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 23.09

Evaluated at bid price : 23.35

Bid-YTW : 5.74 % |

| MFC.PR.N |

FixedReset |

2.25 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.56

Bid-YTW : 6.68 % |

| SLF.PR.C |

Deemed-Retractible |

2.26 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.40

Bid-YTW : 7.23 % |

| PWF.PR.P |

FixedReset |

2.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 14.68

Evaluated at bid price : 14.68

Bid-YTW : 4.17 % |

| MFC.PR.M |

FixedReset |

2.35 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.00

Bid-YTW : 6.46 % |

| SLF.PR.J |

FloatingReset |

2.40 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 12.80

Bid-YTW : 9.97 % |

| FTS.PR.G |

FixedReset |

2.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 16.85

Evaluated at bid price : 16.85

Bid-YTW : 4.60 % |

| RY.PR.D |

Deemed-Retractible |

2.55 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.90

Bid-YTW : 4.68 % |

| FTS.PR.J |

Perpetual-Discount |

2.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 21.55

Evaluated at bid price : 21.55

Bid-YTW : 5.58 % |

| TRP.PR.E |

FixedReset |

2.63 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 17.55

Evaluated at bid price : 17.55

Bid-YTW : 4.81 % |

| TRP.PR.A |

FixedReset |

2.69 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 14.90

Evaluated at bid price : 14.90

Bid-YTW : 4.79 % |

| TRP.PR.C |

FixedReset |

2.86 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 12.21

Evaluated at bid price : 12.21

Bid-YTW : 4.76 % |

| FTS.PR.H |

FixedReset |

2.93 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 13.35

Evaluated at bid price : 13.35

Bid-YTW : 4.34 % |

| GWO.PR.H |

Deemed-Retractible |

3.03 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.09

Bid-YTW : 6.58 % |

| HSE.PR.E |

FixedReset |

3.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 21.66

Evaluated at bid price : 22.00

Bid-YTW : 5.00 % |

| SLF.PR.I |

FixedReset |

3.39 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.85

Bid-YTW : 6.67 % |

| MFC.PR.C |

Deemed-Retractible |

3.49 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.76

Bid-YTW : 7.07 % |

| TRP.PR.D |

FixedReset |

3.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 17.20

Evaluated at bid price : 17.20

Bid-YTW : 4.83 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| IFC.PR.C |

FixedReset |

71,388 |

Scotia crossed 54,900 at 18.30.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.66

Bid-YTW : 7.36 % |

| TRP.PR.D |

FixedReset |

58,645 |

TD crossed 30,000 at 17.21.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 17.20

Evaluated at bid price : 17.20

Bid-YTW : 4.83 % |

| TRP.PR.E |

FixedReset |

52,342 |

TD crossed 30,000 at 18.00.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 17.55

Evaluated at bid price : 17.55

Bid-YTW : 4.81 % |

| MFC.PR.K |

FixedReset |

50,050 |

Scotia crossed 39,200 at 18.55.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.58

Bid-YTW : 7.16 % |

| BMO.PR.R |

FloatingReset |

49,700 |

RBC crossed 48,400 at 21.60.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.70

Bid-YTW : 4.46 % |

| BMO.PR.K |

Deemed-Retractible |

34,388 |

Scotia crossed 25,000 at 25.54.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2016-11-25

Maturity Price : 25.00

Evaluated at bid price : 25.38

Bid-YTW : 4.37 % |

| There were 39 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| IAG.PR.G |

FixedReset |

Quote: 20.17 – 20.95

Spot Rate : 0.7800

Average : 0.5161

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.17

Bid-YTW : 6.61 % |

| FTS.PR.H |

FixedReset |

Quote: 13.35 – 13.95

Spot Rate : 0.6000

Average : 0.4362

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 13.35

Evaluated at bid price : 13.35

Bid-YTW : 4.34 % |

| PVS.PR.D |

SplitShare |

Quote: 23.80 – 24.20

Spot Rate : 0.4000

Average : 0.2954

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2021-10-08

Maturity Price : 25.00

Evaluated at bid price : 23.80

Bid-YTW : 5.53 % |

| MFC.PR.K |

FixedReset |

Quote: 18.58 – 18.92

Spot Rate : 0.3400

Average : 0.2380

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.58

Bid-YTW : 7.16 % |

| PWF.PR.T |

FixedReset |

Quote: 22.01 – 22.40

Spot Rate : 0.3900

Average : 0.2923

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 21.73

Evaluated at bid price : 22.01

Bid-YTW : 3.81 % |

| POW.PR.G |

Perpetual-Discount |

Quote: 24.16 – 24.50

Spot Rate : 0.3400

Average : 0.2489

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-09-30

Maturity Price : 23.69

Evaluated at bid price : 24.16

Bid-YTW : 5.79 % |