You know what Russia needs? Russia needs another James Coyne, that’s what Russia needs:

The message some Russia watchers are getting from Friday’s surprise interest-rate cut is this: Start listening more to what President Vladimir Putin’s aides say about monetary policy and less to central bankers.

Here’s the key evidence. In comments made just nine days ago, the country’s central bank chief indicated she saw no chance of a rate cut any time soon after inflation soared to a five-year high. A week earlier, though, one of Putin’s most vocal economic aides urged the exact opposite, saying a reduction was needed to bolster the ailing economy.

So when the Bank of Russia shocked traders and analysts alike by announcing it was lowering the benchmark rate from an 11-year high, the words spoken by that aide, Andrey Belousov, left many to speculate that the Kremlin is exerting more pressure on central bank policy makers. The rate cut — to 15 percent from 17 percent — triggered a wave of ruble selling that drove the currency down as much as 4 percent, adding to a year-long selloff that’s left it down 50 percent percent [sic] against the dollar.

How ’bout that loonie performance, eh?

Canada’s dollar fell for a 10th week, the longest losing streak since 2000, after a report showing the economy unexpectedly shrank bolstered speculation the central bank will cut interest rates again.

The currency reached the weakest level in almost six years as data showed gross domestic product contracted 0.2 percent in November. Government bonds climbed, pushing yields to record lows. The Bank of Canada reduced borrowing costs last week for the first time since 2009, saying the surprise move was meant to provide insurance as the slump in crude oil, the nation’s biggest export, weighed on the economy.

…

The loonie, as Canada’s dollar is known for the image of the aquatic bird on the C$1 coin, depreciated 0.9 percent to C$1.2732 per U.S. dollar at 5 p.m. in Toronto. It touched C$1.2799, the weakest since March 2009, and sank 2.5 percent on the week. One loonie buys 78.54 U.S. cents.The Canadian currency dropped 8.7 percent since Dec. 31, the fifth consecutive monthly loss and the biggest since October 2008.

…

The yield on Canada’s benchmark 10-year bond sank to as low as 1.246 percent, while two-year yields touched 0.391 percent and 30-year yields reached 1.830 percent, all records.The nation’s largest trade partner expanded less than forecast in the fourth quarter. U.S. GDP grew at an annualized 2.6 percent, the Commerce Department in Washington reported, fanning concern the global slowdown is becoming a drag on the world’s biggest economy. Economists surveyed by Bloomberg had forecast a 3 percent advance after a 5 percent gain from July through September.

The median forecast in a Bloomberg survey for Canada’s monthly GDP was for little change after 0.3 percent growth in October. Instead, it shrank the most in 11 months. The economy grew 1.9 percent in November from a year earlier, versus a forecast of 2.1 percent and an advance of 2.3 percent in October.

Long Canadas at 1.83%. If I had a fifteen year old hat, I’d have to eat it. But honestly, who owns Canadas any more? That’s, like, so 20th century:

With years of income and investing ahead, the Canada Pension Plan Investment Board can afford to own more risky assets such as real estate and stocks, according to Chief Executive Officer Mark Wiseman. Pension contributions will continue to grow through 2022, allowing the fund to reduce its 28 percent holdings in fixed income, he said.

“We’re an 18-year-old investor,” Wiseman, who’s 44, said during an interview Tuesday at Bloomberg’s Toronto office. “The portfolio can afford to have less bonds than it has today.”

…

The 28 percent allocation to bonds and money market securities the CPPIB lists on its website as of March of last year is already below the 29 percent average for private pension plans in Canada, according to data from Towers Watson. In 2000, the Canada Pension Plan was 95 percent invested in fixed income, according to its latest annual report.Caisse CEO Michael Sabia, who oversees the management of pensions in Quebec, said in November that it’s looking to cut its bond holdings to 30 percent from 35 percent. Ontario Teachers’ Pension Plan, the country’s third biggest pension plan, has a 41 percent allocation to fixed income.

Quick! Enact some more regulations to force the banks to buy more! Not that there’s any shortage of buyers now, but there will be, once the tide turns. I’m just waiting for the first big wave of private equity / infrastructure valuation scandals, which I see as being inevitable. Figures can lie and liars can figure. Deal with it.

The politicians will be telling us that economic decline is all oil’s fault, but what are the numbers?

Canada’s economy shrank in November on manufacturing and oil production, pushing the dollar to the weakest in almost six years on speculation the central bank will make another rate cut following last week’s surprise move.

Gross domestic product shrank by 0.2 percent, the most in 11 months, to an annualized C$1.65 trillion ($1.30 trillion), Statistics Canada said Friday in Ottawa. The median forecast in a Bloomberg economist survey was for output to be little changed. Manufacturing declined by 1.9 percent, the most since January 2009, mining and quarrying fell by 2.5 percent, and oil and gas extraction by 0.7 percent.

The IMF recommendations won’t be popular in the halls of power:

Canada’s policy makers should maintain accommodative measures to ensure the economy isn’t sidetracked by the oil shock, the IMF said today in a report.

The Bank of Canada’s decision this month to counter falling oil prices with a rate cut was appropriate, while the federal should consider putting future fiscal tightening on pause once it balances its budget this year to promote growth, the International Monetary Fund said.

Trouble is, the pseudo-conservatives first goosed the economy when it didn’t need it, eliminating the $10-billion surplus. Then there was nothing in reserve when a recession hit. Holy smokes! A recession! Who would have thought they were still possible? And now politics will lead to a tightening – or at least, non-relaxation – in fiscal policy.

I used to be a Conservative. But then my party was taken over by ultra-partisan apparatchiks and sloganeering charlatans.

All over Canada, preferred share investors are telling their buddies about their investments!

Click for Big

About the best thing one can say about the Canadian preferred share market today is that it wasn’t as bad as yesterday! PerpetualDiscounts were off 2bp, FixedResets were down 149bp (bringing their two day loss to a staggering 3.23%) and DeemedRetractibles gained 4bp. ENB and BAM FixedResets are prominent at the extreme bad end of the very length Performance Highlights table – but not much escaped! Volume was high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

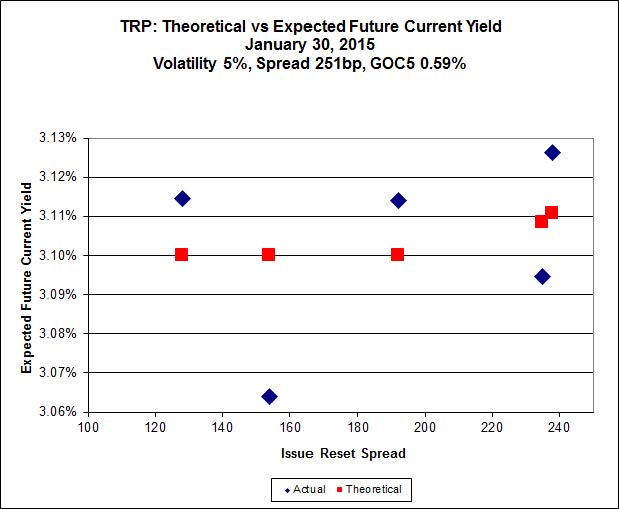

Here’s TRP:

Click for Big

It’s surpising to see that after such a wild day, there is such an excellent fit to theory for the TRP FixedResets!

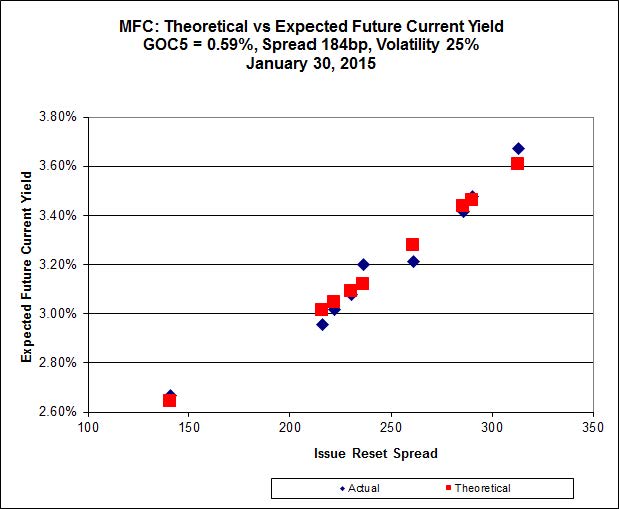

Click for Big

MFC.PR.F is now back on the line defined by its peers; additionally, as a result of today’s big moves in BAM FixedReset prices, Implied Volatility has markedely increased from 20% yesterday.

Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

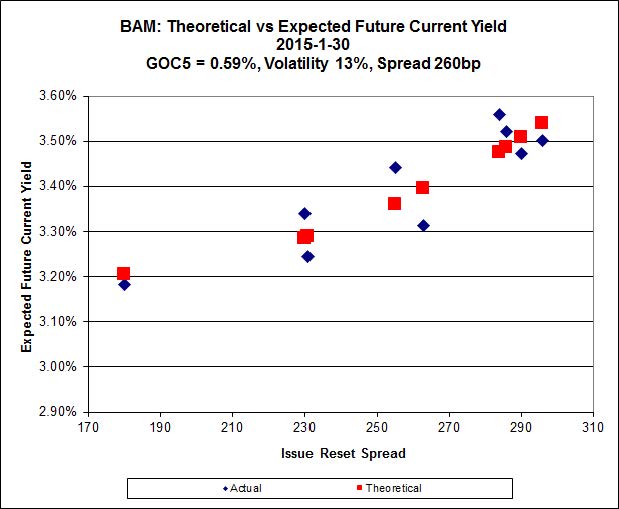

Click for Big

A very strange distinction from the MFC series, because the Implied Volatility for the BAM FixedResets has declined markedly, from 19% yesterday. I would like to think that this means the BAM Implied Volatility will permanently settle to single digits – where I think it should be for true perpetual FixedResets – while MFC Implied Volatility will permanently increase to 40%, where I think it should be for issues with a DeemedRetraction … but I’ll see if this lasts before I start thinking that!

The cheapest issue relative to its peers is now BAM.PF.G, resetting at +284bp on 2020-6-30 (more than five years hence!), bid at 24.10 to be $0.57 cheap. BAM.PF.B, resetting at +263bp 2019-3-31 is bid at 24.30 and appears to be $0.58 rich. With all the fuss over Issue Reset Spreads, it is interesting to see that the relationship between bid and spread is inverted for these two issues.

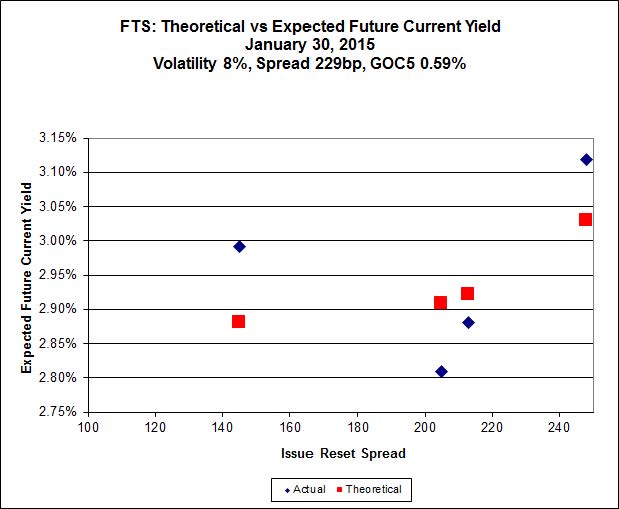

Click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 17.05, looks $0.66 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.50, is still $0.80 expensive after losing $1.71 on the day!

Click for Big

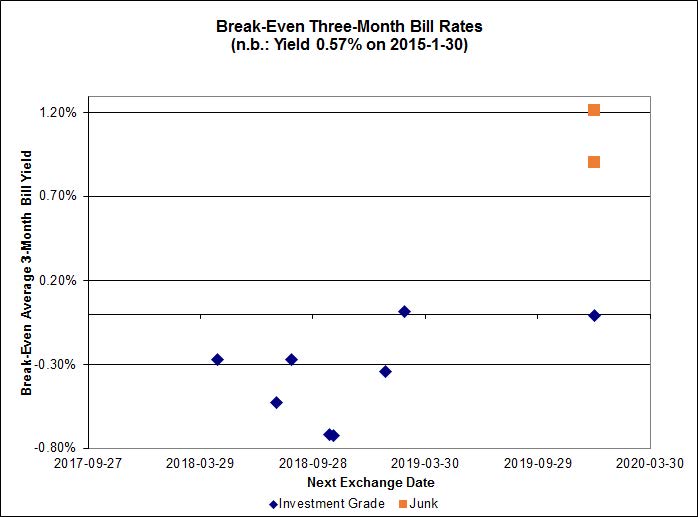

What can I say? Every Investment Grade FixedReset/FloatingReset pair but one (RY.PR.I / RY.PR.K) is now showing a negative break-even average three month bill rate until interconversion … and the exception is showing only a 0.02% breakeven average rate! Meanwhile, the DC.PR.B / DC.PR.D pair (not shown) clocks in at -1.22%, while the other two junk pairs are strongly positive. You guys interpret this, it’s beyond me; but it does show, overall, the market’s extreme distaste for Floating Rate product.

On the other hand, this distaste does not extend to prime, as shown by the FixedFloater/RatchetRate pairs:

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.8601 % | 2,196.0 |

| FixedFloater | 4.42 % | 3.61 % | 19,962 | 18.26 | 1 | -2.4091 % | 3,994.4 |

| Floater | 3.28 % | 3.42 % | 54,328 | 18.68 | 4 | -3.8601 % | 2,334.5 |

| OpRet | 4.05 % | 2.02 % | 98,459 | 0.38 | 1 | -0.0395 % | 2,750.9 |

| SplitShare | 4.29 % | 4.12 % | 32,080 | 3.59 | 5 | 0.0893 % | 3,184.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0395 % | 2,515.4 |

| Perpetual-Premium | 5.42 % | -7.76 % | 56,337 | 0.08 | 19 | 0.1709 % | 2,510.8 |

| Perpetual-Discount | 5.03 % | 4.90 % | 109,890 | 14.97 | 16 | -0.0180 % | 2,755.1 |

| FixedReset | 4.46 % | 3.64 % | 207,362 | 16.73 | 78 | -1.4896 % | 2,393.5 |

| Deemed-Retractible | 4.93 % | 0.59 % | 105,365 | 0.17 | 39 | 0.0365 % | 2,637.5 |

| FloatingReset | 2.57 % | 3.29 % | 75,989 | 6.42 | 7 | -2.2628 % | 2,280.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.X | FixedReset | -6.38 % | Perfectly legitimate. Of the last 25 trades of the day (1:04pm and afterwards), twenty-four were board lots and all these board lots were executed below 19.00. VWAP on the day’s 11,960 shares was 19.08. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 18.77 Evaluated at bid price : 18.77 Bid-YTW : 3.80 % |

| BAM.PR.K | Floater | -6.10 % | Not entirely real. The low for the day was 14.59; a last bid there would have reduced the loss to 2%-odd, but that’s still bad enough! YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 14.00 Evaluated at bid price : 14.00 Bid-YTW : 3.59 % |

| ENB.PR.N | FixedReset | -4.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 4.23 % |

| ENB.PR.B | FixedReset | -4.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 4.17 % |

| ENB.PR.T | FixedReset | -4.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 4.25 % |

| PWF.PR.T | FixedReset | -4.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.85 Evaluated at bid price : 24.00 Bid-YTW : 3.41 % |

| BAM.PR.T | FixedReset | -4.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.10 Evaluated at bid price : 22.35 Bid-YTW : 3.64 % |

| ENB.PR.P | FixedReset | -4.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 20.65 Evaluated at bid price : 20.65 Bid-YTW : 4.22 % |

| FTS.PR.K | FixedReset | -4.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.61 Evaluated at bid price : 23.50 Bid-YTW : 3.22 % |

| MFC.PR.M | FixedReset | -4.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.05 Bid-YTW : 4.60 % |

| PWF.PR.A | Floater | -4.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 2.84 % |

| ENB.PR.Y | FixedReset | -4.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 4.23 % |

| ENB.PR.H | FixedReset | -3.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 19.40 Evaluated at bid price : 19.40 Bid-YTW : 4.06 % |

| TD.PR.Z | FloatingReset | -3.71 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.09 Bid-YTW : 3.41 % |

| SLF.PR.H | FixedReset | -3.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.50 Bid-YTW : 3.90 % |

| BAM.PR.R | FixedReset | -3.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 21.34 Evaluated at bid price : 21.64 Bid-YTW : 3.75 % |

| ENB.PR.F | FixedReset | -3.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 20.70 Evaluated at bid price : 20.70 Bid-YTW : 4.19 % |

| FTS.PR.G | FixedReset | -3.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.71 Evaluated at bid price : 23.61 Bid-YTW : 3.23 % |

| ENB.PF.C | FixedReset | -3.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 21.78 Evaluated at bid price : 22.21 Bid-YTW : 4.17 % |

| BAM.PF.E | FixedReset | -3.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.16 Evaluated at bid price : 22.81 Bid-YTW : 3.94 % |

| ENB.PR.D | FixedReset | -3.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 4.10 % |

| BAM.PF.G | FixedReset | -3.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.80 Evaluated at bid price : 24.10 Bid-YTW : 3.94 % |

| PWF.PR.P | FixedReset | -3.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 18.62 Evaluated at bid price : 18.62 Bid-YTW : 3.33 % |

| BNS.PR.C | FloatingReset | -2.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.58 Bid-YTW : 3.29 % |

| BAM.PR.C | Floater | -2.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 14.60 Evaluated at bid price : 14.60 Bid-YTW : 3.44 % |

| BNS.PR.B | FloatingReset | -2.55 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.29 Bid-YTW : 3.30 % |

| BAM.PR.B | Floater | -2.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 14.67 Evaluated at bid price : 14.67 Bid-YTW : 3.42 % |

| TD.PR.T | FloatingReset | -2.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.30 Bid-YTW : 3.19 % |

| BMO.PR.R | FloatingReset | -2.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.31 Bid-YTW : 3.23 % |

| BAM.PR.G | FixedFloater | -2.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 21.78 Evaluated at bid price : 21.47 Bid-YTW : 3.61 % |

| ENB.PF.E | FixedReset | -2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 21.93 Evaluated at bid price : 22.45 Bid-YTW : 4.15 % |

| ENB.PR.J | FixedReset | -2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 21.99 Evaluated at bid price : 22.45 Bid-YTW : 4.00 % |

| HSE.PR.A | FixedReset | -2.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 17.24 Evaluated at bid price : 17.24 Bid-YTW : 3.83 % |

| ENB.PF.A | FixedReset | -2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 21.92 Evaluated at bid price : 22.40 Bid-YTW : 4.13 % |

| BAM.PF.F | FixedReset | -2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 23.01 Evaluated at bid price : 24.50 Bid-YTW : 3.85 % |

| ENB.PF.G | FixedReset | -2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 21.97 Evaluated at bid price : 22.52 Bid-YTW : 4.16 % |

| MFC.PR.L | FixedReset | -1.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.25 Bid-YTW : 4.34 % |

| MFC.PR.K | FixedReset | -1.85 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.30 Bid-YTW : 4.23 % |

| BMO.PR.Q | FixedReset | -1.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.84 Bid-YTW : 4.49 % |

| MFC.PR.F | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.75 Bid-YTW : 5.93 % |

| MFC.PR.G | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.09 Bid-YTW : 3.86 % |

| CU.PR.C | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 23.35 Evaluated at bid price : 24.60 Bid-YTW : 3.27 % |

| BMO.PR.S | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.98 Evaluated at bid price : 24.35 Bid-YTW : 3.26 % |

| TRP.PR.F | FloatingReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 18.76 Evaluated at bid price : 18.76 Bid-YTW : 3.33 % |

| TRP.PR.E | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.68 Evaluated at bid price : 23.75 Bid-YTW : 3.49 % |

| BMO.PR.W | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.83 Evaluated at bid price : 24.10 Bid-YTW : 3.19 % |

| CM.PR.O | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.98 Evaluated at bid price : 24.40 Bid-YTW : 3.26 % |

| FTS.PR.M | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 23.03 Evaluated at bid price : 24.61 Bid-YTW : 3.44 % |

| MFC.PR.H | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.34 Bid-YTW : 3.99 % |

| PWF.PR.R | Perpetual-Premium | 1.14 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-04-30 Maturity Price : 26.00 Evaluated at bid price : 26.70 Bid-YTW : 4.03 % |

| SLF.PR.B | Deemed-Retractible | 1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.95 Bid-YTW : 4.90 % |

| TRP.PR.C | FixedReset | 1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 17.38 Evaluated at bid price : 17.38 Bid-YTW : 3.48 % |

| GWO.PR.F | Deemed-Retractible | 2.19 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-03-01 Maturity Price : 25.00 Evaluated at bid price : 25.70 Bid-YTW : -20.72 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.J | FixedReset | 1,134,296 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 23.12 Evaluated at bid price : 24.95 Bid-YTW : 3.42 % |

| BNS.PR.Y | FixedReset | 66,503 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.20 Bid-YTW : 4.40 % |

| BMO.PR.Q | FixedReset | 62,196 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.84 Bid-YTW : 4.49 % |

| TRP.PR.D | FixedReset | 57,113 | RBC bought 12,100 from National at 23.26. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 22.72 Evaluated at bid price : 23.75 Bid-YTW : 3.44 % |

| BMO.PR.P | FixedReset | 43,724 | Called for redemption February 25. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.97 Bid-YTW : 3.24 % |

| TD.PF.B | FixedReset | 42,130 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-30 Maturity Price : 23.00 Evaluated at bid price : 24.45 Bid-YTW : 3.17 % |

| There were 48 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.M | FixedReset | Quote: 23.05 – 24.50 Spot Rate : 1.4500 Average : 0.8830 YTW SCENARIO |

| PWF.PR.A | Floater | Quote: 17.50 – 19.00 Spot Rate : 1.5000 Average : 1.1607 YTW SCENARIO |

| HSE.PR.A | FixedReset | Quote: 17.24 – 18.00 Spot Rate : 0.7600 Average : 0.4804 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 23.09 – 23.71 Spot Rate : 0.6200 Average : 0.4027 YTW SCENARIO |

| BNS.PR.Z | FixedReset | Quote: 22.20 – 22.78 Spot Rate : 0.5800 Average : 0.3802 YTW SCENARIO |

| FTS.PR.J | Perpetual-Discount | Quote: 24.41 – 25.09 Spot Rate : 0.6800 Average : 0.4910 YTW SCENARIO |