TransCanada Corporation has announced:

that it will issue 10 million cumulative redeemable first preferred shares, series 11 (the “Series 11 Preferred Shares”) at a price of $25.00 per share for aggregate gross proceeds of $250 million on a bought deal basis to a syndicate of underwriters in Canada co-led by Scotiabank and RBC Capital Markets.

The holders of Series 11 Preferred Shares will be entitled to receive fixed cumulative dividends at an annual rate of $0.95 per share, payable quarterly on the last business day of February, May, August and November, as and when declared by the board of directors of TransCanada. The Series 11 Preferred Shares will yield 3.80 per cent per annum for the initial fixed rate period ending November 30, 2020 with the first dividend payment date scheduled for May 29, 2015. The dividend rate will reset on November 30, 2020 and on the last business day of November in every fifth year thereafter to a rate equal to the sum of the then five-year Government of Canada bond yield plus 2.96 per cent. The Series 11 Preferred Shares are redeemable by TransCanada, at its option, on November 30, 2020 and on the last business day of November in every fifth year thereafter at a price of $25.00 per share plus accrued and unpaid dividends.

The holders of Series 11 Preferred Shares will have the right to convert their shares into cumulative redeemable first preferred shares, series 12 (the “Series 12 Preferred Shares”), subject to certain conditions, on November 30, 2020 and on the last business day of November in every fifth year thereafter. The holders of Series 12 Preferred Shares will be entitled to receive quarterly floating rate cumulative dividends, as and when declared by the board of directors of TransCanada, at an annualized rate equal to the sum of the then 90-day Government of Canada treasury bill rate plus 2.96 per cent.

TransCanada has granted to the underwriters an option, exercisable at any time up to 48 hours prior to the closing of the offering, to purchase up to an additional two million Series 11 Preferred Shares at a price of $25.00 per share.

The anticipated closing date is March 2, 2015. The net proceeds of the offering will be used for general corporate purposes and to reduce short term indebtedness of TransCanada and its affiliates, which short term indebtedness was used to fund TransCanada’s capital program and for general corporate purposes.

Wonder of wonders, this issue actually looks cheap, continuing the brand new tradition set by the announcement of RY.PR.J (which is still cheap according to basic Implied Volatility theory, as far as that goes.

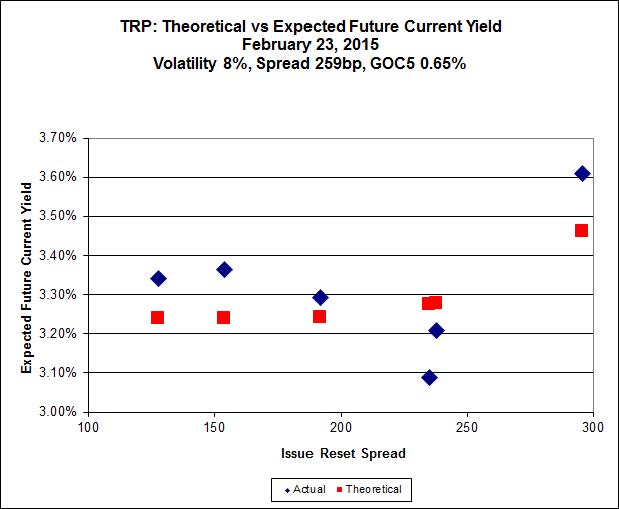

I don’t think this is due to any feelings of generosity amongst the issuers, however. It will be remembered that Implied Volatility theory (in its current stage of development) assumes a constant GOC-5 yield and does not incorporate the current coupon in its calculations (for which it has been harshly criticized).

If instead we look at the single closest comparable, TRP.PR.E, which is a FixedReset 4.25%+235 currently bid at 24.52, we see that it has an Expected Future Current Yield (EFCY) of 3.06%, which is equal to Par Value * (GOC-5 + IRS) / Bid = 25 * (0.65% + 235bp) / 24.52.

If we say that the new issue should have the same EFCY, then its Issue Reset Spread (IRS) should be 3.06% – 0.65% = 241bp. This is 55bp below the actual IRS, implying that the current coupon should also be 55bp below the actual coupon, so we conclude that if it was to trade even-yield with TRP.PR.E, then the new issue should actually carry terms of 3.25%+241. Note that if we were being more precise, the EFCY of the new issue should be a bit more than that of TRP.PR.E, as compensation for the greater negative convexity – call it about 20bp more, which certainly changes the numbers considerably, but not by enough to affect my argument.

The trouble for the issuers is, however, that a current coupon of 3.25% will bring with it a large amount of expected sticker shock for retail. I’m not sure if it would be possible for the underwriters to sell an issue at 3.25%+241 based on current market conditions – or even possible to sell it at 3.45%+261, accounting for negative convexity and volatility. You can be pretty sure they’d try it if they thought they could get away with it!

So what I think is happening is that the issuers are simply selling it based on current coupon and letting the chips fall where they may as far as the Issue Reset Spread is concerned. To a large extent it doesn’t matter much to them – if GOC-5 recovers in the next five years and spreads narrow, then they can just call it and reissue new paper.

This is much the same thing as what the banks did in 2009, with their enormous issuance of FixedResets with huge Issue Reset Spreads.

And all these suppositions break Implied Volatility theory, because – assuming that expectations are met and the market behaves as expected – then there is directionality in market prices and it is entirely possible that capital gains on the currently discounted issues will swamp any differential in coupon. But we will see! Check back in five years.

Still, for what it’s worth, here’s the Implied Volatility Chart for TRP FixedResets, incorporating the new issue at par:

Click for Big

According to this analysis, the new issue would be fairly priced at $26.07.

Unlike most other recent investment grade offerings from “big names”, this one has not yet sold out (3:00 pm on Tuesday). Is this perhaps a sign that the market for new pref issues starting to get saturated?

I think it’s too early to draw any conclusions regarding saturation of the market – these are not just volatile times, but most of the volatility has been downwards in the year to date, so the market is fragile.

I will suggest, however, that the relative sluggishness of sales supports my argument that it would be hard for TRP to sell a new issue with terms of 3.25%+241, no matter how mathematically reasonable the proposition might be.

[…] was issued as a FixedReset, 3.80%+296, that commenced trading 2015-3-2 after being announced 2015-2-23. It reset to 3.351% effective 2020-11-30 and there was no conversion. The issue is tracked by […]