Pembina Pipeline Corporation has announced:

that it has closed its previously announced public offering of cumulative redeemable rate reset class A preferred shares, Series 9 (the “Series 9 Preferred Shares”) for aggregate gross proceeds of $225 million (the “Offering”).

The Offering was announced on March 31, 2015 when Pembina entered into an agreement with a syndicate of underwriters co-led by Scotiabank and RBC Capital Markets. A total of 9,000,000 Series 9 Preferred Shares, which includes 1,000,000 Series 9 Preferred Shares issued pursuant to the partial exercise of the underwriters’ option, were sold under the Offering.

Proceeds from the Offering will be used to reduce indebtedness under the Company’s credit facilities, which indebtedness was incurred in connection with Pembina’s 2015 capital expenditure program.

The Series 9 Preferred Shares will begin trading on the Toronto Stock Exchange today under the symbol PPL.PR.I.

Dividends on the Series 9 Preferred Shares are expected to be $0.2969 quarterly, or $1.1875 per share on an annualized basis, payable on the 1st day of March, June, September and December, as and when declared by the Board of Directors of Pembina, for the initial fixed rate period to but excluding December 1, 2020. The first dividend, if declared, will be payable September 1, 2015, in the amount of $0.4685 per share.

All of Pembina’s dividends are designated “eligible dividends” for Canadian income tax purposes.

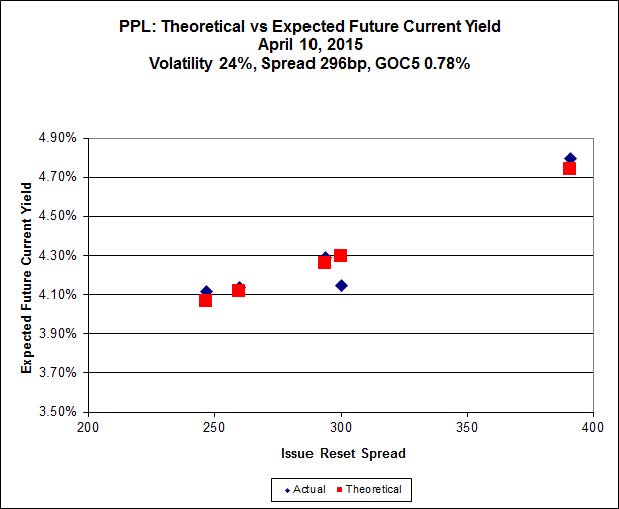

PPL.PR.I is a FixedReset, 4.75%+391, announced March 31. It will be tracked by HIMIPref™ but relegated to the Scraps index on credit concerns.

The issue traded 654,760 shares today (consolidated exchanges) in a range of 24.40-68 before closing at 24.45-50. Vital statistics are:

| PPL.PR.I | FixedReset | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-10 Maturity Price : 22.93 Evaluated at bid price : 24.45 Bid-YTW : 4.75 % |

The price drop of roughly 2% from the issue price as of March 31 isn’t really all that bad – on the month-to-date price-index, TXPR is down 2.41% and TXPL is down 3.46%. Price indices are pretty silly, but they’re available for free and the difference (from total return indices) in April to date is not particularly large.

The calculated level of Implied Volatility has dropped substantially from the 33% calculated at announcement time to a more reasonable but still extremely high 24%. This implies that we should expect Implied Volatility to drop, which implies the calculated curve will flatten, which implies we should expect high-reset issues to outperform low-reset issues over the period.

Click for Big

[…] was issued as a FixedReset, 4.75%+391, that commenced trading 2015-4-10 after being announced 2015-3-31. It reset to 4.302% effective 2020-12-1 and there was no […]