John Heinzl of the Globe penned a paen to FixedResets titled Have rate-reset preferreds hit bottom? Maybe that included some interesting information regarding cash flows:

All three ETFs have been attracting a lot of new money from investors recently. According to a CIBC report, ZPR received inflows of about $34.8-million over the past week – the highest among all Canadian ETFs. CPD was in third spot, with inflows of $26.7-million, and HPR was sixth, with $12.4-million of new funds.

Meanwhile, the recently independent CI Financial has scooped up First Asset:

CI Financial Corp. (TSX: CIX) announced today that it has reached an agreement to acquire 100% ownership of First Asset Capital Corp.

First Asset, which operates through its subsidiary First Asset Investment Management Inc., is a Toronto-based, privately owned investment firm with approximately $3 billion in assets under management. The company is a leader in providing actively managed and factor-based ETFs to the Canadian marketplace, and it also offers a suite of mutual funds and closed-end funds.The transaction, which is subject to regulatory approval, is expected to close by December 31, 2015. Terms were not disclosed.

First Asset is the sponsor of Preferred Share Investment Trust, which has had disappointing performance despite a 28% weighting in corporate bonds (as of September 30).The manager is Aston Hill, which has had its own problems lately as reported on July 20.

Neil Irwin of the NYT has a nice piece on the Phillips Curve:

The idea of the Phillips curve has been under attack almost since William Phillips, the aforementioned New Zealander, wrote his 1958 paper “The Relation Between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861-1957.”

The most crude versions of the Phillips curve have indeed, in recent decades at least, been nearly useless. Any attempt to estimate it requires a researcher to decide what measure of employment to use, what measure of inflation and what time lags to assume, among other choices. So there are nearly as many versions of the Phillips curve as there are researchers who study it.

If you simply look at the unemployment rate in the United States versus the Consumer Price Index, excluding volatile food and energy prices for every year since 1958, there is nearly no statistical relationship at all, just a jumble of dots. (A best-fit line actually points the wrong direction, correlating higher unemployment with higher inflation, albeit very weakly.)

If you take only subsets of that period, the relationship looks stronger. For example, research from the Federal Reserve Bank of Minneapolis shows a fairly clear (negative) correlation between unemployment and inflation from 1977 to 1990, but suggests that relationship basically disappeared in the 1990s and was barely evident in the first decade of the 2000s. But in some ways an ever shifting curve raises more questions than it answers.

And there is another indication of the US higher education scam:

In 2006, Congress extended the federal Direct PLUS Loan program to allow a graduate or professional student to borrow the full amount of tuition, no matter how high, and living expenses. The idea was to give more people access to higher education and thus, in theory, higher lifetime earnings. But broader access doesn’t mean much if degrees lead not to well-paying jobs but to heavy debt burdens. That is all too often the result with PLUS loans.

The consequences of this free flow of federal loans have been entirely predictable: Law schools jacked up tuition and accepted more students, even after the legal job market stalled and shrank in the wake of the recession. For years, law schools were able to obscure the poor market by refusing to publish meaningful employment information about their graduates. But in response to pressure from skeptical lawmakers and unhappy graduates, the schools began sharing the data — and it wasn’t a pretty picture. Forty-three percent of all 2013 law school graduates did not have long-term full-time legal jobs nine months after graduation, and the numbers are only getting worse. In 2012, the average law graduate’s debt was $140,000, 59 percent higher than eight years earlier.

US prosecutors are preparing another sacrifice to the god of Political Expediency:

Prosecutors contend Michael Coscia, the principal of Panther Energy Trading LLC, placed orders he didn’t intend to fill to manipulate prices in a scheme that raked in illegal profits of about $1.4 million over three months. Coscia, indicted last year and charged with six counts of commodities fraud and six of spoofing, claims he had no intent to defraud anyone and didn’t violate the law.

The trial comes after a year of U.S. law enforcement and regulatory actions against traders who authorities allege systematically place orders they don’t intend to execute to trick the market into thinking there’s demand that doesn’t actually exist. It’s the first time jurors are being asked to apply a provision in 2010’s Dodd-Frank Act that singles out spoofing as a form of illegal market manipulation.

…

The government, for its part, wants to bar Coscia from introducing any evidence that shows ambiguity in the law or trading regulations. U.S. District Judge Harry Leinenweber issued a mixed decision on that point, giving the defense some latitude to show Coscia may have been led astray by conflicting rules.The rules may be relevant for Coscia to show that he acted consistently with permitted market behavior and “thus did not reflect intent to defraud or cancel orders prior to execution,” the judge said.

…

If convicted of spoofing, Coscia could face as long as 10 years in prison, plus a fine of as much as $1 million for each count.

…

This type of case is going to present of challenges for the U.S. Attorney’s Office because it’s a complicated market and the conduct doesn’t necessarily appear to be wrongful because traders put in orders and cancel them all the time, said Peter Henning, a law professor at Wayne State University’s Law School in Detroit.The prosecutors have to show intent and “that’s never easy,” Henning said. “If the government loses a couple of these cases it may be that you can’t prove spoofing is a crime,” Henning said. “Even though it’s outlawed you may not be able to prove that spoofing is illegal.”

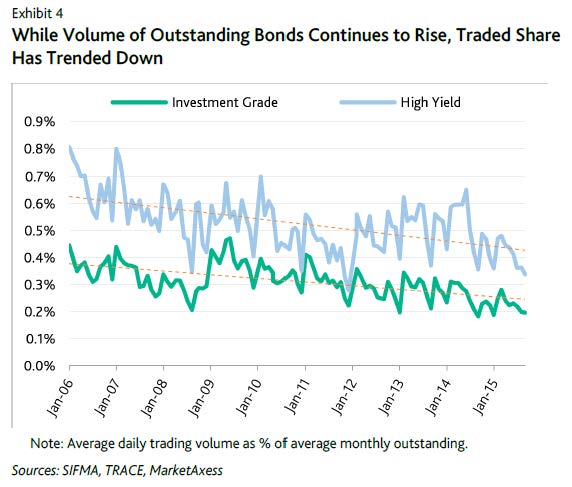

Moody’s has released an interesting report titled Corporate Bond Market Volatility Poses Most Risk for Asset Managers:

Asset managers are most exposed to higher bond market volatility, primarily because they now hold the greatest share of outstanding corporate debt – up to 25% of the total stock in corporate bonds, from just 13% pre-crisis. Should volatility rise sharply, managers could experience fund outflows or reduced fund sales, leading to lower revenues and increasing reputational risks.

…

However, turnover rates – average daily trading volumes relative to outstanding bonds

– have declined over the last decade – falling from around 0.4% of outstanding investment-grade US corporate bonds by volume in 2006 to around 0.2% in September 2015.Further, average trade size has declined, particularly for block trades (those with a value greater than $5 million),1 and market participants have reported a material lengthening of the time needed to ‘offload’ large positions.

…

While asset managers are largely conduits, not ‘storers’, of risk, they are still likely to be most affected by bond market volatility relative to banks and insurance companies. In a protracted market disruption, asset managers could experience fund outflows, or at least reduced fund sales, leading to lower revenues. Further, regulatory focus on asset managers’ liquidity risk management has already increased and could negatively affect the industry. The US Securities and Exchange Commission (SEC) recently voted to propose new liquidity management rules for mutual funds and exchange traded funds (ETFs). These rules include requirements that funds disclose portfolio liquidity and limit illiquid holdings such as certain fixed-income securities. Managers will incur additional costs to comply with the rules, and their funds may underperform their benchmarks owing to the performance drag of carrying more liquid assets.In the US, asset managers’ share of outstanding corporate bond exposures has risen significantly. At the end of June 2015, mutual funds and ETFs held 25% of outstanding US corporate bonds (by volume), up from 13% pre-crisis. Since many pension and etirement funds are also under the purview of asset managers, the investment management industry’s total share of corporate bonds stood at 36% versus 21% pre-crisis). The shares of outstanding bonds held by banks, dealers and finance companies have all declined.

Click for Big

It was a strong day for the Canadian preferred share market, with PerpetualDiscounts up 50bp, FixedResets winning 56bp and DeemedRetractibles gaining 25bp. The lengthy Performance Highlights table is notable for a large number of FixedReset winners. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

Here’s TRP:

Click for Big

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 12.76 to be $0.50 rich, while TRP.PR.A, resetting 2020-12-31 at +192, is $0.50 cheap at its bid price of 15.55.

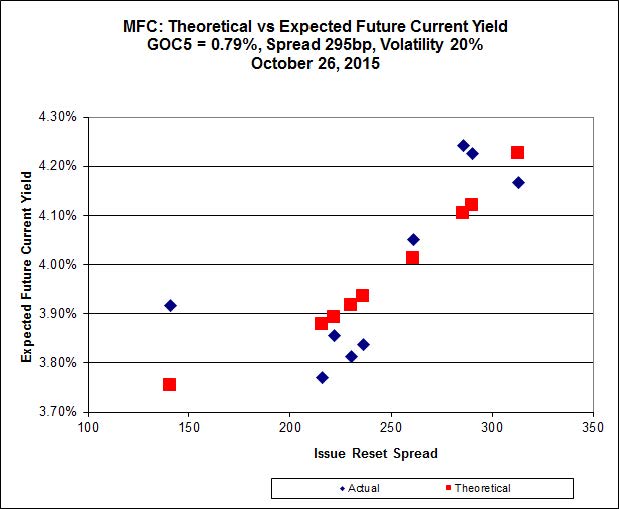

Click for Big

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 19.56 to be 0.54 rich, while MFC.PR.I resetting at +286bp on 2017-9-19, is bid at 21.51 to be 0.73 cheap.

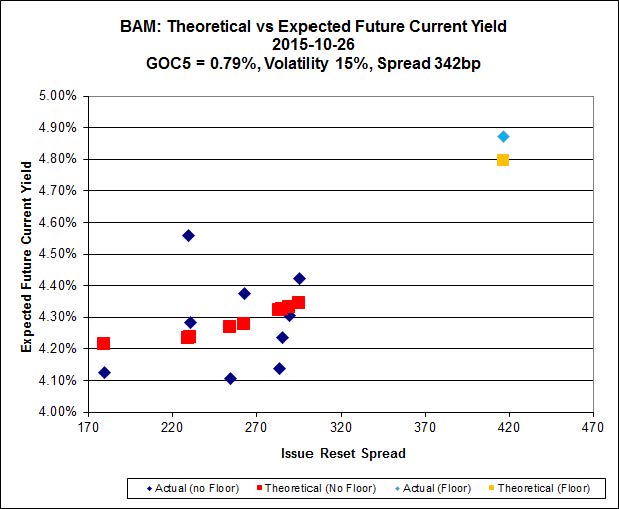

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.95 to be $1.30 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 21.94 and appears to be $0.94 rich.

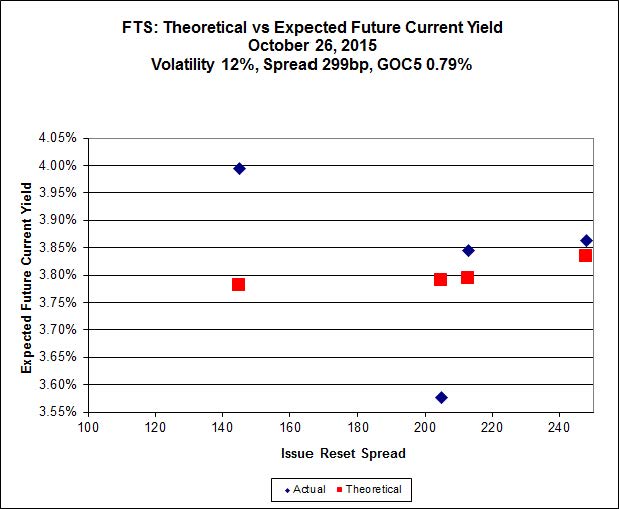

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 19.85, looks $1.12 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 14.02 and is $0.79 cheap.

Click for Big

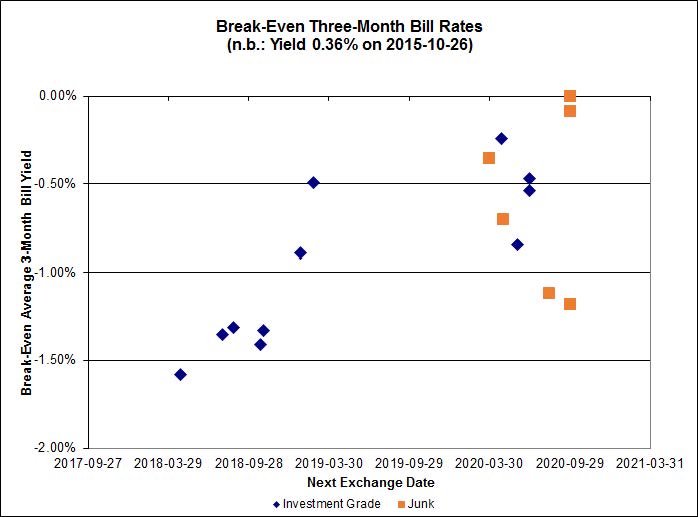

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.87%, with one outlier above 0.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -1.08% and other issues averaging -0.45%. There are two junk outliers above 0.00% and two below -2.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -2.2597 % | 1,700.0 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -2.2597 % | 2,972.3 |

| Floater | 4.37 % | 4.43 % | 60,556 | 16.56 | 3 | -2.2597 % | 1,807.2 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,745.3 |

| SplitShare | 4.37 % | 5.29 % | 81,552 | 2.95 | 5 | 0.0000 % | 3,217.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,510.3 |

| Perpetual-Premium | 5.86 % | 5.81 % | 66,491 | 2.88 | 5 | 0.1761 % | 2,483.2 |

| Perpetual-Discount | 5.63 % | 5.71 % | 79,583 | 14.34 | 33 | 0.4950 % | 2,536.2 |

| FixedReset | 4.89 % | 4.37 % | 211,095 | 15.95 | 76 | 0.5596 % | 2,087.7 |

| Deemed-Retractible | 5.22 % | 4.79 % | 109,116 | 5.46 | 33 | 0.2459 % | 2,560.3 |

| FloatingReset | 2.48 % | 3.98 % | 61,578 | 5.82 | 9 | 0.2140 % | 2,160.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.K | Floater | -2.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 10.70 Evaluated at bid price : 10.70 Bid-YTW : 4.45 % |

| PWF.PR.P | FixedReset | -2.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 14.69 Evaluated at bid price : 14.69 Bid-YTW : 4.12 % |

| BAM.PR.B | Floater | -2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 10.97 Evaluated at bid price : 10.97 Bid-YTW : 4.34 % |

| BAM.PR.C | Floater | -1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 10.77 Evaluated at bid price : 10.77 Bid-YTW : 4.43 % |

| BMO.PR.S | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 19.65 Evaluated at bid price : 19.65 Bid-YTW : 4.26 % |

| PWF.PR.S | Perpetual-Discount | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 21.48 Evaluated at bid price : 21.48 Bid-YTW : 5.62 % |

| BNS.PR.R | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.36 Bid-YTW : 3.77 % |

| HSE.PR.E | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 22.68 Evaluated at bid price : 23.71 Bid-YTW : 4.62 % |

| FTS.PR.G | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 18.99 Evaluated at bid price : 18.99 Bid-YTW : 4.10 % |

| TD.PR.Z | FloatingReset | 1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.33 Bid-YTW : 3.91 % |

| CU.PR.E | Perpetual-Discount | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 21.80 Evaluated at bid price : 22.14 Bid-YTW : 5.61 % |

| BMO.PR.Z | Perpetual-Discount | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 23.66 Evaluated at bid price : 24.00 Bid-YTW : 5.31 % |

| HSE.PR.G | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 22.80 Evaluated at bid price : 24.00 Bid-YTW : 4.54 % |

| HSE.PR.A | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 14.01 Evaluated at bid price : 14.01 Bid-YTW : 4.67 % |

| W.PR.H | Perpetual-Discount | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 23.08 Evaluated at bid price : 23.34 Bid-YTW : 5.93 % |

| MFC.PR.M | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.52 Bid-YTW : 6.18 % |

| MFC.PR.L | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.56 Bid-YTW : 6.65 % |

| GWO.PR.S | Deemed-Retractible | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.28 Bid-YTW : 5.74 % |

| BAM.PR.R | FixedReset | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 16.95 Evaluated at bid price : 16.95 Bid-YTW : 4.73 % |

| SLF.PR.B | Deemed-Retractible | 1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.98 Bid-YTW : 6.66 % |

| BAM.PF.A | FixedReset | 1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 21.42 Evaluated at bid price : 21.42 Bid-YTW : 4.51 % |

| FTS.PR.J | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 21.44 Evaluated at bid price : 21.77 Bid-YTW : 5.53 % |

| TD.PF.F | Perpetual-Discount | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 22.61 Evaluated at bid price : 22.95 Bid-YTW : 5.35 % |

| CU.PR.F | Perpetual-Discount | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 20.59 Evaluated at bid price : 20.59 Bid-YTW : 5.56 % |

| GWO.PR.I | Deemed-Retractible | 1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 6.96 % |

| RY.PR.O | Perpetual-Discount | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 22.67 Evaluated at bid price : 23.01 Bid-YTW : 5.31 % |

| MFC.PR.H | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.52 Bid-YTW : 4.93 % |

| MFC.PR.C | Deemed-Retractible | 1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.70 Bid-YTW : 7.18 % |

| CU.PR.G | Perpetual-Discount | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 20.70 Evaluated at bid price : 20.70 Bid-YTW : 5.53 % |

| GWO.PR.N | FixedReset | 1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.06 Bid-YTW : 9.40 % |

| BAM.PF.G | FixedReset | 1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 21.61 Evaluated at bid price : 21.94 Bid-YTW : 4.41 % |

| BAM.PF.F | FixedReset | 1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 21.27 Evaluated at bid price : 21.55 Bid-YTW : 4.47 % |

| VNR.PR.A | FixedReset | 1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 21.35 Evaluated at bid price : 21.35 Bid-YTW : 4.34 % |

| MFC.PR.N | FixedReset | 1.71 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.26 Bid-YTW : 6.28 % |

| BNS.PR.Y | FixedReset | 1.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.56 Bid-YTW : 5.18 % |

| FTS.PR.K | FixedReset | 1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 3.89 % |

| TRP.PR.G | FixedReset | 1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 21.42 Evaluated at bid price : 21.70 Bid-YTW : 4.39 % |

| FTS.PR.M | FixedReset | 1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 21.16 Evaluated at bid price : 21.16 Bid-YTW : 4.14 % |

| TRP.PR.B | FixedReset | 2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 12.76 Evaluated at bid price : 12.76 Bid-YTW : 4.15 % |

| BAM.PR.N | Perpetual-Discount | 2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 5.78 % |

| SLF.PR.I | FixedReset | 2.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 6.00 % |

| TRP.PR.C | FixedReset | 2.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 13.72 Evaluated at bid price : 13.72 Bid-YTW : 4.30 % |

| BNS.PR.D | FloatingReset | 2.74 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.47 Bid-YTW : 5.55 % |

| IFC.PR.A | FixedReset | 2.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.46 Bid-YTW : 8.54 % |

| BAM.PR.X | FixedReset | 2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 4.47 % |

| BAM.PF.E | FixedReset | 3.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 20.34 Evaluated at bid price : 20.34 Bid-YTW : 4.48 % |

| BNS.PR.Z | FixedReset | 3.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.86 Bid-YTW : 5.43 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PR.T | FixedReset | 69,380 | RBC crossed 56,800 at 18.01. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 4.51 % |

| RY.PR.H | FixedReset | 36,800 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 19.41 Evaluated at bid price : 19.41 Bid-YTW : 4.15 % |

| NA.PR.W | FixedReset | 34,630 | Desjardins crossed 28,100 at 19.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 19.41 Evaluated at bid price : 19.41 Bid-YTW : 4.18 % |

| FTS.PR.K | FixedReset | 32,500 | RBC crossed 15,000 at 19.87. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 3.89 % |

| RY.PR.J | FixedReset | 28,840 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 21.13 Evaluated at bid price : 21.13 Bid-YTW : 4.21 % |

| TD.PF.A | FixedReset | 26,121 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-26 Maturity Price : 19.44 Evaluated at bid price : 19.44 Bid-YTW : 4.15 % |

| There were 34 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BNS.PR.D | FloatingReset | Quote: 19.47 – 20.47 Spot Rate : 1.0000 Average : 0.6244 YTW SCENARIO |

| BNS.PR.Y | FixedReset | Quote: 20.56 – 21.25 Spot Rate : 0.6900 Average : 0.4048 YTW SCENARIO |

| BNS.PR.Z | FixedReset | Quote: 20.86 – 21.50 Spot Rate : 0.6400 Average : 0.3982 YTW SCENARIO |

| GWO.PR.S | Deemed-Retractible | Quote: 24.28 – 24.99 Spot Rate : 0.7100 Average : 0.4713 YTW SCENARIO |

| PWF.PR.P | FixedReset | Quote: 14.69 – 15.24 Spot Rate : 0.5500 Average : 0.3910 YTW SCENARIO |

| CM.PR.Q | FixedReset | Quote: 21.43 – 21.82 Spot Rate : 0.3900 Average : 0.2425 YTW SCENARIO |